Author: DC | In SF

Compiled by: Block unicorn

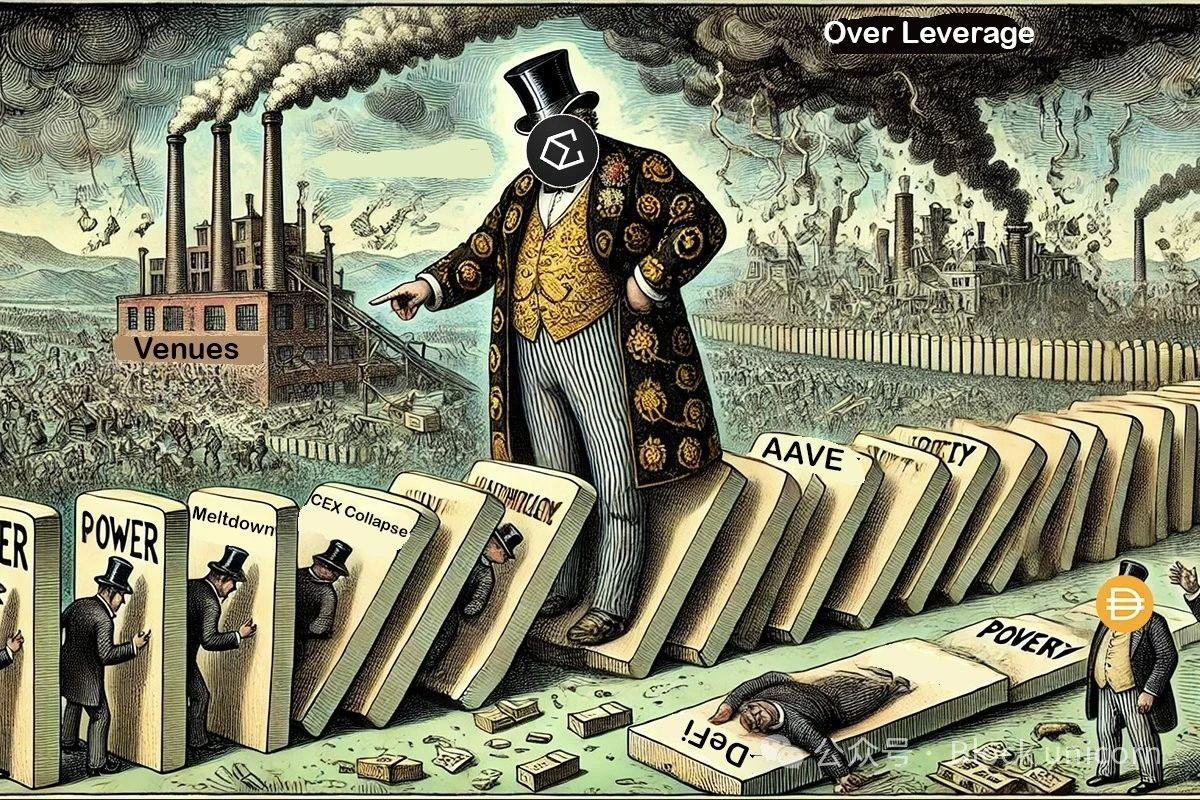

Ethena is the most successful protocol in DeFi history. About a year ago, its total locked value (TVL) was less than $10 million, but now it has grown to $5.5 billion. It is integrated in various ways with multiple protocols, such as @aave, @SkyEcosystem (IE Maker / Sparklend), @MorphoLabs, @pendle_fi and @eigenlayer. There are so many protocols collaborating with Ethena that I had to change the cover multiple times when recalling another partner. Among the top ten protocols by TVL, six are either collaborating with Ethena or are Ethena itself (Ethena ranks ninth). If Ethena fails, this will have a profound impact on many protocols, especially AAVE, Morpho and Maker, which will be insolvent to varying degrees in terms of functionality. At the same time, Ethena's growth of tens of billions of dollars has significantly increased the overall usage of DeFi, similar to the impact of stETH on Ethereum DeFi. So, is Ethena destined to destroy the DeFi we know, or will it usher in a new renaissance for DeFi? Let's dive into this issue.

