Original title: The Crypto Theses 2026

Original author: Messari

Compiled by: Peggy, BlockBeats

Editor's Note: Against the backdrop of a depressed market sentiment in 2025 but accelerated institutional entry, Messari's "The Theses 2026" report systematically outlines the main narratives and structural trends that it believes will continue to have a key impact in the coming years, focusing on seven core areas: Cryptomonney, TradeFi, Chains, DeFi, AI, DePIN, and consumer applications.

This article is excerpted from the core content on cryptocurrencies in "The Theses 2026," focusing on Messari's judgment logic and points of contention regarding the monetary attributes of assets such as BTC, ETH, and ZEC.

introduction

Welcome to "The Theses 2026"!

2025 may be the most divisive year in the history of the crypto industry. Your final assessment of this year will largely depend on where you are and who you are.

If you're flipping through this report from an office overlooking Wall Street, this might be the best year in crypto history you've ever experienced; but if you're at the other end of the spectrum, a trench warrior spending over 12 hours a day lurking in Telegram and Discord groups, you'll probably miss the old days. One thing is certain: 2025 has once again proven that the volatility of this industry is just as dramatic as the price charts we stare at every day.

Looking back on this year:

At the beginning of the year, we witnessed what, in hindsight, was one of the most exciting token launches in history: Trump. Although the excitement quickly subsided, this launch served as an important stress test, validating the extent to which on-chain infrastructure had developed.

The world's largest government has officially declared Bitcoin a unique store of value, including it in its official reserves and even leaving room for further purchases under the premise of "budget neutrality." Just two years ago, this was nothing short of a pipe dream.

The identity crisis that has plagued Ethereum for two years has finally reached its climax, but the result has been that Ethereum has become stronger. Today, Ethereum is consolidating its position as a core hub for institutional adoption.

DAT (Digital Asset Vault) became the buzzword of the year, with its collective buying pushing the entire asset class to record highs.

The first landmark U.S. crypto legislation, the GENIUS Act, has been officially signed, laying the foundation for a stablecoin market that the U.S. Treasury Secretary anticipates could expand to trillions of dollars in the future.

On October 10th, the largest crypto deleveraging event in history occurred, with many assets falling by more than 50% within minutes, and some even trading at zero (literally zero). Since then, crypto assets have significantly underperformed compared to asset classes with strong historical correlations, such as gold, silver, and stocks.

Tomorrow's enterprises are being born on the blockchain. Hyperliquid and Tether may already be among the most profitable companies in history, based on profit per employee. Applications like Polymarket and pump.fun have successfully "crossed the chasm" and entered mainstream culture.

Throughout all of this, Messari Research has been there to help you stay on top of industry trends. We released landmark research reports on two key annual trends—stablecoins and AI; our early 2024 prediction of Hyperliquid was validated, and we continued to track its rise throughout the year. As the industry began to rethink how crypto assets should be priced, we successively released valuation frameworks covering multiple sectors, including L1, public chains, DePIN, lending protocols, and more specialized asset types such as launch platforms and AI hedge funds.

From Trump's tariff policies and their spillover effects on the crypto market, to how tokenization is reshaping the collectibles industry and even bringing Pokémon cards to the blockchain, we maintain a consistently agile research pace. Messari's Protocol Services team has partnered with over 150 protocols to drive industry progress with objective insights.

This year's *The Theses* is divided into seven core sections, focusing on: Cryptocurrency, TradeFi, Chains, DeFi, AI, DePIN, and consumer applications. Within these sections, we will delve into the core narratives and themes we believe will continue to have a significant impact in the coming years.

Following our seven main sections, we've retained popular content such as Messari Analyst Picks and the Messari Awards. This year's addition is Alumni Theses, featuring in-depth articles from Messari alumni—those at the forefront of driving industry progress. Finally, we're giving a sneak peek at a brand-new analytical framework under development: the Disruption Factor.

Cryptomoney is the cornerstone of the industry: core themes

Authors: AJC, Drexel Bakker, Youssef Haidar

Bitcoin has completely distinguished itself from other crypto assets and is undoubtedly the most dominant form of cryptocurrency today.

BTC's relative underperformance in the second half of this year was partly due to selling pressure from early large holders. We do not believe this will develop into a long-term structural problem, and BTC's "monetary narrative" will remain solid for the foreseeable future.

