This report, authored by Tiger Research, analyzes the rapid growth of the digital asset custody industry, examines three business models, and explores regulatory approaches in Singapore, Hong Kong, Japan, and South Korea.

TL;DR

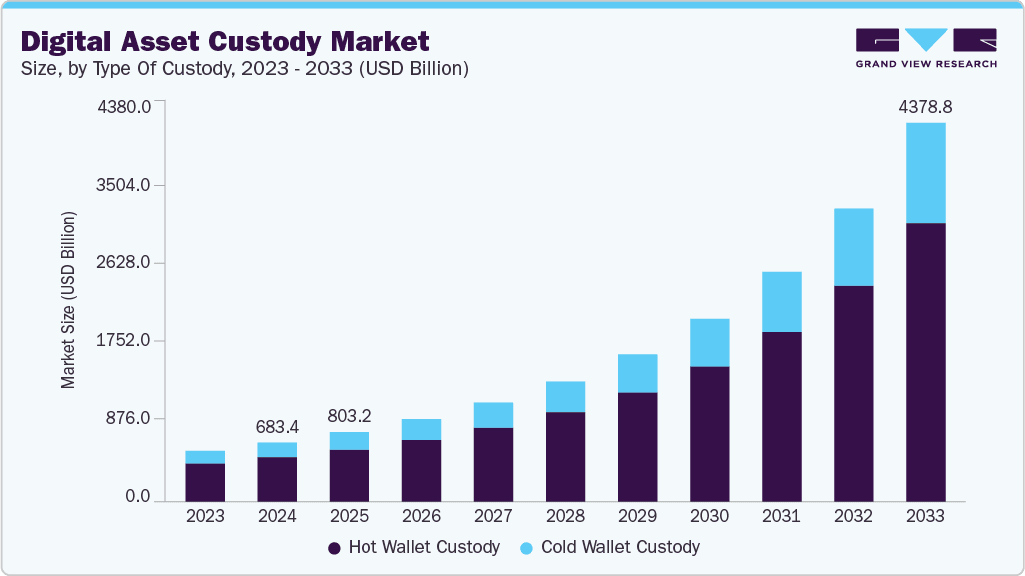

The global custody market is expected to expand by more than 50%, from $447.9 billion in 2022 to $683 billion in 2024, moving beyond simple storage to becoming an essential infrastructure for institutional engagement.

Custody service providers fall into three broad categories. Traditional custody services prioritize regulation and trust, hybrid services prioritize service diversification, and technology infrastructure-based services prioritize security and API provision. Singapore, Hong Kong, Japan, and Korea each have their own distinct local models.

The future of custody hinges on the growth of assets under custody and the services it offers, expanding into the financial infrastructure. At the same time, regulatory understanding and local adaptation are key factors in determining global expansion and the success of latecomers.

1. Custody: Why This Market Matters Now

The custody industry has grown rapidly since its institutionalization. Initially, custody was simply a service for holding virtual assets on exchanges. However, with increasing institutional demand, the customer base has steadily expanded. In particular, the expansion of the virtual asset ETF and digital asset treasury (DAT) markets has fueled institutional demand for virtual assets, leading to a corresponding increase in the size of custody held by custodians.

This is supported by the fact that the global custody market size grew by over 50% in just two years, from approximately $447.9 billion in 2022 to $683 billion in 2024. This growth is accelerating. While many reports project that the digital asset-focused custody market will grow by an average of 17-25% annually, even higher growth is expected now, as institutional infrastructure expands and large-scale institutional capital inflows begin in earnest.

Ultimately, as the scale of assets requiring custody services grows, the need for more stable and reliable services grows. This report examines how the custody market has formed and how custody services are being implemented in each country.

Be the first to discover insights from the Asian Web3 market, read by over 17,000 Web3 market leaders.

2. The custody industry that started from an accident

The custody industry began with an accident. The 2014 hacking incident at the Japanese exchange Mt. Gox was the starting point. Approximately 850,000 Bitcoins were stolen, resulting in massive losses for customers. This incident solidified the industry's perception that "business in the market cannot be conducted without institutional mechanisms to safely store assets."

This shift in perception led to regulatory developments. Since the incident, regulations surrounding the virtual asset custody industry have continued to evolve. In particular, the United States has established custody guidelines similar to those for traditional finance. These regulatory overhauls have laid the foundation for the custody industry to thrive under clearer standards.

