Author | DigiFT

Abstract

• Introduction: On March 20, 2024, the renowned asset management firm BlackRock, in collaboration with the US tokenization platform Securitize, issued the tokenized fund BUIDL (BlackRock USD Institutional Digital Liquidity Fund), further expanding its influence in the Web3 domain. This move closely followed the approval of its Bitcoin spot ETF, marking a significant milestone in mainstream cryptocurrency investment. The tokenized fund BUIDL represents traditional institutions leveraging public blockchain technology to enhance operational and capital efficiency, foreshadowing the broader adoption of blockchain technology.

• Problems Solved by Tokenized Funds: Traditional open-ended funds, such as money market funds, involve multiple institutions, leading to inefficiency and high costs due to independent databases. As tokens issued on public blockchains, tokenized funds eliminate the need for centralized registries, reducing costs by providing real-time, traceable transaction records. They enable real-time atomic settlement and secondary market trading, improving capital utilization and offering higher returns. Tokenized funds also support various applications through smart contracts, such as staking and lending.

• Mainstream Institutions Entering the Public Chain: The DeFi space has demonstrated the advantages of blockchain, but the transfer of traditional financial capital to Web3 faces significant hurdles. Fund tokens with KYC and AML compliant whitelists showcase the efforts of mainstream institutions to explore DeFi. Examples include Franklin Templeton's FOBXX and WisdomTree's WTSYX, which initially used blockchain for auxiliary accounting. BlackRock's BUIDL, by using the public blockchain as the primary accounting tool and collaborating with Securitize as the regulated transfer agent, marks a breakthrough.

• BUIDL's Design and Performance: BUIDL is issued as an ERC20 token on Ethereum, supporting real-time on-chain transfers within the whitelist. It enables interactions with smart contracts and provides real-time USDC redemption through Circle. As of July 9, 2024, BUIDL's AUM reached $502.8 million, held by 17 addresses, including significant participation from institutions like Ondo Finance. BUIDL facilitates the integration of DeFi, channeling stable real-world returns into the DeFi ecosystem.

• Challenges and Future Outlook: Despite its success, BUIDL faces significant regulatory and compliance challenges. The tokenization of assets faces conservative regulations globally, limiting issuance to qualified investors. However, the initiatives of BlackRock and Franklin Templeton are drawing attention to the efficiency of on-chain interactions and driving the development of new laws and standards.

On March 20, 2024, the asset management giant BlackRock, following the issuance of its Bitcoin spot ETF, further expanded its presence in Web3 by collaborating with the US-based tokenization platform Securitize to launch the tokenized fund BUIDL (BlackRock USD Institutional Digital Liquidity Fund). If the approval of the Bitcoin spot ETF recognized cryptocurrencies as a new asset class and incorporated them into the investment universe of compliant funds, the greater significance of the tokenized fund lies in traditional institutions attempting to use the public blockchain as the underlying technology to enhance operational and capital efficiency, signifying the recognition and adoption of blockchain technology.

What problems can tokenized funds solve compared to traditional funds?

The funds that investors are widely exposed to are typically open-ended funds, which are subject to strict regulations due to their low entry barriers, broad coverage, and large fund sizes. Taking money market funds as an example, the operation of such funds typically involves the coordination of multiple institutions, with each institution responsible for a part of the fund's underlying processes. This specialization in operations aims to improve efficiency and prevent the concentration of power in a single entity. The full process from start to finish generally includes: fund distribution channels (banks, brokerages, financial advisors), fund administration, transfer agency, fund auditing, fund custody, exchanges, and so on.

However, the inconsistency of databases among these entities has resulted in significant friction and costs. Typically, each subscription and redemption of a fund involves the various institutions along this chain. Order information is transmitted through manual or automated means, and funds are settled through the settlement system, often taking several days to complete a single fund subscription.

Through fund tokenization, fund shares are issued and traded in the form of tokens on the public blockchain. Shares are directly held in the investors' wallets as tokens, and the share and net asset value can be publicly viewed on the blockchain. All transaction records are accessible and queryable on the blockchain, recorded in real-time and automatically, eliminating the need for centralized registries and the associated costs of reconciliation among multiple parties.

After tokenization, the distribution platform can use smart contracts to achieve real-time atomic settlement between the fund share tokens and payment tokens (such as various stablecoins), reducing the waiting time for investors. If the fund tokens achieve a secondary market on the blockchain, investors can directly enter and exit the market in real-time, which can reduce the redundant cash holdings required to meet redemptions, thereby improving the fund's capital utilization efficiency and generating higher returns. Investors can also enjoy a more efficient trading experience through the real-time settlement of the secondary market, avoiding the waiting period for subscriptions and redemptions.

