Source: Seven bottles of robots that don’t get drunk

Introduction: The core business logic of RWA is asset tokenization, which means taking a step forward on the basis of asset securitization , using the technical form of tokens as a carrier to carry the various rights and risks of the underlying assets. Its significance lies in giving full play to the technical advantages of the underlying architecture of blockchain, and has inherent advantages in cost and efficiency in lowering the threshold for investor participation, improving the turnover efficiency of financial products and improving the level of automated execution . However , RWA has relatively high requirements for the degree of dataization of business scenarios, and its application landing is subject to the constraint of "going online first before going on the chain" . What specific factors can accelerate the transition of RWA from being well-received to being popular ? What specific paths can guide the effective investment of market resources? In the current market, what factors can RWA rely on to gain its own living space? Here, based on our deep recognition of the development trend of RWA, we have some cold thinking on the RWA craze in the current market , in order to play the role of eliminating the false and retaining the true, and eliminating interference , so that the industry can concentrate on finding the development path of RWA more efficiently .

Since the beginning of this year, RWA has continued to be a hot topic of great concern worldwide. On the one hand, the United States and the European Union have continuously issued relevant policies to respond to and regulate innovative formats in the fields of asset tokenization and stablecoins. For example, on April 3, the U.S. House of Representatives Financial Services Committee voted to pass the "Stablecoin Transparency and Accountability for a Better Ledger Economy" (STABLE Act), and clarified the reserve and capital requirements and anti-money laundering standards required for the issuance of stablecoins; on the other hand, many financial institutions and industry leaders have announced the launch of tokenization-related products, such as:

Ondo Finance in the United States tokenizes U.S. short-term Treasury bonds (T-Bills), allowing investors to hold and earn Treasury bond returns (about 4-5% annualized);

China Asset Management (Hong Kong) launched the "China Asset Management Hong Kong Dollar Digital Currency Fund", becoming the first tokenized fund for retail investors in the Asia-Pacific region;

Standard Chartered Bank and the Hong Kong Monetary Authority (HKMA) use the blockchain platform eTrade Connect to tokenize trade documents such as letters of credit (LCs) and bills of lading, allowing small and medium-sized enterprises to quickly obtain financing;

Value Partners Group launched a private equity fund token (VPF Token) based on Ethereum. The investment targets include Hong Kong technology start-ups and Southeast Asian infrastructure projects. Investors can redeem fund shares through tokens or transfer them in the over-the-counter market (OTC);

BlackRock and Securitize have partnered to launch a blockchain-based real estate investment fund that allows investors to hold equity in some commercial properties (such as office buildings in New York and San Francisco) through tokens (such as SEC-compliant Reg D securities);

Australia's Maple Finance tokenizes SME loans, and investors can obtain fixed returns ( 8-12% annualized) through MPL tokens;

Switzerland’s Toucan Protocol tokenizes traditional carbon credits (such as Verra-certified carbon offset projects);

Shell Oil UK pilots oil futures contracts trading via blockchain;

Sotheby’s auction house tokenizes high-end artworks through NFT + RWA, allowing investors to purchase fractional ownership.

The above events not only provide support for RWA to become the focus of the industry, but also attract many asset parties to turn their attention to RWA in order to obtain financing through this innovative format, including a large number of small and medium-sized enterprises and individual operators who hope to obtain financing based on physical assets. The main difference between physical assets and financial assets is that holding such assets cannot obtain a certain cash flow . However, the market reaction is very realistic. The RWA issuance that has appeared so far in the world is based on financial assets . (It also includes gold, crude oil and other categories that have both financial attributes and commodity attributes.) There has been no successful issuance based on physical assets. Even RWA projects based on financial assets are often led by traditional financial head institutions or industry leaders. "When will the swallows in front of the halls of the rich and the poor fly into the homes of ordinary people ? " It is still unknown. How does RWA, with the benefits of technology, affect the innovation of financial products? What specific factors can accelerate or hinder the transition from being well-received to being popular? What specific paths can guide the effective investment of market resources and achieve a closed business loop? This article intends to conduct some calm thinking on the hot topic of RWA, in order to provide support for the large-scale application of RWA.

