01 The Evolution of RWA Paradigms

The paradigm evolution of RWA is essentially the history of the expansion of the blockchain capability stack.

2009-2015: Early RWA attempts at colored coins

In 2009, the Bitcoin Genesis Block was created, successfully establishing the first decentralized value ledger in human history. However, Satoshi Nakamoto's vision of building "a P2P electronic currency" led him and subsequent Bitcoin developers, such as the Bitcoin Core team, to adhere to the development philosophy of "verification over computation" and use a non-Turing-complete scripting language, making the Bitcoin mainnet difficult to use as the infrastructure for hosting RWA assets.

Furthermore, in the early days of the crypto industry, from 2009 to 2015, the concept of RWA itself was still immature. During this period, the crypto industry was dominated by cypherpunks and believers in Austrian economics. They were keen to fork the fully open-source Bitcoin mainnet code and innovate in consensus, mining algorithms, and signature mechanisms to create digital currencies with faster confirmation, fairer distribution, and greater privacy protection, thereby joining the historically rare free market competition for private currencies.

However, amid the collective frenzy of "Long Bitcoin, Short The Real World," some industry pioneers, such as Amir Taaki, co-founder of Colored Coins, and JR Willett, founder of Mastercoin (later renamed Omni Layer), recognized the potential of RWAs and began exploring technical routes to allow users to create and trade coins representing physical assets such as stocks, bonds, and real estate on the Bitcoin mainnet. Tether launched USDT based on the Omni Layer, becoming one of the earliest centralized US dollar stablecoins. However, due to insufficient programmability and lack of liquidity support, Colored Coins and the Omni Layer gradually faded from the mainstream of crypto history after the mainstream technological paradigm shift.

2015-2020: STO's attempts at compliant asset issuance

In 2015, Vitalik, the editor of Bitcoin Magazine who advocated for Turing-complete technology, broke up with the Bitcoin community and created Ethereum. He introduced the EVM virtual machine and smart contracts, adding a new execution layer on top of the blockchain consensus layer, providing a programmable container for asset tokenization. This in turn gave rise to the ICO super wave with the free issuance of assets as its core feature, which ultimately triggered backlash and constraints from the financial regulatory authorities of major sovereign countries in the world.

Against this backdrop, STOs (Security Token Offerings) became the mainstream paradigm for RWAs, ostensibly under the guise of compliant ICOs. However, due to the incomplete on-chain liquidity infrastructure, the immaturity of oracles serving as the intermediary layer between on-chain and off-chain, and the lack of decentralized financial application scenarios, RWAs remained a formalized concept, with exit channels primarily located in traditional financial markets such as the US and Hong Kong stock markets.

The subsequent failure of STO revealed the fundamental flaw in the early RWA paradigm: attempting to copy the business model of traditional financial assets (stocks, bonds) onto the chain, but ignoring that the core advantage of blockchain is to create new types of liquidity rather than replicate the old financial system.

2020-2022: DeFi Summer Gives Birth to Chain Natives

During the DeFi Summer of 2020, fueled by the wealth effect of yield farming, traditional cryptocurrency traders and tech finance professionals transformed into DeFi Degens, becoming the first generation of true on-chain natives. DeFi protocols evolved in tandem with developers and users, and new concepts such as DEXs, decentralized pool lending protocols, CDP stablecoin protocols, and decentralized derivatives exchanges emerged like mushrooms after rain. Uniswap's AMM DEX paradigm completely replaced on-chain CLOBs (central limit order books) DEXs as the foundation of on-chain liquidity infrastructure, and ChainLink's oracle mainnet launch became a fundamental component of price feeds and risk management for DeFi protocols. At this point, Reliable Transaction Access (RWA) transitioned from formalized concept hype to practical exploration, and the classic architecture of off-chain assets, middle-layer oracles, and on-chain liabilities began to take shape.

