2.6 RWA and Stablecoins

In 2024, RWA (Real World Assets) and stablecoins became important drivers of the crypto market, promoting the deep integration of blockchain technology and traditional finance.

Rapid growth of the RWA market:

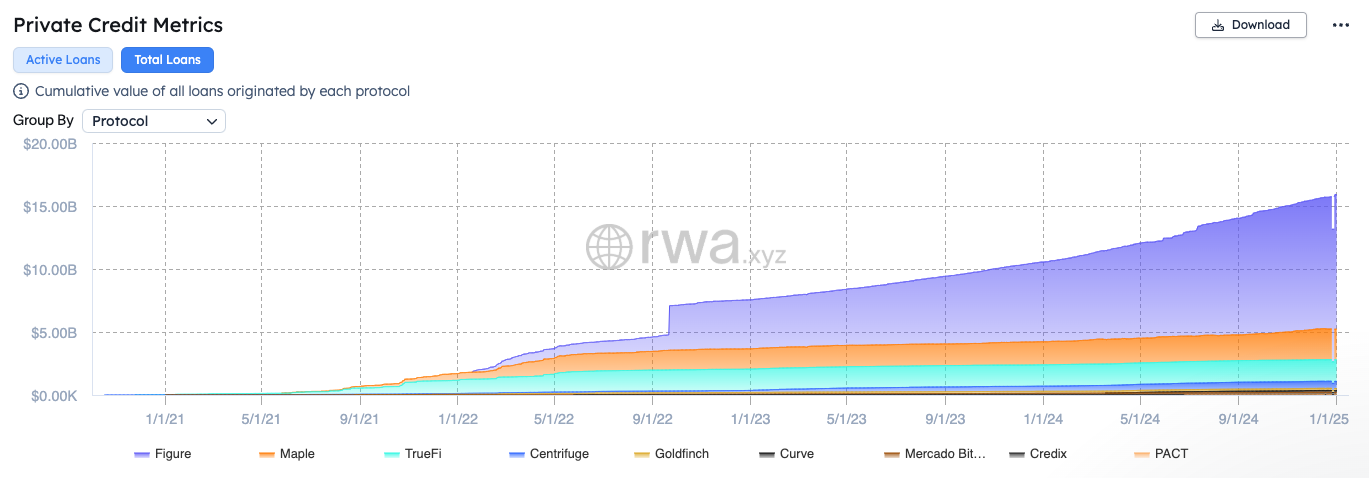

In 2024, the on-chain real-world assets (RWA) market continued to expand, with a total asset size reaching $15.2B, an increase of nearly $7B compared to 2023, and the number of holders exceeded 80,000. In terms of scale, private credit accounted for the largest share and its scale continued to expand; US Treasuries accounted for the second largest share, and its scale also continued to expand; the scale of commodities, corporate bonds, stocks and other RWA assets was relatively small, with weaker growth.

Private credit (Private Credit) dominates the RWA market. Figure continues to maintain a leading position, occupying more than 70% of the market share in terms of total loan volume and active loan balance. Established projects such as Maple, TrueFi, Centrifuge and Goldfinch have maintained a stable market share.

In terms of RWA projects, Ondo Finance, by tokenizing US Treasuries and corporate bonds, has exceeded $3 billion in locked-in value (TVL), becoming a benchmark project in the RWA field. MakerDAO, through the launch of the RWA custody plan, has introduced $10 billion in assets on-chain, driving the expansion of the collateral assets of its decentralized stablecoin DAI from crypto assets to RWA. OpenEden is an RWA (Real World Assets) tokenization protocol that focuses on US debt on-chain, launching the OpenEden TBill Vault product, allowing users to mint TBILL tokens with USDC to earn yields, and collaborating with Binance Labs to expand the market.

