TL;DR

Paradigm shift: On-chain US stocks turn "account vouchers in accounts" into programmable and composable on-chain assets that can not only be traded, but also mortgaged, loaned, used as LPs, and stacked strategies.

Efficiency and Accessibility: 24/7 continuous trading + stablecoin settlement, fragmentation and cross-border access for global long-tail users far exceed the time and regional restrictions of traditional online brokerages/ATS.

Core comparison:

- Traditional securities firms: strong regional supervision, weak after-hours liquidity, and assets locked within the securities firm system.

- On-chain solution: open infrastructure + DeFi composability, more continuous price discovery and more flexible capital turnover.

Three mainstream paths:

- xStocks/SPV: Redeemable, DeFi-native, strong liquidity and transparency; limited shareholder rights before redemption, and regulation is still evolving.

- Robinhood/CFD: Clear compliance and controllable products; closed ecosystem, non-transferable on-chain, and weak on-chain usability.

- Securitize/Direct Registry: Strongest ownership and compliance; but limited trading and composability, and low liquidity.

Regulatory landscape: Mature markets tend to extend regulation to "same business, same rules", while emerging markets tend to adopt sandbox approaches; secondary markets are generally more cautious towards retail investors.

User portrait:

- Users in emerging markets with limited access (without overseas accounts);

- Crypto/traditional "amphibious" users seeking capital efficiency;

- High net worth and income-driven users (activating "dormant" stocks to generate on-chain income).

Realistic trade-offs: The costs are roughly similar, but there are slippage/market-making depth risks on the chain; compliance and technical paths have not yet been unified, and early liquidity and experience are still bottlenecks.

Evolutionary path: In the short and medium term, a hybrid model of "Web2 experience, Web3 core" will be presented; in the long term, on-chain settlement and custody are expected to become the underlying infrastructure of the next-generation stock market, promoting the "coin-stock integration" into the mainstream.

01 The Improvement of On-chain US Stocks Compared to Online Brokerages / A Brief History of Brokerage Development

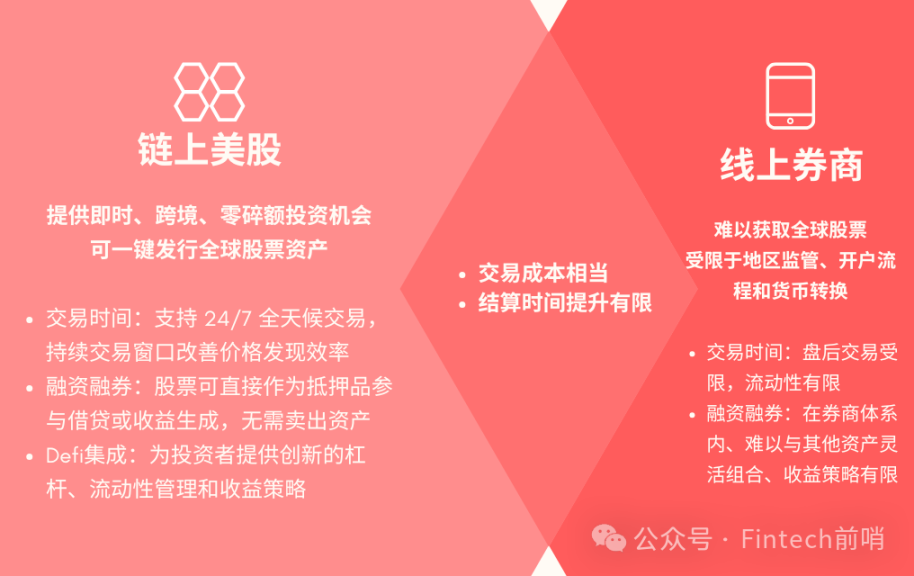

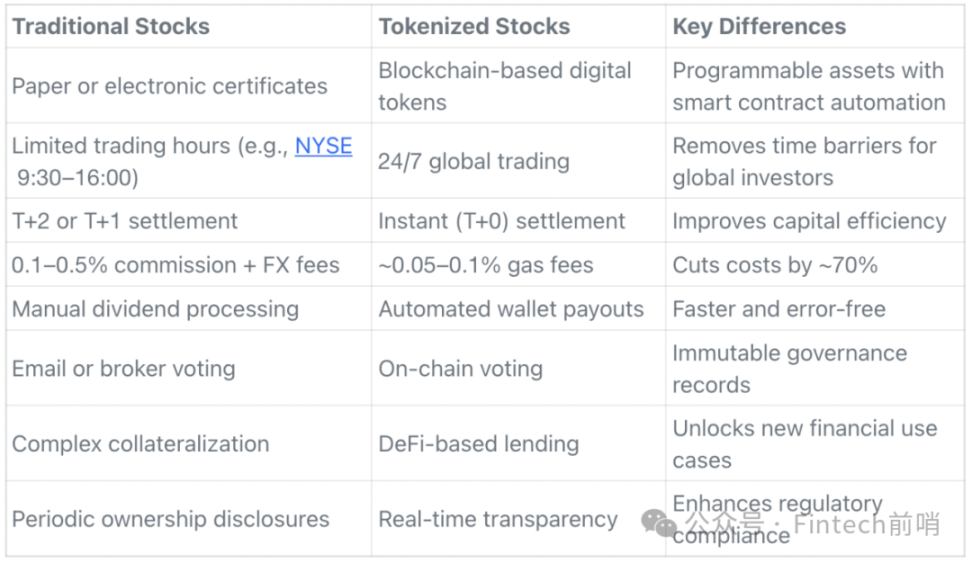

Compared to the closed architecture of traditional online brokerages, the core advantage of On-Chain US Stocks lies in its open, composable financial infrastructure. This architecture comprises two core components: a 24/7, borderless transaction settlement layer powered by blockchain, and a natively integrated DeFi protocol ecosystem. The synergy between these two not only fundamentally enhances asset accessibility (global access) and liquidity efficiency (24/7 trading), but also, through the composability of DeFi, unlocks a new paradigm for traditional equity assets in lending, yield generation, and strategy building.

Comparison of core competitive points

Retail Investor Perspective: Global Stock Access

- Traditional online brokerages are restricted by regional regulations, account opening procedures and currency conversion, making it difficult for investors to access global stocks.