During the period of active innovation from 2020 to 2022, while the application and middle layers experienced a Cambrian explosion, the consensus and execution layers also underwent rapid evolution. Innovations at the consensus layer during this period included: Solana's PoH consensus algorithm, the HotStuff Byzantine consensus algorithm adopted by Sui and Aptos, and Avalanche's Avalanche consensus algorithm. Innovations at the execution layer included: an EVM-compatible framework for L1 blockchains and SVM support for state parallel processing. These evolutions in the consensus and execution layers, bringing new features like rapid finality and fast state execution, laid a solid technical foundation for RWA's vigorous growth in the next cycle.

2023-2025: The hegemony of the US dollar stablecoin is established

2023 to 2025 is a period of explosive growth for broad RWA (including stablecoins). During this period, the tokenization of U.S. debt (mainly expressed in the form of U.S. dollar stablecoins) will replace STO and become the new paradigm of RWA.

In the early days, the correlation between stablecoins and RWAs was very weak. Cryptocurrencies at the time never envisioned that stablecoins would one day become the mainstream expression of RWAs. Centralized stablecoins primarily relied on commercial paper as their asset base, while decentralized stablecoins primarily relied on crypto-native assets. In 2022, following the devastating social impact of the consecutive collapses of the algorithmic stablecoin Luna and the crypto exchage FTX, the Biden administration in the United States demanded that the SEC strengthen its oversight of the cryptocurrency sector. Under regulatory pressure, stablecoin operators and protocols gradually evolved their asset base to a portfolio primarily comprised of short-term U.S. Treasuries, offering both high liquidity and minimal risk. Starting in the first half of 2023, crypto industry practitioners began to view stablecoins as a tokenized subclass of U.S. Treasury bonds within the broader concept of RWAs.

Take USDT as an example. It was initially claimed to be 100% backed by US dollar reserves, but its actual reserves include a large amount of commercial paper (short-term unsecured debt). The first reserve disclosure on March 31, 2021 showed that about 65.39% of the reserves were commercial paper, cash accounted for only 3.87%, and the rest included trust deposits (24.20%), repurchase agreements (3.6%), and Treasury bonds (2.94%) [1]. This disclosure triggered market controversy over its transparency and risk management. As regulatory pressure increased, Tether began to reduce its commercial paper holdings. The May 2022 report showed that the proportion of commercial paper fell from US$24.2 billion in the first quarter of 2021 to US$20 billion. In 2023, after the Silicon Valley Bank crisis in the US stock market caused USDC to decouple, it further fell to zero, and instead increased its holdings of cash, short-term deposits, and US Treasury bonds. As of September 2, 2025, the scale of Tether's short-term US Treasury bond reserves on the asset side was approximately US$105.3 billion [2].

On the technical level, the modular design concept aimed at solving the "Blockchain Trilemma paradox" of the blockchain has swept the entire industry, and the on-chain settlement-off-chain execution architecture has become popular. Rollup L2s represented by Arbitrum and Base have increased the block space supply quickly, efficiently and economically (Celestia, Bitcoin L2), providing technical support for the scale expansion of RWA, especially stablecoins; the technological progress of Baas/Raas such as Cosmos SDK and OP Stack (for example, Vote Extensions in Cosmos SDK ABCI++ 2.0 allows blockchains to submit and verify external data during the consensus process) and cost compression have paved the way for the emergence of RWA/stablecoin Appchains such as Pharos; the cross-chain intent standard of ERC-7683 jointly formulated by Uniswap and Across, the intent paradigm represented by Cowswap, the chain abstraction DEX represented by Infinex and Particle, and the CLOB+AMM liquidity solution represented by GTE and Kuru have further improved RWA. liquidity access and capital efficiency.

By 2025, the RWA market will be dominated by stablecoins. According to RWA.xyz, stablecoins will account for 90.7% of all RWA assets, making them the dominant force in RWA.