In RWA innovation, USUAL is an innovative RWA stablecoin protocol that has launched the fully compliant and permissionless stablecoin USD0, which is 1:1 backed by real-world assets (RWA), aiming to integrate the liquidity of RWA tokens from various platforms/companies and merge CeFi and DeFi. Usual has integrated with multiple decentralized finance (DeFi) platforms and protocols, including the lending platform Morpho, the yield platform Pendle, etc., with a total locked-in value (TVL) of over $1.6B, demonstrating its strong growth momentum in the stablecoin field.

In 2024, large financial institutions are also entering the RWA track. BlackRock has launched the first tokenized asset fund BUIDL on the Ethereum network, and has partnered with Securitize and Circle to support 24/7 real-time subscription and redemption. Tether, the issuer of the stablecoin USDT, has announced the launch of the asset tokenization platform Hadron by Tether, aiming to simplify the tokenization process of real-world assets (stocks, bonds, real estate, funds and loyalty points, etc.).

Rapid development of stablecoins:

The total supply of stablecoins reached a historic high of $200B in 2024, becoming a core driver of the crypto market, not only as a value anchor, but also as the liquidity foundation for DeFi protocols and exchanges.

In the stablecoin track, USDT continues to maintain a leading position, with its market capitalization and circulation both experiencing significant growth. USDT has been issued multiple times on various blockchain networks (including TRON and Ethereum, etc.), and as of December 2024, USDT's market capitalization has exceeded $140 billion, an increase of nearly $50 billion from the beginning of the year, an increase of more than 55%.

At the same time, Ethena is the best performing stablecoin project this year, further catalyzing the boom of yield-bearing stablecoins. Ethena's USDe has a market capitalization of over $5.9B, not only contributing a large amount of new liquidity to mainstream DeFi protocols such as Aave, Maker, Morpho, Pendle, etc., but also being the main source of income for these DeFi protocols.

In addition to rapid growth in the crypto field, the application of stablecoins in global payments and cross-border remittances is also accelerating. According to estimates by Castle Island Ventures and Brevan Howard Digital, the payment settlement volume of stablecoins in the first half of 2024 has reached about $2.62 trillion, and is expected to exceed $5.28 trillion for the full year. There are about 20 million active addresses on-chain conducting stablecoin transactions monthly, and more than 120 million addresses hold non-zero stablecoin balances.

In emerging markets, the use of stablecoins has surpassed the traditional crypto trading domain and integrated into daily financial activities in regions such as Brazil, India, Indonesia, Nigeria and Turkey. Surveys show that 69% of respondents use stablecoins for currency substitution, 39% for payment of goods and services, 39% for cross-border payments, and another 20% to 30% of respondents use stablecoins for payroll and business activities. The Africa-based cross-border payment company Juicyway has already processed over $1.3 billion in stablecoin transactions. Nigeria ranks second globally in crypto adoption.

In 2024, large enterprises and banks are also actively entering the stablecoin track. US online payment company PayPal has launched the US dollar-pegged stablecoin PayPal USD, and announced in September that it will allow merchants to buy, hold and sell cryptocurrencies through their business accounts. In addition, Stripe acquired the stablecoin platform Bridge for $1.1 billion, restoring the service for US businesses to make crypto payments on Ethereum, Solana and Polygon using USDC. The three major banks in Japan - Mitsubishi UFJ Financial Group (MUFG), Sumitomo Mitsui Banking Corporation (SMBC) and Mizuho Bank - jointly launched a cross-border payment system called "Project Pax" in September 2024, using stablecoins to replace traditional intermediary banks in cross-border payments, improving efficiency and reducing costs.

2.7 The Explosion of the TON Ecosystem

In 2024, the TON public chain, relying on Telegram's huge user base and the innovative Mini App product model and airdrop gameplay, achieved large-scale explosion in the fields of gaming and social networking. The explosive popularity of social games such as Notcoin, Hamster, and Catizen quickly attracted a large number of Web2 and Web3 users, boosting the on-chain activity and market heat of the TON public chain.