1. Can everything be RWA?

RWA literally means real-world assets, but its core business logic is asset tokenization, which is to go one step further on the basis of asset securitization and use the technical form of tokens as a carrier to carry the various rights and risks represented by the underlying assets . The Hong Kong Securities and Futures Commission defines tokenization as a process involving the recording of asset rights recorded in traditional ledgers on a programmable platform through the use of DLT.

The role and significance of asset tokenization lies in that it can give full play to the technical advantages of the underlying architecture of blockchain. Compared with the existing financial infrastructure (financial electronicization and Internetization), it has inherent advantages from the perspective of cost and efficiency in terms of lowering the threshold for investor participation (mainly reflected in global investor participation, self-service account opening and 7*24 all-weather trading convenience), improving turnover efficiency ( mainly reflected in the absence of intermediary agency participation and clearing and settlement) and improving the level of automated execution (reducing the participation of third-party institutions to reduce operational risks and operating costs). However , its disadvantages are also very obvious, mainly reflected in the fact that asset tokenization has relatively high requirements for the degree of dataization of business scenarios and is subject to the constraint of "going online first to go on the chain". For example, in the financial industry, all factors that can affect the risk and return of assets must be digitized, and can provide full-dimensional and real-time continuous data as support for the risk and return assessment of financial assets in order to achieve complete asset tokenization .

This requirement is obviously too high , but it is determined by the technical characteristics of blockchain and is a reality that we must recognize. To put it in simple terms, blockchain is just a database with its own reconciliation mechanism. It is deaf and blind to the outside world and can only receive external data input, but cannot actively obtain data . What if you want to actively obtain data? Then you must use IoT devices as the source of data collection. How to ensure that the data collected by IoT devices can be 100% authentic on the chain ? One method is technical means. If the entire business process is fully automated and no human participation is required throughout the process, then the data is of course credible; another method is to use the supervision of a trusted third-party organization as a credit endorsement . The first method obviously depends on the degree of intelligence of the business scenario, and at this stage, the second method, that is, first relying on a " mixed solution " to achieve data credibility, and then establishing a business model such as RWA based on trusted data, is an effective "stopgap measure" . Therefore, the margin of RWA business lies in the acquisition of trusted data. In the current state, it is obviously not everything can be RWA.

Furthermore , since the essence of RWA is asset tokenization, its core logic is reflected in financial logic. The basic principle of matching risks and returns emphasized by financial business should play a fundamental role in RWA product design . This principle is also the core standard for selecting RWA priority landing scenarios in the current market . We know that the main risk-return characteristics of the underlying assets are a comprehensive reflection of the changes in various factors in the business scenario, and will not change because of whether its carrier is a token . Therefore, whether it can provide sufficient credible data to help eliminate the information asymmetry of investors becomes an effective method for selecting RWA priority landing scenarios. In industry practice, Ant Financial announced that it would give priority to the issuance of RWA in the new energy track , because the new energy industry chain, whether it is distributed power generation or charging piles, of course, also includes wind power generation and energy storage, generally operates based on intelligent systems , and has the characteristics of synchronous cash flow and information flow . The issuance of RWA based on new energy underlying assets will greatly reduce the information asymmetry faced by investors , and thus provide investors with an investment opportunity with clear returns and transparent risks . If charging piles are also charged manually like traditional parking lots, then RWA for such assets will be meaningless.

This model of risk control through real-time data obviously goes beyond the scope of what traditional financial institutions are good at, such as asset mortgages . Therefore , from the perspective of controllable risks , Ant Financial is willing to recommend this type of asset to its customers as a "digital investment bank" . Otherwise, if traditional financial institutions cannot achieve risk control purposes based on traditional risk control methods , what reason does Ant Financial have to package them as tokens and recommend them to its customers?