- On-chain US stocks provide instant, cross-border, and fractional investment opportunities. Users can buy fractional stocks or tokenized stocks directly through their mobile phones.

Platform Perspective: One-Click Offering & User Acquisition

- On-chain platforms can issue global stock assets with one click, reach long-tail user groups, and use DeFi protocols to improve the liquidity and income generation potential of asset portfolios.

Comparison of the development of traditional brokerages and crypto exchage

Traditional online brokerages: Increase revenue and customer stickiness by expanding product lines (such as overseas stocks, ETFs, and options).

Crypto exchage: For example, FTX once tried to offer US stock trading, but the product was closed; tokenization projects such as Mirror partially failed.

Private equity on the blockchain: Improving the tradability of illiquid assets (such as private equity and employee options) in the market.

- Private company equity, pre-IPO stocks, etc. are traditionally difficult to trade and have extremely poor liquidity.

- Singapore's ADDX uses blockchain and smart contracts to tokenize private equity and unlisted company shares, lowering the investment threshold from millions of dollars to thousands. It also supports on-demand transfers through the secondary market, facilitating exits. It has tokenized multiple private equity funds (such as Partners Group and Hamilton Lane), enabling fast settlement and transparent transactions.

Comparison of on-chain US stocks and online brokerages

Trading time comparison

Traditional brokerage firms/ATS (e.g. Futu/Robinhood via Blue Ocean ATS)

1. After-hours trading is restricted, liquidity is limited, and bid-ask spreads may be wide. The market primarily covers large-cap stocks; small-cap stocks or OTC stocks may not be traded during the night session.

2. Price discovery is weak and easily influenced by a small number of participants, which may lead to differences in the next day's opening; after-hours trading volume is low. For example, NVDA's after-hours trading volume on Robinhood is approximately $80,000.

US stocks on the chain

1. Support 24/7 trading and achieve continuous liquidity through DEX (such as Raydium); after-hours trading volume is significantly higher than ATS. For example, NVDAx/USDC has an after-hours trading volume of approximately $8–12 million on Raydium.

2. The continuous trading window improves price discovery efficiency, allowing investors to respond to global market events at any time, achieving more continuous market pricing and a complete price discovery mechanism.

3. Backed Finance xStocks can be traded 24/5 through Kraken/Bybit. After transferring tokens to a self-custodial wallet, DEX can achieve 24/7 trading, breaking the traditional trading time limit.

Cost and settlement comparison

Transaction costs: The overall difference is not significant. On-chain transaction fees are low, but there are slippage and liquidity risks.

1. Futu costs: Standard commission US$0.0049/share, minimum US$0.99/trade, capped at 0.5%; platform fee US$0.005 per share; additional liquidation fees, SEC and FINRA TAF for sell orders; margin rate approximately 4.8% annualized; options minimum US$1.99 per contract.

2. Robinhood costs: Zero commission trades; SEC selling fee of approximately $5.10 per $1 million in trading volume, FINRA TAF of approximately $0.000166 per share; options contracts of $0.00279–$0.00279 per contract; Robinhood Gold monthly fees of $5–$50; margin interest rates of approximately 5.7–6.75%; account transfer fee of $75.

3. Xstocks Cost (Kraken): Trading is commission-free (USDG/USD); issuance/redemption fees are up to 0.50%; ETF annual management fee is 0.20%, with no management fee per share; on-chain liquidity and slippage may increase hidden costs.

Settlement time: Overall improvement is limited, and on-chain US stocks can be instantly converted into USDC or other stablecoins

1. Traditional brokerages settle on a T+1 basis; Robinhood Gold and other platforms offer instant settlement (funds can be reinvested immediately after selling, but withdrawals are still subject to settlement date restrictions).

2. On-chain US stocks can be immediately converted into USDC or other stablecoins for lending or reinvestment.

Margin Trading and DeFi Integration

Breaking through traditional financial barriers: Solving the pain points of traditional stocks being confined to the brokerage system, difficult to flexibly combine with other assets, and having limited profit strategies.

Stocks can be used directly as collateral for lending or yield generation without having to sell assets.

1. Tokens like xStocks can be used as collateral in protocols like KaminoFinance to borrow USDC or USDG stablecoins.

Providing investors with innovative leverage, liquidity management and income strategies.

1. Swap and 24/7 Trading: Tokenized stocks (such as xStocks) can be swapped on DEXs such as Raydium and Jupiter, which is a key mechanism to achieve 24/7 trading.

2. Deploy liquidity pools: You can form LPs with stablecoins or SOL on platforms such as Raydium to earn transaction fees and other income.

User experience comparison

Traditional process: Investors need to open overseas accounts, handle KYC/AML, pay foreign exchange fees, and are restricted by market trading hours.

On-chain US stocks: For example, Indonesian investors who want to gain exposure to Tesla stock can buy tokenized Tesla stock directly on their mobile phones and lend or provide liquidity in DeFi protocols. The operation is simple, 24/7, and can be invested in small amounts.

02 Regulatory Status in Various Regions

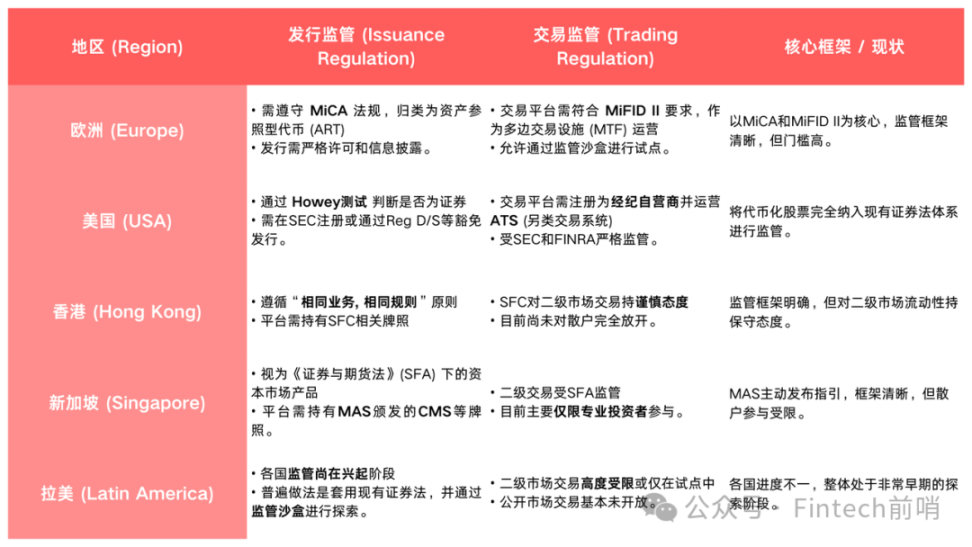

Global regulation has shown a clear divergence in its approach to tokenized issuance. Mature financial markets, such as the United States, the European Union, Hong Kong, and Singapore, generally adopt a "regulatory extension" model, directly incorporating tokenized securities into existing securities regulations and subjecting them to the same registration, exemption, and licensing requirements as traditional stocks. In contrast, emerging markets, such as Latin American countries like Brazil and Argentina, tend to adopt a "sandbox innovation" model, establishing controlled testing environments to explore and validate technical feasibility and accumulate practical experience for future formal regulations.