(Data source: tonstat.com)

NOTCOIN became a phenomenal application, relying on its Tap-to-Earn model, attracting 5 million users within a week of its launch, and its user base exceeded 40 million in just a few months, becoming the hottest Web3 application in the Telegram Apps Center. Its token was fairly launched with a FDV of over $1 billion, leading the Telegram Mini Apps craze.

Following NOTCOIN, the continued explosive popularity of games and social applications such as Catizen, Dogs, Hamster Kombat, and Uxlink, combined with the wealth effect of airdrops and token listings, successfully focused market attention on these Mini App projects.

Relying on Telegram's huge user base (over 900 million MAU), TON provided a powerful user and traffic entry point for Web3 projects. Many Web3 projects leveraged TON to expand their user base and community traffic. The focus on users and traffic also drove Telegram to achieve its first profitability in 2024, with the number of Premium subscription users exceeding 12 million, and total annual revenue exceeding $1 billion.

Although TON has achieved great success in the gaming and social ecosystem, its DeFi and other ecosystem development is relatively weak, and the mainnet is more like a traffic pool and user service platform. As homogeneous projects within the ecosystem increase, the wealth effect gradually weakens, and user stickiness has declined significantly. The intensification of competition and the decline of project heat have led to a significant downward trend in the on-chain activity of the TON ecosystem by the end of the year.

3. Crypto Market Financing Situation and Investment Trends in 2024

In 2024, the financing situation in the crypto market showed a trend of diversification and gradual recovery. Although the market has experienced volatility over the past year, innovative projects and technology-driven projects still attracted the attention of investors, especially in areas such as Web3 infrastructure, DeFi, CeFi, gaming and AI+blockchain, with significant growth in financing activity and amount.

3.1 Recovery of the investment environment and capital injection

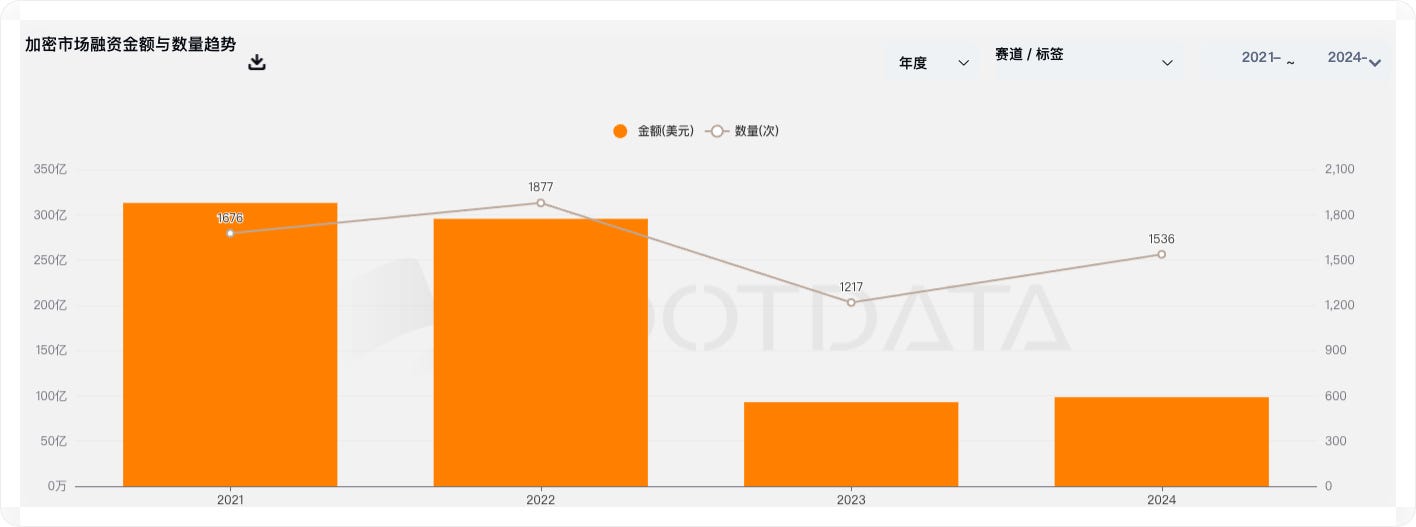

Followin' the overall financing data, 2024 is a year of recovery in the crypto market financing. According to RootData statistics, there were 1,536 disclosed investment and financing events in the cryptocurrency and blockchain sector in the primary market in 2024, with a total financing amount exceeding $10.1 billion, an average financing amount of $9.13 million, and a median financing amount of $4.1 million.