As the first crypto administration, the Trump administration prioritizes clarifying stablecoin regulation on par with establishing a national Bitcoin reserve. It sees stablecoins as a novel solution to consolidating the dollar's hegemony, marginally increasing demand for US Treasury bonds, and even competing for influence in the global financial order. The US GENIUS Act (Establishing National Innovation for Stablecoins Act) establishes a gold standard for stablecoin reserves: a combination of cash and highly liquid Treasury bonds. At the 25th Bitcoin Conference, US Vice President Cyril Vance stated, "Stablecoins are a power multiplier for the US economy." US Treasury Secretary Benson has frequently stated in major public appearances his optimistic prediction that the stablecoin market will reach $2 trillion or more within a few years.

The evolution of RWA from STO as the dominant paradigm to stablecoin as the dominant paradigm shows that the ultimate form of RWA is not the simple on-chain asset transfer, but the gradual replacement of the old industrial-era financial infrastructure consisting of SWIFT, foreign exchange markets, bond markets and stock exchanges by new technological financial infrastructure driven by AI and Crypto in the new era of technological acceleration. This is exactly the vision and goal of Project Crypto recently announced by SEC Chairman Atkins to ensure that the United States maintains its financial leadership in the future.

This is bound to catalyze a new round of exponential growth in block space demand, which will in turn force a new round of paradigm shift in block space supply: high-function L1/L2 such as Monad, MegaETH, and Pharos achieve millisecond-level finality and 100,000-level TPS through new blockchain architecture designs such as decoupling state execution and state finality, supporting state parallel processing, and optimizing database throughput; Solana launched a new consensus algorithm, Alpenglow, to further optimize block voting and verification processes, and is committed to helping Solana realize the vision of the next generation of Nasdaq. Ethereum has adopted a "simplified L1" route to return to Bitcoin's development philosophy, accelerating the ZKization, statelessness, and L1/L2 state finality of the Ethereum mainnet, and is committed to becoming the basic settlement layer of modern finance.

02 The current reality of RWA

The current structure and future trends of RWA off-chain assets

Traditional industry insiders have many wildly ambitious ideas about RWAs, such as tokenizing non-standard, real-world assets like industrial parks and hydropower stations, which lack fair market prices and mature risk management mechanisms, and exiting them through the crypto market. However, the current RWA off-chain asset market is dominated by stablecoins, private credit, tokenized US Treasury bonds, tokenized commodities, institutional alternative investment funds, and tokenized US stocks, with other non-standard, real-world assets holding virtually zero market share. This market structure is the result of a multi-faceted equilibrium reached through two market cycles between market forces and technological realities.

