Human economic history is essentially a history of the continuous definition, quantification, and financialization of "value." From seashells and gold to paper money and stocks, and now to digital assets, every leap in financial paradigms stems from our renewed answer to the question, "What is value?"

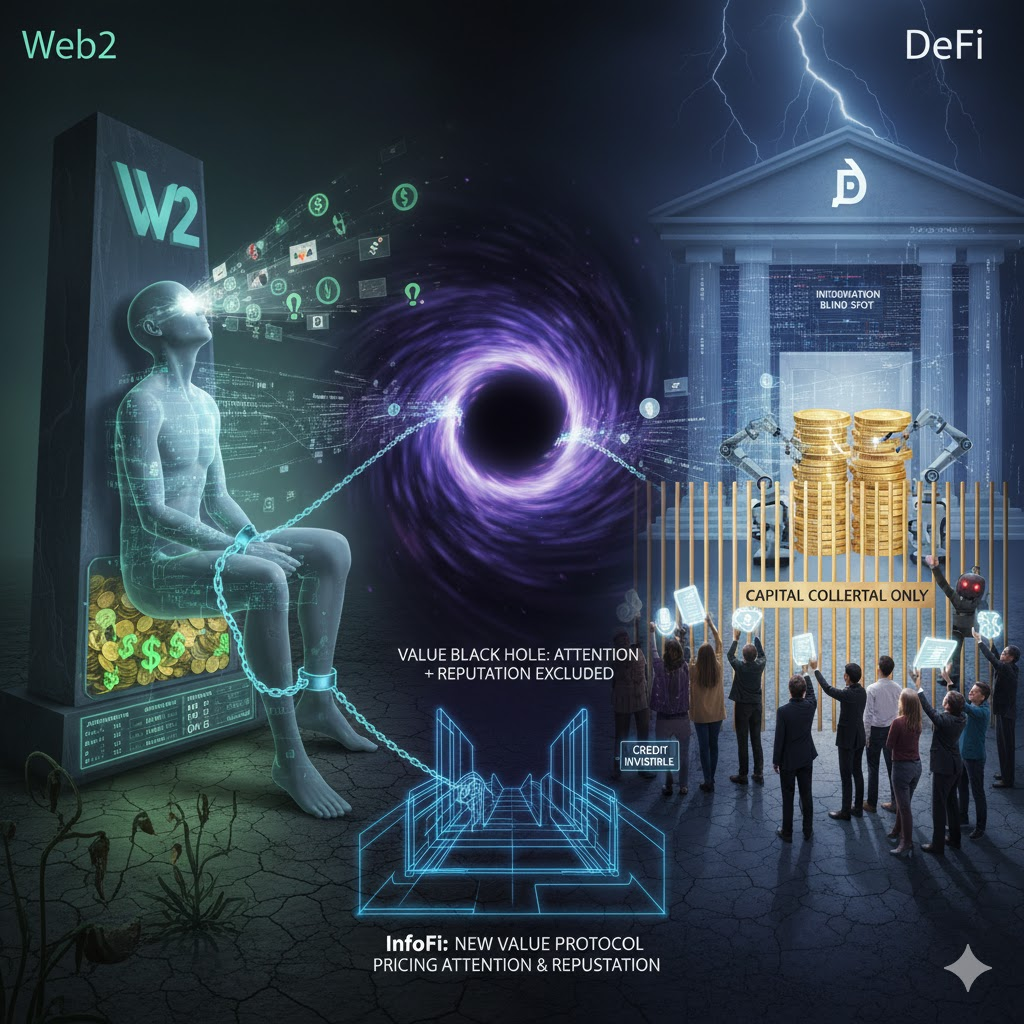

Today, contemporary digital civilization faces two core dilemmas: on the one hand, there is the "digital exploitation" of Web2, a trillion-dollar attention economy whose fuel is provided free of charge by 99% of "digital tenants," while its value is ruthlessly captured by 1% of platform operators; on the other hand, there is the "capital wall" of DeFi, a revolution aimed at "financial inclusion" that excludes billions of "credit-invisible" individuals worldwide due to its systemic reliance on "over-collateralization."

These two seemingly separate problems, belonging to "social media" and "decentralized finance," share a strikingly similar root cause: all of our existing financial systems have failed to provide a fair and credible pricing standard for the most valuable intangible asset of the digital age—human reputation and attention.

I. Exploited Value and Excluded Credit

Before proclaiming the future, we must deeply understand the current predicament. The limitations of Web2 and DeFi together constitute the "historical inevitability" of the birth of InfoFi.