For the same reason, existing technical conditions make it impossible to put the main data required for the valuation of physical assets on the chain, and it is impossible to provide reliable data to support risk control . Overall, the RWA of physical assets cannot find an effective path.

Of course, according to the standard of "synchronization of data flow and cash flow", it is not only the new energy industry that can be used as the priority scenario for RWA. For example, cars with autonomous driving functions, whether for financial leasing or shared travel, can be used as ideal basic assets for RWA . As the degree of digitalization in various industries increases, issuing RWA based on these industry scenarios will give the market greater room for imagination.

2. Are all traditional financial products worth reconstructing using RWA?

The core logic based on RWA is mainly reflected in the premise of financial logic. Especially after the financial industry has experienced electronicization and Internetization, financial assets naturally exist in the form of data. The degree of dataization of the financial industry chain has been greatly improved. Compared with physical assets , financial assets are easier to achieve the goals of lowering the participation threshold, improving turnover efficiency and improving the level of automation through tokenization. So, are all financial products worth reconstructing with RWA? Obviously not. According to the previous analysis, if the risk control ability of financial institutions cannot be significantly improved by providing more credible data , "going on the chain" is neither worth the loss nor meaningful. A more realistic path for the tokenization of financial assets is a "mixed solution", that is, first completing asset securitization based on the professional capabilities of financial institutions, and then anchoring the securitized assets and specific tokens to obtain the advantages of "going on the chain" at the capital end and some operating ends of financial assets. Below, we take the tokenization of REITs as an example to illustrate the basic characteristics of this model.

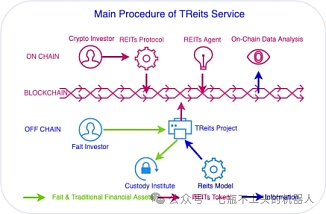

FTJLabs is the first in the world to propose the RWA project REITs, which connects traditional financial assets and on-chain liquidity based on a compliance architecture. The project focuses on Reits assets listed on global exchanges , builds Reits investment portfolios by issuing funds, and issues REITs Tokens with fund shares as underlying assets; each REITs Token corresponds to a share of a specific fund product; investors can obtain REITs Tokens through the Reits assets, legal currency or stablecoins corresponding to the investment portfolio, and can trade them anywhere and at any time globally, and can also build investment portfolios with different return characteristics based on these token assets.

On the chain, the project develops REITs Protocle, which supports the automatic execution of REITs Token distribution, trading, dividends and other functions , and extracts data from blockchain public information to serve investors through the On-Chain Data Analysis module . Off the chain, the project selects licensed institutions to undertake the custody function of assets on the chain, and issues fund net value data in real time to provide reference for REITs Token secondary market transactions, and regularly issues asset custody reports to ensure that the on-chain assets and custody assets are equal in value.

Based on the above functions , tokenization gives Reits assets global liquidity, making it easier to discover their value. It can also provide a wider range of investors with an investment target with unique risk-return characteristics. The investment portfolio that originally required cross-exchange operations can now be achieved with just one token.

In this product, two designs can better reflect the characteristics of product design. First, the asset custodian plays a basic supporting role in the value of REITs Token . Based on its own principal credit, the asset custodian discloses the net value of the managed assets through regular reports to ensure that the value of REITs Token is equally anchored to the managed assets. Second, the project only uses exchange-listed Reits as underlying assets. The asset custodian can provide reference prices for REITs Token based on the price information provided by the exchange . If the underlying assets of the project also include private Reits products, the asset custodian will not be able to provide reference quotations for REITs Token , and thus cannot guarantee the asset transparency of REITs Token , which will further affect its liquidity.

3. RWA, a wealth opportunity for mass participation?

Under the current circumstances, "mainland assets + Hong Kong funds" is a more ideal model for conducting RWA business, but the Hong Kong Securities and Futures Commission ( SFC) maintains a cautious attitude towards the supervision of asset tokenization , and has made clear regulations on the identification of qualified investors and fundraising methods to avoid investors from taking excessive risks.