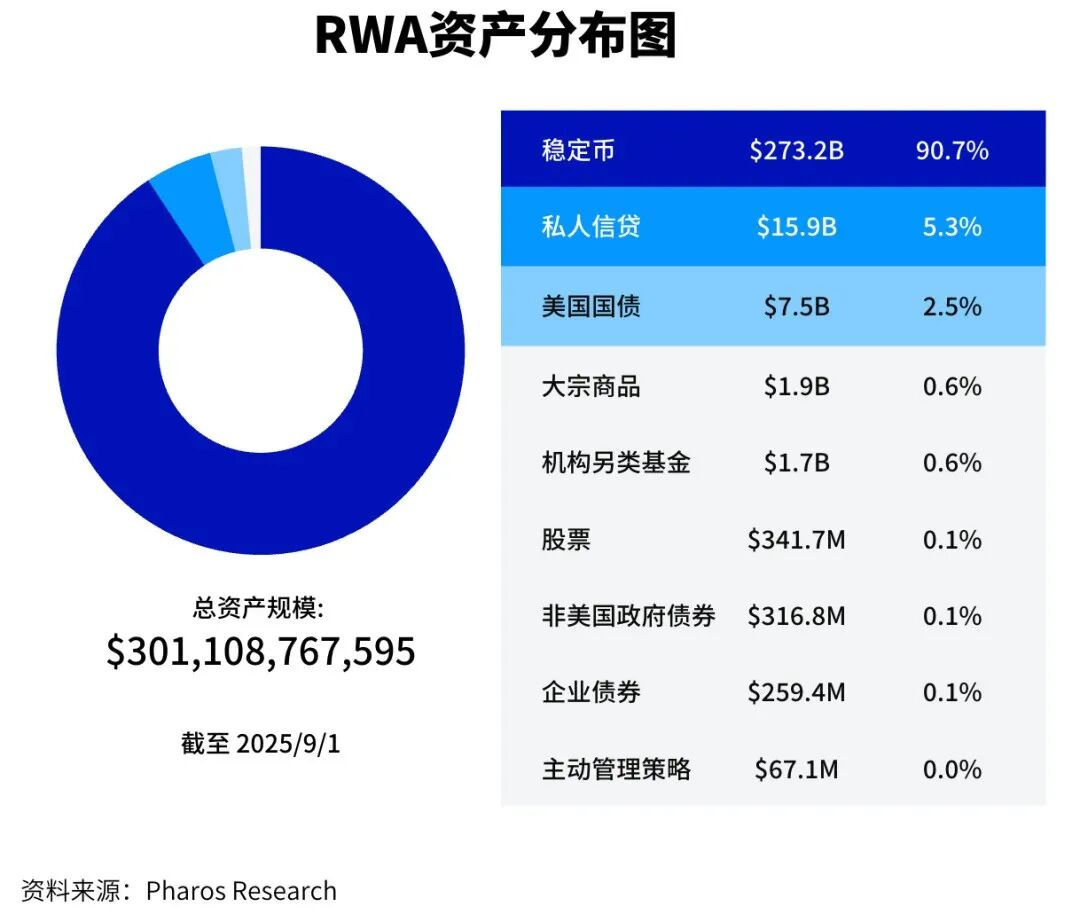

The following are the details of the main categories in the current structure of RWA off-chain assets as of September 2, 2025[3]:

• Stablecoins: The total stablecoin market capitalization is $273.18 billion, with a monthly transaction volume of $2.82 trillion, 33.02 million monthly active addresses, and 191 million stablecoin holding addresses. 99% of these stablecoins are pegged 1:1 to the US dollar. The top five stablecoins are USDT, USDC, USDS, USDE, and BSC-USD, with market shares of 60.79%, 25.33%, 4.58%, 3.43%, and 1.68%, respectively. Because USDT and USDC, the two leading stablecoins, hold approximately 75% of their off-chain assets in US Treasury bonds, stablecoins are considered a special type of US Treasury tokenized RWA. Currently issued stablecoins are primarily held on Ethereum and Tron, with stablecoin market capitalizations of $155.5 billion and $78.4 billion, respectively. Solana, ranked third, saw its stablecoin market capitalization plummet to $11.1 billion.

•Private credit: The total loan size of private credit is $29.58 billion, with an average yield of 9.75% and a total of 2,583 loans. The top three entities in the private credit field are Figure, Tradable, and Maple, with credit sizes of $15.30 billion, $5.02 billion, and $4.08 billion, respectively. Figure is the largest non-bank home equity line of credit (HELOC) provider in the United States, using blockchain and AI technology to provide consumers with fast online loan services. Tradable is a fintech company that assetizes private credit, allows it to be traded on the market, and provides an on-chain assetization platform for asset management institutions. Maple is a CeDeFi platform that provides digital asset loans and income products to institutional and individual qualified investors.

• U.S. Treasury Tokenization: Technically, the off-chain assets of U.S. Treasury tokenization are 100% U.S. Treasury bonds, with the majority of the proceeds from holding U.S. Treasury bonds distributed to token holders. The total value of U.S. Treasury tokenization is $7.46 billion, with an average yield of 4.08%, and a total of 52,793 holders. The top five U.S. Treasury tokenization projects are BUIDL (issued by Securitize), WTGXX (issued by WisdomTree), BENJI (issued by Franklin Templeton), OUSG (issued by Ondo Finance), and USDY (issued by Ondo Finance), with respective values of $2.39 billion, $880 million, $740 million, $730 million, and $690 million.