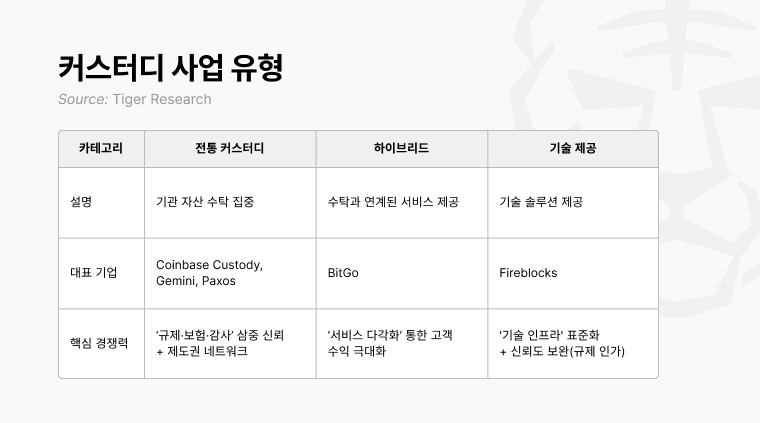

Custody operators generally operate primarily through consignment services, but also offer a variety of additional services. This means that depending on the primary focus of the business, their market positioning and competitiveness can vary significantly.

Custody service providers fall into three main categories. First, there are those focused solely on asset custody, like traditional custodians. Second, there are hybrid providers, which focus on expanding their offerings beyond custody. Third, there are those offering technology-based solutions, such as SaaS. Each model targets different customer segments and needs, competing in the market based on their respective strengths.

The core business direction of traditional custody services lies in "custody." They have built a high level of trust based on numerous successful examples, and based on this, they focus on safely storing institutional investors' virtual assets. A representative example is Coinbase Custody.

Coinbase Custody's success is evident in the US spot ETF market. As of 2025, the company held custody of nine out of eleven SEC-approved Bitcoin spot ETFs and eight out of nine Ethereum ETFs. It has secured an overwhelming market share and established itself as the most trusted custodian.

This trust stems from Coinbase's strategic decision to secure regulatory approval early on. Coinbase Custody received a Limited Purpose Trust Charter from the New York Department of Financial Services (NYDFS) in 2018. In 2025, it was recognized as a "Qualified Custodian" under the Securities and Exchange Commission's (SEC) asset custody regulations. This grants Coinbase Custody the legal status to hold customer assets in custody, much like a typical bank or securities firm.

While other competitors are only just beginning to gain approval, Coinbase already boasts years of operational experience. This accumulated experience plays a crucial role in attracting new institutional clients. While technological prowess is crucial when companies choose a custody service, ultimately, a proven track record is the key criterion for trust.

Ultimately, the core competitive edge of traditional custody systems lies in their accumulated experience. Even if a latecomer emerges with exceptional technology, it will be difficult for them to surpass the established players, who focus on the essence of custody based on their accumulated regulatory history and operational experience.

Hybrid models primarily focus on virtual asset custody, but also offer a variety of services linked to custody. Simply put, they are a comprehensive package that provides institutional clients with everything from asset custody to asset management. A prime example of this model is BitGo.

Bitgo's services extend beyond custody, encompassing staking, over-the-counter (OTC) trading, lending, and real asset tokenization (RWA) management. It supports asset management and financial system integration through institutional wallets and API infrastructure, and its staking service is integrated with custody accounts. Regarding OTC trading, Bitgo operates under license from the German Financial Supervisory Authority (BaFin).

Furthermore, Bitgo leveraged its diversified service offerings to achieve rapid global expansion. Early entry into regulatoryly flexible markets like Hong Kong, Singapore, and Abu Dhabi allowed the company to offer a diverse range of services tailored to each region, enabling it to rapidly build a customer base.

Ultimately, the core competitiveness of hybrid platforms lies in "service diversification based on custody services." This is because they can offer a wide range of functions, from simple custody functions to trading, operations, and tokenization. While traditional custody platforms derive their growth momentum from "regulatory trust," hybrid platforms derive their growth momentum from "service diversification."

Technology providers do not directly store virtual assets. Instead, they sell technology solutions that enable banks, exchanges, and fintech companies to build their own storage systems. Fireblocks is a leader in this field.

Fireblocks leverages its outstanding technical expertise to support client service development. This is evidenced by its acquisition of major clients such as BNY Mellon, Galaxy Digital, and Crypto.com. As of 2025, assets under management on the Fireblocks platform amount to approximately $200 billion, with over 1,800 clients. Thanks to its accumulated experience and proven technology, Fireblocks has become the preferred technology partner for companies developing custody services.

