1. Macro data update

Economic recession or peak and fall?

In this section, we will introduce some macro-environment related data and what it means to the market.

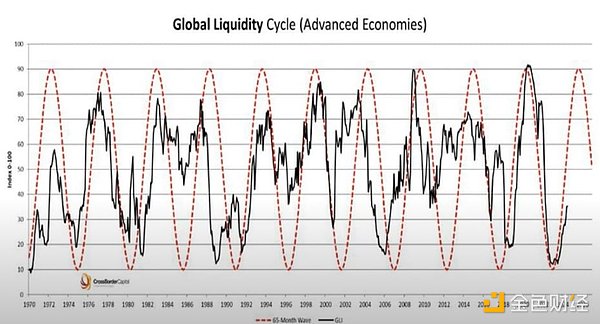

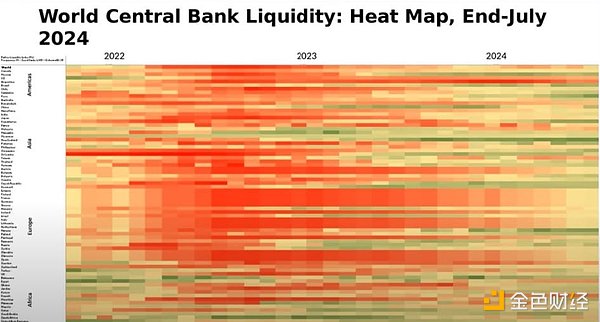

1. Global liquidity

Global liquidity is rising and looks set to continue until the first half of 2025.

Central banks around the world are turning dovish (lower deficits in 2024 = more liquidity).

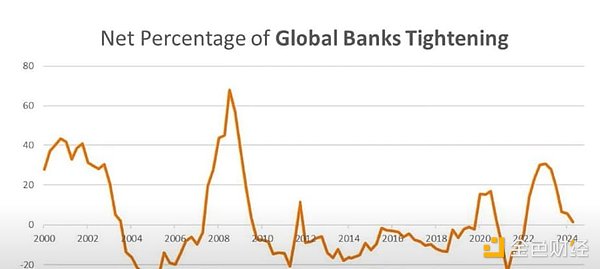

The chart below shows the net share of central banks that are implementing monetary tightening policies:

Bottom Line: Global central banks appear to be engaging in a coordinated easing campaign, with the Federal Reserve expected to cut interest rates in September.

2. Business Cycle

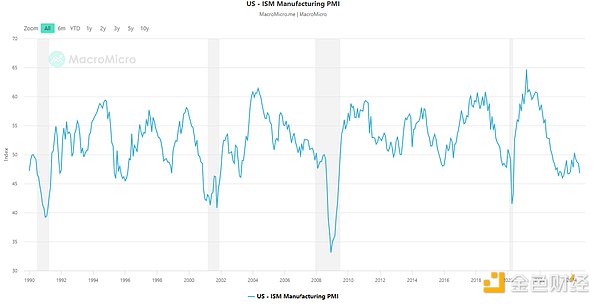

The chart below is the ISM index used to measure manufacturing conditions, such as new orders, production, employment, supplier deliveries and inventory.

This indicator seems to be bottoming out: the business cycle is bottoming out, unemployment is rising (4.3%), and inflation is falling (1.47% according to Truflation).

Summary: A bottom in the ISM index is usually followed by a recession (grey bars in the chart above). However, with the amount of fiscal spending coming from the Treasury, we are not seeing any signs of a recession - a point we will discuss later in this article.

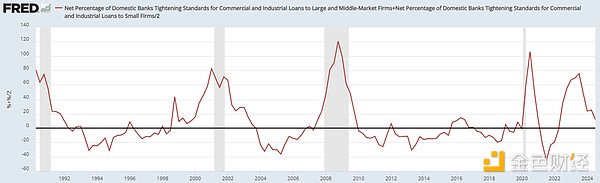

3. Credit Market

Below is the net share of U.S. banks that have tightened their lending standards.

Currently, less than 12% of the banks surveyed are tightening their lending standards, so there is no recession in sight.

