introduction

The tokenization of real-world assets (RWAs) is reshaping the global financial landscape.

By converting traditional assets such as real estate, bonds, and commodities into digital tokens on the blockchain, RWA significantly improves asset liquidity, lowers investment barriers, and provides unprecedented opportunities for global investors.

The rise of RWAs is not only a breakthrough in blockchain technology, but also a milestone in the integration of traditional finance and the crypto economy. From MakerDAO's issuance of the DAI stablecoin, collateralized by US Treasury bonds, to BlackRock's tokenization of fund shares, this movement is evolving into an experiment in the value integration of institutional capital and crypto-native protocols.

This report systematically reviews the differentiated landscape of the RWA ecosystem in 2025 , focusing on its main categories and representative projects , to help everyone understand the current status of industry development and quickly find reference projects.

The report is approximately 10,000 words and is expected to take 10 minutes to read. (This report is produced by DePINOne Labs. Please contact us for reprinting.)

RWA: Reconstructing the value flow of traditional assets on the chain

By the end of 2024, total assets in the RWA tokenized market (excluding stablecoins) exceeded $50 billion, a nearly 67% increase from approximately $30 billion at the beginning of the year. This growth reflects widespread interest from both institutional and retail investors.

The Security Token Market Report shows that over 1,200 unique security tokens are trading on various platforms, covering debt, equity, real estate, and commodities. Tokenized trading volume has been steadily climbing each month, reaching a peak market capitalization of $14 billion in December alone.

- Real estate dominated the market. Issuers announced $24 billion in tokenization projects, of which $5.4 billion was already on-chain. Platforms such as RealT and RedSwan CRE led the way in both residential and commercial real estate. Secondary market trading volume for tokenized real estate is projected to increase by 40% year-over-year in 2024, demonstrating its growing liquidity.

- Tokenized bonds also garnered attention. Germany (59.8%), China (13.1%), Hong Kong (7.5%), and other European markets accounted for a total of $12.8 billion in issuance. Notable examples include Germany's digital bond issuance platform and the Hong Kong Monetary Authority's green bond pilot program. Bond tokenization reduces settlement times from T+2 days to near-instant on-chain settlement, attracting banks such as Deutsche Börse and JPMorgan Chase to explore this model.

- Liquidity funds are rapidly gaining adoption. Franklin Templeton's Franklin On-Chain U.S. Government Money Fund (BENJI) amassed $375 million in AUM within six weeks of its launch, exceeding $709 million by April 2025. Hashnote's USYC soon surpassed BENJI, leading the market with $648.5 million in AUM at year-end. These tokenized money market products address market demand for safe, yield-generating assets that can also serve as DeFi collateral on platforms like FalconX and Hidden Road.

These figures highlight the rapid adoption of RWA tokenization. They highlight a maturing market where tokenized assets can provide real-world liquidity, reduce costs, and enable new investment opportunities.

RWA ecological classification and representative projects

Treasury bonds and securities

Treasury bonds and securities are the core areas of RWA tokenization. The underlying assets primarily consist of bonds issued by sovereign states (with US Treasuries being the primary target) and standardized financial securities. Current market coverage is concentrated in the US Treasury market (accounting for over 90%), with a gradual expansion into European sovereign bonds. Representative projects include Ondo Finance (a tokenized US Treasury ETF). This category offers low volatility and stable income streams. By using fragmented tokens, the traditional US$100,000 investment threshold for Treasury bonds is lowered, enabling 24/7 on-chain clearing, providing compliant US dollar yield exposure to global investors.

Ondo Finance

https://ondo.finance/

Ondo Finance focuses on tokenizing U.S. Treasury bonds and fixed-income products. Its OUSG Fund (Ondo Short-Term US Government Bond Fund) provides investors with a blockchain-based entry point to Treasury bond returns.

In 2024, Ondo's assets under management will exceed US$1 billion, and it will be integrated with multiple DeFi protocols (such as Aave) to achieve on-chain reinvestment of profits.

In 2025, Ondo Finance further expanded the bridging capabilities of its USDY token to the Solana blockchain, enabling cross-ecosystem liquidity through LayerZero. This development enhanced its competitiveness in the institutional-grade RWA market.

BUIDL by BlackRock

https://www.blackrock.com/

BlackRock's BUIDL Fund, a tokenized money market fund operating on Ethereum with nearly $2 billion in assets under management, has attracted widespread attention from institutional investors by offering a transparent and efficient investment approach using blockchain technology.

By collaborating with Securitize, BUIDL ensures compliance and security, becoming a benchmark project for the integration of traditional finance and blockchain.