In 2019, the Hong Kong Securities and Futures Commission issued the "Statement on the Issuance of Security Tokens", imposing the restriction of "professional investors only (personal financial assets ≥ HK$8 million or licensed institutions)" on the distribution and promotion of security tokens. In November 2023, the Hong Kong Securities and Futures Commission issued two circulars, "Circular on Intermediaries Engaged in Tokenized Securities-Related Activities" and "Circular on Tokenized Securities and Futures Commission-Approved Investment Products", no longer treating tokenized securities as "complex products" and no longer limiting their sale and marketing to professional investors; however, the Securities and Futures Commission retained a provision of the "2019 Statement", namely that intermediaries intending to engage in tokenized securities-related activities should discuss their business plans with the Securities and Futures Commission in advance. Tokenized securities cannot be directly issued to all investors.

In December 2023, Harvest Global cooperated with Meta Lab HK to tokenize its fixed-income fund products, but mainly for professional investors. On September 10, 2023, Taiji Capital launched Hong Kong's first real estate fund security token (PRINCE Token) for "professional investors". The token is the first fund tokenization fundraising product approved by the Hong Kong Securities and Futures Commission . The fundraising target is about 100 million yuan, and the minimum investment standard is 1,000 Hong Kong dollars, which is much lower than the 1 million US dollars generally required to invest in private real estate funds . However, according to the relevant regulations of the Hong Kong Securities and Futures Commission, Hong Kong's licensed digital asset exchanges cannot accept registrations from mainland users, and mainland China also explicitly prohibits relevant institutions ( for mainland residents) from providing virtual asset trading services. Even if Hong Kong allows licensed institutions to provide virtual asset trading services to retail investors, mainland users cannot directly participate in it.

In addition, the RWA products that have been successfully issued at this stage often have the attributes of fixed income or income sharing rights. The relatively fixed expected rate of return is more suitable for asset allocation by institutions with larger capital scale. Therefore, at this stage, RWA is still far from the wealth opportunities in the minds of general investors.

4. Is RWA an ideal channel for SMEs to obtain financing?

RWA cannot provide the imagined returns for general investors on the funding side, so can it provide an ideal channel for small and medium-sized enterprises to obtain financing on the asset side?

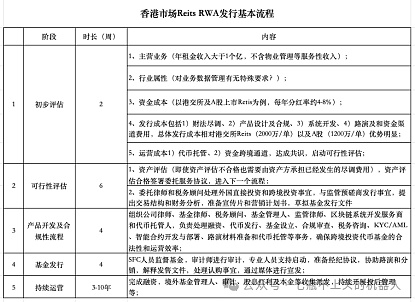

As we all know, financing costs are the core factor that affects the choice of corporate financing channels . According to market news, the issuance cost of RWA in Hong Kong generally includes two parts : issuance fees and capital costs. Among them, capital costs are mainly determined by the risk-return characteristics of the assets and the capital market environment during the issuance period (the current market forecast is generally 6-10% annualized ); and issuance costs include due diligence costs, product design and development costs , cross-border funding channels, and post-management costs . The total of various issuance costs is about millions of levels. According to the issuance cost, the lower limit of the underlying assets of RWA can be deduced . Obviously, it is not economical to issue RWA with an asset scale of less than 100 million. In addition to the capital cost, there is also the time cost. This article takes the issuance of tokenized REITs as an example to sort out the asset screening criteria, the main issuance process and the time period as shown in Table 1:

In summary, under the current market environment, RWA issuance has high thresholds in terms of financing costs and financing time, and is not an ideal channel for most small and medium-sized enterprises to obtain financing; and for large enterprises whose financial indicators have reached or are close to those of the Hong Kong Stock Exchange, the three digital asset exchanges that are currently the main channels for RWA issuance in the Hong Kong market (as of May 2025, a total of 10 institutions have been authorized by the Hong Kong Securities Regulatory Commission to engage in digital asset trading-related businesses, but only three platforms have been launched and can provide external transactions ) have certain advantages in issuance costs, but obviously have obvious disadvantages in terms of capital costs and fundraising efficiency . For those with relatively stable asset returns and large capital demand, they would rather give priority to listing and issuing on the Hong Kong Stock Exchange , and only those whose financial indicators cannot meet the issuance standards of the Hong Kong Stock Exchange are more willing to spend a higher cost to choose digital asset trading platforms for RWA issuance. This is also the main reason why RWA is difficult to land in the current Hong Kong market .

5. Finance or Internet? RWA’s way to survive in the current market!

Whether from the definition of tokenized securities by the Hong Kong Securities Regulatory Commission or the general consensus of the market, RWA based on financial assets has not changed its financial attributes, but only materialized the original risk and return characteristics of the underlying assets with tokens as new technical carriers . With tokens as new carriers , financial products have unprecedented advantages in transaction convenience , transaction efficiency and process transparency. If we go back hundreds of years, in 1397 , when the Medici family in Florence first used bills of exchange to create cross-border exchange business in Europe; in 1602 , when the Amsterdam Stock Exchange launched the world's first stock, the Dutch East India Company ; or in 1844 , when the Bank of England monopolized the right to issue banknotes in the UK and took the first step towards becoming a global central bank, let them make a choice again. They should choose distributed ledgers as the underlying architecture of these pioneering financial instruments. After all, the advantages of cost and efficiency are obvious .

But this is just a romantic assumption, time cannot be reversed . After hundreds of years of accumulation, the financial industry has completed a profound binding with the global economic system in terms of product form , service breadth and depth . RWA, which started with securities tokenization , is unlikely to completely reconstruct all traditional financial products . Just like the penetration of the Internet into traditional society, RWA is more likely to find its own opportunities by starting from the most cost-effective and technologically superior fields .

Although artificial intelligence has defeated humans in specialized fields such as chess and Go , it is unlikely to replace humans in providing personalized financial services to all investors . The advantage of the Internet is first reflected in providing services to large-scale long-tail users. Therefore, when traditional financial institutions have occupied a major market share based on their service experience for head customers, RWA, which is based on financial attributes as its basic business logic, has to rely on the attributes of the Internet to find its own living space.

In the short term, RWA needs to withstand the minimum requirements of market launch for traffic accumulation. It is a beneficial attempt to verify the specific product form in various scenarios, especially in the track where C-end users have a good degree of participation and are in line with the current industry development trend, such as games and entertainment, where opportunities may be greater; in the medium and long term, when new energy power supply such as solar energy and wind energy can be seamlessly connected with traditional power grids through intelligent systems and automatically provide charging services; when taxis with self-driving functions have a significantly lower comprehensive use cost than families buying cars; when agents can perform more tasks on behalf of humans under the support of artificial intelligence , computing power, models and data become the main production factors, and humans no longer need to directly participate in production , the role of RWA will be irreplaceable . As an innovative financial service model , RWA will grow irreversibly into the mainstream form of financial services along with the development and growth of the intelligent economy that has the same genes and is closely integrated with it . After World War II , the rise of the comprehensive national strength of the United States and the replacement of the British pound as the "global hard currency" is a good example .

Last words

The current RWA is still in the proof-of-concept stage, but we all agree that trends represent the future. We are here to have some sober reflections on the RWA craze, not to deny RWA and its innovative exploration . On the contrary, it is based on our deep recognition of its development trend that we are willing to separate the true from the false, eliminate interference, and focus on finding a more efficient development path for it. It is still the old saying reflected by Gartner's new technology application curve that for a new technology, people often overestimate its short-term effects and underestimate its long-term effects. According to the idea of verifying the product prototype, perhaps we can find a more suitable living space for RWA at the moment !