has developed into a highly liquid global asset that is available 24/7. This creates conditions for investors to speculate, trade, and express macroeconomic views when traditional markets are closed.

continues to prove itself as an emerging store of value asset, with cumulative net capital inflows exceeding $850 billion. It also serves as a medium of exchange asset, processing nearly $9 billion in daily transactions.

New demand indicators remain elevated, but are far below the peaks of previous cycles.

The composition of digital asset investors is also changing, with a significant increase in more mature institutional investors in the space. This has led to generally lower drawdowns and volatility compression over time.

Since its inception in 2009, has evolved into a highly liquid global asset that remains actively traded 24/7. Given that global events often occur outside of traditional market trading hours, this makes one of the few assets that investors can use to express views on weekends.

On weekends, and other digital assets experienced sharp declines and then rebounds, as market participants reacted to the Trump administration's imposition of tariffs on Mexico, Canada, and China:

· trading price fell from $104,000 to $93,000 (-10.5%), then rebounded to $102,000.

· trading price fell from $34,000 to $25,000 (-26.5%), then rebounded to $28,000.

· trading price fell from $236 to $184 (-22.0%), then rebounded to $217.

is now playing an increasingly important role on the world stage, with the Kingdom of Bhutan undertaking large-scale mining operations, El Salvador pushing to make legal tender, and the U.S. government considering the potential of as a strategic reserve asset.

has now broken through the key psychological barrier of $100,000 for several consecutive weeks, a feat that many critics deemed impossible.

While the acceptance of among traditional investors is steadily increasing, for many, remains a controversial and polarized topic, often based on dubious claims of a lack of intrinsic value or utility.

Nevertheless, has solidified its position as one of the world's largest assets, with a market capitalization of $2 trillion, ranking 7th globally. Notably, this places above silver ($1.8 trillion), Saudi Aramco ($1.8 trillion), and Meta ($1.7 trillion), making it increasingly difficult to ignore.

As the asset's valuation and weighting reach such a large scale, its inertia will also rise accordingly. The implication is that now requires a significant influx of new capital to sustain its market capitalization growth.

Utilizing the realized capitalization metric, which measures the cumulative net capital inflows into digital assets, we can see that since the November 2022 cycle low, has absorbed an additional ~$450 billion in capital inflows, more than doubling its realized capitalization.

This reflects a total value of around $850 billion "stored" in , with each token priced based on its last on-chain transaction.

While is typically viewed as an emerging store of value asset, the network also serves as a decentralized rail for as a medium of exchange. The combination of nodes and miners allows any individual or entity to settle cross-border payments without the interaction of third-party intermediaries.

Utilizing Glassnode's entity-adjusted heuristic method to filter transactions, the network has processed an average of $8.7 billion per day over the past 365 days, with a total value transferred of $3.2 trillion over the past year.

The actual market value and economic volume settled on the network provide empirical evidence that has both "value" and "utility", challenging the critics' assumption that has neither.

Since the FTX collapse in November 2022, 's dominance has been on a sustained upward trend, rising from 38% to 59%. This indicates that in the digital asset realm, 's net rotation and value accretion are prioritized over other assets.