Regarding secondary market transactions, global regulators demonstrate a highly consistent and cautious approach, with investor type being a key risk management tool. While the US and EU allow trading on licensed trading venues (such as ATSs and MTFs), entry barriers are extremely high. Hong Kong and Singapore explicitly limit secondary market participants to professional investors to isolate potential risks. In most emerging markets, such as Latin America, public secondary market trading has yet to be liberalized, remaining strictly confined to sandboxes or the early exploratory stages of private placements.

Europe

Tokenized issuance

- MiCA (EU Crypto-Asset Market Regulation) clarifies the classification of crypto assets, including asset-referenced tokens (ARTs) and electronic money tokens. Equity tokenization is generally classified as ART and is subject to strict licensing, information disclosure, investor protection and behavioral regulatory requirements.

- BeToken, issued on the Polygon Chain, utilizes the ERC-3643 token standard, integrating KYC/AML compliance directly into transactions. This project is Spain's first officially recognized security token offering (STO), regulated by the CNMV (Spanish National Securities Market Commission) under the Securities Market and Investment Services Law (Law 6/2023). The trading platform, Token City, and the custodial service, ONYZE, are both approved by the CNMV, ensuring full compliance.

Tokenized US/European stock trading

- EU MTFs (Multilateral Trading Facilities) or trading platforms must comply with MiFID II requirements, including capital adequacy, risk management, transaction transparency, investor protection, and a cross-border regulatory passporting system. Some innovative projects can be piloted through the DLT sandbox mechanism.

Revolut

- Securities License: Regulated by MiFID II, holding an investment firm license, it only performs trading, market making, and custody services, and does not provide asset management or wealth management services.

- US stock trading: Executed through DriveWealth, a US licensed brokerage firm, in compliance with SEC/FINRA regulatory requirements.

USA

Project Crypto Updates

- The SEC (U.S. Securities and Exchange Commission) established the Crypto Task Force to promote regulatory sandboxes, industry collaboration, and innovation exemptions, gradually clarifying the regulatory framework for tokenized securities.

Tokenized issuance

- The Howey test is used to determine whether a security is present. S-1 registration or Regulation D/S exemptions may be chosen for issuance to qualified investors, and the underlying assets must be held by a regulated custodian and auditable.

Tokenized US Stock Trading

- Trading platforms must register as a national securities exchange or broker-dealer and operate under Reg ATS (Registered Alternative Trading System), subject to supervision by the SEC and FINRA; cross-border platforms avoid US compliance risks through geo-fencing or cooperating with licensed entities.

Robinhood

- Adhering to customer asset segregation, best execution, and compliance reporting, Robinhood Financial LLC holds a broker-dealer license, is a member of FINRA and SIPC, and offers insurance coverage. Other exchanges, such as tZERO and INX, hold ATS licenses and specialize in trading digital asset securities.

Hongkong

Tokenized issuance

- The Securities and Futures Commission (SFC) adopts the “same business, same risks, same rules” principle and regards tokenized stocks as a digital extension of traditional securities.

- Platforms involved in issuance, trading, or custody must hold relevant SFC licenses (such as Type 1, 4, 9, or VATP) and implement AML/KYC. For example, ADDX issues tokenized private equity to professional investors; HashKey and OSL hold VATP licenses to operate virtual asset trading platforms.

Tokenized US Stocks/Stock Trading

- The SFC is cautious about secondary trading of tokenized securities, emphasizing that additional regulatory protection is needed and that it has not yet been fully liberalized.

- Hong Kong launched Project Ensemble Sandbox in 2024 to promote pilot projects such as tokenized bonds, funds, and green finance, but the secondary market details for stock tokenization have not yet been clarified.

Futu (Hong Kong)

- License and regulatory framework: We hold multiple SFC licenses (Type 1, 4, 9, etc.) through our Hong Kong subsidiary and operate legally and in compliance with local regulations.

- US stock execution and asset protection: As an introducing broker, we route client US stock orders to licensed US clearing brokers for execution. Stock assets are held in custody by DTC and protected by SIPC.

Singapore

Tokenized issuance

- Tokenized shares are considered capital markets products under the Securities and Futures Act (SFA) and, if they represent equity interests in a company or traditional securities, are subject to the same prospectus, disclosure and trading authorization requirements as traditional shares.

- Compliance requirements: Issuing platforms must hold a MAS Capital Markets Services License (CMS) or a Recognized Market Operator (RMO) license; institutions providing investment advice must hold a Financial Advisory License (FAA); and comply with the AML/KYC requirements of the Payment Services Act (PSA).

- Platform and Sandbox Case Studies: ADDX, InvestaX, and SDAX have completed tokenized private equity, real estate, and fund issuances; BeToken, a similar example, has been authorized under the European Sandbox. The InvestaX E-VCC project, through Project Guardian, collaborated with UBS and State Street to test tokenized fund structures and verify technical feasibility.

Tokenized US/Singapore Stock Trading

- Secondary trading is subject to the regulatory requirements of the SFA, FAA and PSA, and the MAS’s Circular on Tokenised Securities (November 2023) provides guidance covering issuance, custody, trading and investor protection.

- Complex products are only open to professional or qualified investors, and participation by retail investors is restricted.

Futu (Singapore)

- Licenses and Regulatory Framework: Subsidiary Futu Singapore Pte. Ltd. holds a MAS Capital Markets Services (CMS) license and is a securities and derivatives trading and clearing member of SGX. It has also obtained a Major Payment Institution (MPI) license, achieving deep integration of local compliance.