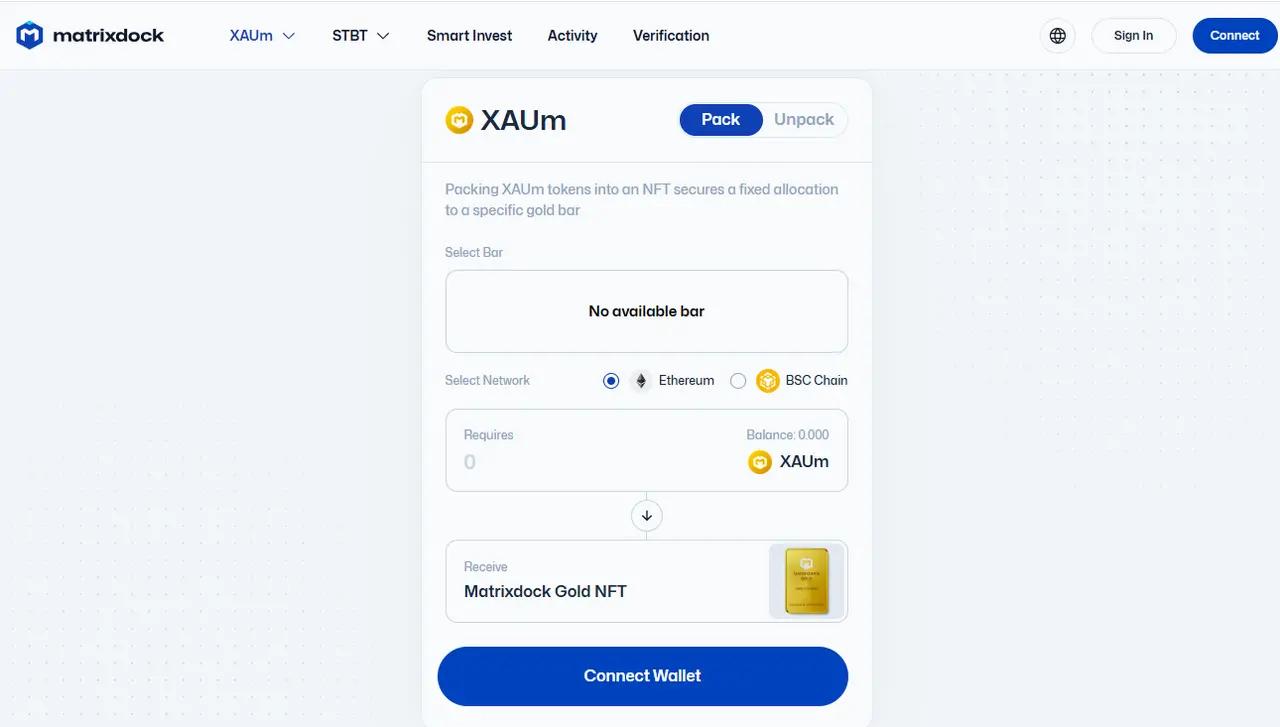

Matrixdock

https://www.matrixdock.com/

Matrixdock is a multi-chain RWA platform that focuses on tokenizing traditional financial assets.

By partnering with Chainlink, Matrixdock ensures accurate and reliable asset pricing, providing investors with a secure investment environment. Matrixdock's platform supports multiple asset classes, including government bonds and ETFs, and plans to further expand its market coverage by 2025.

Other projects

Backed Finance, Compound (COMP), OUSG, Midas, Dusk Network, Finteum, OpenEden

Private credit

RWA Private Credit leverages commercial real estate mortgages, SME accounts receivable, and supply chain finance assets as underlying assets, focusing on addressing the financing needs of businesses in emerging markets (for example, Southeast Asian supply chain finance accounts for 35% of Centrifuge's asset size). Its advantage lies in its automated cash flow allocation through smart contracts, addressing pain points in the traditional credit market, such as redundant intermediaries and inefficient cross-border settlement. The Goldfinch protocol, a representative project, maintains a bad debt rate below 1.2%, demonstrating the transformative power of blockchain technology in credit risk assessment.

