On August 23, 2024 , U.S. Federal Reserve Chairman Powell officially announced at the Jackson Hole annual meeting of global central banks that "it is time for policy adjustments. The way forward is clear, and the timing and pace of interest rate cuts will depend on the upcoming information, changing prospects and the balance of risks.”

This also means that the U.S. Federal Reserve's tightening cycle, which has lasted for nearly three years, has reached a turning point. If there are no surprises in the macro data, the first interest rate cut will be held at the interest rate meeting on September 19.

However, entering the early stage of the interest rate cut cycle does not mean that a sharp increase is imminent. There are still some risks that deserve everyone's vigilance. Therefore, the author here summarizes some of the issues that need most attention at present, hoping to help everyone avoid some risks.

In general, in the early stages of interest rate cuts, we still need to pay attention to six core issues, including the risk of recession in the United States, the pace of interest rate cuts, the U.S. Federal Reserve’s QT (quantitative tightening) plan, the risk of rekindling inflation, the efficiency of global central bank linkage and U.S. political risk.

A rate cut does not necessarily mean an immediate rise in risk markets, but in most cases a fall

The U.S. Federal Reserve's monetary policy adjustments have a profound impact on global financial markets.

Especially in the early stages of interest rate cuts, although interest rate cuts are usually seen as measures to stimulate economic growth, they are also accompanied by a series of potential risks, which means that interest rate cuts do not necessarily mean an immediate rise in the risk market. On the contrary, in most cases they will fall. .

The reasons for this can usually be classified as the following:

1. Increased volatility in financial markets

Interest rate cuts are usually considered a signal to support the economy and markets, but in the early stages of interest rate cuts, the market may experience increased uncertainty and volatility. Investors tend to interpret the Fed's actions differently, and some may view rate cuts as reflecting concerns about an economic slowdown. This uncertainty can lead to greater volatility in stock and bond markets.

For example, during the 2001 and 2007-2008 financial crises, the stock market experienced significant declines even as the Federal Reserve began a rate-cutting cycle. This is because investors worry that the severity of the economic slowdown outweighs the positive impact of interest rate cuts.

2. Inflation risk

Cutting interest rates means borrowing costs fall, encouraging consumption and investment. However, if the rate cut is excessive or lasts too long, it could lead to rising inflationary pressures. When abundant liquidity in the economy chases a limited supply of goods and services, price levels can rise quickly, especially if supply chains are constrained or the economy approaches full employment.

Historically, for example, in the late 1970s, the U.S. Federal Reserve's interest rate cuts led to the risk of soaring inflation, which necessitated subsequent more aggressive interest rate hikes to control inflation, triggering an economic recession.

3. Capital outflows and currency devaluation

Interest rate cuts by the U.S. Federal Reserve typically reduce the interest rate advantage of the U.S. dollar, causing capital to flow from the U.S. market to higher-yielding assets in other countries. Such capital outflows would put pressure on the U.S. dollar exchange rate, causing the U.S. dollar to depreciate. Although the depreciation of the US dollar can stimulate exports to a certain extent, it may also bring the risk of imported inflation, especially when raw material and energy prices are high.

In addition, capital outflows may also lead to financial instability in emerging market countries, especially those that rely on U.S. dollar financing.

4. Instability of the financial system

Cutting interest rates is often used to reduce economic stress and support the financial system, but it can also encourage excessive risk-taking. When borrowing costs are low, financial institutions and investors may seek riskier investments to obtain higher returns, leading to the formation of asset price bubbles.

For example, after the technology stock bubble burst in 2001, the U.S. Federal Reserve slashed interest rates to support economic recovery. However, this policy fueled the subsequent bubble in the real estate market to a certain extent, which ultimately led to the outbreak of the financial crisis in 2008.

5. The effectiveness of policy tools is limited

In the early stages of cutting interest rates, if the economy is already close to zero interest rates or in a low interest rate environment, the Fed's policy tools may be limited. Over-reliance on interest rate cuts may not be able to effectively stimulate economic growth, especially when interest rates are close to zero, which requires more unconventional monetary policy measures, such as quantitative easing (QE).

In 2008 and 2020, the Fed had to use other policy tools to respond to economic downturns after cutting interest rates to near zero, suggesting that in extreme cases, the effectiveness of rate cuts is limited.

Let us look at historical data. With the end of the Cold War between the United States and the Soviet Union in the 1990s, and the world entering the political landscape of U.S.-led globalization, until now, the U.S. Federal Reserve's monetary policy response has shown a certain degree of lag. At present, the confrontation between China and the United States is in full swing. The fragmentation of the old order has undoubtedly exacerbated the risk of policy uncertainty.

Take stock of the main risk points in the current market

Next, let us take stock of the main risk points existing in the current market, focusing on the risk of recession in the United States, the pace of interest rate cuts, the US Federal Reserve's QT (quantitative tightening) plan, the risk of rekindling inflation, and the efficiency of global central bank linkage.

