Author: Bai Ding, Xian Ran

Blockchain technology is reshaping the global financial system, and RWA has become a bridge between traditional finance and DeFi. Once traditional assets such as real estate, art, bonds, and gold are converted into on-chain tokens, they can achieve global asset mobility and ownership separation. This is undoubtedly a financial technology revolution.

According to current market data, the market capitalization of non-stablecoin RWAs has reached $33.7 billion and is expected to exceed one trillion yuan by 2030. This success is due to the trustlessness and transparency of blockchain in asset custody and circulation. However, it is clear that RWAs also face challenges in liquidity fragmentation and security.

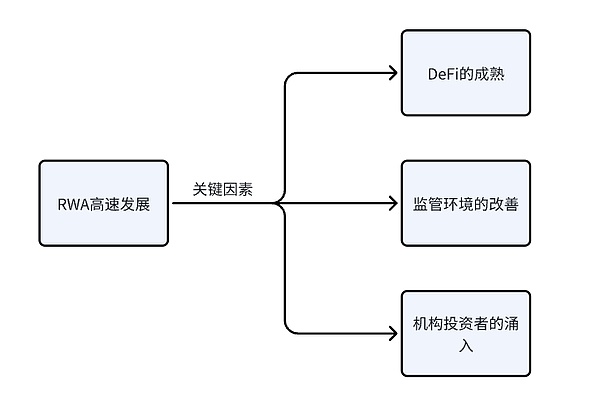

The concept of RWA stems from blockchain's digital transformation of traditional assets, mapping physical assets into programmable tokens to absorb global liquidity. According to a recent report, the RWA tokenization market is expanding at a compound annual growth rate (CAGR) exceeding 50%, driven primarily by the maturation of DeFi, an improving regulatory environment, and an influx of institutional investors.

For companies in traditional industries, issuing RWAs has multiple positive implications.

First, it broadens financing channels . Traditional financing methods often rely on bank loans or stock issuance, but these methods have high barriers to entry and long cycles. Through RWA, companies can tokenize assets such as real estate and intellectual property, directly attracting global investors and achieving low-cost financing. For example, a real estate company can split a property into thousands of tokens, each costing only a few hundred dollars. This low-barrier approach can significantly reduce financing costs.

Secondly, RWA improves asset liquidity . For example, art or private equity often have extremely poor liquidity, and transactions can take months from proposal to completion. However, through on-chain RWA tokens, these assets can be traded instantly in the secondary market at any time.

Furthermore, RWA promotes financial innovation and effective risk diversification. Traditional investment institutions can create new financial products through tokenization, such as yield-bearing tokens, allowing token investors to receive dividends from asset returns. Furthermore, RWA of heavy assets like real estate can fragment ownership, attracting a diverse range of investors and effectively diversifying risk.

Furthermore, RWAs have enhanced the competitiveness of certain companies. Amidst the wave of digital transformation, companies adopting blockchain technology are more likely to gain access to resources within the Web3 ecosystem and the attention of investment and financing institutions. For example, last August, Longsin Group partnered with Ant Financial to complete China's first RWA financing transaction based on new energy assets. The financing involved using some of Longsin's charging stations as RWA anchor assets, raising 100 million RMB.

Overall, RWA can inject vitality into traditional companies, helping them transition from closed local markets to a global, open system. However, despite its significant significance and rapid development, RWA is hampered by a core pain point: in the Web3 world, there are too many public chains, and liquidity is spread across hundreds of them, resulting in severe fragmentation.

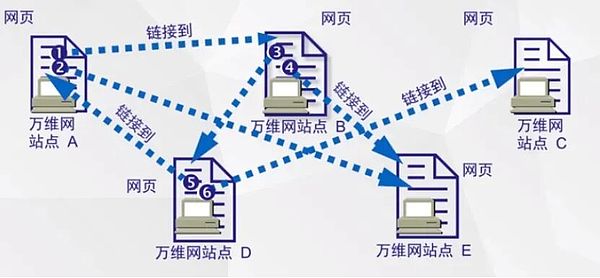

In fact, similar phenomena are common in the traditional internet. Before the World Wide Web (WWW) became the dominant text data transmission protocol, there were multiple competitors, such as Gopher, Archie, WAIS, Usenet, and BBS. These systems or protocols all provided file retrieval, forum communication, and file transfer capabilities, but due to various limitations, they ultimately operated independently and failed to establish a unified and efficient consensus.

After Tim Berners-Lee proposed the concept of the World Wide Web in 1989, it quickly became popular thanks to its hypertext links, multimedia support and user-friendliness. By 1995, the World Wide Web had basically established its dominant position, ending the mixed and incompatible state of Internet text transfer protocols and realizing a unified, open and inclusive network system on a global scale.