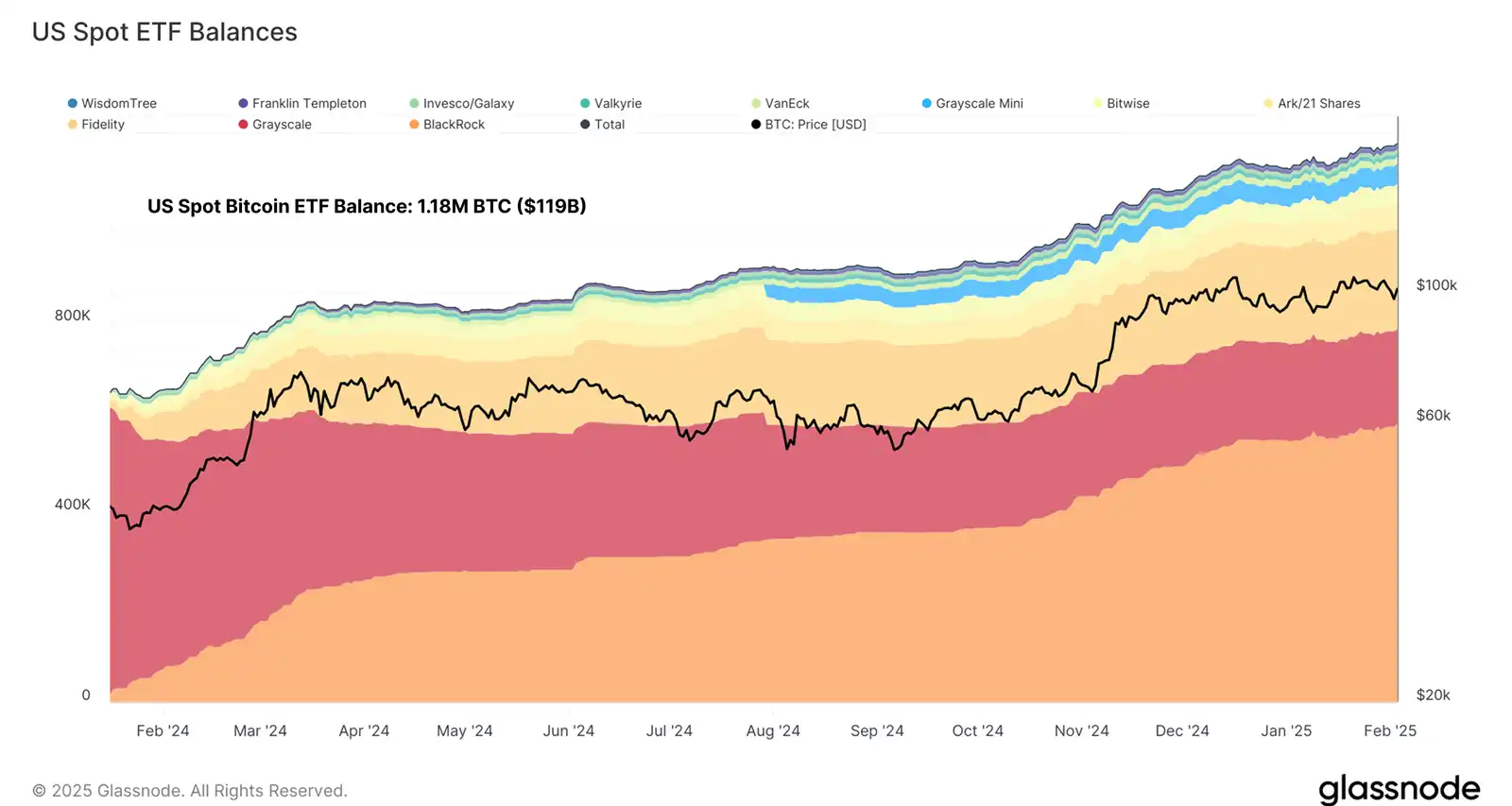

This may be partly attributable to the broader institutional capital access provided by U.S. spot ETFs. As a scarce asset, 's core narrative is also clearer, with many holding as a hedge against the devaluation of global fiat currencies.

While there is a significant valuation gap between and various (excluding Ethereum and stablecoins), the correlation between the two remains strong. This suggests that the reason for this disparity is not the growth rates between the two, but rather the vast difference in the capital entering the space versus the space.

As continues to capture the majority of capital from investors, its dominance can be expected to continue rising (a reversal of this metric would signal a rotation of capital in the other direction).