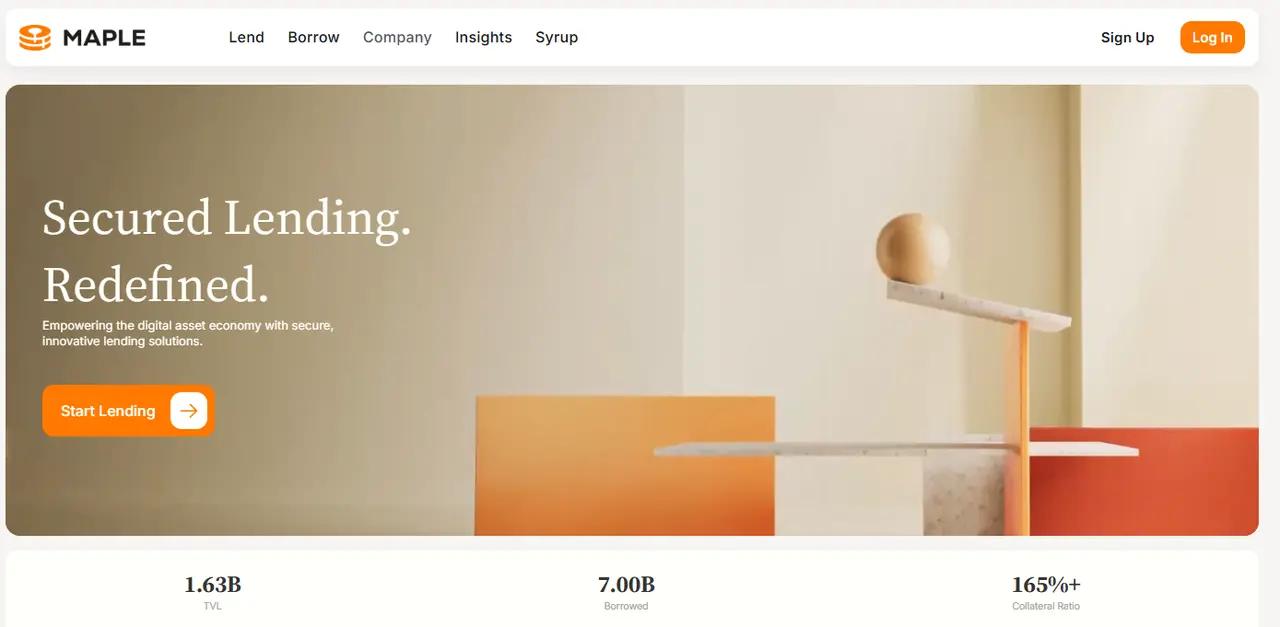

Maple

https://maple.finance/

Maple is a decentralized lending platform focused on providing on-chain credit services to institutions and businesses. Through its governance token, MPL, Maple enables community governance and risk management, and its loan pool size has grown significantly in 2024.

In 2025, Maple launched a BTC income strategy, offering an annualized yield of 5.1%, which attracted the attention of traditional financial players.

Goldfinch

https://www.goldfinch.finance/

Goldfinch specializes in private lending in emerging markets, providing loans to borrowers without a credit history through blockchain technology. Investors can participate in the lending pool using GOLD tokens, earning an annualized return of 8-15%.

In 2024, Goldfinch's active loan value reached US$446 million, and it plans to expand to the African and Southeast Asian markets in 2025 to further promote financial inclusion.

Centrifuge

https://centrifuge.io/

Centrifuge tokenizes real-world assets like invoices and loans through its Tinlake protocol, providing low-cost financing for small and medium-sized enterprises. By 2024, Centrifuge's tokenized asset pool exceeded $500 million, and it partnered with MakerDAO to bring private credit to DeFi. In 2025, Centrifuge released version 3, further optimizing the efficiency and scalability of on-chain finance.

Other projects

Defactor ($FACTR), TrueFi ($TRU), Clearpool ($CPOOL), Credix Finance, Intain, FortunaFi, Credefi Finance, KKR, Dinari, Creditcoin (CTC)

real estate

The underlying real estate RWA portfolio encompasses commercial real estate (58%), residential properties (32%), and land development projects (10%), primarily active in the US REITs market, Dubai Free Zones, and Southeast Asian tourism real estate. Using a hierarchical token structure (such as RealT's home equity NFT), it enables fragmented investment in multi-million-dollar assets per property. Combined with an automated on-chain distribution mechanism for rental income, this addresses the core pain points of traditional real estate investment, including poor liquidity (average exit period of 6-8 months) and high management costs (average annual management fees of 3-5%). The Propy platform also pioneered an on-chain property rights registration system, completing over 23,000 cross-border real estate transactions.

Propy

https://propy.com/

Propy leverages blockchain technology to streamline real estate transactions, providing decentralized land registries and online homebuying services. Propy's transaction volume in the US and European markets is projected to grow by 50% in 2024, enabling investors to purchase fractional shares in properties. Propy's platform ensures transaction transparency and security through smart contracts, and the company plans to expand into Asia in 2025.

RealT

https://propy.com/

RealT specializes in tokenizing US residential properties, allowing investors to purchase property tokens for as little as $50. Token holders receive rental dividends and returns on property appreciation. By 2024, RealT's tokenized real estate assets will account for 60% of the total market value. The company plans to expand into commercial real estate by 2025 to attract more institutional investors.