First, there is the "sovereignty" dilemma of Web2: value is being exploited.

The Web2 business model is "you are not the user, you are the product." Platforms manipulate our dopamine levels through algorithms to maximize our "time spent on the platform," and then package and sell this "marketable attention" to advertisers. We are the "data fuel" of this trillion-dollar empire, yet we have no say in the distribution of value.

The fundamental flaw in this model lies in "sovereignty mismatch." Our digital identities, social graphs, content libraries, and influence—these intangible assets that should constitute the core of our "digital sovereignty"—are instead locked within the walled gardens of the platform, becoming merely a line of numbers on the platform's "balance sheet." We cannot own them, carry them, control them, or benefit from them.

Secondly, there is the "trust" dilemma of DeFi: credit is rejected.

DeFi was created to replace TradeFi's expensive and inefficient institutional trust intermediaries with a trustless system based on "code is law." It was a brilliant innovation, but it came at a high price.

To manage risk in an anonymous environment, DeFi has chosen the sole path of "overcollateralization." It only recognizes "capital," not "credit." This "capital wall" systematically excludes the billions of people with "invisible credit"—those who possess abundant "reputation assets" (such as skills, influence, and business reputation) but lack the "crypto collateral" recognized by DeFi.

The fundamental flaw of this model lies in its "information blind spot." Ironically, DeFi, as a product of information technology, lives in this information blind spot. It cannot read, verify, or quantify "reputation," the oldest and most important source of credit in the financial system, and thus can only self-mutilate, becoming "the rich man's Lego."

The picture is now clear: Web2 exploits our "attention assets," while DeFi excludes our "reputation assets." These two types of assets are precisely the most valuable and urgently needed core production factors in digital civilization.

A systemic value black hole has formed, spanning both Web2 and Web3. This is no longer an "application layer" problem; it's an "infrastructure layer" crisis. We need a completely new value protocol, a fundamental standard capable of pricing both "attention" and "reputation."

II. InfoFi Defines the Third Wave of Finance

Looking back at the evolution of finance is looking at the evolution of "trust." From TradeFi to DeFi, and then to InfoFi, these represent three great leaps in the cornerstone of trust.

The first wave was TradFi (traditional finance), whose cornerstone of trust was institutional credit. TradFi operates on the principle that trust originates from centralized institutions—banks, governments, law firms, and clearinghouses. Financial services are a "top-down" privilege; you must first be "permitted" by an institution to participate. Its limitations are obvious: high barriers to entry, low efficiency, and financial exclusion.

The second wave is DeFi (Decentralized Finance), whose cornerstone of trust is programmable capital. The operating logic of DeFi is to replace institutional credit with "code is law." It "removes" trust in institutions, but in order to manage risk in an anonymous environment, it also "removes" trust in people. It only trusts the capital you stake. Financial services become anonymous contracts that are "permissionless." The revolution of DeFi lies in making "capital" programmable, but it also exposes a fact: a financial system that only understands "capital" but not "credit" is incomplete.