Furthermore, tokenized funds can be combined with more application scenarios, such as supporting staking and lending through smart contracts, to meet a wider range of user needs.

Institutional Forays into the Public Chain - From Auxiliary Tool to Primary Ledger

The DeFi space has fully demonstrated the advantages of blockchain, but the transfer of the vast traditional financial capital from the Web2 system to the new Web3 technology-based system faces significant hurdles that require gradual progress and the exploration of new practical solutions.

Due to compliance requirements, especially KYC and AML, fund tokens, unlike the cryptocurrencies we commonly see, often have a whitelist mechanism, where each whitelisted address corresponds to a user who has completed KYC through the fund platform. Transactions from non-whitelisted addresses cannot be executed. Issues such as transfer risks, fund loss risks, and transaction monitoring that arise from the free transfer function between addresses will be difficult to overcome until effective risk control solutions are in place.

However, we note that mainstream asset management institutions are also exploring the DeFi field, attempting to reform their products by incorporating the characteristics of blockchain technology. We can see the evolution of their product designs.

In 2021, the US asset management giant Franklin Templeton issued the tokenized fund Franklin Onchain U.S. Government Money Fund - FOBXX. In the initial design, the tokens were actually maintained in the official records of the transfer agent's private database system, with secondary records on Stella and Polygon. If there were conflicts between the centralized and public blockchain records, the centralized records would take precedence. Investors traded the fund share tokens through Franklin's app, with each user assigned a blockchain address, but investors could not transfer the tokens in their wallets.

In 2022, WisdomTree also issued a similar tokenized fund WTSYX, investing in short-term US Treasuries, on the Stella blockchain.

The designs of FOBXX and WTSYX effectively only used the blockchain as an auxiliary accounting tool, making the share records public, without actually gaining the real benefits.

In March 2024, BlackRock's BlackRock USD Institutional Digital Liquidity Fund (BUIDL), issued through the tokenization platform Securitize, represented a significant breakthrough, partly because Securitize, as a regulated transfer agent, was able to use the public blockchain as the primary accounting tool to record the ownership and changes of the issued assets.

Delving into BUIDL's Design - Obstacles and Improvements

According to the BUIDL issuance documents, the basic information is as follows:

Issuer: BlackRock USD Institutional Digital Liquidity Fund Ltd. (BlackRock's BVI entity, established in 2023)

Registration Exemption: SEC Reg D Rule 506(c), Section 3(c)(7) (Reg D is an exemption clause for securities issuance, allowing fundraising from accredited investors without limits on the number of investors or the fundraising amount)

Security Type: Pooled investment fund

Investment Threshold: Qualified Purchaser

Minimum Investment: $5 million USD for individual investors; $25 million USD for institutional investors

Issuance Size and Investor Scale: No cap

The only distribution channel at the time of issuance is Securitize Markets, LLC, which is an SEC-registered securities broker. In addition, Securitize, LLC, a related entity of Securitize, is an SEC-registered transfer agent and can register and record the ownership of securities on the blockchain.

It is worth noting that the issuance of this fund used a newly registered BVI entity of BlackRock, rather than its regular fund issuance entity, which may be due to risk considerations in order to avoid impact on the compliant entity. In addition, the four relevant persons mentioned in the SEC registration document are Ian Pilgrim in Bermuda, Jennifer Collins in the Cayman Islands, W. William Woods in Canada, and Noëlle L'Heureux in California, USA. Only Noëlle L'Heureux is a Managing Director at BlackRock, having worked there for 32 years. The other three are likely from third-party institutions.

BUIDL Product Design

Trading Currency: USD and USDC

Subscription and Redemption: Daily subscription and redemption

Strategy: Primarily investing in short-term government bonds

Net Asset Value: 1 BUIDL = 1 USD

Token Standard: A specially designed ERC20 with a whitelist mechanism, where tokens can only circulate within the whitelist addresses, and transfers and transactions to non-whitelist addresses will fail.

Earnings Calculation: Earnings are recorded based on the number of shares held at 3:00 PM Eastern Time on each business day, and distributed through the issuance and airdrop of BUIDL tokens on the first business day of each month.