Other projects

LABS Group ($LABS), Tangible ($TNGBL), Parcl, Realio Network ($RIO), PropChain, Homebase, LandX Finance, PlayEstates

Stablecoins

Stablecoins, as on-chain representations of fiat assets, use sovereign currencies like the US dollar and the euro as their underlying reserves (USDC and USDT hold over 96% of their reserves in US dollars), achieving value stability through a 1:1 peg mechanism. The current market size has reached $140 billion, covering cross-border payment scenarios in over 200 countries/regions, with an average daily settlement volume exceeding $10 billion. Their core advantage lies in combining the stability of traditional finance with the 24/7 global liquidity of blockchain. Circle, the issuer of USDC, holds both a New York BitLicense and a UK Electronic Money Institution license. Its reserve assets undergo monthly third-party audits to ensure compliance and transparency.

Tether (USDT)

https://tether.to/

As the largest stablecoin by market capitalization, USDT (USDT) is backed by US dollar reserves and short-term bonds and is widely used in crypto trading and DeFi protocols. In 2024, USDT's on-chain transaction volume accounted for over 60% of the stablecoin market. Tether generates returns by investing in highly liquid assets, such as US Treasury bonds, while maintaining a 1:1 USD peg.

Circle (USDC)

https://www.circle.com/

USDC is known for its transparent reserve management and regulatory compliance, with its reserve assets consisting of cash and short-term Treasury bills. Circle has partnered with Coinbase to provide seamless fiat-to-crypto conversions for institutional and retail users using USDC. USDC's use in cross-border payments and DeFi lending is expected to grow further in 2025, solidifying its market position.

Other projects

MakerDAO($MKR), Reserve Rights (RSR), OpenEden OpenDollar (USDO), Compounding OpenDollar (CUSDO)

precious metals

Precious metals RWAs use London Bullion Market Association (LBMA)-certified physical gold (82%), silver (15%), and platinum group metals (3%) as underlying assets. They offer divisible investments in as little as one gram of gold (approximately $65) through on-chain certificates. Representative projects such as PAX Gold (PAXG) and Tether Gold (XAUT) store physical gold bars with top-tier custodians like Brink's, with quarterly audits. With an annualized volatility of less than 8% and a correlation of only 0.2 with Bitcoin, these assets have become a crucial safe-haven asset in crypto portfolios. On-chain gold trading volume surged 340% year-over-year in 2023.

Paxos

https://paxos.com/

Each PAXG (PAX Gold) token issued by Paxos corresponds to a one-ounce London Good Delivery gold bar, providing investors with a convenient gold investment channel. Paxos also issues other stablecoins, such as USDP, committed to providing secure and compliant digital assets, and its market share has steadily increased in 2024.

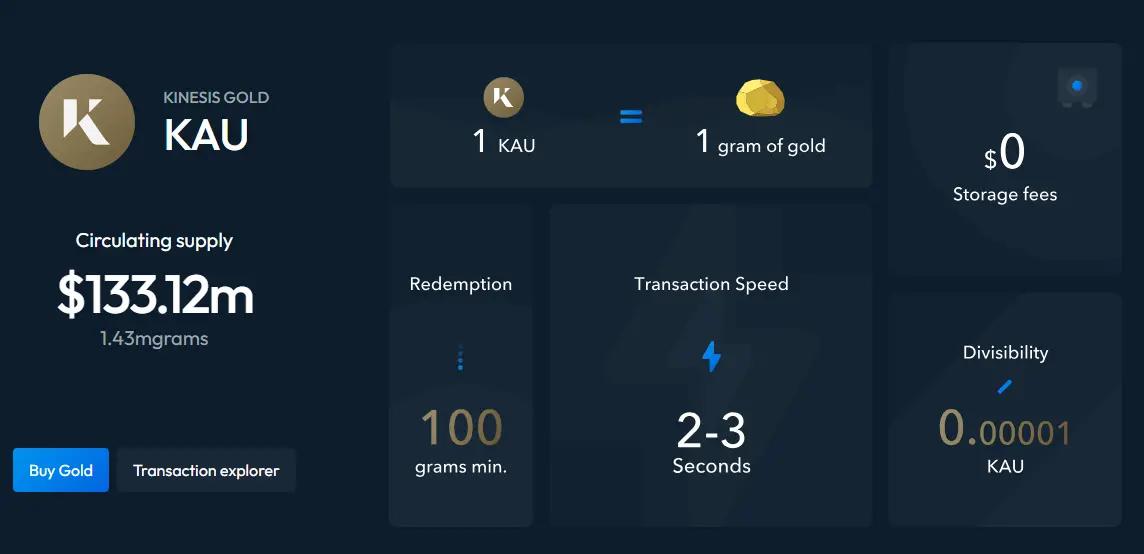

Kinesis Gold

https://kinesis.money/gold/

Kinesis Gold (KAU) is a digital currency. Each KAU is backed by one gram of pure gold, stored in fully insured and audited vaults on your behalf. KAU allows you to spend, trade, send, and earn physical gold anywhere in the world.