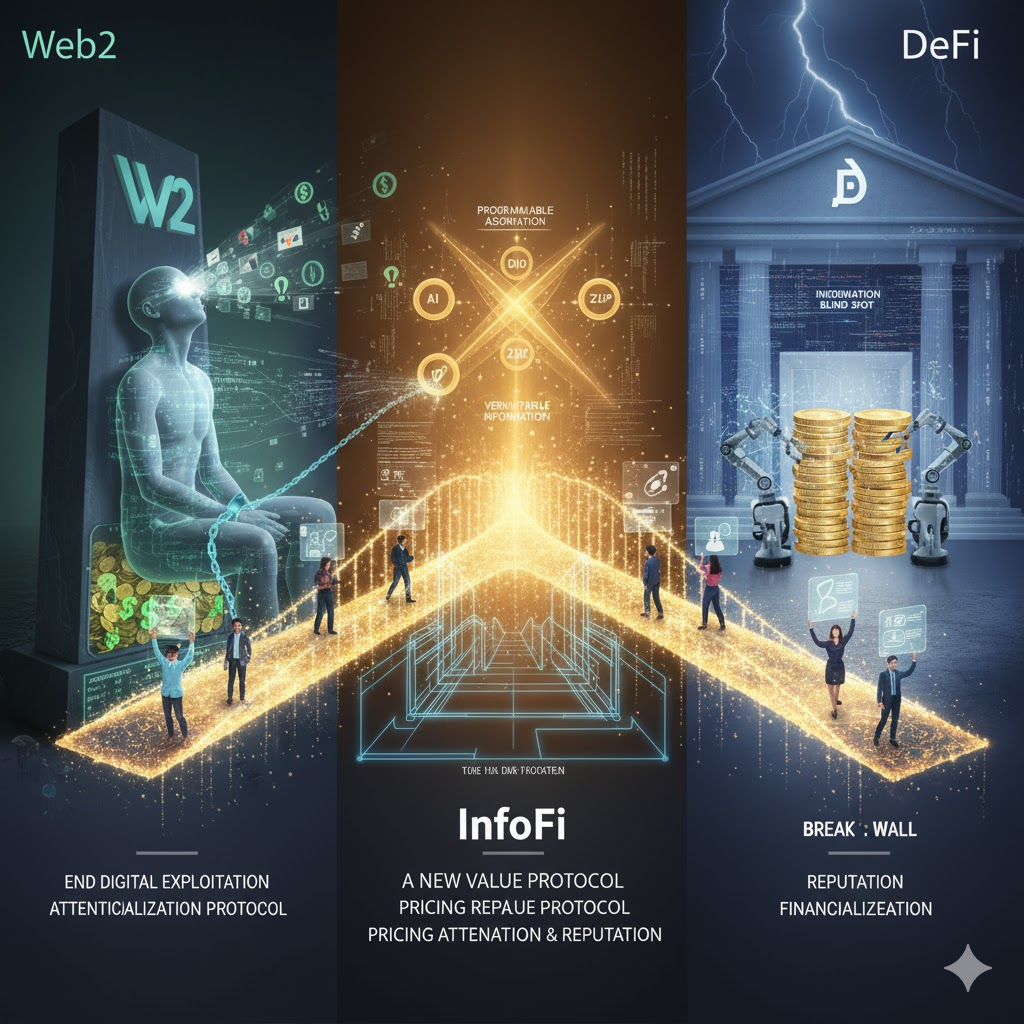

Now, we are witnessing the third wave: InfoFi. Its cornerstone of trust is programmable reputation and information. The operating logic of InfoFi is that the source of trust is no longer institutions or anonymous collateral, but "verifiable information." It aims to objectively "quantify" assets that have long been considered "intangible" through tools such as AI, DID, and zero-knowledge proofs (ZKP), making them programmable, tradable, and verifiable.

The core of the InfoFi Manifesto is simple: in the digital age, your reputation and attention are your most valuable digital assets. They must be quantified, recognized, priced, and sovereignly owned by you.

III. How InfoFi Unties the Deadlock Between "Exploitation" and "Exclusion"

InfoFi is not just a grand narrative; it's a systemic solution. It will fundamentally cure the chronic problems of Web2 and DeFi because it directly addresses that shared "value vacuum."

On the one hand, InfoFi aims to end Web2's "digital exploitation" through "value sovereignty".

The root of Web2 exploitation lies in the platforms' monopoly on the pricing and revenue rights of "attention." InfoFi aims to build an open, decentralized "attention financialization protocol." In this new protocol, value will no longer be assessed using platform-private, black-box algorithms focused on "stay time," but rather through a transparent AI model shared by the community and focused on "value contribution." Simultaneously, brand (advertiser) budgets will no longer be paid to the platform, but directly injected into a "value pool" managed by smart contracts. Users and creators will directly receive rewards from this pool through valuable contributions (such as in-depth content and high-quality curation).

On the other hand, InfoFi breaks down the "capital walls" of DeFi with "reputation finance".

The root of DeFi's rejection lies in its inability to identify and quantify "reputation" as a substitute for "over-collateralization." The core of InfoFi is to build a global verification layer for "reputation and trust." On this new infrastructure, it will securely aggregate your cross-platform, cross-chain data (using privacy technologies like ZKP), including your on-chain behavior, social influence, and even professional contributions. Based on this "programmable reputation," DeFi will, for the first time, be able to provide "low-collateral" or even "uncollateralized" financial services. This is the true beginning of "Bank the Unbanked," unlocking the economic potential of billions of "credit-hidden" individuals and opening up a trillion-dollar incremental market for DeFi.

Looking back, TradeFi financialized "institutional credit," and DeFi financialized "programmable capital." Both waves created immense value but also left profound regrets. Today, we stand at the starting point of the third wave. InfoFi is not about overthrowing DeFi, but about empowering it by providing the engine of "credit"; InfoFi is not about replicating Web2, but about liberating Web2 and reclaiming "sovereignty" for its people. We are moving from a world that prices only "capital" to a world that will ultimately price "reputation" and "attention" fairly. This is not just a financial revolution; it is a value reconstruction of digital civilization.