How does Ethena actually work?

Although it has been launched for more than a year, there is still widespread misunderstanding about how Ethena works. Many claim it is the new Luna and then refuse to elaborate further. As someone who has warned about Luna, I find this view very one-sided, but I also believe that most people lack a sufficient understanding of the details of how Ethena operates. If you think you fully understand how Ethena manages delta-neutral positions, custody and redemption, please skip this section, otherwise this is important reading material for a thorough understanding.

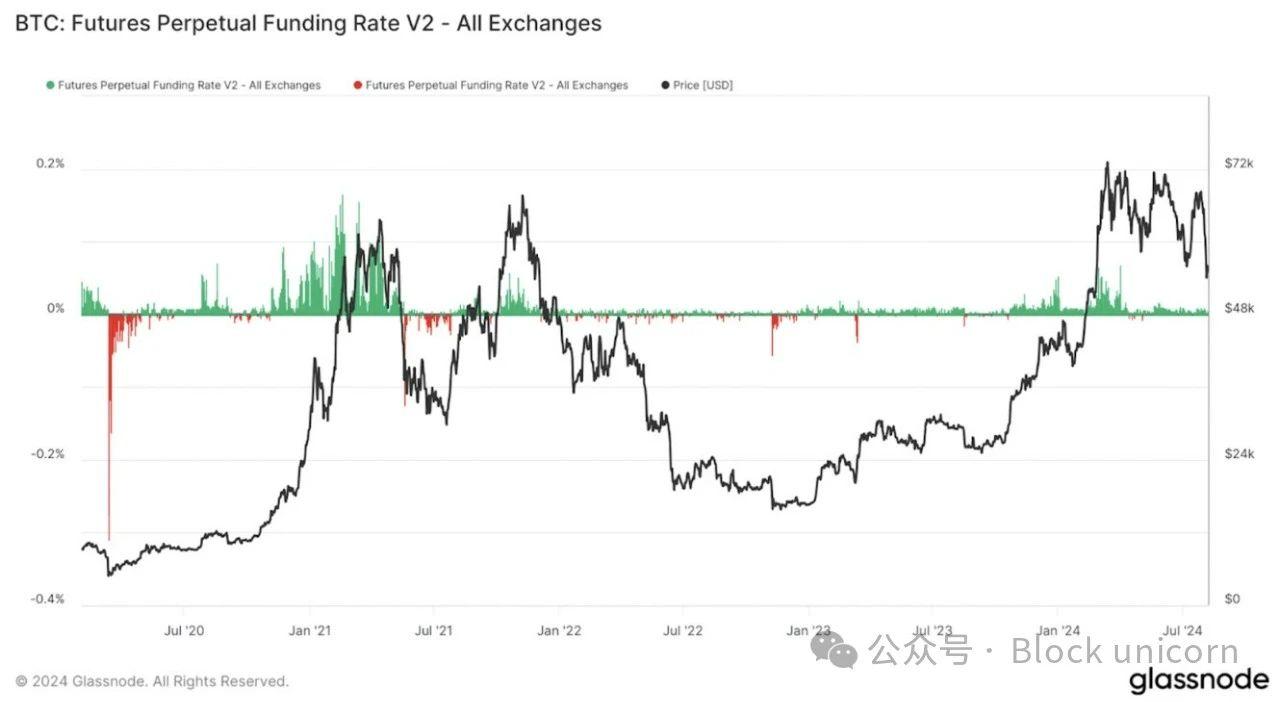

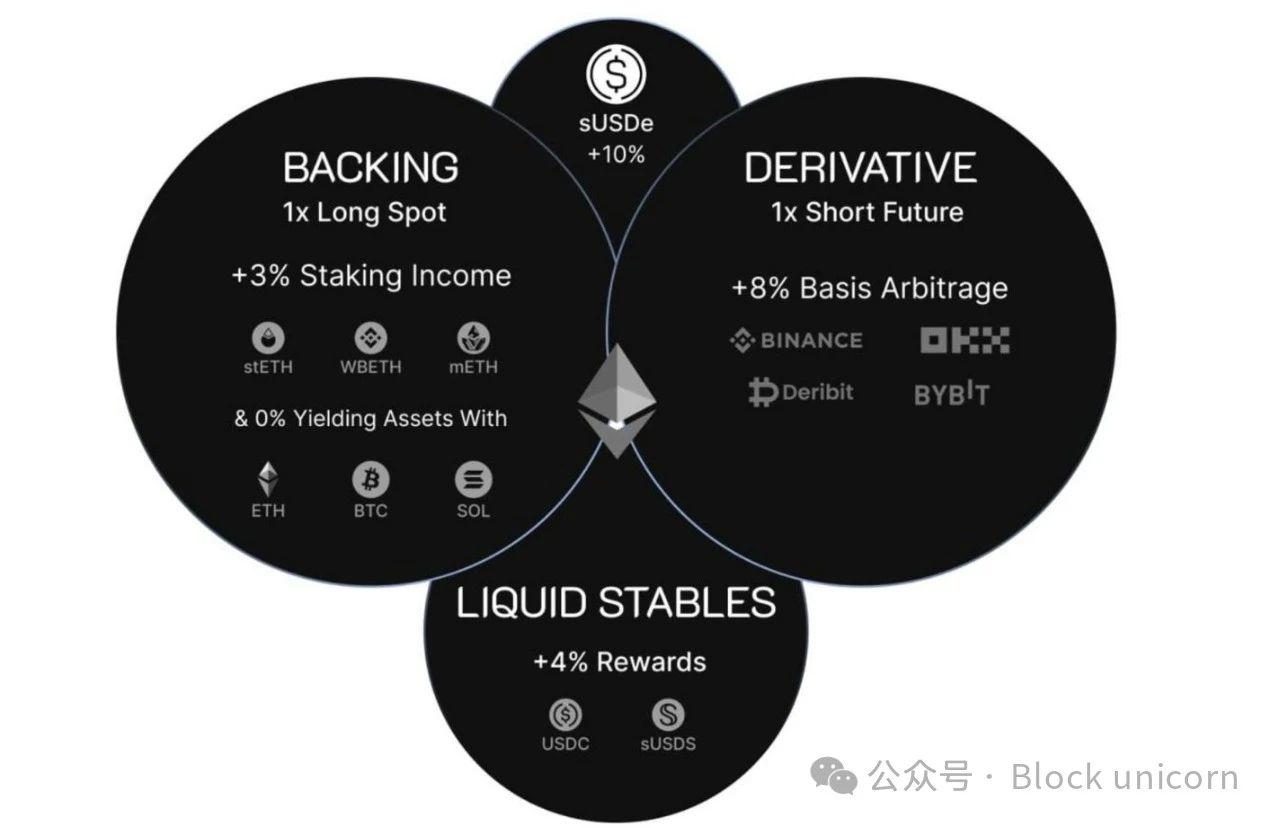

Overall, Ethena benefits from financial speculation and the cryptocurrency bull market, but in a more stable manner than BTC. As cryptocurrency prices rise, more and more traders want to long BTC and ETH, while fewer and fewer traders are willing to short. Due to the supply-demand relationship, the short traders pay fees to the long traders. This means that traders can hold BTC while shorting the same amount of BTC, thereby achieving a neutral position, where the gains and losses of the long and short positions offset each other, while the traders still earn interest income. Ethena's operation is entirely based on this mechanism; it leverages the lack of sophisticated investors in the crypto market, who are more interested in earning yield rather than simply going long on BTC or ETH.