• Commodity tokenization: Current commodity tokenization is essentially equivalent to gold tokenization. Gold tokenization introduces a high-quality, decoupled asset from core crypto assets like BTC and ETH to the crypto market, allowing institutional and professional investors to diversify their crypto portfolios. Currently, the total value of commodity tokenization is $2.39 billion, with a monthly trading volume of $958 million, 7,866 monthly active addresses, and 83,700 holding addresses. Among these, PAXG, the gold tokenization project issued by Paxos, has a market capitalization of $975 million and a 40.80% market share; XAUT, the gold tokenization project issued by Tether, has a market capitalization of $8.54 million and a 35.75% market share.

• Institutional Alternative Investment Funds: The RWA model of private equity and hedge funds offers greater transparency, lower fees, and improved liquidity. Currently, institutional alternative investment funds have a total size of $1.75 billion, with 27 products. Centrifuge, Securitize, and Superstate rank first and third in this segment, with market shares of 40.31%, 37.34%, and 11.95%, respectively.

• US Stock Tokenization: The total value of US stock tokenization currently stands at $342 million, with a monthly trading volume of $164 million and 62,600 holding addresses. Securitize's Exodus Movement Inc. Class A tokenized US stock product has a market capitalization of $226 million and a 79.34% market share. Backed, which partners with Kraken, Coinbase, and Bybit to issue US stock tokenized products, has 71 products (including the S&P 500, T-bills, TSLA, and AAPL), with a total issuance value of $88 million and a monthly trading volume of $163 million.

The above data reveals that RWA's off-chain assets are primarily based on highly liquid and trustworthy standard assets (US Treasuries hold a monopoly position), supplemented by private credit. The primary forms of on-chain representation are transaction-medium stablecoins and interest-bearing stablecoins (YBS). The core business logic of RWA is to bring these real-world assets from off-chain to on-chain for yield generation and portfolio risk diversification.

However, as the new generation of high-performance public chains (represented by Monad, MegaETH, Pharos, etc.), the new generation of liquidity creation paradigms (intent Centric, CLOB and AMM integration, etc.), and the new generation of oracle technology (Chainlink, Redstone's high-frequency price feed function) enter the mature stage of their life cycle, the core business logic of RWA will evolve to focus on selling volatility, that is, on-chain high-frequency trading of tokenized US bonds, tokenized US stocks, tokenized financial derivatives and participating in their global pricing will become the new dominant paradigm for RWA in the next cycle.

In April 2025, Robinhood submitted a proposal to the SEC requesting a federal framework for tokenizing real-world assets (RWAs), aimed at modernizing the U.S. securities markets. Specifically, it aims to treat tokenized assets like stocks and bonds as legally equivalent to their traditional counterparts, rather than derivatives. The framework includes a hybrid liquidity system with off-chain matching for speed and on-chain settlement for transparency, as well as Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance tools. However, Robinhood's proposal will not be viable in the real market until the CLARITY Act is passed by the U.S. Congress later this year.

Therefore, Robinhood chose to launch tokenized US stock trading services in the EU on June 30th, allowing EU users to trade over 200 US stocks and ETF tokenized assets using blockchain technology. These tokenized assets are issued on Ethereum's L2 Arbitrum and will be migrated to the Robinhood Chain, which is isomorphic to Arbitrum.

Components and functions of the RWA middle layer

From a blockchain technology perspective, the RWA middle layer primarily addresses the consistency and finality of the status between off-chain assets and on-chain liabilities, as well as on-chain and off-chain messaging. From a business model perspective, the RWA middle layer primarily addresses off-chain security, credibility, and compliance, while on-chain liquidity, availability, and application scenarios.

The RWA middle layer stack consists of off-chain hosting entities, state settlement layer, oracle, application layer, interoperability protocol, on-chain liquidity layer, etc.

• Off-chain asset custodian: Off-chain asset custodians are responsible for managing underlying assets (e.g., custody of physical assets) and minting RWA asset-mapping tokens in a compliant, transparent, and trustworthy manner. Currently, the top five narrow RWA off-chain asset custodians are Securitize, Tradable, Ondo Finance, Paxos, and Superstate, with market shares of 28.0%, 16.0%, 10.6%, 6.9%, and 6.7%, respectively.