L1 valuations are increasingly detached from their fundamentals. L1 revenue has declined significantly year-over-year, and its valuation is increasingly based on the assumption of a "currency premium." With a few exceptions, we expect most L1s to underperform BTC.

ETH remains the most controversial asset. Concerns about value capture haven't completely dissipated, but market performance in the second half of 2025 suggests the market is willing to view it as a cryptocurrency similar to BTC. If a bull market returns in 2026, Ethereum DAT could have a "second life."

ZEC is gradually being priced as a private cryptocurrency, rather than just a niche privacy coin. In an era of increased surveillance, institutional dominance, and financial repression, it may become an important complementary hedging asset to BTC.

More and more applications may choose to build their own monetary systems rather than relying on the native assets of the networks they run on. Applications with social attributes and strong network effects are most likely to be the first to take this path.

Introduction

We're opening this year's *The Theses* by focusing on the most fundamental and important element of the crypto revolution: currency. This is no coincidence.

When we started planning this year's Theses in the summer, we never anticipated that market sentiment would swing so dramatically to the negative.

In November 2025, the Crypto Fear & Greed Index briefly fell to 10, entering the "extreme fear" zone. Prior to this, the index had only touched or fallen below 10 a few times in history, occurring in the following instances:

During the Luna crash and the 3AC chain reaction in May–June 2022

The massive, forceful waterfall in May 2021

The market crash caused by the COVID-19 pandemic in March 2020

Several phases in the 2018–2019 bear market

Throughout the history of the crypto industry, there have been very few instances of such low market sentiment, and almost all of them occurred when the industry was truly on the verge of collapse and its future prospects were seriously questioned. But clearly, this is not the case today.

No major exchanges absconded with user funds; no obvious Ponzi schemes were hyped up to valuations of hundreds of billions of dollars; and the overall market capitalization did not fall below the high point of the previous cycle.

Conversely, crypto assets are being recognized and gradually incorporated into the highest levels of global institutional systems. The U.S. SEC has publicly stated that it expects all U.S. financial markets to be on-chain within two years; stablecoin supply has reached an all-time high; and the adoption narratives we've repeatedly mentioned over the past decade—"it will come someday"—are truly becoming a reality.

However, despite this, the mood in the crypto industry has almost never been worse. Almost every week or two, a post goes viral on X: some people are convinced they've wasted their lives in the crypto industry; others assert that everything the industry has built will eventually be copied, appropriated, and captured by existing institutions.

It is precisely in this stark contrast between the continued collapse of sentiment and the rising institutional adoption that the crypto industry has become the perfect time to re-examine its first principles. And that original core principle that gave birth to this chaotic yet fascinating industry is actually extremely simple: to build a monetary system that is superior to and a more viable alternative to the existing fiat currency system.

Since the birth of the Bitcoin Genesis Block, this ideal has been deeply embedded in the industry's DNA. That block deliberately inscribed a line that later became widely known: "The Times 03/Jan/2009 Chancellor on brink of second bailout for banks."

These starting points are important because, at some point, many people have forgotten what problem cryptocurrencies were originally created to solve.

The purpose of Bitcoin is not to provide banks with a more efficient clearing channel; not to save a few basis points in foreign exchange transfers; and certainly not to drive a "slot machine" that never stops issuing speculative tokens.

Its creation was essentially a response to a failing monetary system.

Therefore, if we want to truly understand where the crypto industry is today, we must go back to the core question of the entire industry: Why is crypto important?

Why Cryptomonney?

For much of modern history, people had virtually no real choice about what currency to use. In today's fiat-based global monetary system, individuals are effectively tied to their national currency and the decisions of its central bank.

The government decides which currency you use to earn money, save money, and pay taxes. Whether that currency is inflated, devalued, or systematically mismanaged, you can only passively bear the consequences.