However, a major risk of this strategy is the custody risk of exchanges, as evidenced by the collapse of FTX and its impact on first-generation delta-neutral managers. Once an exchange goes bankrupt, all funds may be lost. This is why, no matter how efficiently and securely mainstream managers manage capital, they were greatly impacted by the collapse of FTX, the most obvious example being @galoiscapital, and this was not their fault. Exchange risk is one of the important reasons why Ethena has chosen to use @CopperHQ and @CeffuGlobal as custodians. These custodial service providers, as trusted intermediaries, are responsible for holding assets and assisting Ethena in interacting with exchanges, while avoiding exposing Ethena to the custody risk of exchanges. The exchanges, in turn, can rely on Copper and Ceffu, as they have legal agreements with the custodial institutions. The net profit and loss (i.e., the amount Ethena needs to pay to the long traders, or the amount the long traders owe to Ethena) is settled periodically by Copper and Ceffu, and Ethena systematically rebalances its positions based on these settlement results. This custodial arrangement effectively mitigates exchange-related risks while ensuring the stability and sustainability of the system.

The minting and redemption of USDe / sUSDe is relatively simple. USDC or other major assets can be used to purchase or mint USDe. USDe can be staked to generate sUSDe, which will earn yield. sUSDe can then be sold to the market by paying the corresponding swap fee, or redeemed for USDe. The redemption process usually takes seven days. USDe can then be exchanged 1:1 for the underlying assets (corresponding to $1 in value). These underlying assets come from the asset reserve and the collateral used by Ethena (mainly BTC and ETH/ETH derivatives). Given that some USDe are not staked (many of which are used for Pendle or AAVE), the income generated by the assets supporting these unstaked USDe helps to enhance the yield of sUSDe.

So far, Ethena has been able to handle large amounts of withdrawals and deposits relatively easily, although the USDe-USDC slippage can sometimes be as high as 0.30%, which is relatively high for a stablecoin, but far from reaching a significant de-peg level or posing a danger to lending protocols, so why are people so concerned?

Well, if there is a large withdrawal demand, say 50%...

How could Ethena "fail"?

Given that we now understand Ethena's yields are not "fake" and how it operates at a more granular level, what are the main real concerns about Ethena? Basically, there are a few scenarios. First, the funding rate could turn negative, in which case, if Ethena's insurance fund (currently around $50 million, sufficient to withstand a 1% slippage/capital loss on the current TVL) is not enough to cover the losses, Ethena will ultimately lose money instead of profiting. This scenario seems relatively unlikely, as most users would likely stop using USDe when yields decline, which has happened in the past.

Another risk is the custodial risk, i.e., the risk of Copper or Ceffu trying to operate with Ethena's money. The fact that the custodians do not have full control of the assets mitigates this risk. The exchanges have no signing authority and cannot control any wallets holding the underlying assets. Copper and Ceffu are "commingled" wallets, meaning that all institutional users' funds are mixed in hot/warm/cold wallets, with multiple risk mitigation measures such as governance (i.e., control) and insurance. From a legal perspective, this is a bankruptcy-remote trust structure, so even if the custodians go bankrupt, the assets held by the custodians do not belong to the custodians' property and the custodians have no claim over these assets. In practice, there are still risks of simple negligence and centralization, but there are many safeguards to avoid this, and I would consider this a black swan event.

The third, and most commonly discussed, risk is the liquidity risk. To manage redemptions, Ethena must sell both its derivative positions and spot positions simultaneously. If there are violent price fluctuations in ETH/BTC, this could be a difficult, expensive and potentially very time-consuming process. Currently, Ethena has prepared billions of dollars to be able to redeem USDe 1:1 for dollars, as it holds a large amount of stable positions. However, if Ethena's share of the total open interest (i.e., all outstanding derivatives) becomes larger and larger, this risk becomes more severe and could lead to a drop in Ethena's net asset value (NAV) by a few percentage points. However, in this case, the insurance pool would likely fill the gap, and this alone is not enough to cause a catastrophic failure of the protocols using it, which naturally leads to the next topic.

What are the risks for protocols using Ethena?