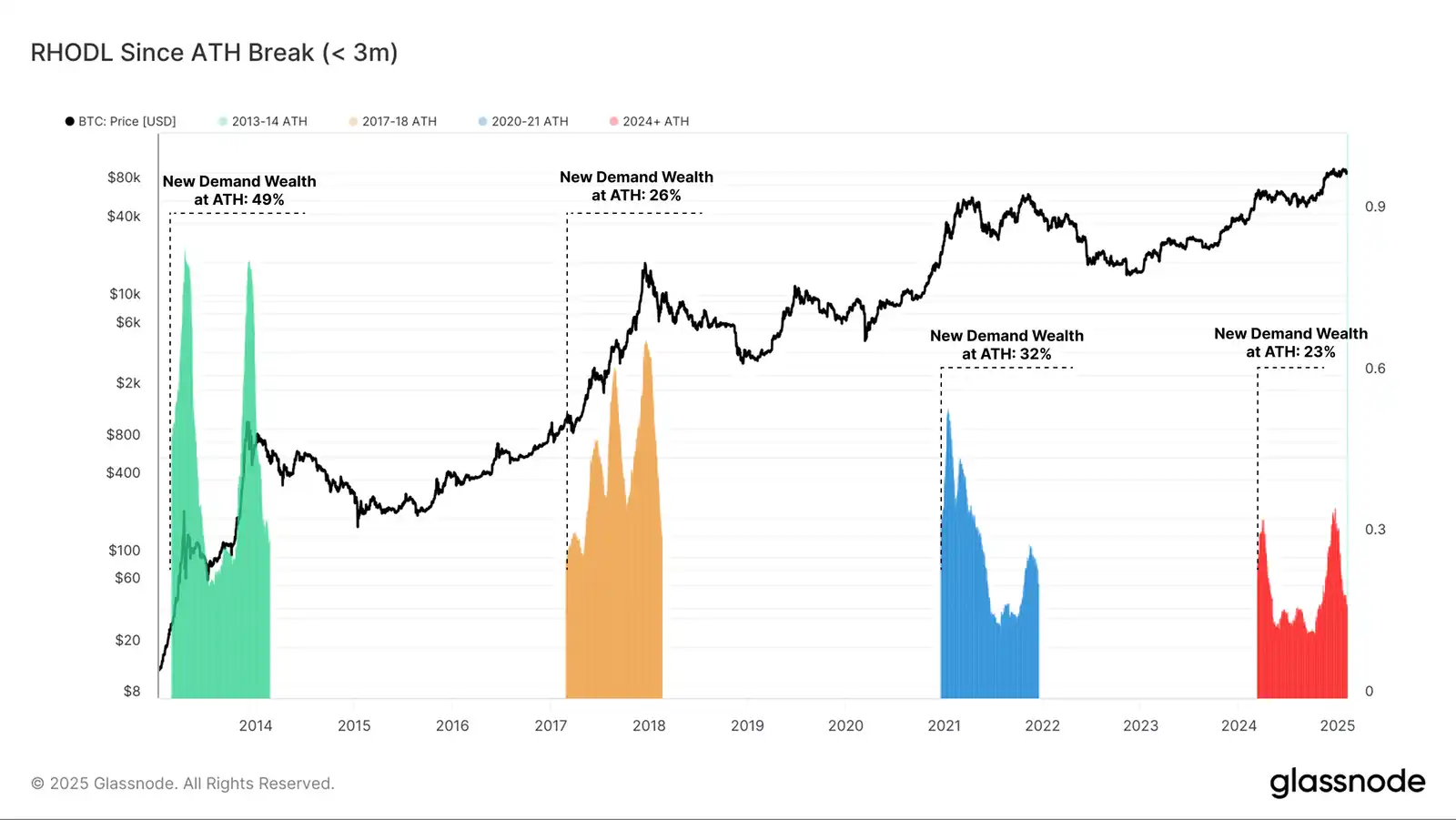

With prices breaking the $100,000 mark, there are expectations of a significant increase in 's exposure. We can assess this by evaluating the percentage of network wealth held by tokens purchased less than 3 months ago.

While this cycle's new demand is meaningful, the wealth held by 3-month-old tokens is much lower compared to previous cycles. This suggests that the scale of new demand inflows is not the same, appearing to be sporadic and peaking, rather than sustained.

Interestingly, all previous cycles ended around 1 year after the first ATH breakthrough, highlighting the atypical nature of our current cycle, which is expected to reach a new ATH in March 2024.