• State Settlement Layer: The state settlement layer is typically implemented by an L1/L2 blockchain and is responsible for the consistency and finality of the RWA asset state. Currently, the top five state settlement layers used by narrowly defined RWAs are Ethereum, Zksync Era, Stellar, Aptos, and Solana, with market shares of 59.4%, 17.7%, 3.5%, 3.4%, and 2.8%, respectively. The market share distribution of the RWA state settlement layer differs significantly from the familiar market share distributions of DEX trading volume, TVL, and transaction count. This is due to the fact that the current RWA business model is primarily business-to-business. Large and active retail investors prefer to participate in volatility trading. Therefore, for Solana, Sui, and other new-generation high-performance public chains, accelerating the transition of the RWA paradigm from yield generation to selling volatility is a pressing challenge. Only by addressing this challenge can they better adapt to the new system environment characterized by clearer regulatory policies and the integration of cryptocurrencies and stocks.

• Oracles: Oracles are responsible for providing secure and reliable off-chain data, ensuring that the on-chain representation of RWAs is synchronized with the real world. For example, RedStone's RWA Oracle provides price feeds for $20 billion worth of RWAs on the Solana chain (including Apollo's ACRED and BlackRock's BUIDL); Chainlink provides RWA asset PoR (Proof of Reserve) services for platforms/protocols such as Backed, Superstate, 21BTC, ARK 21Shares (ARKB), and Solv. Currently, oracles in the RWA space primarily serve the yield generation of off-chain assets and the lending, liquidation, and spot trading of on-chain assets. In the future, if oracles are expanded to high-frequency trading scenarios, there is room for optimization in terms of price feed speed, time granularity, and cost.

• Application Layer: The application layer provides on-chain debt-side use cases such as lending, LST, loops, interest tokenization, and vaults, enhancing the yield and liquidity of RWA assets. Mainstream DeFi protocols are still in the early stages of supporting and integrating RWA assets, and their attitude is relatively conservative. However, RWA public chains such as Plume and Pharos are actively building a complete set of application layer components for RWA.

• Interoperability Protocols: Currently, the most in-demand cross-chain interoperability in the RWA space is stablecoin transfers, which has contributed to Chainlink's CCIP protocol's high market share in this niche. However, with the improvement of chain-abstracted DEXs and Centric infrastructure, and the evolution of RWA off-chain asset structures, cross-chain bridges like Wormhole and Across are likely to gain traction.

• On-chain Liquidity Layer: Creating on-chain liquidity for RWAs has always been a systematic financial engineering exercise, requiring both spot liquidity for convenient swaps and futures liquidity for risk hedging. AMM-style liquidity is essential for cold-starts and long-tail assets, while CLOB-style liquidity improves capital efficiency and reduces transaction costs. Currently, the most fashionable and comprehensive on-chain liquidity layer consists of the DEX's LP Pool, aggregator's transaction routing, the intent DEX's Solver, and the chain-abstract DEX's intent aggregation. It's important to note that current on-chain liquidity optimization isn't limited to the execution layer of the blockchain stack, but extends deeper into the consensus layer, optimizing TX ordering and block finality performance and mechanisms. Examples include Celestia's new narrative, CLOB on Blobs, and Solana's new consensus algorithm, Alpenglow.

RWA on-chain liabilities: transaction medium stablecoin, YBS, RWA equity assets

The liability side is the financial abstraction layer that users directly contact, and its RWA is mainly expressed in the form of transaction medium stablecoins, interest-bearing stablecoins (YBS) and RWA equity asset tokens.

Medium-of-transaction stablecoins primarily include USDT and USDC. These are issued and maintained by centralized entities with extensive on-chain and off-chain liquidity networks. They offer advantages such as ease of access, low transfer costs, fast confirmation, and programmability. Medium-of-transaction stablecoins differ fundamentally from central bank digital currencies (CBDCs). While medium-of-transaction stablecoins are essentially on-chain tokens representing fiat cash, CBDCs are essentially new forms of fiat cash. The Trump administration in the United States explicitly opposes CBDCs and supports stablecoins, while the EU and China have chosen to promote CBDCs and restrict stablecoins. In this cycle, stablecoin application scenarios extend beyond the previously mentioned roles of medium of exchange and store of value in the crypto market, cross-border payments, and helping to liquidate US debt. These applications also include new use cases such as PayFi and supply chain finance, such as Huma's cross-border settlement financing and JD.com's stablecoin's supply chain finance. The primary battlefield for traditional stablecoin competition in the next cycle will be A2A micropayments. Tether and Circle have invested in and incubated Stablecoin and Arc, respectively, to ensure their continued leadership in the stablecoin market in the AI era.

