Original author: Robbie Petersen, Delphi Digital researcher

Original compilation: Luffy, Foresight News

Looking back on the history of cryptocurrency development, value capture in the blockchain stack has always been a topic of great interest. The core debate has always centered on the protocol layer and the application layer, but there is a third layer in the stack that most people have overlooked: the wallet.

The "fat wallet" theory holds that as protocols and applications become "leaner", whoever owns the two most valuable resources - distribution and order flow - will capture the most value. And as the ultimate front-end, no one is better positioned than the wallet to monetize this value.

This article will explore the "fat wallet" theory in three steps. First, we will outline three structural trends that will continue to drive the commoditization of the protocol layer and the application layer. Second, we will explore the various ways wallets can be profitable, including payment for order flow (PFOF) and application distribution services (DaaS). Finally, we will discuss why Jupiter and Infinex may outcompete wallets in the battle for user attention.

Protocols and Applications Becoming Leaner

The question of where value will ultimately accrue in the blockchain stack can be simplified into a simple framework. For each corresponding layer of the stack, ask yourself the following question:

If this layer raises its fees, will users leave and choose a cheaper alternative?

In simple terms, if Arbitrum raises its fees, will users switch to using other protocols like Base, and vice versa? Similarly, at the application layer, if dYdX raises its fees, will users switch to using another undifferentiated perpetual DEX.

Based on this logic, we can identify where the highest switching costs are, and thus determine who has strong pricing power. Conversely, we can use this framework to identify where switching costs are lowest, and thus determine which layer of the stack will become increasingly commoditized over time.

While historically protocols have had strong pricing power, I believe this is changing. Today, there are three structural trends that are increasingly "weakening" the protocol layer:

Multi-chain applications and chain abstraction: As applications deploy across multiple chains to remain competitive, cross-blockchain user experiences will become increasingly indistinguishable, in turn driving down switching costs between chains. Furthermore, chain abstraction through cross-chain bridges will further compress switching costs. As a result, applications will no longer be beholden to the network effects of a single chain, and instead chains will become increasingly beholden to the traffic distribution of applications.

Maturation of the MEV supply chain: While MEV will never be fully eliminated, there are many initiatives, both at the application layer and closer to the base layer, to redistribute the MEV extracted from users. Importantly, as the MEV supply chain matures, value will accrue increasingly to the MEV supply chain, and then be captured by applications with the most exclusive user order flow. This means protocols will lose bargaining power, while the position of the front-end and wallets will rise.

Rise of the proxy paradigm: In a world where transactions are primarily executed by proxies and "solvers" rather than humans, attracting this proxy flow will become a necessary condition for blockchain survival. Importantly, given that proxies and "solvers" are programmed to optimize for best execution, protocols will no longer compete around intangible assets like "decentralization". Instead, transaction fees and liquidity will be paramount, which will only further "weaken" the protocol layer as protocols are forced to compress fees and incentivize liquidity to remain competitive.

Revisiting our initial question then: if a protocol raises its fees, will users leave it for a cheaper alternative? While this may not be obvious today, I believe that as switching costs continue to compress, the answer for an increasing number of protocols will be: YES.

Source: dune analytics @0x Kofi

Intuitively, one might think that if protocols are weakened, applications must necessarily become stronger. While applications will certainly recapture some of the value, the "fat application" theory itself is an oversimplification. The way value accrues to different vertical applications varies, and the question is not "will applications become fatter?", but "which applications?".

As I mentioned in "A New Framework for Crypto Market Moats", the unique structural differences of crypto applications (forkability, composability, and token-based value capture) can lower the barriers to entry and costs for emerging competitors. Therefore, while a few applications may have some attributes that cannot be easily replicated, as crypto applications, cultivating moats and maintaining market share is extremely difficult.

Revisiting our initial framework again: if an application raises its fees, will users switch to a cheaper alternative? I believe 99% of applications will face this issue. As such, I expect most applications will struggle to capture value, as turning on the fee switch will inevitably lead to users migrating to the next undifferentiated application offering more generous incentives.