- Execution and Asset Protection: Similar to Hong Kong, US stock orders are executed by US-licensed clearing brokers, stock assets are custodied by SIPC, and local licensed entities are responsible for bookkeeping and customer service to ensure the compliance and security of cross-border transactions.

Latin America

Tokenized issuance

- Brazil: CVM (Brazilian Securities and Exchange Commission) considers tokenized securities to be equivalent to traditional securities and subject to securities issuance, disclosure and trading regulations; Law 14,478/2022 provides a framework for VASP authorization and supervision, and a regulatory sandbox to test the on-chain listing of stocks and the issuance of innovative securities.

- Mexico: If stock tokens are deemed securities, they must comply with the registration, disclosure, and issuance requirements of the CNBV (Mexican National Bank and Securities Commission); the Fintech Law stipulates the regulation of virtual assets, but security tokens are subject to traditional securities regulations.

- Colombia: Equity tokens are not yet considered formal securities, and their issuance without permission will be deemed illegal fundraising; the Colombian Financial Supervisory Authority (SFC) is cautious about tokenized securities and complies with existing securities regulations and AML/CFT requirements.

- Argentina: CNV will release the first securities tokenization framework in 2025, allowing financial trusts and closed-end funds to tokenize physical assets; stock tokens are not yet included, but the regulatory sandbox is being promoted in phases and may be expanded to stock issuance in the future.

Tokenized US Stocks/Stock Trading

- Brazil: Secondary trading is still under exploration. BEE4 provides on-chain trading of small and medium-sized enterprise stocks, combining OTC and custody mechanisms.

- Mexico: Secondary trading is subject to CNBV securities market rules, and equity tokens are still in the private placement and restricted trading stages.

- Colombia: Public market trading is prohibited, and equity tokens can only be traded in a restricted sandbox or internal registry.

- Argentina: Secondary market trading is not yet permitted for stock tokenization, and the current sandbox is limited to financial trusts and closed-end funds.

Brazil BEE4

- Licenses and Regulatory Framework: Approved to exit the CVM regulatory sandbox, obtained licenses for an organized over-the-counter market and a central securities depository, and legally provided services for the issuance and trading of tokenized shares of small and medium-sized enterprises.

- Issuance and Trading: Supports on-chain registration, custody, and secondary market trading of stocks. The first blockchain-based IPO was Roda Conveniência. Transactions are completed through OTC collaboration with mainstream brokerages.

03 Analysis of existing solutions

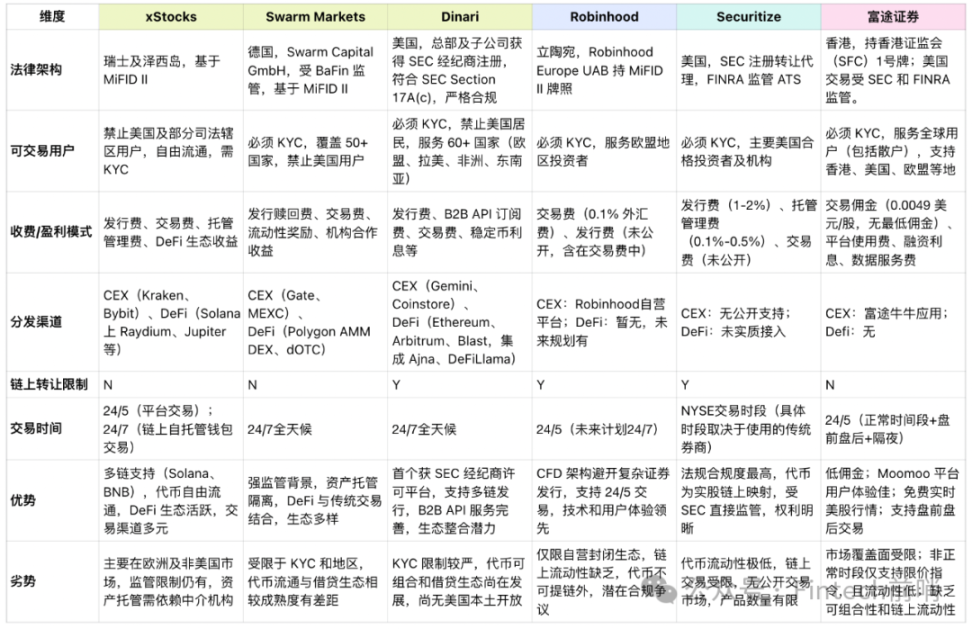

The current mainstream solutions for on-chain US stock trading have followed different compliance and technical paths and differentiated into three core architectural paradigms:

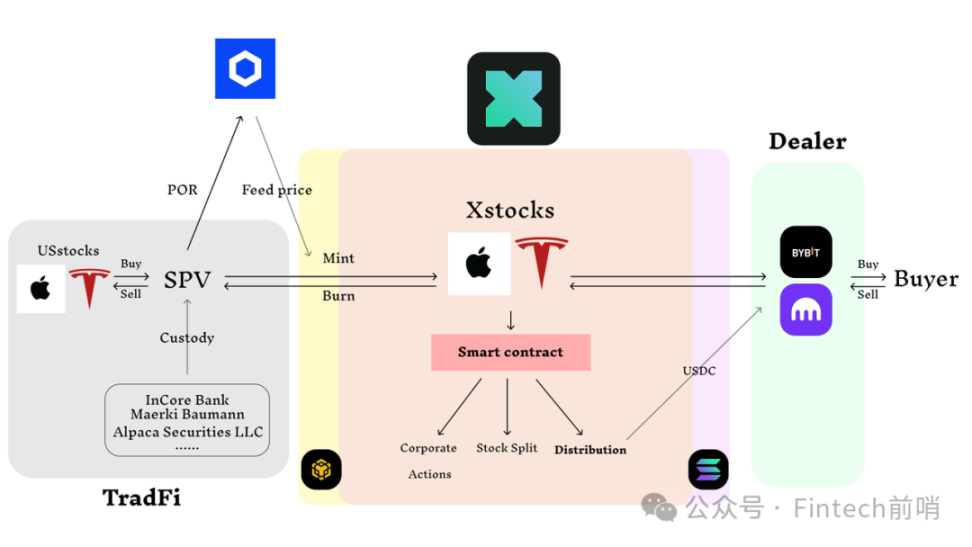

1. The asset-backed model, represented by Xstocks, achieves asset isolation and 1:1 on-chain mapping through an SPV structure. Its core advantage lies in DeFi's native composability and open circulation.