To protect the traditional banking industry from disruption, the GENIUS Stablecoin Act prohibits compliant stablecoins from paying interest to stablecoin holders. This, in turn, provides a niche opportunity for YBS, a DeFi product primarily operating within the regulatory sandbox. YBS income typically comes from DeFi lending, market-neutral strategies, staking rewards, or interest income from RWAs. RWA YBS, which includes traditional financial assets such as US Treasuries and structured credits, can be used as collateral or investment targets for stablecoins after on-chain tokenization. This combination not only enhances the stability of stablecoins but also provides DeFi users with income opportunities similar to those in traditional finance.

RWA equity tokens are equity tokens that bring real-world assets (such as private credit, commodities, US Treasury bonds, and US stocks) onto a blockchain. Previously, RWA equity tokens had limited DeFi composability and on-chain liquidity. However, with the clarification of crypto regulation, embedding RWA equity tokens into DeFi and pursuing stronger on-chain liquidity has become a new trend. For example, AAVE recently launched an RWA lending platform that supports lending stablecoins against licensed RWA assets. In the future, equity tokens for US Treasury bonds, US stocks, and commodities will be legally equivalent to off-chain assets, further increasing the demand for DeFi composability and on-chain liquidity.

Observing the current market structure of RWAs, we find that the most successfully on-chain RWAs currently consist primarily of standardized assets with high liquidity and fair and effective market prices, such as US Treasury bonds, private credit, gold, and US stocks. Currently, RWAs are primarily focused on encapsulating and abstracting standardized assets into on-chain tokens.

This is due to technical bottlenecks in oracles' processing of non-standard asset prices and ownership, which has limited the RWA conversion of a vast number of non-standard real-world assets (such as real estate, industrial parks, land, forests, and mines). How are prices determined for non-standard assets like real estate and minerals? How is ownership confirmed? Existing oracle technology struggles to reliably assess prices and verify ownership of non-standard assets. Furthermore, putting non-standard assets on-chain typically requires the establishment of a legal entity (SPV) to hold the actual assets. On-chain tokens often represent only income rights, not actual property rights.

The future of RWAs isn't simply about moving "everything onto the blockchain." A more realistic path lies in finding a balance between regulatory compliance and technological innovation by abstracting the compliance layer (encapsulating real-world assets with legal entities) and enhancing on-chain liquidity (a high-performance public blockchain combined with a CLOB/AMM hybrid market-making model), thereby unlocking trillions of dollars in non-standard asset value. The large-scale explosion of RWAs for non-standard assets will likely require further maturity of oracle technology and the successful implementation of regulatory sandboxes, with a potential period of rapid growth expected after 2026.

03 Conclusion

RWA 1.0 simply tokenizes traditional assets such as real estate, industrial parks, and artworks. This approach is inherently flawed because it assumes that blockchain is a magic machine that creates liquidity.

The current RWA 2.0 is based on the stablecoin paradigm with U.S. Treasuries as the core reserve asset. It has achieved huge scale success in terms of transaction medium, cross-border transfer, and storage of value, but its compatibility with traditional financial infrastructure is not good enough, and there is serious friction when on/off ramp.

The future RWA 3.0 will use technologies such as high-performance blockchain, RWA-friendly oracles, AMM+CLOB hybrid model, and Intent Centric to create a new financial primitive for the era of sovereign individual capitalism driven by AI and Crypto.

What we are about to witness is not only a technological and financial innovation, but also a major historical process of restructuring the global capital order.