In terms of the number of financings and the amount of financing, the investment and financing market situation in 2024 is basically the same as that in 2023, with the latter completing $9.3 billion in financing through 1,217 transactions. However, compared to the financing amount and volume in 2021 and 2022, there is a significant gap, reflecting that the financing situation in the crypto market has improved to some extent, but is far from recovering to the peak of the previous DeFi bull market, and the overall market investment trend is inclined to be cautious and rational.

3.2 Capital Flow and Track Popularity:

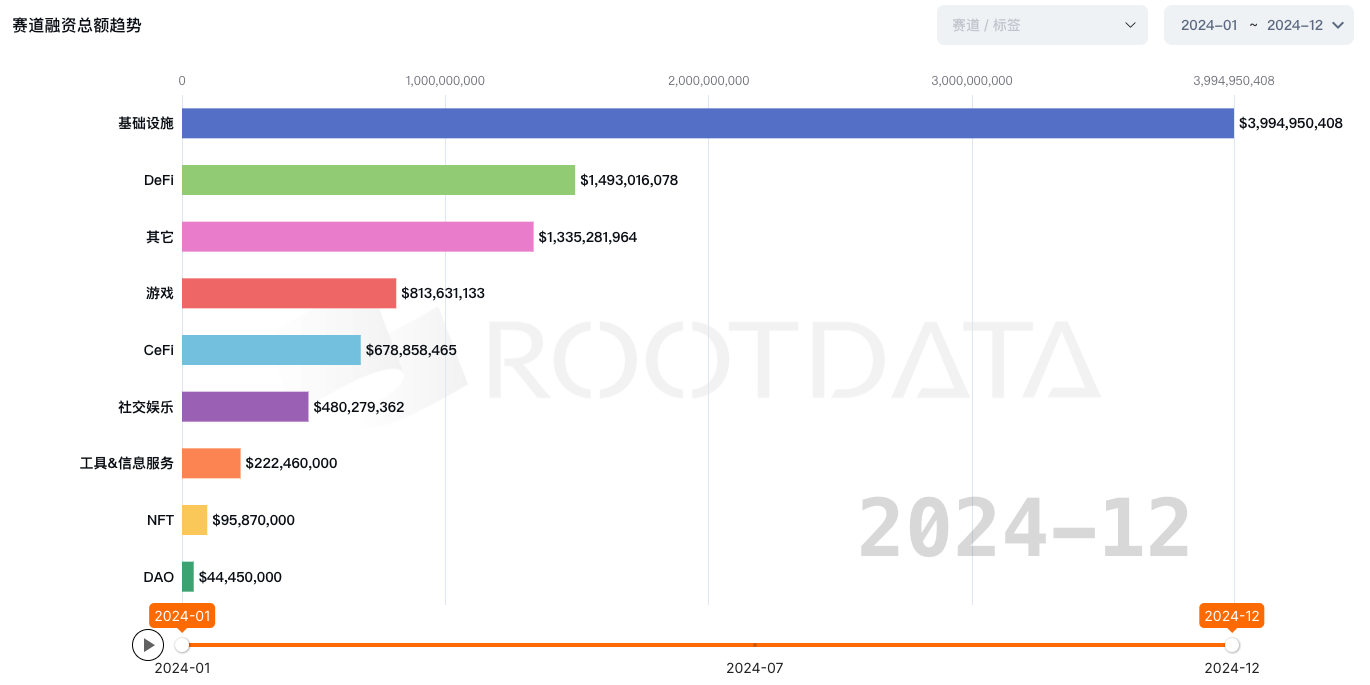

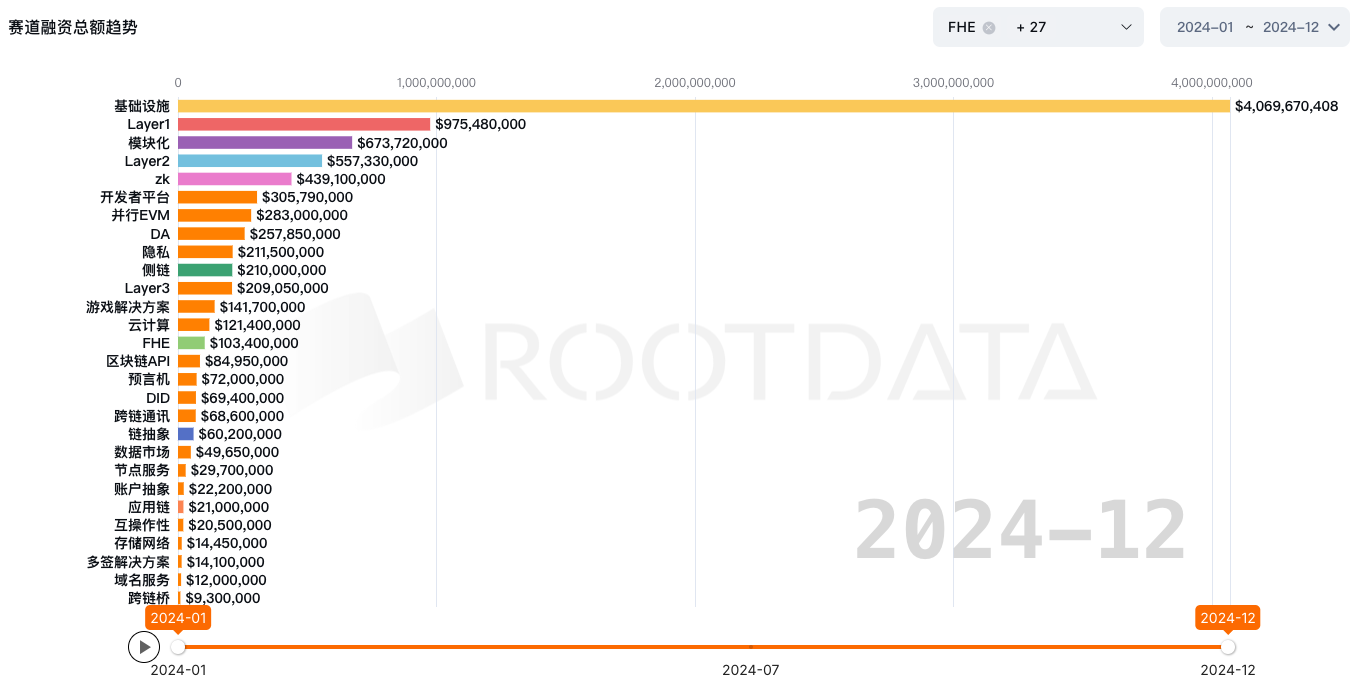

In 2024, the capital flow in the crypto market showed a clear trend of concentration, with several tracks becoming the focus of investors' attention. According to RootData's data statistics, the Web3 infrastructure, DeFi, gaming and CeFI, social entertainment and AI tracks received the most financing, with the Web3 infrastructure track receiving nearly $4 billion in financing, accounting for nearly 40% of the total financing amount.

Within the Web3 infrastructure track, it can be seen that in 2024, public chain infrastructure and L2 scaling solutions including Layer1, modular blockchains, Layer2, ZK, parallel EVM, DA, sidechains, and Layer3 have become the preferred investment targets for investment institutions. This also reflects the preference of investment institutions for infrastructure investment.