The chart below shows credit spreads:

Bottom line: When spreads widen, it indicates that it is becoming increasingly difficult and expensive for risky companies to access credit markets (a sign of stress in the financial system). Likewise, with credit spreads near historic lows, there are no signs of a recession.

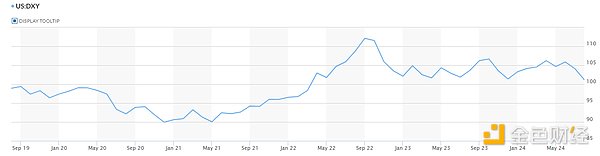

3. US Dollar

After peaking at 112 in October 2022, coinciding with the bottoming of global liquidity, the DXY Dollar Index has now fallen to 101.

As the Fed’s monetary policy shifts, we expect the downward trend to continue and the DXY index to fall to 90-95 by 2025.

Bottom line: Further declines in the dollar could benefit hard assets like Bitcoin and gold. If Bitcoin performs well, we expect Altcoin and the crypto market in general to outperform traditional assets.

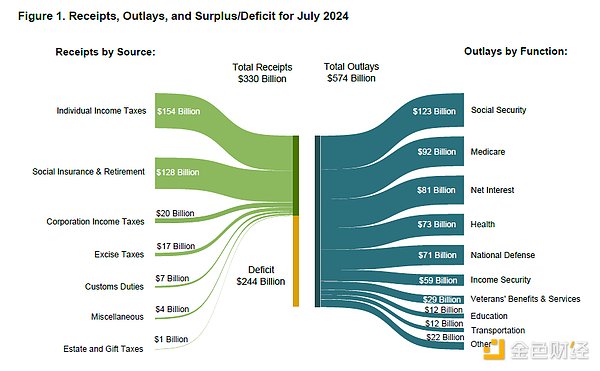

4. Fiscal policy

As mentioned earlier, the federal government continues to spend money it doesn't have, racking up a $244 billion deficit in July alone.

Meanwhile, the projected annual budget deficit recently increased to $1.8 trillion from $1.6 trillion in June.

It's hard for the economy to have a recession when the Treasury is injecting money like this.

5. Forward Guidance from the Federal Reserve

Here are the main points from Federal Reserve Chairman Jerome Powell’s Jackson Hole speech:

Inflation: Powell expressed confidence that inflation has been successfully controlled and the 2% target is within reach.

Unemployment rate: With unemployment rising to 4.3% (3.8% in August 2023), the Fed's focus seems to have shifted from fighting inflation to maintaining a strong labor market. Our guess is that the Fed is closely following the Sahm Rule - a recession is triggered when the 3-month moving average of the unemployment rate rises 0.5% or more from the lowest point in the previous 12 months. The figure was 0.53% in July.

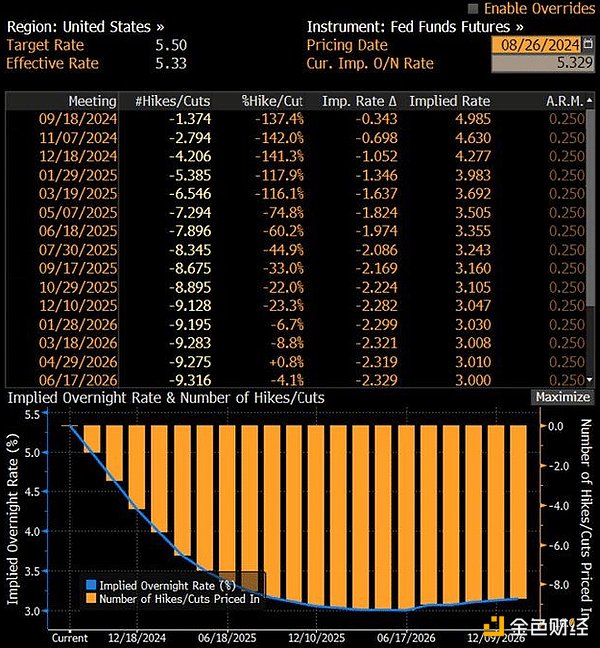

Rate cuts coming: Powell is certain to cut rates in September. Meanwhile, futures markets are pricing in nine rate cuts by the end of 2025, with a final rate of 3%.