In 2024, Fireblocks received a limited purpose trust license from the New York Department of Financial Services (NYDFS), legally empowering it to directly custody assets. However, Fireblocks' core focus remains as a "technology solutions provider." Obtaining the license is more of a means of enhancing credibility to secure institutional clients. While Fireblocks has evolved into an infrastructure company with direct custody capabilities, it is leveraging this as a strategic tool to further solidify its technology-centric market position.

Not all countries apply the same financial regulations. Because regulatory standards vary across countries, demand for local companies tailored to each country's circumstances is steadily increasing. Even though the market for ETFs and DATs (digital asset trusts) isn't as vibrant as in the US, services tailored to each country's regulatory environment exist.

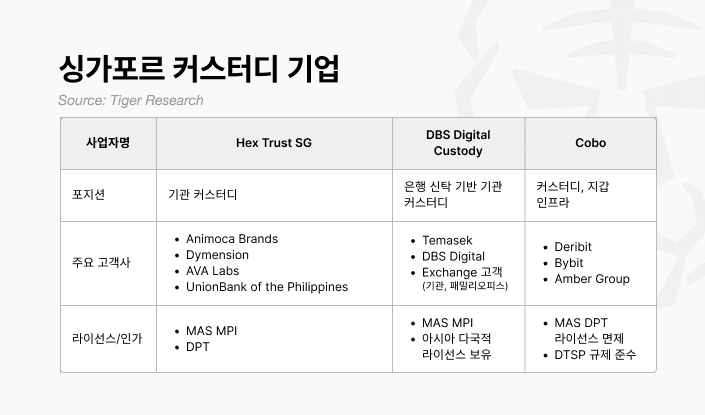

Singapore expanded custody into the scope of virtual asset services through the Financial Services and Markets Act (FSMA) on June 30th. Accordingly, custody firms that cater exclusively to international clients must obtain MAS approval to operate in Singapore. MAS has announced stricter criteria for issuing custody licenses, implying that only banks and institutional firms will be eligible to participate.

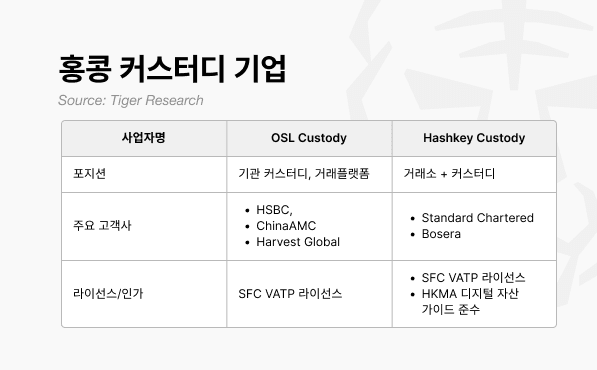

Hong Kong integrated trading and custody into a single regulatory framework when the SFC introduced the VATP system in 2023. This system goes beyond a simple registration system and establishes a structure that simultaneously authorizes exchanges and custody services.

OSL provides integrated custody, OTC, and tokenization services linked to exchanges, and notably, supports custody for three of the four spot virtual asset ETFs approved in Hong Kong. HashKey, in partnership with Standard Chartered, provides fiat on-ramp and off-ramp services to institutional investors, leveraging its infrastructure to enhance the efficiency of virtual asset-to-fiat settlements.

Hong Kong's direction is as clear as its laws. The custody industry is centered around "regulation + bank collaboration." While Singaporean custody firms have served as a bridge for the industry by collaborating with global players, Hong Kong's model is one of attracting institutional capital through collaborations with traditional financial institutions and local custody businesses.

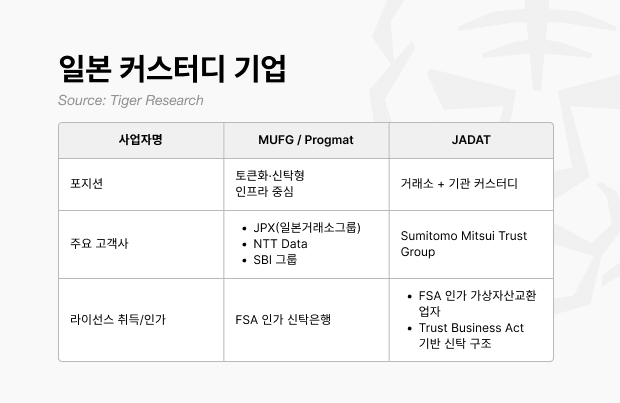

Japan's Financial Services Agency (FSA) enforces regulations that prioritize the protection of customer assets. Custody providers are required to store at least 95% of customer assets in cold wallets isolated from the internet. For the remaining 5% or less in hot wallets, fiat currency or bonds of equal size must be deposited as collateral, and external audits are also mandatory.