Redemption Rules: Daily redemption, where redemption is based on the number of BUIDL tokens held at a rate of 1 BUIDL = 1 USD; direct redemption through Securitize requires sending the tokens to a designated address, after which the BUIDL tokens are burned and the USD redemption is completed offline, generally T+0. Accumulated earnings between the last distribution and the redemption request need to be redeemed through a "full redemption" process, which is completed 2-3 business days after the interest distribution (on the first business day of each month).

BUIDL is an ERC20 token issued on the Ethereum blockchain, which allows free circulation within the whitelist and can also enter whitelisted smart contracts, while interactions with non-whitelist addresses will fail. For DeFi users, this is a simple step, but a major breakthrough in traditional finance, as it means that large institutions are beginning to recognize public chains as accounting tools to register asset ownership transfers and changes, and the associated rights and interests will also be recorded on the public chain, enjoying its characteristics of openness, transparency, efficiency, and traceability.

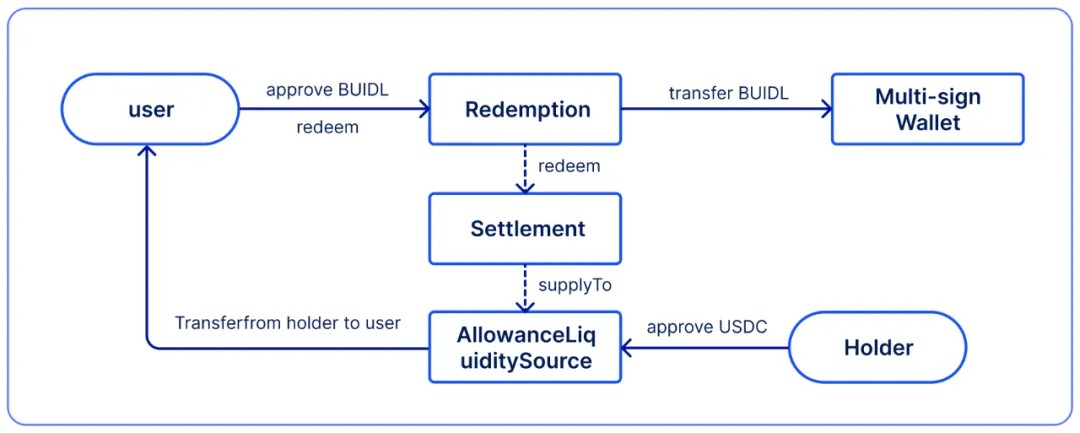

By opening up the transfer function, BUIDL enjoys the advantages of the blockchain settlement system to a certain extent. One use case is provided by Circle, which, after the launch of BUIDL, released a contract that allows real-time BUIDL to USDC conversion, and prepared a 100 million USDC redemption reserve to provide BUIDL holders with the option of real-time 1 BUIDL = 1 USDC redemption.

This redemption option is provided by Circle, which is essentially an OTC transaction: Circle provides the conversion contract (the Redemption address in the figure), and the user transfers funds to the conversion contract, triggering the contract to transfer the USDC from another EOA account (the holder address in the figure) to the user's address, all of which are on-chain transactions with atomic settlement.

Figure 1: Flowchart of the USDC redemption contract provided by Circle for BUIDL

At the time of establishment, this EOA account had a balance of 100 million USDC. Here, since the daily interest on the BUIDL token is realized through centralized accounting, if USDC is exchanged through the Circle contract, it is a transfer from the issuer BlackRock's perspective, so the interest recorded daily between the last distribution and the transfer will still be distributed at the next distribution time. After the BUIDL exchange, Circle will hold the BUIDL, and the subsequent operations will be decided by Circle. From the current on-chain information, Circle will periodically redeem BUIDL through Securitize to exchange for USD, and then mint USDC and replenish the liquidity pool.

What is the current status of BUIDL three months after its launch?

On May 15, 2024, BUIDL's AUM (Asset Under Management) exceeded Franklin Templeton's tokenized government bond fund FOBXX, becoming the largest tokenized fund project. As of October 17, 2024, the total AUM reached $557 million. However, compared to the trillions of dollars in the traditional market, the overall tokenized government bond fund market is only $2.35 billion, leaving a lot of room for growth. (Data source: RWA.XYZ, October 17, 2024)