2. The derivatives model, represented by Robinhood, whose tokens are essentially financial contracts (CFDs) anchored to stock prices, operates within a closed ecosystem, sacrificing composability in exchange for complete control over products and trading environments.

3. The direct registration model, represented by Securitize, directly registers users as registered shareholders, providing the strongest legal ownership. However, its extremely high compliance threshold and closed trading system also almost completely deprive it of on-chain liquidity and composability.

Xstocks model: SPV structure, users are SPV shareholders; can redeem US stocks after KYC

Xstocks

Legal framework

Issuer and supervision

1. The issuer is Backed Assets (JE) Limited, which is registered in Jersey and regulated by the Jersey Financial Conduct Authority.

2. Its parent company, Backed Finance AG, is registered in Switzerland and claims that its tokenized architecture complies with European regulatory standards such as MiFID II.

Asset isolation and custody

1. Use a special purpose vehicle (SPV) structure to deposit actual shares into an independent SPV, which is then held by a licensed third-party custodian (such as Clearstream or InCore Bank).

2. Assets are not included in the balance sheet of the issuer (Backed Finance), achieving asset isolation.

3. Verify the 1:1 peg between assets and tokens on-chain through Chainlink’s Proof of Reserves system, increasing transparency.

Token Nature and Shareholder Rights

1. Token stage (before redemption):

• The token is a security token, which is an on-chain mapping of the shares held by the SPV.

• The holder has economic rights such as price changes and dividends, but does not directly have shareholder rights such as voting rights (voting rights belong to the SPV).

2. Redemption Phase (after redeeming actual shares): After completing the redemption, users can register their shares in their own name, thereby being included in the company's shareholder register and enjoying all shareholder rights, including voting rights.

Trading users

Geographic Restrictions: Products are expressly not for sale to or for the accounts of U.S. persons; not available in certain restricted jurisdictions.

Compliance requirements: Users must complete KYC/AML (Customer Identification/Anti-Money Laundering) verification on compliant exchanges (such as Kraken and Bybit) before purchasing.

Fee/profit model

Main source of profit

1. Issuance Fees: Fees may be charged when minting tokens to institutions or market participants.

2. Transaction Fees:

• Partner exchanges (such as Bybit) will charge transaction fees based on the user’s VIP level.

• Kraken has zero fees on some trading pairs (USD/USDG), but other pairs may include spreads.

3. Hosting and management fees: The management fees incurred by cooperating with third-party hosting institutions may be partially passed on to users or partners.

4. DeFi ecosystem benefits (indirect): Through the widespread use of tokens in DeFi protocols, the demand and issuance of tokens will increase, thereby indirectly benefiting.

Distribution Channels

Centralized Exchanges (CEX): Mainly distributed and traded through compliant centralized exchanges such as Kraken and Bybit.

Decentralized Exchange (DEX): Supports trading on DEXs on the Solana chain (such as Raydium and Jupiter).

Self-custody: Users can withdraw tokens to a compatible personal wallet (such as the Solana wallet) for complete self-control.

On-chain transfer restrictions: No platform lock-in

xStocks tokens are issued based on Solana’s SPL or BNB Chain’s BEP-20 standard.

This standardized design enables free transfers between compatible wallets, exchanges, and DeFi protocols without being locked into a single platform.

Trading Hours: 24/7 trading is supported, unconstrained by traditional stock market trading hours.

Advantages

Strong DeFi composability: As a standard SPL/BE-P20 token, it can be seamlessly integrated into the DeFi ecosystem of Solana and BNB Chain for lending, providing liquidity or serving as collateral, with high capital efficiency.

Highly transparent and secure assets

1. Use SPV structure to isolate assets and have them managed by a regulated third-party institution.

2. Utilize Chainlink’s on-chain reserve proof for verification, ensuring asset transparency.

Wide and flexible circulation channels: It supports both CEX and DEX transactions and allows users to self-custody, providing high flexibility and a wider range of liquidity options.

Automated corporate action processing: Corporate actions such as dividends (in the form of stablecoins such as USDC) and stock splits can be automatically processed through smart contracts and oracles, ensuring the rights of on-chain holders.

Disadvantages

Regulatory uncertainty: The global regulatory landscape for tokenized shares is still evolving and may face new restrictions or compliance requirements in the future.

Limited shareholder rights (before redemption): Before redemption for real shares, token holders only enjoy economic rights and cannot directly exercise full shareholder rights such as voting rights.

Third-party counterparty risk: The terms of service clearly state that the platform is not responsible for the failure, bankruptcy or regulatory enforcement actions of third-party custodians, issuers or market makers.

Market size and liquidity risk: The product has been launched for a short time, and its current overall market capitalization and daily trading volume are relatively small. There is a risk of price deviation from the underlying assets and insufficient liquidity.

Similar mode players: Swarm

Adopting an SPV structure, operated by an entity licensed by Germany's BaFin, providing a hybrid trading channel

Legal framework

Comparison with xStocks

1. Similarities: Similar to xStocks, Swarm also uses an SPV structure to isolate underlying assets, ensuring that they are not included in the company's balance sheet; the tokens it issues also do not provide full shareholder rights such as voting rights.

2. Key Differences: The core difference lies in their regulatory bodies. xStocks is regulated by the Jersey Financial Authority, while Swarm is directly licensed and regulated by the more stringent German Federal Financial Supervisory Authority (BaFin), making it the world's first DeFi platform to receive a BaFin license.

Trading users

Geographic restrictions and compliance requirements: Prohibits US users, serves users in more than 50 countries including Europe and Asia; requires KYC/AML verification and connection to a self-hosted wallet.

Fee/profit model

Main source of profit

1. Issuance and Redemption Fees: Fees are charged during the issuance and redemption of tokens.

2. Transaction Fees: A fee (e.g. 0.1%) is charged for transactions in the liquidity pool, part of which is distributed to holders of the platform token SMT.

3. Liquidity Mining Rewards: By issuing the platform’s native token SMT, users are incentivized to provide liquidity for the tokenized stock pool.

Distribution Channels

Proprietary decentralized exchange (DEX): mainly distributes and trades through its own AMM DEX on Polygon.