Due to these high regulatory barriers, the Japanese custody market is dominated by traditional financial groups rather than Web3-native companies. Only financial groups with the capital and system infrastructure can meet the FSA's stringent requirements.

MUFG/Progmat, for example, is focusing on tokenization and building trust infrastructure based on its FSA-authorized trust bank credentials. JADAT has adopted a hybrid model that combines exchange and institutional custody functions. It operates as an FSA-authorized virtual asset exchange operator and a Trust Business Act-compliant trust structure, offering both trading and custody services.

Japan is a classic example of how the influence of traditional finance grows as regulations become more stringent. Due to the high collateral standards and external audit requirements imposed by financial authorities, banks and trust companies with strong capital and systems have come to dominate the market.

The Korean custody industry is governed by the Special Financial Transactions Act and operates through registration as a Virtual Asset Service Provider (VASP). A key characteristic of the Korean market is the simultaneous development of financial institution integration and technology-based differentiation. A diverse range of models coexist, from joint ventures led by traditional financial institutions like KODA to startups competing on security and infrastructure differentiation.

Recently, in preparation for Phase 2 of the Financial Services Commission's roadmap for corporate virtual asset trading, exchanges have launched a full-scale competition to secure corporate clients. This is because institutional demand is expected to intensify once the corporate investor market opens.

A near-term turning point for the Korean virtual asset custody industry is the entry of approximately 3,500 professional investors. If these institutions participate and achieve tangible results, there is a high possibility that the industry will expand into real-world asset-linked products, such as security token offerings (STOs) and real-asset tokenization (RWA). This is a time when institutional entry goes beyond mere regulatory compliance and can lead to the creation of new markets.

Competitive strategies in the custody industry can be broadly divided into two categories.

The first is to establish a customer base by securing a market lead, like Coinbase Custody. The second is to differentiate through diversifying services like staking, real-asset tokenization (RWA), and lending, tailored to market demand, like BitGo.

The virtual asset market is now shifting from a structure centered on individual investors to one that includes institutional investors. In response, custody firms are focusing on establishing bank-level custody and auditing systems that institutions can trust. At the same time, technological infrastructure services that facilitate the entry of new players into the market are also attracting attention.

However, successful entry requires understanding each country's regulatory direction and local ecosystem. In the US, institutional trust must first be secured through licensing procedures, and the daunting hurdle of Coinbase Custody must be overcome. In Hong Kong and Singapore, a collaborative model with banks is key to success. Japan, with its stringent customer asset protection regulations, prioritizes collaboration with local major companies for entry. While Korea boasts a diverse range of operators, it still takes time for institutional investors to fully embrace the market.

Therefore, companies seeking to enter the market must focus on accuracy rather than speed. Only companies that properly analyze the regulatory environment and design collaborative structures with local financial institutions and partners can achieve stable growth. Even latecomers can seize opportunities by establishing structures and partnerships that align with the system.

이번 리서치와 관련된 더 많은 자료를 읽어보세요.

Disclaimer

This report has been prepared based on reliable sources. However, we make no express or implied warranties as to the accuracy, completeness, or suitability of the information. We are not responsible for any losses resulting from the use of this report or its contents. The conclusions, recommendations, projections, estimates, forecasts, objectives, opinions, and views contained in this report are based on information current at the time of preparation and are subject to change without notice. They may also differ from or be inconsistent with the opinions of other individuals or organizations. This report has been prepared for informational purposes only and should not be construed as legal, business, investment, or tax advice. Furthermore, any reference to securities or digital assets is for illustrative purposes only and does not constitute investment advice or an offer to provide investment advisory services. This material is not intended for investors or potential investors.

Tiger Search Report Usage Guide

Tigersearch supports fair use in its reports. This principle allows for the broad use of content for public interest purposes, provided it does not affect commercial value. Under fair use rules, reports may be used without prior permission. However, when citing Tigersearch reports, 1) "Tigersearch" must be clearly cited as the source, and 2) the Tigersearch logo must be included. Reproducing and publishing materials requires separate agreement. Unauthorized use may result in legal action.