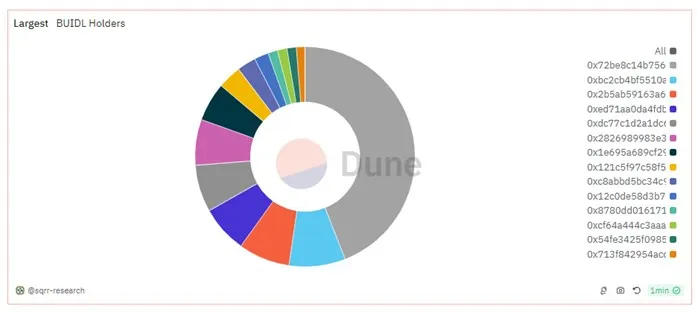

Currently, BUIDL is held by 27 addresses, with the following distribution:

Figure 2: Distribution of BlackRock BUIDL token holders (data as of October 17, 2024)

Securitize allows each client to bind up to 10 on-chain whitelist addresses. Among the 27 addresses above, 2 belong to Ondo Finance, the largest holder, with a total of 216 million BUIDL, worth $216 million. The two addresses are 0x72, holding about 164 million BUIDL, and 0x28, holding 51 million BUIDL, which are the underlying assets of Ondo Finance's tokenized government bond fund product OUSG (AUM $216 million). Previously, the underlying assets were BlackRock iShares' short-term government bond ETF, which was entirely converted to BUIDL after its issuance. Currently, the redemption of OUSG is realized through Circle's redemption contract for real-time USDC redemption.

In addition, as BUIDL collaborates with several crypto custodians, multiple on-chain addresses appear as EOA addresses without historical transaction records, or are accounts of traditional institutions invited by BlackRock and Securitize to try tokenizing funds and holding them in these custodian accounts.

The USDC redemption pool provided by Circle currently has a balance of 80.03 million USDC, with Ondo Finance being the main redeemer. The Circle address (0xcf) also holds about 19.96 million BUIDL.

Figure 3: USDC balance held by the BUIDL USDC redemption contract (data as of October 17, 2024).

The DeFi Journey of Financial Institutions

Due to the investment threshold set for BUIDL, ordinary users find it difficult to obtain BUIDL directly. However, by issuing a money market fund with stable returns and secure assets on the chain, BlackRock allows other institutions to introduce stable real-world returns into the DeFi world by using BUIDL as the underlying asset.

A typical example is Ondo Finance. As mentioned earlier, Ondo is the largest holder of BUIDL, and through BUIDL and the redemption contract provided by Circle, Ondo Finance has realized the rapid subscription and redemption of its money market fund product OUSG through USDC, while also lowering the user access threshold from $5 million to $5,000. Ondo can also collaborate with other DeFi protocols to further pass on the returns to the DeFi world, such as through DeFi lending platforms like Flux Finance, allowing anonymous DeFi users to also access real-world returns. This layered structure can channel the real-world returns provided by traditional large institutions into the DeFi world.

Full-scale Institutional Entry? Facing Numerous Obstacles

Products like BUIDL, through the on-chain and off-chain integrated design, have improved the liquidity management efficiency of money market funds and provided a channel for on-chain investors to access real-world returns. BlackRock, through fund tokenization, and in collaboration with Web3 institutions such as Securitize, Circle, and Ondo Finance, has enabled Web3 institutions to obtain real-world returns in the form of on-chain tokens, avoiding complex deposit and withdrawal processes, and increasing interoperability and improving capital efficiency through smart contracts.

In fact, what BUIDL has done here is to allow tokens to be transferred on-chain without going through centralized institutions. The simple transfer function actually has very high compliance and legal costs behind it. On traditional financial platforms, it is very difficult to transfer between different accounts, and even the same named account is very difficult. Financial institutions generally only allow transactions, subscriptions, and redemptions on the platform. One month after BlackRock implemented the transfer function, Franklin Templeton's FOBXX also realized this function, indicating the institution's recognition of the public chain as a ledger, which is also a breakthrough at the product level. (The difference is that FOBXX holders do not have control over the address private keys, so they can only transfer within the platform and cannot truly operate on-chain).

From the regulatory perspective on asset tokenization across different countries and regions, the current regulation tends to be conservative: the United States has no clear legislation, so asset issuers can only rely on various exemption clauses, and BlackRock also issues through the establishment of a BVI SPV to avoid affecting its compliant entity. In other regions, such as Singapore, asset tokens have whitelist restrictions and can only be offered to accredited investors. These various restrictions and uncertainties hinder users and institutions from further entering the Web3 domain. On the optimistic side, the deep exploration of tokenization by institutions like BlackRock and Franklin Templeton has greatly attracted the attention of the financial industry, demonstrating the high efficiency of on-chain interactions through real-world cases, while also driving regulatory progress to facilitate the development of new laws and standards.