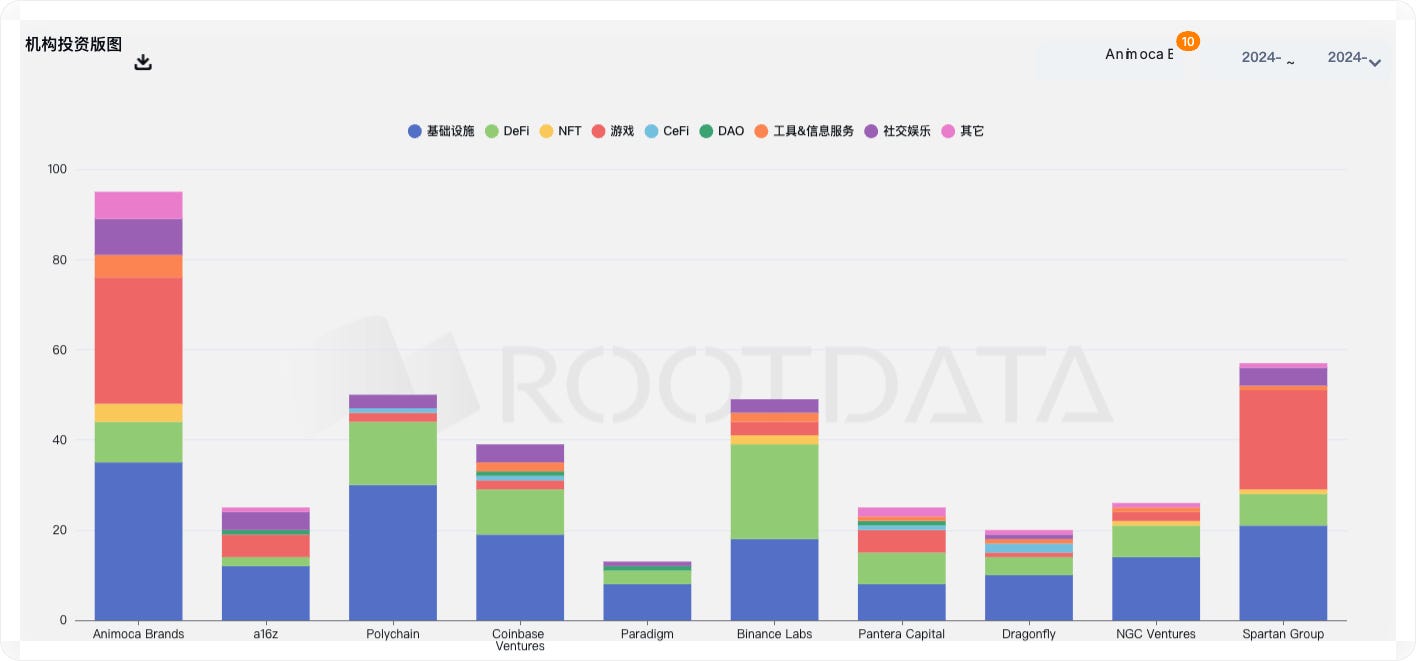

Well-known VC firms such as Animoca Brands, Andreessen Horowitz (a16z), Polychain, Coinbase Ventures, Binance Labs, Spartan Group, and Paradigm have increased their investment in the blockchain and Web3 sectors in 2024. From their investment preferences, investment institutions tend to invest in Web3 infrastructure and DeFi, with Animoca Brands and Spartan Group preferring infrastructure and gaming tracks, with the most investments in these areas.