Finally, I believe the rise of AI agents and solvers will have a similar impact on applications as it does on protocols. Given that agents and "solvers" are primarily optimizing for execution quality, I expect applications will also be forced to compete fiercely to attract agent flow. While in the long run, liquidity network effects should lead to a winner-take-all dynamic, in the short to medium term, I expect applications to experience a race to the bottom.

This then begs the question, if both protocols and applications are continually weakened, where will value re-aggregate?

The "Fat Wallet" Theory

The simplest answer is: whoever owns the end-user wins. While in theory this could be any front-end, including applications, the "fat wallet" theory posits that no one is better positioned than the wallet to be closest to the user.

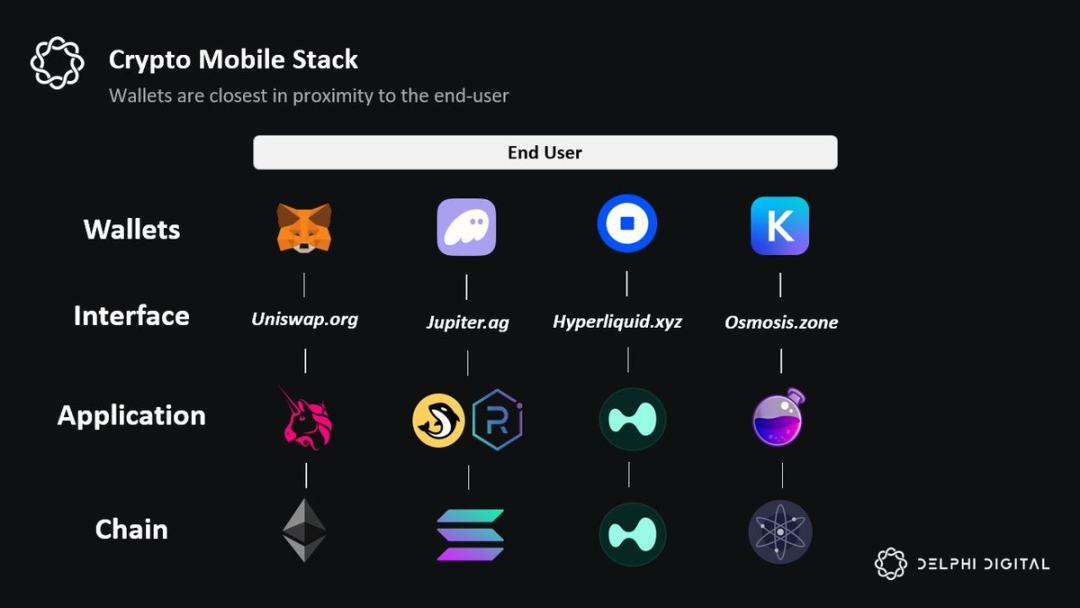

Wallets dominate the mobile crypto user experience: To understand who owns the end-user in the mobile web, the best litmus test is to ask: which Web2 app does the user ultimately interact with? While most users "interact" with the Uniswap front-end to make trades, they still access this front-end through a wallet application. This means that if mobile devices come to dominate the crypto user experience, wallets will only strengthen their connection to the end-user.

Wallets are where the users are: Crypto applications are fundamentally financial in nature. Unlike Web2, nearly every on-chain transaction is some form of financial transaction. As such, the account layer is critical for crypto users. Furthermore, there are unique wallet layer functionalities: payments, native yield on idle user balances, automated portfolio management, and other consumer use cases like crypto debit cards.