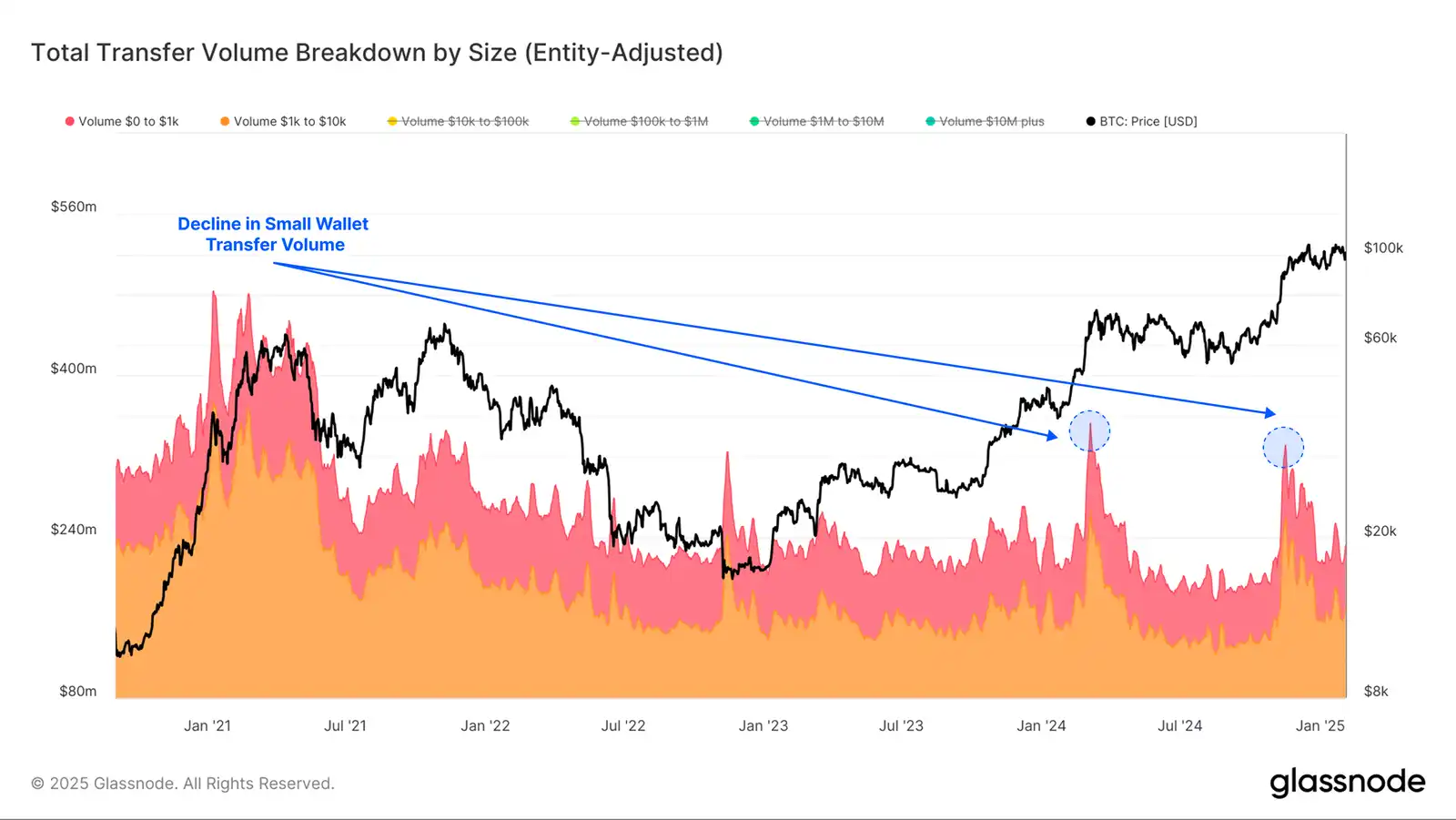

If we list the transaction volume of small wallets (less than $10,000) separately, we can see a significant decline compared to the peak in 2021. Despite the significant increase in overall settlement volume this cycle and the significant rise in the Bit price, this is still the case.

This indicates that the new demand for BTC is mainly driven by large entities rather than small retail entities.

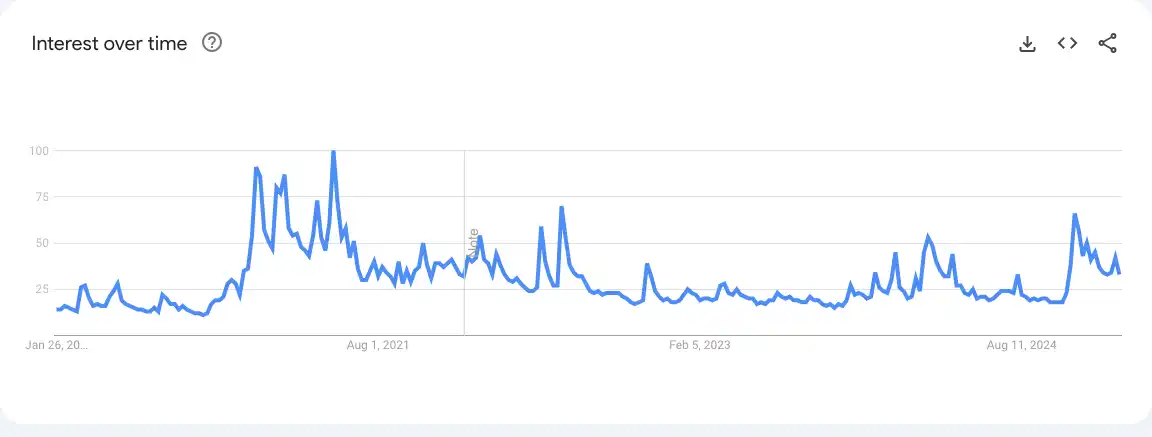

We can also use other data sets to support our argument. Although the asset has many favorable factors, the search intensity has not yet reached the frenetic level of the 2021 bull market.

Evolving Investor Base

While the structure and consensus code of the Bit protocol are essentially fixed, the market's response to it is an evolving and dynamic process. The regulatory environment is constantly changing, and new financial instruments such as derivatives and ETF products continue to develop around it. As the Bit environment evolves, the composition of Bit investors is also constantly changing, which is most evident in this cycle.