Risk 1: Risk of U.S. economic recession

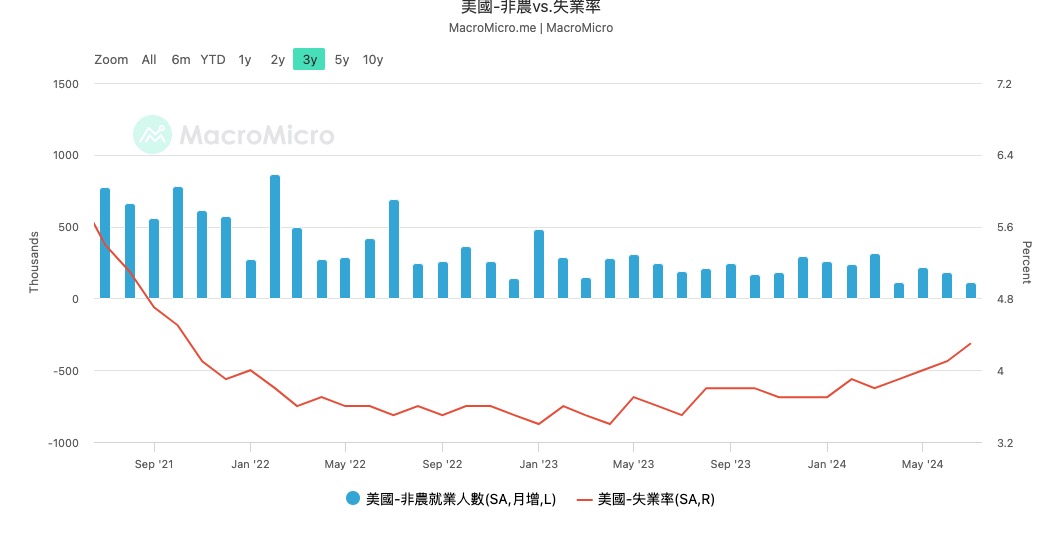

Many people refer to the potential rate cut in September as a "defensive rate cut" by the US Federal Reserve. The so-called defensive interest rate cut refers to an interest rate cut decision made to reduce the risk of potential economic recession when economic data does not deteriorate significantly.

The U.S. unemployment rate has officially reached the "Sam's Rule" warning line for recession. Therefore, it is extremely important to observe whether the interest rate cut in September can curb the rising unemployment rate and thereby stabilize the economy against recession.

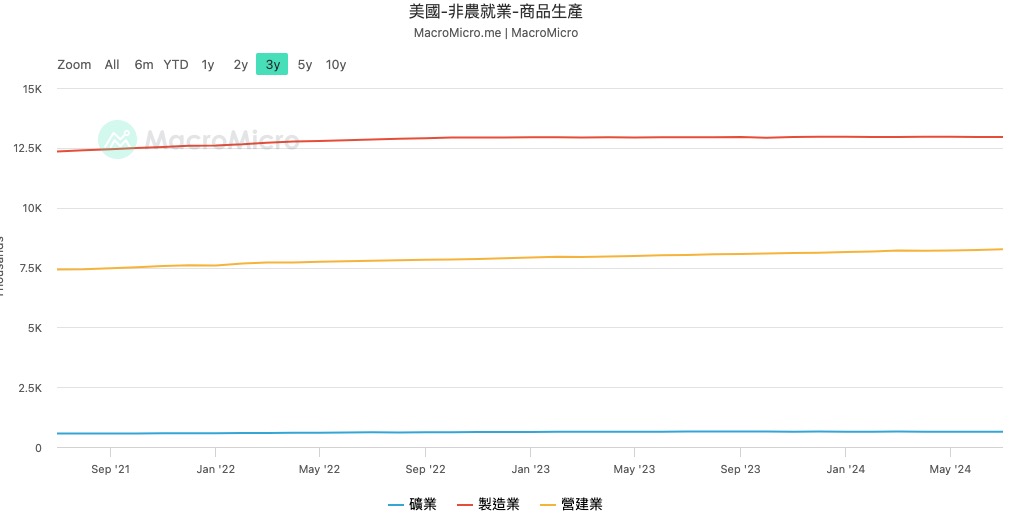

Let us look at the details of non-farm employment data to see what happened specifically. We can see that in the commodity production category, manufacturing employment has experienced low fluctuations for a long time, and the construction industry has contributed more to the data.

For the U.S. economy, high-end manufacturing, as well as its matching technology and financial services industries, are the main driving forces. That is to say, when the income of this high-income elite rises, consumption will increase due to the wealth effect, thereby benefiting Other middle and low-end service industries, so the employment situation of this group of people can be used as a leading indicator of the overall employment situation in the United States.