A true stablecoin, KAU allows cryptocurrency traders to easily exit volatile markets and enter the enduring value of physical gold, while earning a monthly yield on the precious metal through transaction fee revenue redistributed among users. This yield is earned by holding assets on the Kinesis platform and by spending KAU on the Kinesis virtual card. The card enables users to spend gold and cryptocurrencies with real-time, instant conversions at over 80 million locations worldwide.

Uranium308

https://u3o8.co/

Uranium308 (U3O8) is a tokenized precious metal project.

According to a Canaccord Genuity report from September 2021, the total global uranium supply is approximately 150 million pounds, which, at the current price of $45 per pound, amounts to approximately $6.7 billion per year. Uranium supply is projected to increase to approximately 250 million pounds by 2035, but demand will continue to outstrip supply.

Other projects

LODE, Project 79, Ethena, Cache Gold, Meld Gold, Aurus, Tether Gold (XAUT), Quorium (QGOLD)

Carbon assets/renewable finance (ReFi)

RWA carbon assets refer to carbon emission rights such as carbon credits and carbon quotas recorded in the form of digital tokens through blockchain technology on the RWA (Real World Assets) platform to achieve the digitization and segmentation of assets, thereby increasing their liquidity and transaction efficiency.

On-chain regenerative finance projects are a relatively new field even in traditional finance, aiming to solve real-world social and environmental problems by leveraging blockchain.

Toucan Protocol

https://toucan.earth/

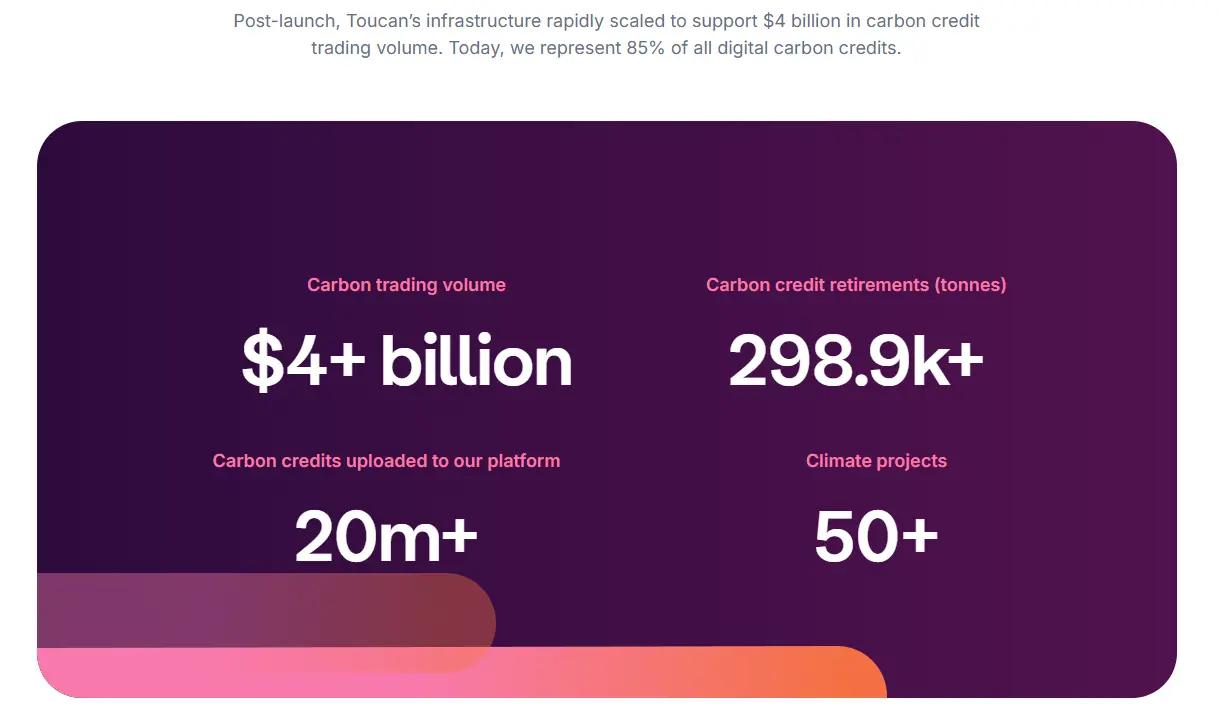

Toucan tokenizes carbon credits, creating an on-chain carbon market that allows businesses and individuals to purchase carbon offset tokens. By 2024, Toucan's carbon token trading volume will exceed 100 million tons of CO2 equivalent. By 2025, Toucan will continue to play a key role in building carbon market infrastructure, promoting transparency and efficiency in the carbon removal sector.

Flowcarbon

https://www.flowcarbon.com/

Flowcarbon specializes in the on-chain trading and management of carbon credits, collaborating with traditional energy companies to advance the carbon market. Flowcarbon's platform provides investors with transparent and efficient carbon credit investment opportunities, and the company expects to further expand its market influence by 2025.