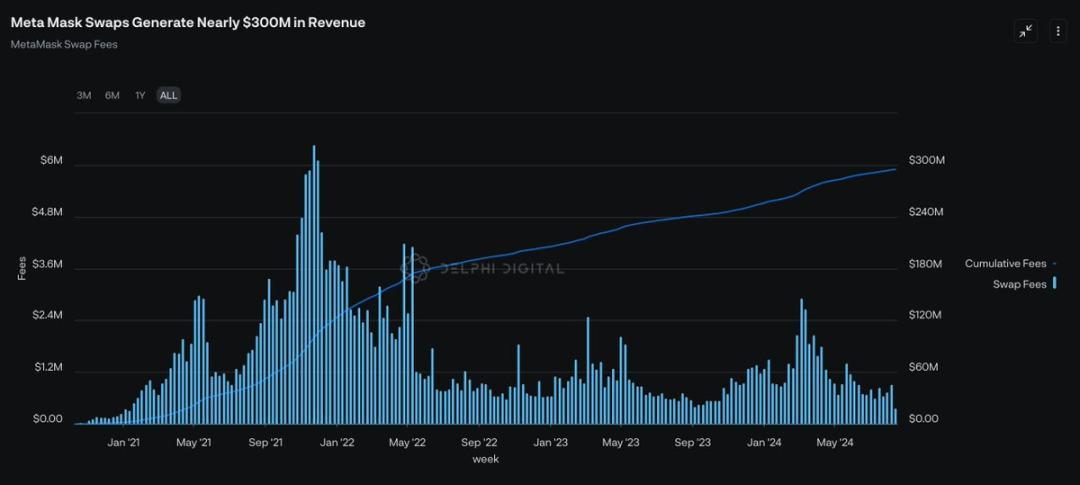

Wallet switching costs are incredibly high: While in theory switching wallets is as simple as copying and pasting a seed phrase, for most ordinary users this is still a psychological hurdle. Given the high level of trust users place in wallet providers, I believe branding and "affinity" are a powerful source of moat at the wallet layer. Revisiting our initial question again: if a wallet raises its fees, will users switch to a cheaper alternative? The answer appears to be: "NO". The MetaMask wallet charges a 0.875% fee for its swap functionality, yet still has a large user base.

Chain abstraction: While chain abstraction is a technically challenging problem, one of the more compelling solutions is to solve it at the wallet layer. The idea of being able to seamlessly access any application on any chain through a single account balance feels particularly intuitive. Projects like oneBalance, Brahma, Polaris, Particle Network, Ctrl Wallet, and Coinbase's smart wallet are all moving towards this vision. Going forward, I expect more teams to address user needs through chain abstraction at the wallet layer.

The Unique Synergy with AI: While I expect AI agents to increasingly commoditize the rest of the blockchain stack, users will still need to authorize agents to ultimately execute transactions on their behalf. This means the wallet layer is best suited to become the canonical front-end for AI agents. Integrating AI into the account layer also includes outcomes such as automated staking, yield farming strategies, and more.

We've outlined the "why" of wallets owning the end-user relationship, so let's now consider how they might "monetize" this relationship.