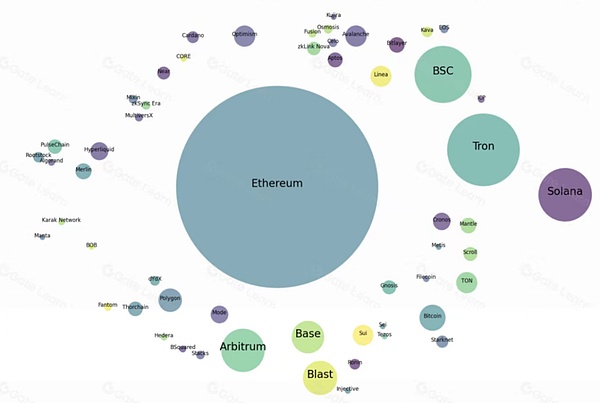

Compared to the traditional internet, blockchain, deeply tied to financial capital and geopolitical factors, has long lacked a unified set of standards. Furthermore, with everyone eager to build a public blockchain, even after more than a decade of development, it remains far from achieving the same unified technical standards as the traditional internet, and remains multipolar to this day. Many public chains have their own set of technical standards and independent ecosystems, leading to a serious problem: liquidity fragmentation.

Different public chains such as Ethereum, Solana, and Sui each have their own advantages, but assets cannot flow seamlessly across chains, and traders are forced to be limited to the liquidity pool of a specific chain.

For example, an RWA token issued on Ethereum may not be easily transferable to Solana, a pain point that can be magnified into a systemic problem.

First, insufficient liquidity leads to large price fluctuations. The trading volume of single-chain RWA is often limited and easily manipulated by large investors, and investors face high slippage risks.

Secondly, the opportunity cost is high. Users need to switch wallets and assets between multiple chains, which increases operational complexity and security risks.

Third, from an ecological perspective, single-chain issuance hinders the deep integration of RWA and DeFi , and cannot fully utilize cross-chain DeFi income or lending opportunities.

This is the blockchain's "island effect." Consensus mechanisms and token standards (such as ERC-20 and SPL) across different chains are incompatible, and asset transfers rely on cross-chain bridges, which are often the weakest link in the system. Cross-chain bridges not only hinder the development of RWAs but also restrict the development of the entire blockchain industry.

Current cross-chain technology and its pain points

To address the problem of blockchain silos, various cross-chain technologies have emerged. However, most solutions fail to perfectly achieve multi-chain liquidity transfers, not to mention that many cross-chain bridges do not support RWA assets. To this day, the simplest and crudest multi-signature cross-chain bridges remain the mainstream, but these solutions have been plagued by numerous failures. As of June 2025, cross-chain bridge hacks have resulted in losses exceeding $2.8 billion, the vast majority of which were caused by multi-signature bridges.

For RWA, since it involves high-value physical assets, any security vulnerability could result in huge losses. This is much more complex and difficult to resolve than simple Web3 issues. Therefore, cross-chain issues have become one of the bottlenecks in the development of RWA. How to efficiently mobilize liquidity within the multi-chain ecosystem is a serious issue.

Another significant pain point of traditional cross-chain bridges is excessive latency. Verification of multi-signature bridges requires consensus among multiple nodes, so asset transfers from Ethereum to Solana can take minutes to half an hour, a significant challenge for those accustomed to instant payments in the traditional financial system. In high-frequency trading scenarios, high latency can severely restrict the efficiency of RWA circulation, especially during market fluctuations, where delays of seconds can lead to significant losses.

The operational experience of cross-chain bridges is another major bottleneck. For example, if a user wants to use coin B on chain A to purchase coin D on chain C, a so-called "ABCD transaction," they must go through a tedious process: first, convert the coin to a shared asset on chain A's DEX, then transfer it to chain C via a cross-chain bridge, and finally complete the transaction on chain C's DEX.

The entire process requires users to complete it manually in at least three dApps. This not only involves multi-chain wallet switching and gas fee payment, but also requires understanding the operating logic of the bridge protocol. Non-experienced Web3 users find it difficult to master it. Potential Web3 users give up participating in on-chain interactions due to the complexity of cross-chain operations, accounting for almost 95%, which greatly limits the popularity of RWA and the expansion of the Web3 ecosystem.

The rise of chain abstraction and case studies

Based on the above analysis, the limitations of traditional cross-chain bridges in security, speed, and user experience make it difficult to meet the needs of the rapid growth of RWA and the expansion of the Web3 ecosystem. Centralization risks, transaction delays, and cumbersome operational processes not only hinder the full-chain liquidity of RWA assets, but also restrict the participation of non-experienced users, hindering the popularization of Web3.

In this context, chain abstraction as an emerging concept has gradually attracted attention, providing a new perspective for solving cross-chain interoperability.

Chain abstraction is a grand vision of Web3. It refers to shielding various complex operational details and cumbersome components through a single user interface, so that users do not need to be aware of the existence of major public chains and liquidity pools. It can help users automatically obtain liquidity within different public chain ecosystems with one click on a single platform, and provide the best trading experience through the method of "analyzing user intent → splitting orders → routing → transaction".