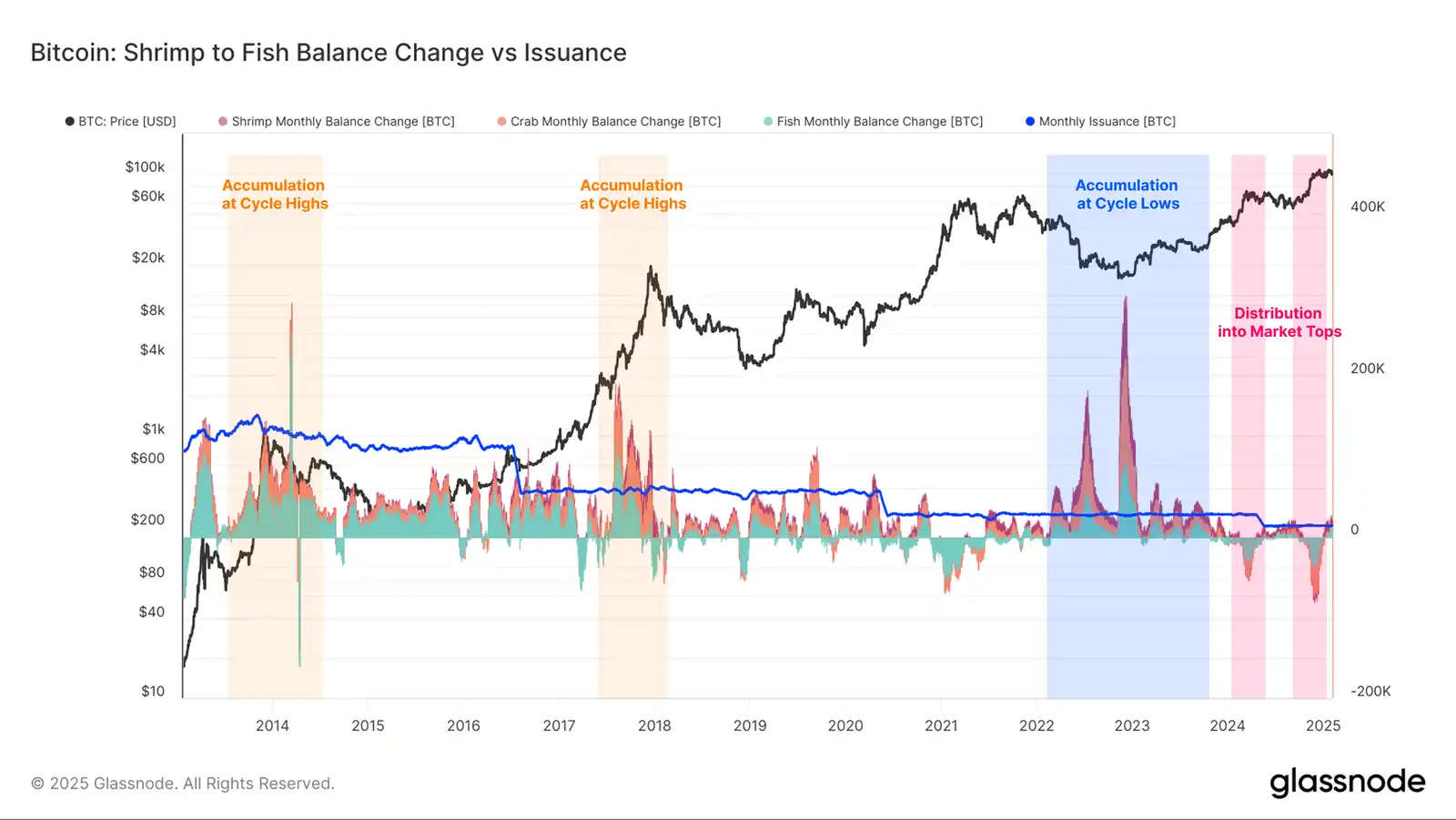

When comparing the balance changes of smaller entities (retail investors holding <10 BTC), we notice a clear change in behavioral patterns in recent years.

During the bull markets of 2013 and 2017, we could identify periods of significant token accumulation in these groups, which is often synonymous with "excited top buying". This pattern seems to have been broken this cycle, with smaller entities engaging in more aggressive accumulation during adjustments and pullbacks, then transitioning to distribution as the market rebounds to new highs.

This suggests that even within the investor groups typically viewed as retail investors, there is a more mature and well-educated investor base.

The launch of US spot ETF Bit instruments has also provided new investment channels for institutional investors, offering them regulated Bit investment opportunities. This has facilitated potential institutional capital flows, with net inflows into ETFs exceeding $40 billion in the 12 months since launch, and total assets under management exceeding $120 billion.