Monetization Opportunities

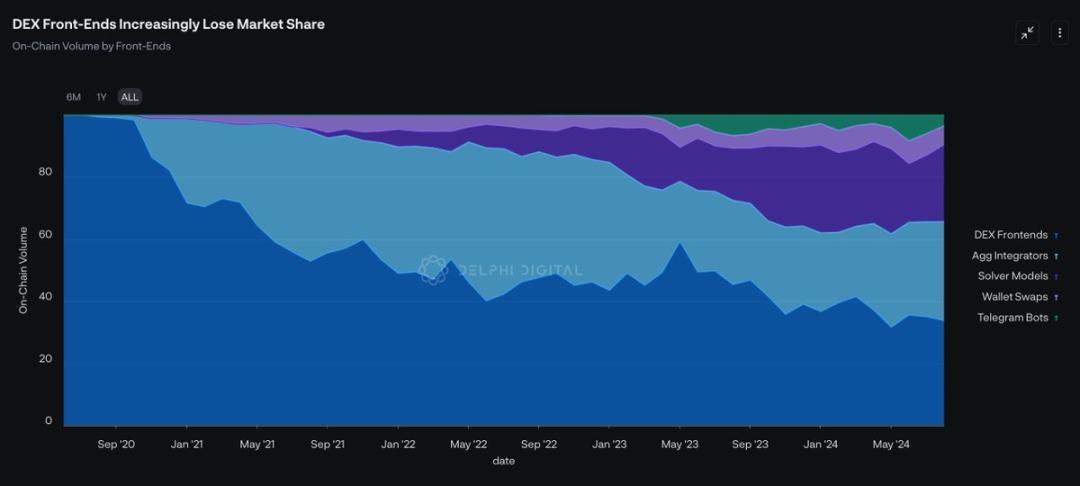

The first monetization opportunity for wallets is owning the user order flow. As I mentioned earlier, while the MEV supply chain will continue to evolve, one thing will become inevitable: value will disproportionately accrue to those with the most exclusive access to order flow.

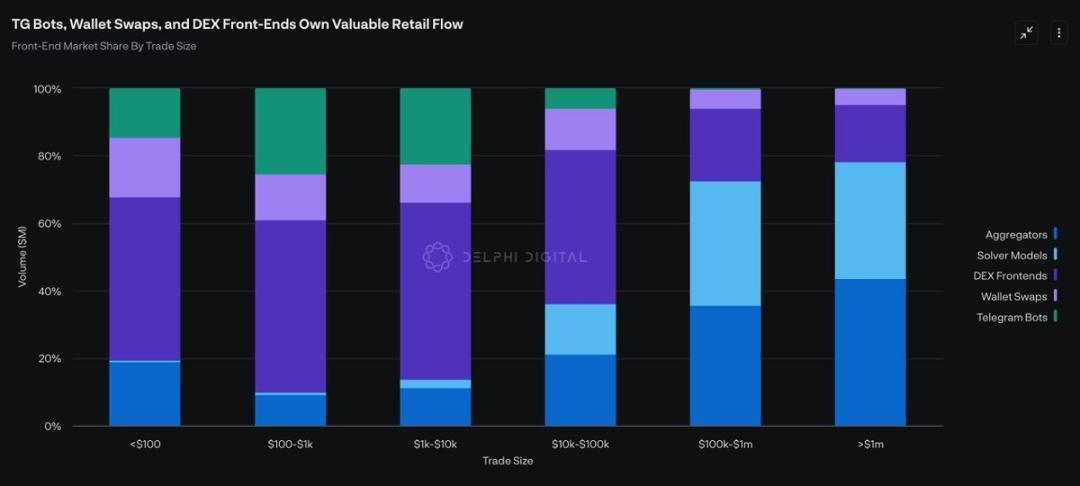

Today, the front-ends that own the majority of order flow by volume are solvers and DEXes. However, this chart doesn't reveal the nuances. The key is to understand that not all order flow is created equal. There are two types of order flow: (1) fee-sensitive order flow and (2) fee-insensitive order flow.

Generally, solvers and aggregators dominate the "fee-sensitive" order flow. Given these users' trade sizes typically exceed $100k, execution is critical to them. These traders won't accept even a 10 bps overpay. So "fee-sensitive" traders are a lower-value customer segment. While they account for the majority of front-end market share by volume, they generate far less value per $1 of trade.