Decentralized over-the-counter (dOTC): Provides institutional users with large-scale, customized trading channels to reduce slippage.

On-chain transfer restrictions: Free transfer with KYC verification

The tokens are based on the ERC-20 standard and can be freely transferred between user wallets that have passed KYC verification.

Advantages

Strong German BaFin supervision: As the first DeFi platform licensed by BaFin, its compliance and security endorsement stand out among similar products.

Hybrid trading channel: Provides both retail-oriented DEX and institutional-oriented dOTC services to meet the trading needs of different users.

Good DeFi composability: Based on Polygon and Arbitrum, tokens can be easily used in DeFi scenarios such as liquidity mining and staking.

Disadvantages

Platform ecosystem risk: The platform’s incentive mechanism relies on its native token, SMT, which has a low market capitalization and large price fluctuations, which may affect the stability and liquidity of the entire ecosystem.

TVL (total value locked) instability: The platform’s TVL has experienced significant fluctuations, indicating that the stability of its user and fund retention is facing challenges.

Lack of traditional shareholder protections: Like similar products, investors do not have access to legal protections such as voting rights and are subject to the risk of bankruptcy of the custodian or issuer.

Similar player: Dinari

SPV structure; more direct asset holding through SEC registered entities, focusing on B2B distribution model

Legal framework

Comparison with xStocks

1. Similarities: Like xStocks, Dinari also uses an SPV structure to isolate assets, and its tokens (dShares) also do not provide full shareholder rights such as voting rights.

2. Key Differences: The core differences lie in regulatory status and asset holding methods. xStocks relies on Jersey regulation and a third-party custodian; Dinari's US subsidiary is registered as a broker-dealer and transfer agent by the SEC. This allows it to legally handle stock registration and custody directly, creating a more direct and clearer compliance path for its self-custody and self-registration model than xStocks.

Trading users

Geographic restrictions and compliance requirements: US users are prohibited, serving more than 60 non-US countries; all users must pass KYC verification.

Fee/profit model

Main source of profit

1. B2B API subscription fees: Charge subscription fees to fintech companies and banks that use their API services.

2. Transaction fees: They may receive a share of fees from transactions on their partner platforms.

3. Issuance and Management Fees: Fees are charged for the issuance and ongoing management of tokenized assets.

4. Stablecoin income: Earn income through the interest-bearing stablecoins (USD+) it issues.

Distribution Channels

B2B API and white label services: core channels that do not directly target retail users, but instead embed their tokenized stock functionality into other fintech platforms or digital banks through APIs.

Partner Platforms: Distribute to end users through regulated exchanges like Gemini.

Multi-chain network deployment: Its tokens are issued on multiple mainstream blockchains such as Ethereum, Arbitrum and Blast.

Advantages

Top-tier US Compliance Qualifications: As the first tokenization platform to obtain SEC broker-dealer and transfer agent registration, its US compliance framework is ahead of all competitors.

Innovative B2B business model: Through API and white label services, its products can be quickly integrated into existing financial platforms, with high expansion efficiency.

Disadvantages

Internal risks brought by self-custody: Compared with models that rely on third-party custody (such as xStocks), Dinari's self-custody model reduces external intermediaries but also increases its own operational and security risks.

Dependence on partners for distribution: The B2B model means that its user growth and transaction volume are highly dependent on the performance and integration capabilities of its partners.

Lack of traditional shareholder rights: Like similar products, users only obtain economic exposure and cannot exercise shareholder rights such as voting rights.

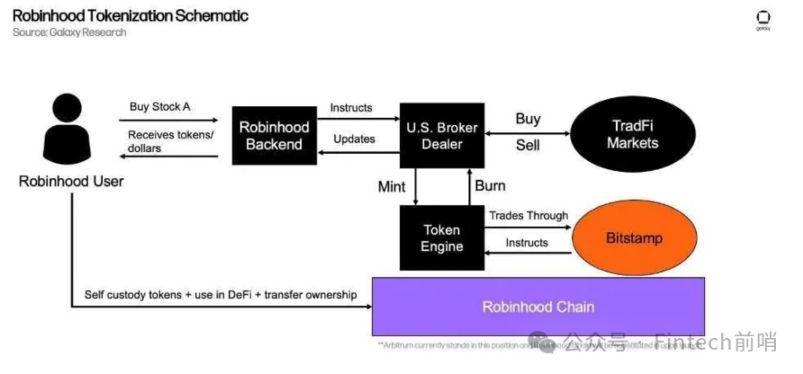

Robinhood: Similar to CFD exposure, Robinhood's stock holdings are just a hedge; they are not redeemable.

Legal framework

Issuer and supervision

1. The issuer is Robinhood Europe, UAB, which is registered in Lithuania, holds an EU MiFID II investment firm license, and is regulated by the Bank of Lithuania.

Asset segregation and custody

1. The underlying real stocks are purchased and held in custody by a cooperating US brokerage firm, and asset isolation is achieved through an SPV structure, and they are not included in Robinhood's balance sheet.

2. The specific information of the third-party custodian institution has not been disclosed publicly.

Token Nature and Shareholder Rights

1. The token is essentially a digital certificate for a "financial contract for difference (CFD)", a blockchain-based derivative that is 1:1 anchored to the stock price.

2. Users only gain economic exposure to price fluctuations, not actual stock ownership, and therefore do not have any shareholder rights such as voting rights.

Trading users

Geographic Restrictions: Available only to users in the European Union (EU) and the European Economic Area (EEA). Not available to users in the United States.

Compliance requirements: Users must complete a rigorous KYC/AML process through the Robinhood EU app, including identity verification, risk assessment, knowledge questionnaire, etc., to meet MiFID II regulatory requirements.

Fee/profit model

Main source of profit

1. Foreign Exchange Transaction Fee (FX Fee): Although the transaction itself is zero commission and zero spread, the platform will charge a 0.1% foreign exchange transaction fee, which is reflected in the exchange process between US dollars and euros.

2. Issuance Fees: Users or institutions may be charged an initial issuance fee, but the specific rate is not disclosed or may be included in the foreign exchange fees.

3. DeFi Ecosystem Benefits (Future): We plan to obtain indirect benefits through DeFi protocol integration on our future proprietary chain "Robinhood Chain".