KlimaDAO

https://www.klimadao.finance/

KlimaDAO promotes climate finance through tokenized carbon credits. KLIMA token holders can participate in the governance of the carbon market. By 2025, KlimaDAO will collaborate with traditional energy companies to expand the application of carbon credit tokenization and become a leading project in the ReFi space.

Other projects

Regen Network ($REGEN), Agro Global Token

Art and collectibles

The underlying asset class of Artwork RWA encompasses museum-quality collections (such as Picasso paintings), luxury goods (Patek Philippe watches), and cultural IP (NBA player trading cards). Currently, the auction market primarily focuses on Europe and the United States (Sotheby's NFT auction sales reached $120 million in 2023). Fractional ownership tokens address the liquidity challenges of the billion-dollar art market. Furthermore, the immutable nature of NFTs is leveraged to create digital twin certificates, reducing the provenance time of Christie's auction items from an average of 14 days to instant on-chain verification. However, it's important to note the compliance costs associated with the reliance on third-party certification bodies (such as ARTFRAME's AI authentication system) for the valuation of non-standard assets.

Courtyard.io

https://courtyard.io/

Courtyard.io is an art tokenization platform that allows investors to hold partial ownership of artworks through the purchase of NFTs. The platform supports secondary market trading of artworks, enhancing their liquidity and leading to significant growth in trading volume in 2024.

Freeport

https://www.freeport.art/

Freeport is a storage and management platform focused on high-value artworks and collectibles. It provides secure and transparent ownership records through blockchain technology, allowing users to invest in fragmented artworks with tokens on Ethereum.

Freeport's platform provides convenient on-chain transaction services for art owners and is expected to attract more high-end collectors by 2025.

Other projects

Curio ($CUR), Galileo Protocol, Lingo, Golteum, ClubRare, Artrade (ATR), Keeta

RWA Infrastructure

The RWA infrastructure layer comprises a compliance framework (Security Token Standard), cross-chain protocols (such as Circle CCTP), and a legal entity structure (Special Purpose Vehicle). Securitize's DS Protocol has facilitated the compliant issuance of over 400 RWA assets. The technology stack in this area is trending toward modularity, with Chainlink's Proof of Reserve price feeds being adopted by 85% of RWA projects. The infrastructure market is projected to reach $4.7 billion by 2025 (according to a Traceni report). Its development will directly impact the development of compliant channels for bringing trillions of dollars of traditional assets onto blockchains.

Plume

https://plume.org/

Plume is an EVM-compatible public blockchain built for the next generation of real-world assets (RWAs). We not only tokenize assets, but also create a way to seamlessly use them like cryptocurrencies: stake, redeem, lend, borrow, recycle, and more.

Plume is building a permissionless, transparent, and demand-driven financial system where anyone can access high-quality assets, trade freely, and innovate with new financial tools.

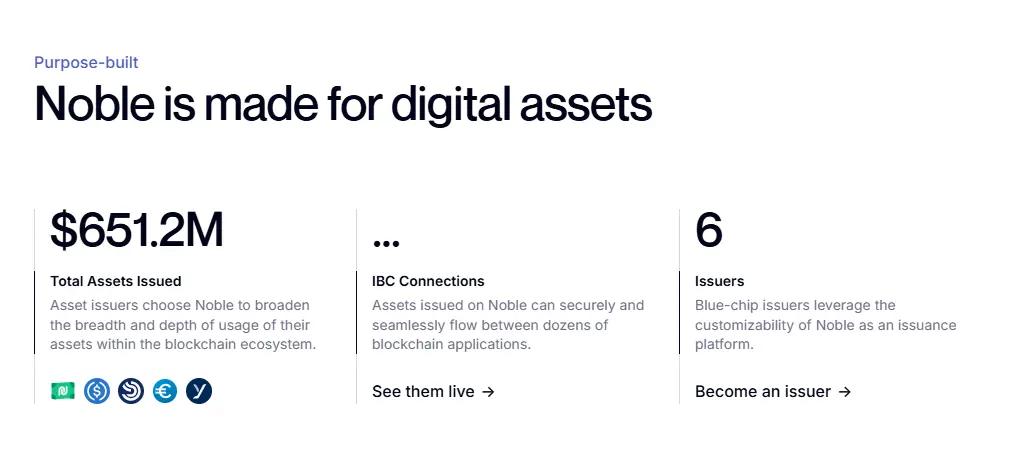

Noble

https://www.noble.xyz/

Noble is a Cosmos application-specific blockchain built for native asset issuance. Noble brings the efficiency and interoperability of native assets to the broader Cosmos ecosystem, starting with USDC.