Summary: If Bitcoin can trade at $73,000 at a 5.5% Fed Funds rate, what do you think Bitcoin will trade at when rates drop to 3%? We think Bitcoin will go higher, but there will be volatility along the way.

6. Summary

The pundits are out in force these days, but it's hard to see any signs of an impending recession.

What we are seeing are signs of fiscal spending, currency debasement, and increased global liquidity – signs that should be bullish for risk assets like cryptocurrencies as we move into the second half of this year and as we head into 2025.

Now, let’s move on-chain and see what investor behavior can tell us.

2. On-chain data

As always, we use BTC to measure everything that happens on-chain. Why?

Because Bitcoin is still the granddaddy that drives the rest of the crypto market. Until that changes, we intend to use BTC as our reference point.

1. Long-term holders

We see long term holders of Bitcoin, the “smart money”, taking some profits at the end of Q1 and Q2 as the yellow line above turns down. So far, the market has been volatile for about 5 months (including two 20%+ drops and one 30%+ drop).

Over the past few weeks, we have been seeing initial signs that long-term holders have returned to the market as buyers.

Summary: Smart money thinks we are bullish on Bitcoin?

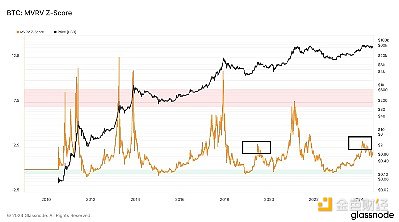

2. MVRV Ratio

In March, Bitcoin’s MVRV (market value to realized value ratio, representing the cost basis market value of all Bitcoins in circulation) reached 3 (moderately overbought).

We hit a similar level in mid-2019 and then readjusted, eventually peaking at 7.5 in '21.

The current MVRV ratio is 1.6, which is neither overbought nor oversold.

Will we see a repeat of 2019, with greater volatility later in the year in the first quarter? Stay tuned, and we’ll share our conclusions in a later story.

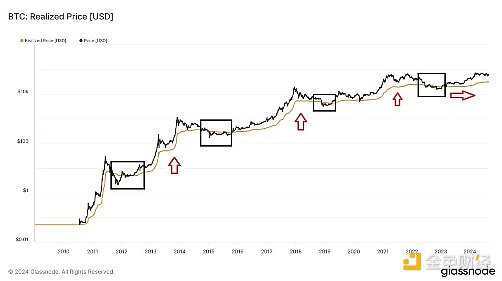

3. Realized Price

The realized price of Bitcoin (the yellow line in the above chart — representing the cost basis per Bitcoin in the network) is currently $31,000. As we can see from the red arrows, the realized price has fluctuated wildly over past cycles:

During the 2017 cycle, realized prices rose by more than 1,000%.

During the 2021 cycle, realized prices have risen by 242%.

In the current cycle, realized prices have risen by only 55%.

The recent 55% move is within the range we saw in 2019, followed by a period of consolidation and ultimately a parabolic move in late 2020 into 2021.

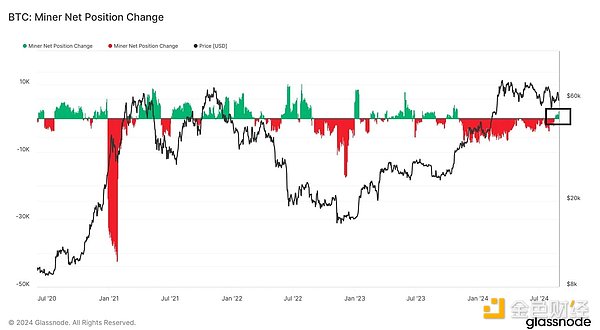

4. Bitcoin Miners

The above chart shows the overall change in the 30-day net position of Bitcoin miners. The green part of the upper part of the chart indicates that for the first time in nearly a year, the BTC accumulation of Bitcoin miners has exceeded their BTC sales. We are closely watching this trend.