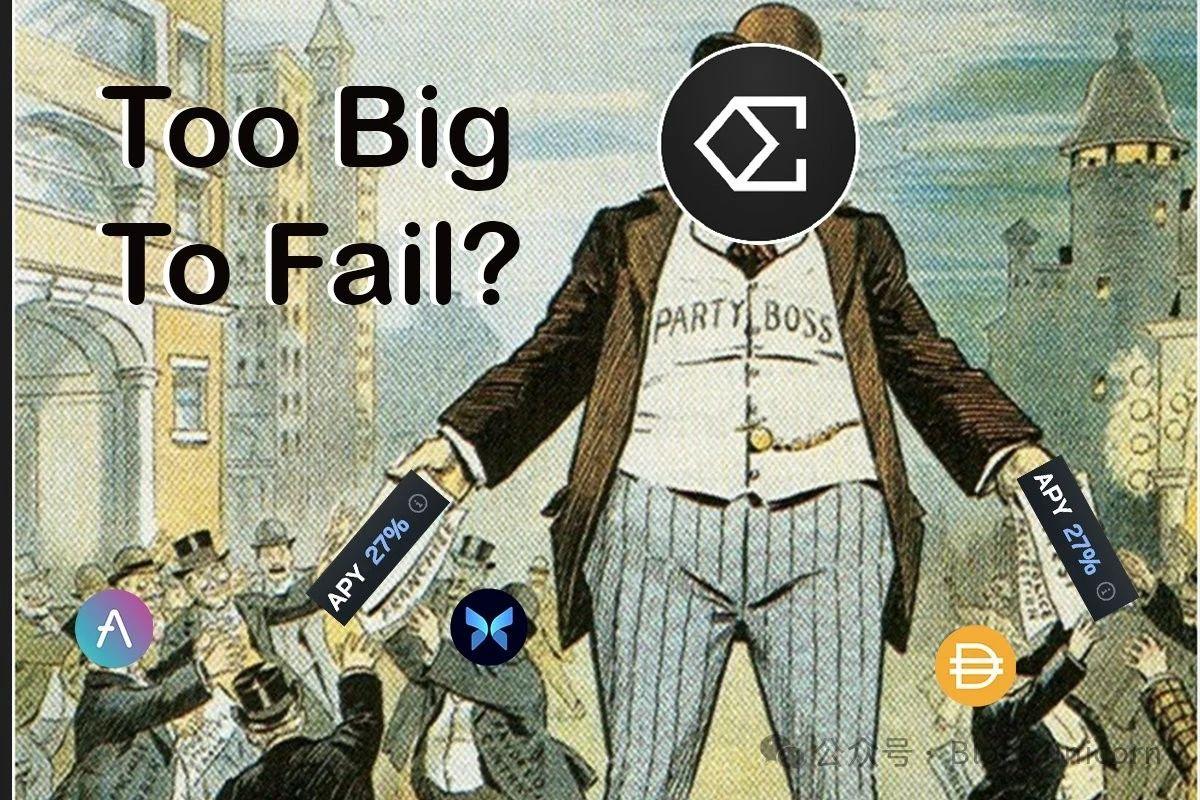

In short, not using the Ethena protocol may face the risks of lower yields and lower demand, but it is necessary to avoid the risk of serious de-pegging or collapse of the USDe price, which may be negligible. Systems like Morpho, due to their independent structure, may be better able to adapt and avoid potential collapses. Therefore, it is understandable that systems based on larger liquidity pools, such as AAVE, take longer to adopt Ethena. Now, while most of the content is a review of the past, I would like to offer some perspectives more focused on the future. Recently, Ethena has been working hard to integrate DEXs. Most DEXs lack short demand, that is, users who want to short the contract. Generally, the only type of user who can do this on a large scale and continuously is delta-neutral traders, of which Ethena is the largest. I believe that perpetual contract platforms that can successfully integrate Ethena while maintaining a good product can escape competition in a very similar way to Morpho by working closely with Ethena to escape their smaller competitors.