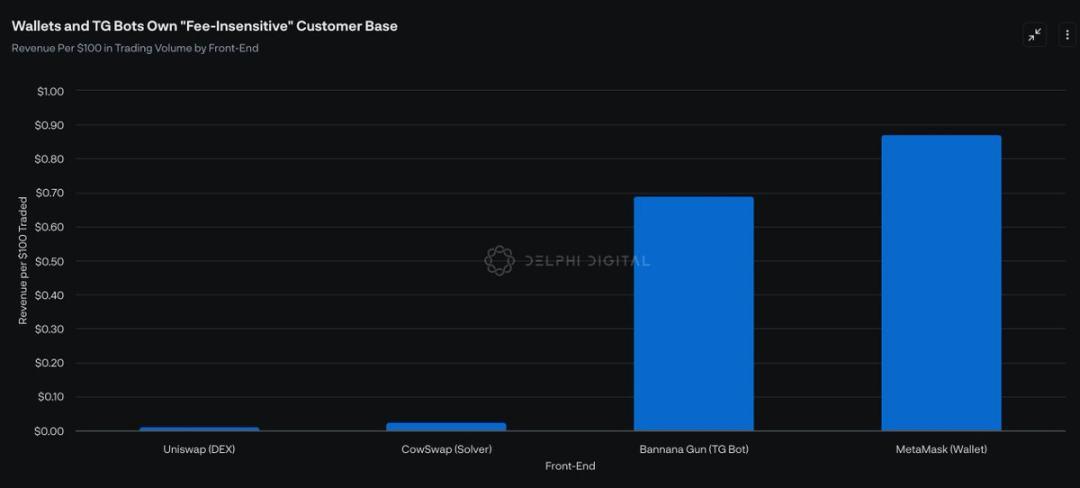

In contrast, wallet swaps and TG bots have a more valuable user base: "fee-insensitive" traders. These traders are paying for convenience, not execution. So paying 50 bps for a trade is irrelevant to them. As a result, TG bots and wallet swaps generate far more revenue per $1 of trade volume.

Looking ahead, if wallets can leverage these trends and continue to own the end-user relationship, I expect the swap functionality within wallets to continue cannibalizing market share from other front-ends. More importantly, even a 5% market share gain would have a massive impact, as wallet swaps generate nearly 100x the revenue per $100 of trade compared to DEX front-ends.

The second monetization opportunity for wallets, due to their proximity to end-users, is Distribution-as-a-Service (DaaS).

Beyond serving as the canonical front-end for user on-chain interactions, apps will ultimately depend on wallets as distribution channels, especially in mobile environments. So, similar to how Apple monetizes through iOS, wallets could strike exclusive deals with apps in exchange for distribution services. For example, wallet providers could build their own app stores and charge apps through some revenue-sharing arrangement.

Likewise, wallet providers could also steer users towards using specific apps in exchange for some economic sharing. This approach has an advantage over traditional advertising in that users can seamlessly purchase and interact with the app directly from their wallet. Coinbase seems to be exploring a similar path with "Featured" apps and in-wallet "Missions".

Wallets could also get economic upside by sponsoring user transactions to help bootstrap emerging blockchains. For instance, maybe Bearachain just wants users to join their blockchain. They could pay Metamask a fee to sponsor Bearachain's cross-chain fees and gas on their behalf. Given wallets ultimately own the end-user, they can negotiate favorable terms.

As more users access the on-chain world primarily through wallets, we can see demand shifting from "block space" to "wallet space", as attention becomes the most valuable resource in the crypto economy.

Challenges Facing Fat Wallets

Finally, while wallets have a clear lead in the race for end-user ownership, I remain excited about the prospects of two alternative front-ends:

Jupiter: Through their DEX aggregator, Jupiter has already been able to cultivate strong relationships with end-users. This could be the best launchpad for them to build out other related products in crypto, including their perps DEX, Launchpad, native LST, and their recent RFQ/Solver offering. I'm particularly excited about the launch of Jupiter's mobile app, as it could allow them to get in front of end-users in the mobile environment before wallets.

Infinex: By serving as the front-end aggregator for apps on both EVM chains and Solana, Infinex aims to provide a CEX-like experience while retaining principles like non-custodial and permissionless. Infinex will initially offer spot trading and staking services, and plans to integrate perpetual contracts, options, lending, margin trading, yield farming, and fiat on-ramps. By abstracting the account layer and using Web2-familiar features (like key management), I believe Infinex has the potential to displace wallets as the canonical crypto front-end.

While I'm still not sure who will ultimately win the battle for end-user ownership, it's becoming increasingly clear that (1) user attention and (2) exclusive order flow will continue to be the scarcest, and therefore most monetizable, resources in the crypto economy. Whether it's wallets or alternative front-ends like Infinex or Jupiter, I expect the value capture kings in crypto will be the projects that own these two resources.