Combined with the German government’s sale of $2.5 billion in BTC in July, miners’ shift from net sellers to buyers could stabilize the market and set the stage for the next leg up.

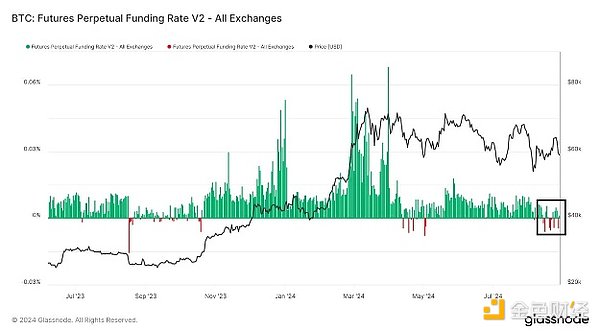

5. Financing rate

Funding rates can give us a sense of market sentiment (and the amount of leverage). As we can see, sentiment peaked at the end of Q1 (funding rates were 6.8%) and has actually turned negative recently.

For reference, financing rates peaked at 16.6% in the 2021 cycle.

Bottom line: While it may seem paradoxical, it is healthy to see such negative sentiment during a bull market. The market cannot go straight up forever. During consolidation, traders experience frequent volatility, become impatient, and eventually turn bearish – creating conditions for a short squeeze.

This is a necessary process, and only after this process is completed can we hope to see the arrival of a bull market.

6. Stablecoins

Total stablecoin balances are now just back to their highs at the end of 2021. We believe this is part of the reason why Bitcoin is having trouble breaking out of its all-time highs.

There is not enough liquidity in the system.

Impending rate cuts and increasing liquidity suggest that stablecoin balances will move to the right of the chart as investors are likely to migrate away from money market accounts (which currently hold nearly $6.5 trillion).

7. Forced Sellers

We should also mention the recent spate of large-scale selling of BTC and ETH by a number of larger entities:

The German government sold $2.5 billion worth of BTC in June and July of this year.

Jump Crypto sold nearly $400 million in ETH in July and August of this year.

To date, Mt. Gox creditors have received about $3 billion, with another $5.8 billion to be distributed (assuming a lot of that was sold, creditors are likely sitting on huge proceeds).

The court approved the distribution of $12.7 billion of FTX to customers on August 9, and all claims of $50,000 or less (98% of claimants) will be paid by October 9.

Of course, in the long run, this is all noise, but we think it is a factor in the consolidation and volatility we have seen this summer. As the selling subsides, a solid foundation may be formed leading to the next bull run.

3. Conclusion

In many ways, the movement we saw in Bitcoin from Q4 last year to Q1 this year ($27,000 to $73,000) is similar to what we saw in 2019 ($4,000 to $14,000). In 2019, crypto native users were very excited and thought we would return to all-time highs. But the reality was that there were no new users entering the crypto space at that time. Ultimately, Bitcoin experienced a full year of consolidation (and recovery from the panic of the new crown epidemic) and finally broke through the all-time high in Q2 2021, reaching $66,000, coinciding with interest rate cuts, currency debasement, and the election cycle.

After BTC firmly broke through its all-time high, we saw an explosion in the number of new users, the emergence of countless DAOs, the rise of DeFi, a 10-fold increase in stablecoin issuance, the explosion of NFTs, and crypto-native users with high confidence and optimism in the cryptocurrency market, showing a "WAGMI" sentiment.

If history repeats itself, the frenzy could emerge later this year and last until 2025.

What are the risks?

Recession? In some sectors of the economy, like commercial real estate, yes. But more broadly, fiscal spending is unlikely to cause a recession.

A Harris victory in November would be a negative for this cycle, but would have little impact in the long run.

More fighting in Europe, Middle East could disrupt markets (again, short-term effects).

Traditional markets are seeing a major correction as the Federal Reserve shifts monetary policy due to concerns about a recession. If this happens, the Fed’s monetary easing and increased global liquidity will ultimately boost the market in the long run.

We will continue to monitor the data and will be sure to let you know if we turn bearish.