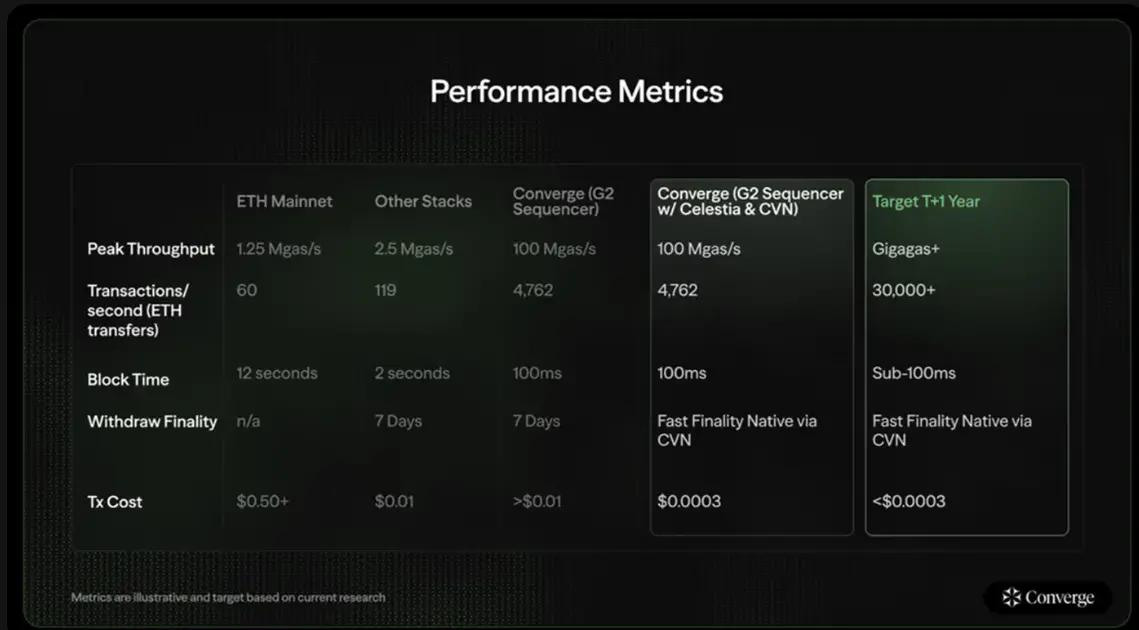

Converge

https://www.convergeonchain.xyz/

Converge is moving towards the most ambitious goal in the cryptocurrency space today: bringing billions of dollars of institutional capital on-chain and achieving the integration of risk-weighted assets (RWA) and DeFi.

Converge is building various financial applications on top of Ethena and Securitize. The combined TVL/AUM (Total Asset Under Management) of Ethena and Securitize is approaching $10 billion, making Converge poised to become one of the largest blockchain networks currently.

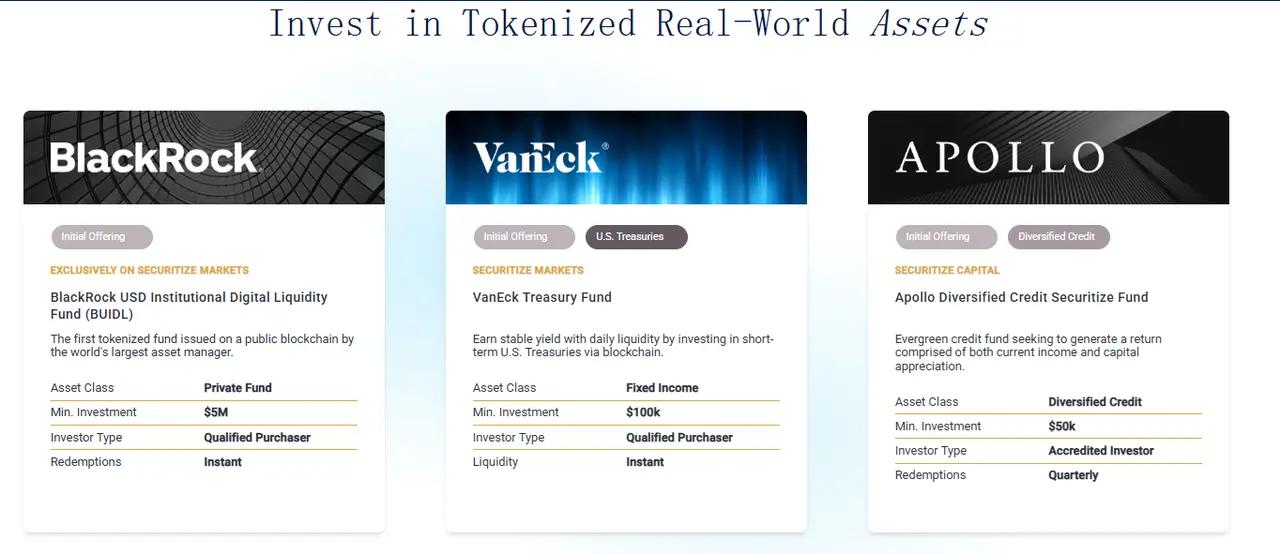

Securitize

https://securitize.io/

Securitize is a leader in tokenizing real-world assets, with over $1 billion in on-chain assets issued and partnering with top issuers: BackRock, KKR, Hamilton Lane, etc.