3.3 Popular Investment Cases

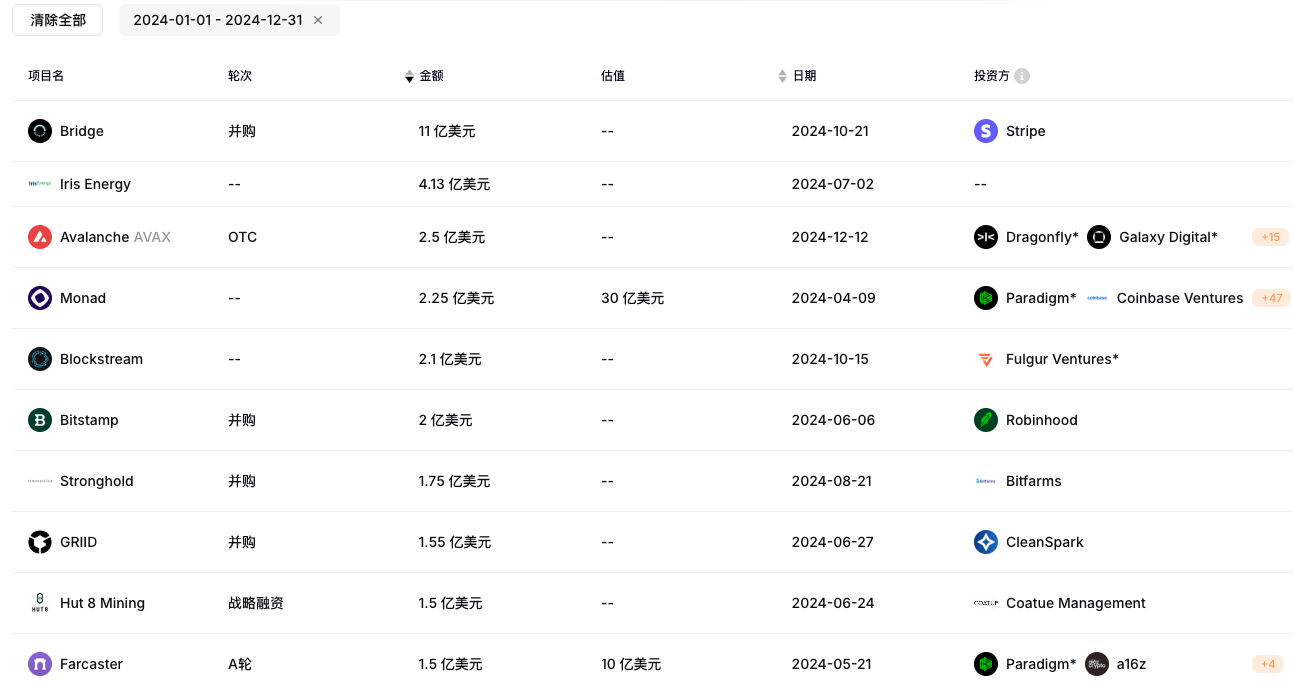

In the 2024 Web3 blockchain project financing, typical cases include Monad mainnet's $225 million, Farcaster's $150 million Series A, Berachain's $100 million Series B, EigenLayer's $100 million Series B, and HashKey Group's $100 million Series A.

(Top 10 blockchain financing amounts in 2024, data source: ROOTDATA)

The financing scale of these projects indicates that investment institutions are more inclined to projects with clear commercialization paths and innovative technologies, and capital is beginning to concentrate on protocols with long-term growth potential, cross-chain capabilities, and scalability. The Web3 investment and financing market is gradually shifting from the "bubble-like" investment in the early stage to a more rational, technology-driven capital flow.

3.4 The Rise of Crypto Project M&A Activities

With the maturity of the crypto market, M&A activities have become another highlight of crypto market investment and financing in 2024. Many large companies are enhancing their competitiveness by acquiring innovative projects and technologies. Among them, the payment company Stripe acquired the stablecoin payment platform Bridge for $1.1 billion, which is the largest acquisition transaction in the crypto field. Other M&A cases include Robinhood's acquisition of the cryptocurrency exchange Bitstamp for $200 million, Bitfarms' acquisition of Stronghold Digital for $175 million, Cleanspark's acquisition of Bitcoin miner GRIID for $155 million, and Riot Platforms' acquisition of the Bitcoin mining infrastructure and custody service platform Block Mining for $92.5 million. The M&A trend shows that large companies are strengthening their market position by absorbing innovative projects and technologies.