Distribution Channels

Proprietary Platform: Tokens can only be distributed and traded through Robinhood’s own EU crypto app, which is a completely closed ecosystem.

On-chain deployment: Tokens are deployed on the Arbitrum network to improve efficiency, but users cannot withdraw tokens to personal wallets or other exchanges outside the platform.

On-chain transfer restrictions: restricted by whitelist

The token is a "Permissioned Token" whose smart contract has a whitelist mechanism embedded in it.

Transfers are only allowed between addresses that have passed Robinhood KYC verification and cannot circulate freely on the open blockchain network.

Trading hours: Support 24/5 trading, and plan to expand to 24/7

Advantages

Compliance and brand endorsement: Operating under the EU MiFID II framework, it has a clear compliance path and leverages Robinhood's strong brand reputation.

Integration of technology and financial services: Integrating issuance, trading, and clearing, reducing dependence on external intermediaries and achieving complete control over products and user experience.

Flexible asset coverage: The CFD-based derivatives structure enables it to quickly cover listed stocks and unlisted popular companies (such as OpenAI), with flexible market response.

Avoiding MEV: By planning to build its own L2 and controlling the sorter, it is theoretically possible to fundamentally eliminate MEV problems such as front-running and ensure transaction fairness.

Disadvantages

High centralization and counterparty risk: As a closed system, the custody, trading, and clearing of user assets rely entirely on the Robinhood platform, which poses significant single points of failure and counterparty risk.

Lack of transparency and on-chain utility: Transaction data is not public, and tokens cannot be transferred out of the platform, resulting in it currently not having any DeFi composability (such as lending, providing liquidity, etc.).

Legal and reputational risks: Unauthorized tokenized offerings by private companies, such as OpenAI, have sparked public controversy, exposing inadequate information disclosure and potential legal risks.

Limited liquidity: Liquidity is entirely provided internally by Robinhood and cannot be interconnected with external CEX or DEX markets, limiting price discovery and users' exit options.

Securitize: Extremely compliant, SEC-registered transfer agent model, users are direct shareholders of record; non-redeemable

Legal framework

Issuer and supervision

1. Securitize is a transfer agent registered with the U.S. Securities and Exchange Commission (SEC).

2. Its subsidiary, Securitize Markets, is an alternative trading system (ATS) regulated by the U.S. Financial Industry Regulatory Authority (FINRA) and is qualified to trade security tokens in the secondary market.

Asset docking and custody

1. Under the Direct Registration System (DRS) model, investors must first register their shares in their own name through a traditional brokerage firm.

2. Securitize acts as a transfer agent and only issues corresponding tokens to investors on the chain after confirming their identities on the official shareholder register.

Token Nature and Shareholder Rights

1. Tokens are digital securities regulated by U.S. securities laws and are an on-chain mapping of real stock ownership.

2. The holder is a legally registered shareholder and enjoys full shareholder rights (such as dividend distribution, governance rights, etc.).

Trading users

User restrictions: Mainly for qualified investors and institutional users in the United States who have passed complete KYC/AML and investor suitability certification.

Fee/profit model

Main source of profit

1. Issuance Fee: An initial issuance fee is charged to the asset issuer, usually based on a certain percentage of the asset size (e.g. 1-2% for EXOD issuance).

2. Custody and management fees: An annualized asset management fee (approximately 0.1%-0.5%) is charged.

3. Transaction Fees: Securitize Markets, its secondary market platform, charges a fee for transactions that occur.

Distribution Channels

Traditional assets on-chain: The main channel is for investors to convert their existing traditional stocks on the Securitize platform through the DRS process to obtain on-chain tokens.

On-platform secondary market: Securitize Markets, its proprietary, regulated alternative trading system (ATS), was the only compliant venue for secondary market trading of tokenized shares. However, following EXOD's listing on the New York Stock Exchange (NYSE American), trading shifted primarily to traditional public markets, and trading on Securitize Markets ceased.

On-chain transfer restrictions: restricted transfers based on whitelists

The token embeds compliance rules into smart contracts through its proprietary Digital Securities (DS) protocol.

Transfers are only allowed between whitelisted addresses that have passed KYC/AML review and cannot be freely circulated in the open market.

Advantages

Top-tier compliance framework: Possessing both an SEC-registered transfer agent and a FINRA-regulated ATS license, we provide the highest level of compliance assurance currently available in the market.

True Equity Ownership: Tokens directly represent legally registered equity, providing investors with full shareholder rights rather than just price exposure.

Automated compliance enforcement: Compliance rules such as transfer restrictions are codified through smart contracts, reducing the risks of manual operations.

Disadvantages

Market liquidity is extremely low: active products and trading volume on its secondary trading platform (ATS) are extremely limited, and the main trading of the only equity token product EXOD has been transferred to the New York Stock Exchange.

Limited liquidity and composability: The strict whitelist mechanism and closed trading environment prevent tokens from circulating freely and making it impossible to integrate or combine with external DeFi protocols.

Complex asset on-chain process: Investors need to operate through the traditional DRS system, which is a cumbersome process and has a high threshold for ordinary users.

Single product range: Currently, there is only one example of tokenized publicly listed company stocks, EXOD, and its product line is very limited.

04 Future trajectory: From channel replacement to native financial infrastructure

The true value and future trajectory of on-chain US equities lies not in the linear optimization of existing brokerage businesses, but in the profound paradigm shift it triggers. This shift is underpinned by three core pillars: first, a radical reshaping of the underlying nature of equity assets, transforming them from closed accounting vouchers to open, composable assets; second, the resulting multi-layered, structured user needs, encompassing everything from asset access to capital efficiency; and finally, its role as the next generation of financial infrastructure, the inevitable trend of driving the mainstream adoption of "equity-cryptocurrency integration."

Core value proposition: Reshaping the attributes of equity assets

The core value proposition of on-chain US stocks is not to simply replace channels or optimize efficiency for online brokerages, but to fundamentally reshape the underlying attributes of equity assets, transforming them from closed, single-purpose accounting vouchers to open, programmable, and composable on-chain native financial assets.

From regional access to global programmable access:

- The models of traditional online brokerages (such as Futu and Robinhood) are inherently regional and subject to strict regional regulations, complex KYC/AML processes, and high-friction currency exchange and cross-border remittances.

- On-chain US stocks change the entry threshold from "having a compliant overseas bank account" to "having a crypto wallet", providing global users with a nearly frictionless equity investment path using stablecoins as a medium.