Other projects

ELYSIA ($ELFI), Tokeny Solutions, StrikeX ($STRX), INX ($INX), Polytrade, Sologenic, Polymesh Network, MANTRAO ($OM), Provenance ($HASH), SpruceID, Quadrata, Swarm Markets ($SMT)

RWA tokenization trends worth watching in 2025

Deepening institutional involvement

The deep involvement of traditional financial institutions is a core driver of the development of the RWA ecosystem. By 2024, giants such as BlackRock, JPMorgan Chase, and Goldman Sachs will be reshaping the financial market through tokenization projects. For example, BlackRock's BUIDL fund manages nearly $2 billion in assets on Ethereum, setting a benchmark for institutional tokenization. JPMorgan Chase's Kinexys platform has processed over $1.5 trillion in transactions, with an average daily trading volume exceeding $2 billion. Franklin Templeton's OnChain US Government Money Fund, which manages fund shares through blockchain, demonstrates the potential of tokenized funds. By 2025, as more traditional financial institutions enter the RWA sector, the market size and credibility are expected to increase significantly.

Improvement of the regulatory framework

An improved regulatory environment provides critical support for the maturation of the RWA ecosystem. The EU's Markets in Crypto-Assets (MiCA) Directive is expected to fully take effect in the second quarter of 2025, providing a unified compliance framework for RWA tokenization and mitigating legal risks. The UK's Electronic Trade Documents Act, passed in 2023, legalizes electronic trade documents and paves the way for their tokenization. Furthermore, regions like Singapore and Hong Kong are currently developing RWA-related regulations, with further clarity expected in 2025. These regulatory measures will bolster investor confidence and attract more institutional and retail investors to the RWA market.

Expansion of market size

According to an Ozean report, the RWA tokenization market (excluding stablecoins) is expected to reach $5 billion in 2025, an approximate 230% increase from $1.52 billion in 2024 (Coingeek). Longer-term, forecasts compiled by Tren Finance suggest that the market size could range from $4 trillion to $30 trillion by 2030, with a median of approximately $10 trillion. This represents a more than 54-fold increase from the current market size of $18.5 billion (including stablecoins).

Diversification across asset classes

RWA tokenization is expanding beyond traditional financial assets into emerging sectors, with coverage expected to expand to even more asset classes by 2025. Real estate tokenization, which lowers investment barriers by fragmenting ownership, accounted for 60% of the total market value in 2024 and is expected to continue dominating the market in 2025. Private credit tokenization uses blockchain to provide financing for small and medium-sized enterprises. Active loan value at Centrifuge and Goldfinch reached $446 million in 2024, with further growth expected in 2025. Carbon credit tokenization has become a highlight in the ReFi sector, with transaction volumes at Toucan Protocol and KlimaDAO exceeding 100 million tons of CO2 equivalent in 2024, and the market size is expected to double by 2025. Furthermore, the tokenization of art, collectibles, supply chain finance, and intellectual property is also growing, injecting new vitality into the RWA ecosystem.

Conclusion

The above outlines a blueprint for the development of real-world assets (RWAs) in 2025. Through an in-depth analysis of RWA's definition, development, 2024 market review, trends worth noting in 2025, and representative projects in key areas of the ecosystem, we can clearly see the diversity and potential of the RWA ecosystem.

In 2024, total assets in the RWA market (excluding stablecoins) reached approximately $1.52 billion, an 85% increase from the previous year. These assets encompass a wide range of asset classes, from real estate to bonds, from funds to art. This growth not only reflects the market's demand for liquidity and transparency, but also signals the growing attention paid to RWA by institutional investors. Looking ahead to 2025, the RWA ecosystem will continue to expand, driven by the deeper involvement of traditional financial institutions, the improvement of regulatory frameworks, and the diversification of asset classes, all contributing to its prosperity.

The rise of RWAs not only reshapes the value flow model of traditional assets but also provides unprecedented opportunities for investors. Leveraging blockchain technology, RWAs enable the unbundling of asset ownership, improve liquidity, and lower investment barriers. However, for investors, technology developers, and policymakers, the future presents both challenges and opportunities.

References

- https://www.binance.com/zh-CN/square/post/17324425199913

- https://foresightnews.pro/article/detail/30855

- https://www.chaincatcher.com/article/2096718

- https://web3caff.com/archives/58122

- https://www.techflowpost.com/article/detail_11880.html

- https://www.hellobtc.com/kp/du/07/4360.html

Special statement: All articles of DePINone Labs are for information and knowledge purposes only and do not constitute any investment advice.

End