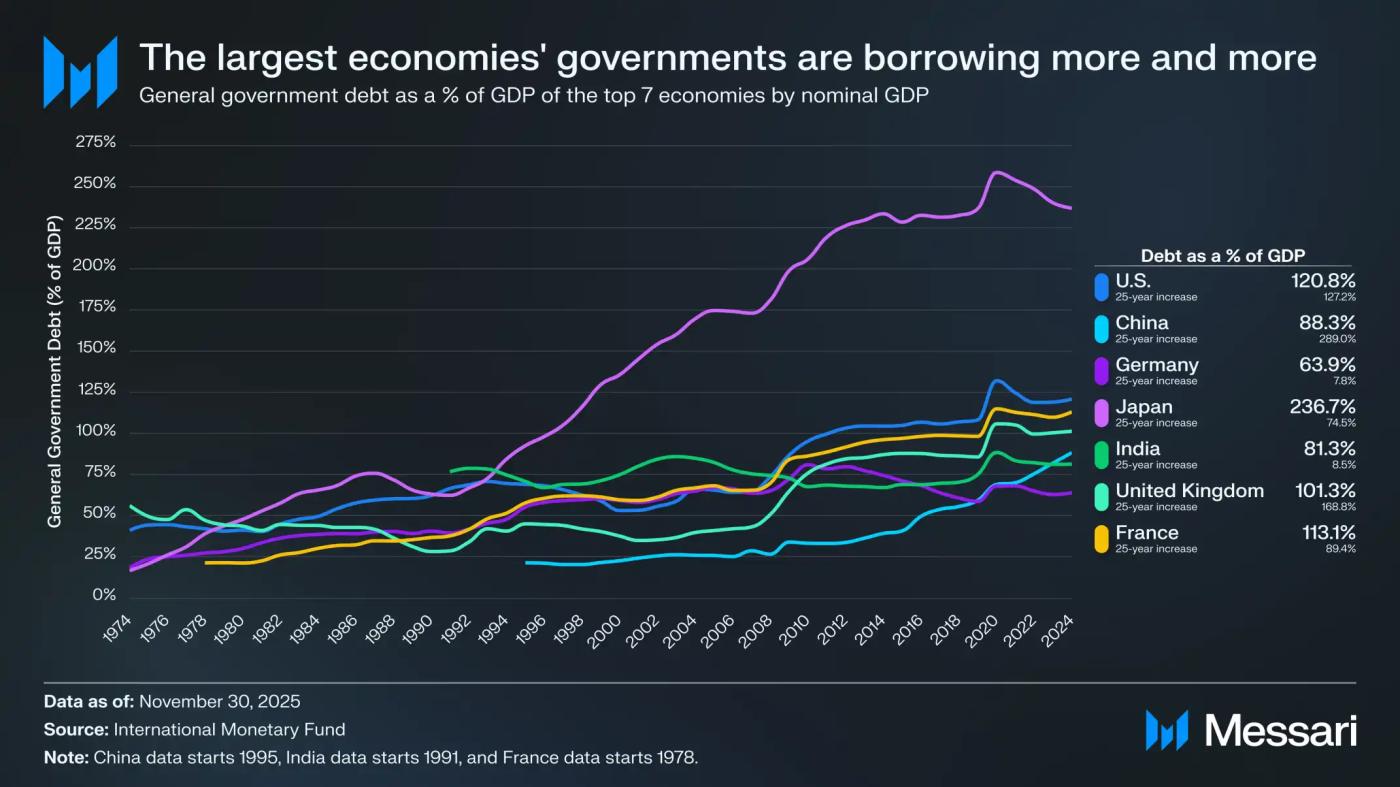

Moreover, this situation does not differ based on political or economic systems—whether it is a free market, an authoritarian regime, or a developing economy, almost all exhibit the same pattern: government debt is a one-way street.

Over the past quarter-century, government debt as a percentage of GDP has generally increased significantly in major global economies. As the world's two largest economies, the United States and China have seen their general government debt-to-GDP ratios increase by 127% and 289%, respectively. Regardless of political systems or changes in growth models, the continued expansion of government debt has become a structural feature of the global financial system.

When debt grows faster than economic output for an extended period, the costs often fall most directly on savers. Inflation and low real interest rates continuously erode the purchasing power of fiat currency savings, effectively completing a transfer of wealth from individual savers to the nation.

Cryptomoney offers an alternative to this system by separating the state from the currency. Historically, governments have tended to adjust monetary rules when inflation, capital controls, or stricter regulations are in their own interest. Cryptomoney, however, returns monetary governance to a decentralized network, rather than concentrating it in a single authority.

In this process, the "currency option" re-emerges: savers can choose a monetary asset that better aligns with their values, needs, and preferences, rather than being forced into a system that frequently undermines their long-term financial health.