From fragmented liquidity to 24/7 continuous markets:

- Traditional brokerage firms' after-hours trading (ATS) has inherent defects such as limited liquidity, large bid-ask spreads, and few covered targets, resulting in low price discovery efficiency.

- By integrating with decentralized exchanges (DEXs) like Raydium, on-chain US stocks create a 24/7 liquidity pool powered by automated market makers (AMMs). This not only enables true 24/7 trading but also significantly improves price discovery through continuous trading windows, allowing investors to instantly respond to global market dynamics.

From isolated utility to native composability:

- Traditional stocks are "locked" in the closed system of securities firms, and their financial utility is basically limited to trading and limited margin trading.

- Tokenized on-chain stocks (such as xStocks) are standardized digital assets (SPL/BEP-20 tokens) with the native properties of DeFi "Lego bricks". Their value is no longer limited to the stock price itself, but extends to the vast scenarios built by the entire DeFi protocol ecosystem.

1. Collateralized lending: You can directly use your stablecoins as collateral in lending agreements to increase capital utilization without having to sell your stocks.

2. Income generation: You can form a liquidity pair (LP) with stablecoins or other assets (such as SOL) to earn a share of transaction fees in DEX.

Demand user portrait: multi-dimensional and clear

The market demand for on-chain US stocks is not a single dimension, but rather presents a clear user stratification structure, accurately solving the core pain points of different groups.

Users with restricted access:

- User profile: Mainly distributed in countries with foreign exchange controls or imperfect financial services such as China, Indonesia, Vietnam, and Nigeria.

- Core pain points: Unable to open overseas bank or brokerage accounts, traditional deposit and withdrawal channels are blocked, and being completely excluded from the global high-quality equity market.

- Solution value: On-chain US stocks provide the only feasible "stablecoin-US stock" investment channel, completely bypassing the entry barriers of traditional finance.

Capital efficiency drives users:

- User profile: Holds both crypto assets and traditional brokerage accounts, but is trapped by the separation of the two major financial systems.

- Core pain point: Low leverage ratio. Traditional securities firms offer limited leverage ratios (such as 2.5 times), which cannot meet their pursuit of higher capital efficiency.

- Solution value: Allows users to directly use existing on-chain funds to invest in US stocks, and achieve leverage ratios far higher than traditional brokerages through DeFi lending protocols (such as achieving nearly 9x leverage through 90% LTV).

High net worth or income driven users:

- User profile: Investors who hold a large amount of U.S. stock assets for a long time.

- Core pain point: The existing stocks in traditional brokerage accounts are "sleeping assets" and it is difficult to generate additional compound returns except for dividends and stock price increases.

- Solution value: By tokenizing stocks, the DeFi utility of this part of existing assets is activated, allowing them to participate in various strategies such as on-chain market making, lending, and derivative construction, and earn additional on-chain income without giving up ownership.

Long-term trend: promoting the integration of cryptocurrencies and stocks

Judging from the long-term trend, the ultimate goal of on-chain US stocks is not to completely replace the front-end applications of brokerage firms, but it is more likely to become its underlying core infrastructure, pushing "stock-to-currency integration" into the mainstream.

Transitional Paradigm: Web2 Experience, Web3 Core

- Currently and for the next few years, the barrier to entry for ordinary users to directly interact with on-chain protocols is still too high. Therefore, the most realistic evolution path is a hybrid model.

- Under this model, users still conduct transactions through the familiar and user-friendly brokerage or CEX APP front-end, but the mid- and back-end processes such as asset clearing, settlement, custody and circulation are completed on the efficient and transparent blockchain.

- This not only retains the low threshold and user stickiness of Web2 products, but also obtains the technical architecture advantages of Web3 at the bottom layer. It is the best path to balance innovation and large-scale application.

Evolution of the long-term competitive landscape:

- As technology matures and regulations become clearer, the business boundaries between traditional stock exchanges and crypto exchage will become increasingly blurred, and they may eventually compete directly on the same blockchain-based infrastructure layer.

- The strategies of existing players (such as Robinhood) also confirm this trend: the CFD model they are currently launching can be seen as a first-phase deployment of "lightweight, fast and compliant"; and their business model and technological preferences naturally determine that they will inevitably move towards the second phase of full-process chain-linking to completely get rid of dependence on traditional financial intermediaries and reduce costs.

05 Conclusion

The development of on-chain US equities reveals a fundamental revolution in asset ownership, liquidity, and access to financial services. Rather than simply providing an alternative trading channel in existing markets, it positions itself as a new, open, and native financial infrastructure by combining the world's highest-quality equity assets with the composability of DeFi.

Its core advantages are:

- It fundamentally reshapes the underlying attributes of equity assets: It liberates traditional stocks from the closed system of brokerages and transforms them into open, programmable, and composable on-chain native assets, thereby unlocking unprecedented financial utility.

- It accurately solves the pain points of real users at multiple levels: It not only provides users in emerging markets with the only access channel to global assets, but also meets the urgent needs of professional investors for higher capital efficiency (leverage, income generation).

However, the challenges and uncertainties it faces are equally significant:

- Complex global regulatory environment: Countries generally adhere to the prudent principle of "same business, same rules", and in particular, they still maintain a highly restrictive attitude towards secondary market transactions involving retail investors, and compliance paths are still being explored.

- The technology and compliance paths have not yet been unified: The market presents a situation where multiple solutions coexist, and there is a clear path differentiation and experience trade-off between DeFi composability (such as the xStocks model) and extreme compliance (such as the Securitize model).

- Early market liquidity and user experience bottlenecks: The current on-chain transaction volume and liquidity depth are still far behind those of traditional markets, and the threshold for ordinary users to directly interact with on-chain protocols is too high.

For market participants, on-chain US stocks paint a picture that is full of opportunities but extremely challenging:

- Value Proposition: Its true disruptiveness lies not in the product itself, but in its potential as the next generation of financial infrastructure. Its unshakable core values are a 24/7 continuous market, native DeFi composability, and borderless asset accessibility.

- Development Path: While the long-term vision of "stock-to-cryptocurrency integration" is exciting, the sector as a whole is still in the early stages of exploration, with challenges in regulation, technology, and market acceptance. A hybrid model of "Web2 experience, Web3 core" may be the most realistic transition path towards mainstream adoption.