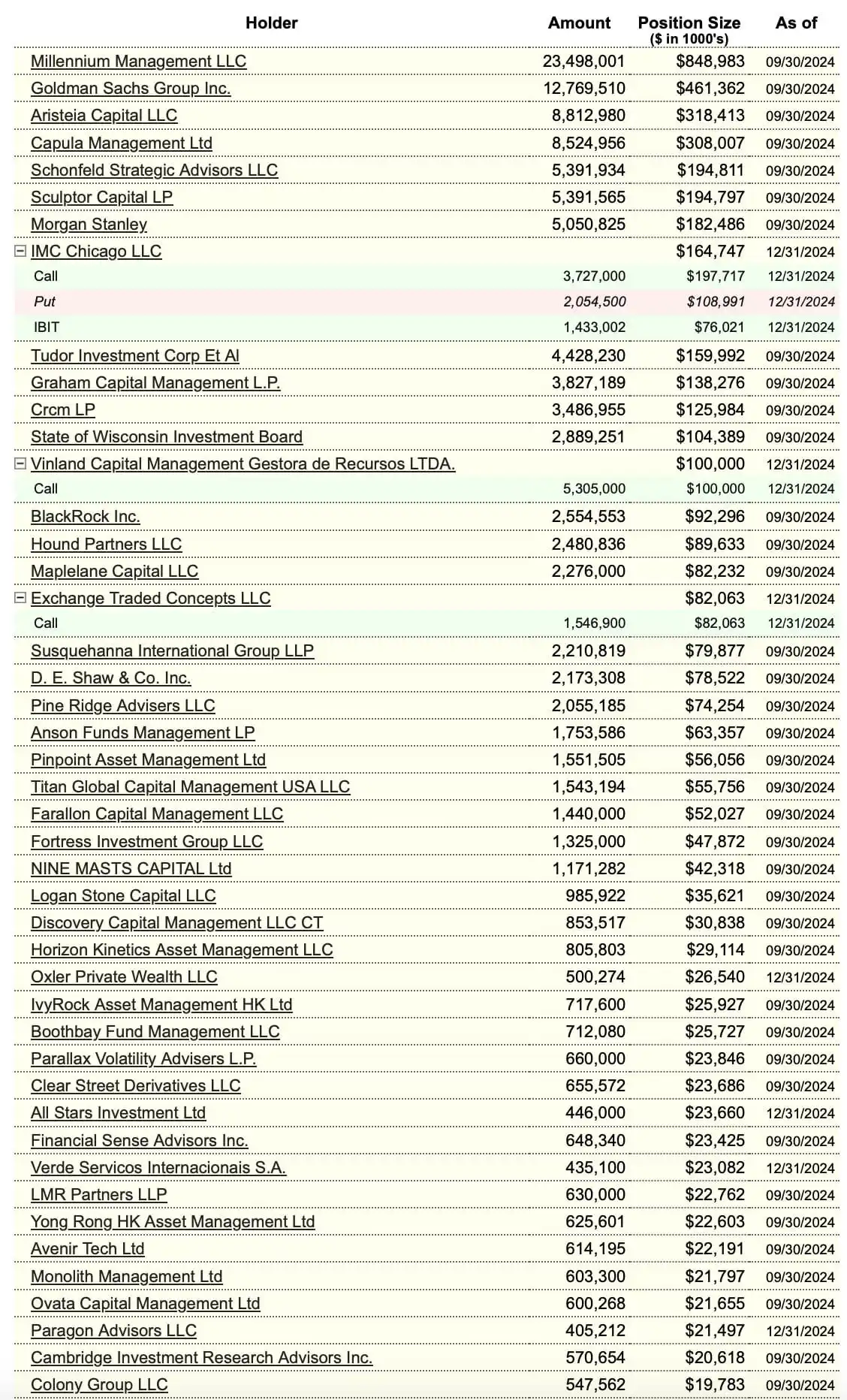

If we delve into the IBIT investor capital table (as analyst TXMC has analyzed), we can clearly see signs of increasing institutional investor demand. This further demonstrates that Bit is attracting an increasingly mature investor base.

Controlled Downside

One of the many advantages of on-chain data is that it can help us analyze investor behavior during periods of stress (such as corrections and downturns).