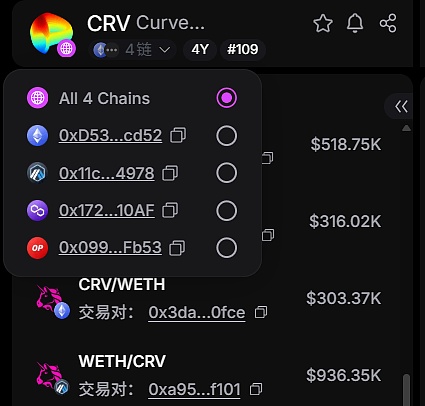

For example, within the UniversalX platform, we can see the liquidity distribution of CRV tokens across four public chains. The platform can automatically split large user orders into multiple smaller ones, each interacting in different pools to minimize slippage. Achieving this requires a mature, cross-chain interaction system.

In addition to UniversalX, some other cutting-edge projects have begun to fully explore the potential of chain abstraction and intent platforms, attempting to reshape the issuance and circulation model of RWA through bridgeless interoperability and unified settlement mechanisms.

For example, PicWe leverages omni-chain infrastructure to aggregate liquidity across the entire chain and issue RWAs with one click. This approach helped AK BUURA Energy Group raise $1 million through RWAs for its Isfayram Phase I small hydropower station. PicWe's omni-chain RWA solution offers a deeper understanding of the impact of chain abstraction on RWAs.

PicWe has built a user-intentioned, full-chain swap system for RWA assets in the Initial RWA Offering (IRO). Using the stablecoin WEUSD as the medium of exchange, PicWe eliminates the need for traditional bridges. This design eliminates the complexity of inter-chain operations and optimizes liquidity and security.

PicWe's chain abstraction implementation is based on the Chain Abstract Transaction Model (CATM). This model is essentially a distributed transaction coordination framework, deploying standardized contracts on each chain PicWe connects to. These contracts act as state synchronization and execution nodes. Unlike traditional cross-chain solutions that rely on a "lock-and-mint" process involving an intermediary bridge, CATM employs intent-driven execution logic:

Users submit transaction intentions on the source chain, and the system automatically matches and settles transactions through the contract network, eliminating the need for manual user intervention in inter-chain transfers. This abstraction layer treats multiple chains as a logical entity, with users experiencing only a single transaction entry point. Under the hood, contracts handle verification, routing, and release, ensuring atomic execution across multiple chains.

The key technology behind CATM is the Omni-Chain Permissionless Bidding Orchestration Protocol (OPBOP), an open bidding coordination protocol that allows any liquidity provider (LP) to participate in cross-chain order matching without permission. OPBOP works similarly to a decentralized auction market:

When a user initiates a cross-chain purchase, the protocol broadcasts the order details to the contract pool on the target chain. LPs then bid to provide the desired assets based on real-time quotes. This bidding process incorporates a time-decay mechanism—the initial bid is high, and as more LPs respond, the price gradually decreases until the optimal match is reached.

In this way, not only is low-threshold liquidity injection achieved, but economic incentives can also be used to encourage LPs to actively bridge supply gaps, avoiding the static lock-in of traditional bridges.

If OPBOP is the technical basis for PicWe to complete chain abstract swap, the stablecoin WEUSD is an important medium in this process.

WEUSD is minted at a 1:1 ratio using user-collateralized USDC and can be redeemed at any time. In the "ABCD transaction" process mentioned earlier, Coin B on Chain A is first swapped for WEUSD on Chain A, then automatically converted to WEUSD on Chain C by PicWe's smart contract, and finally swapped back to Coin D. This entire process is completed with a single click on the PicWe exchange. Users are completely unaware of the cross-chain bridge and WEUSD; it's as if their Coin B has been directly exchanged for Coin D.

In DeFi, WEUSD will be used as collateral for lending to enable multi-chain yield farming; on the RWA platform, it bridges TradFi assets such as bonds or real estate tokens to ensure compliant circulation and undertake the income settlement of RWA assets; in cross-chain payments, WEUSD becomes the exchange medium for the entire chain.

As PicWe integrates more and more chains, even into all public chains, WEUSD will become the settlement layer of the entire blockchain ecosystem, providing support for DeFi, RWA platforms, and cross-chain payments. If this process can be effectively promoted, we may see the emergence of a standardized RWA full-chain liquidity protocol.

Conclusion

The rise of RWA opens up a vast prospect for Web3, connecting traditional finance with the decentralized ecosystem. However, the fragmentation of cross-chain liquidity, security risks, and complex user experience remain core pain points that hinder its potential. The island effect caused by single-chain issuance, the high cost and latency of traditional cross-chain bridges, and the entry barriers for non-experienced users have all hindered the global circulation of RWA and the innovative vitality of Web3.

Chain abstraction, as an emerging paradigm, shields the complexity of multi-chain operations and enables seamless asset flows. Chain abstraction not only promises to address the challenges of cross-chain interoperability but also enhances the capital efficiency and security of RWA. Perhaps in the future, as chain abstraction technology matures and cross-chain issues are truly resolved, RWA will be able to move from a tens-billion-dollar market to a trillion-dollar market, truly achieving the deep integration of traditional and digital finance.