The weakness in manufacturing employment may present certain trigger risks. In addition, if we look at the U.S. ISM Manufacturing Index (PMI), we can see that the PMI is in a rapid downward trend, which further supports the weakness of the U.S. manufacturing industry.

Next, let’s look at the service industry. The professional technology industry and the retail industry have shown the same frozen situation. The main ones that make positive contributions to the indicators are education, medical care, and leisure and entertainment. I think there are two main reasons. One is that there have been some reversals in the new crown epidemic recently, and affected by the hurricane, there has been a certain degree of difficulty in the related medical rescue personnel. shortage. The second reason is that most Americans are on vacation in July, which has led to the growth of tourism and other leisure and entertainment industries. When the holidays are over, this industry is bound to receive a certain blow.

Therefore, in general, the current recession risk in the United States still exists, so readers need to further observe related risks through macro data, which mainly includes non-farm employment, the number of initial unemployment benefits, PMI, consumer confidence index CCI, housing price index, etc.

Risk 2: The pace of interest rate cuts

The second thing that needs attention is the pace of interest rate cuts. Although it has been confirmed that interest rates have begun to be cut, the speed of interest rate cuts will affect the performance of the risk asset market.

Historically, emergency interest rate cuts by the US Federal Reserve are relatively rare. Therefore, economic fluctuations between interest rate meetings require the market's own interpretation to affect price trends. When certain economic data indicate that the US Federal Reserve will raise interest rates too slowly. At this time, the market will be the first to react, so it is crucial to determine a suitable pace of interest rate cuts and guide the market to implement the Fed's goals through interest rate guidance.

The current market estimate for the September interest rate decision is that there is a nearly 75% probability of a reduction of 25 to 50 BP, and a 25% probability of a reduction of 50 to 75 BP. Therefore, paying close attention to the market's judgment can also clearly judge the market sentiment.

Risk Three: QT Plan

Since the financial turmoil in 2008, the U.S. Federal Reserve has quickly lowered interest rates to 0, but it still has not been able to revive the economy. At that time, monetary policy had become ineffective because it could not continue to cut interest rates, so in order to inject further liquidity into the market, The US Federal Reserve established the quantitative easing (QE) tool to inject liquidity into the market by expanding the US Federal Reserve's balance sheet and at the same time increase the reserve size of the banking system.

This method actually transfers market risks to the US Federal Reserve. Therefore, in order to reduce systemic risks, the US Federal Reserve needs to control the size of the balance sheet through quantitative tightening QT. Avoid disorderly easing that leads to excessive risks for oneself.

Powell's speech did not involve judgment on the current QT plan and subsequent planning, so we still need to pay attention to the QT program and the resulting changes in bank reserves.

Risk 4: Renewed inflation risk

Powell maintained an optimistic attitude towards inflation risks at Friday's meeting. Although it did not reach the expected 2%, he was relatively confident in controlling inflation. Indeed, this judgment can indeed be reflected from the data, and many economists have begun to wonder whether the target inflation rate of 2% is too low after experiencing the baptism of the epidemic.

But there are still some risks here:

- First of all, from a macro perspective, the reindustrialization of the United States is affected by various factors and is not going smoothly. Moreover, it coincides with the anti-globalization policy of the United States in the context of the confrontation between China and the United States. The supply-side problem has not been solved in essence. Any geopolitical risk will exacerbate the resurgence of inflation.

- Secondly, considering that in this round of interest rate hike cycles, the U.S. economy has not entered a substantial recession cycle. As interest rates are cut, the risk asset market will recover. When the wealth effect occurs again, with the expansion of the demand side, services Industrial inflation will also reignite again.

- Finally, there is the problem of data statistics. We know that in order to avoid seasonal factors interfering with the data, CPI and PCE data usually use annual growth rates, that is, year-on-year data to reflect the real situation. Starting from May this year, 2023 High base period factors will be exhausted. At that time, the performance of relevant information will be easily affected by growth.

Risk five: Global central bank linkage efficiency

I think most readers still have fresh memories of the Japan-U.S. carry trade risks in early August. Although the Bank of Japan immediately stepped in to calm the market, we can still see its hawkish stance from Ueda and the Ombudsman's Diet hearings in the past two days. manner. Moreover, during his speech, the yen also showed a significant rise and recovered after officials reassured it again after the hearing.

Of course, in fact, Japan's domestic macro data does require an interest rate increase, but as the core source of global leverage funds for a long time, any interest rate increase by the Bank of Japan will bring great uncertainty to the risk market. Therefore, it is necessary to pay close attention to its policies.

Risk six: U.S. election risk

The last thing that needs to be mentioned is the risk of the U.S. election. As the election approaches, more and more confrontations and uncertain events will occur. Therefore, it is necessary to always pay attention to election-related matters.