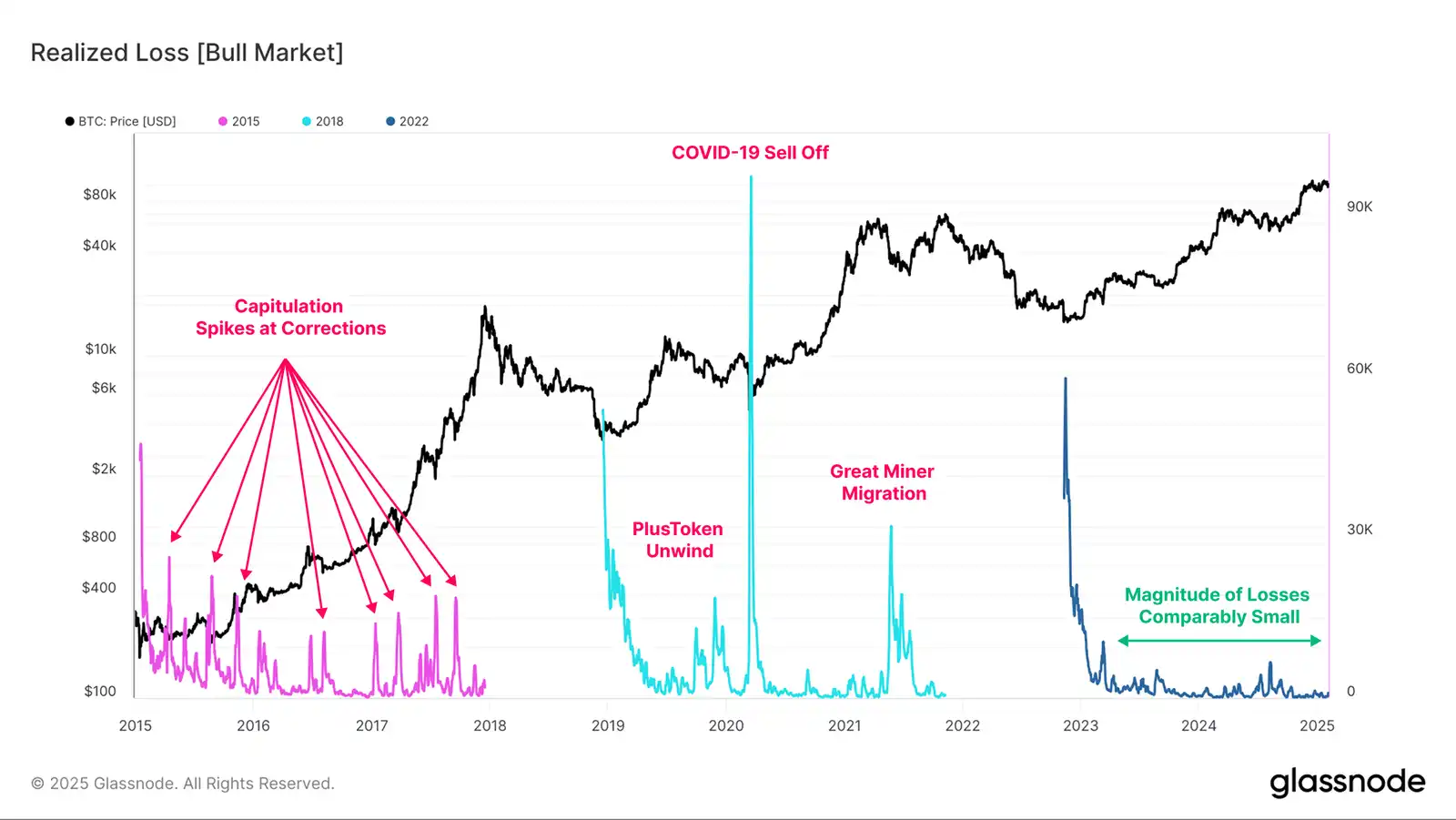

When we assess the actual magnitude of losses locked in during the bull market, our current cycle is still the most conservative. The only notable event of Bit holders suffering significant losses was the yen arbitrage liquidation on August 5th. Apart from that, the magnitude of losses remains relatively small, indicating a more patient, resilient, and price-insensitive investor base.

This is quite different from the structure of previous cycles, which were characterized by multiple local capitulation events during 2015-2018. The 2019-2022 period was more turbulent, experiencing several deep and severe capitulation events, such as the PlusToken unwind in mid-2019, the COVID-19 selloff in March 2020, and the large-scale miner migration in mid-2021.

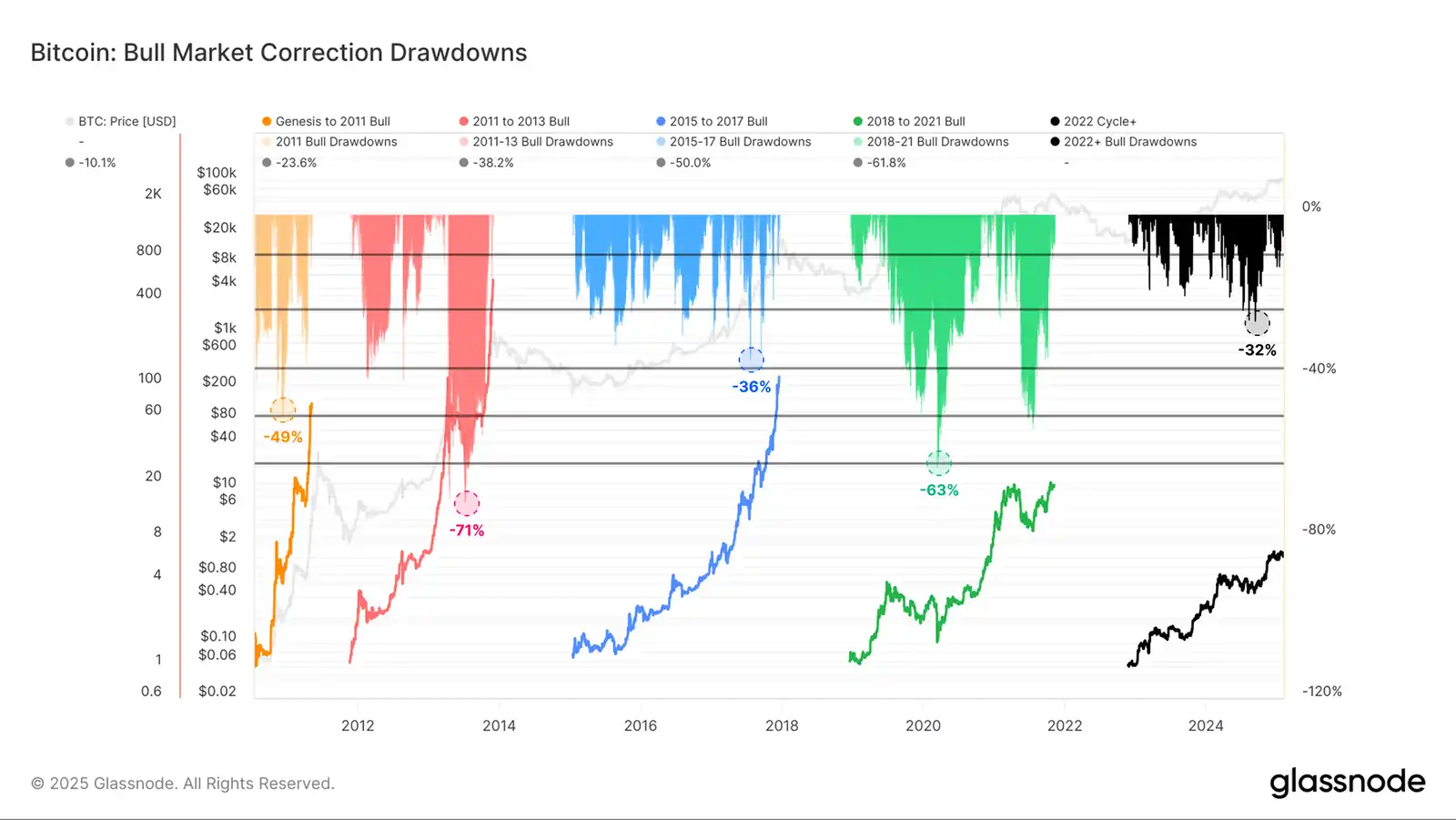

The volatility profile of Bit is also in a state of change, with realized volatility at historical lows for bull markets. The 3-month rolling window realized volatility in this cycle is typically below 50%, whereas in the previous two bull markets, realized volatility often exceeded 80% to 100%.

This reduction in volatility, combined with a relatively calm investor base, is reflected in a more stable price structure. So far, the 2023-25 cycle has essentially been a series of stair-step price movements (an uptrend followed by a consolidation period).

We also see more controlled drawdowns, with the current cycle experiencing the shallowest average drawdown from local highs across all cycles to date.

Conclusion

Bit continues to establish its position as a global macro asset. It remains available for trading, allowing investors to express their market views at any time of the day, while its deep liquidity enables investors to execute large-scale transactions.

Regarding the criticism of Bit's role as a store of value and medium of exchange, the network has attracted over $850 billion in net capital inflows and processes nearly $9 billion in daily transaction volume. These data largely dispel the doubts about these claims.

Recent regulatory changes in the digital asset ecosystem have led to a shift in the investor composition, resulting in a growing presence of mature institutional investors in the Bit market. This more patient, resilient, and price-insensitive investor base helps to reduce the magnitude of drawdowns and lower volatility.

Original link

Welcome to join the official community of BlockBeats:

Telegram subscription group: https://t.me/theblockbeats

Telegram discussion group: https://t.me/BlockBeats_App

Twitter official account: https://twitter.com/BlockBeatsAsia