Of course, the choice itself only makes sense when "the chosen object truly possesses an advantage." This is precisely the case with Cryptomoney, whose value is based on a series of attributes that have never existed simultaneously before.

The first cornerstone of cryptomoney's value is its predictable, rules-based monetary policy. These rules do not come from the commitment of any single institution, but are inherent properties of software run by thousands of independent participants. Any rule change requires broad consensus, not the discretion of a few, making arbitrary and sudden monetary policy adjustments extremely difficult.

In stark contrast to the fiat currency system, where the money supply often expands passively under political or economic pressure, cryptocurrencies operate under public and predictable rules, enforced through consensus mechanisms, and cannot be quietly modified "in a secret room."

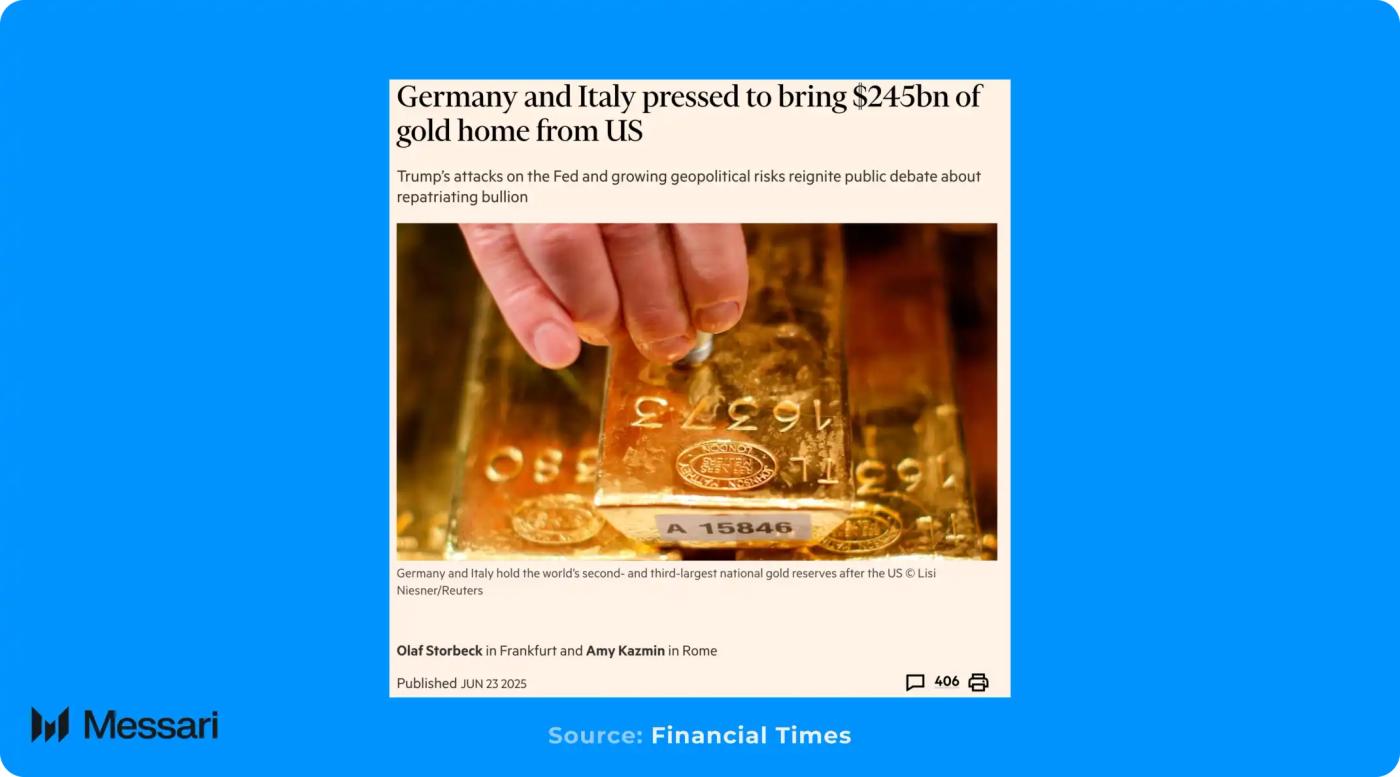

Cryptomoney has also fundamentally changed how individuals safeguard their wealth. In the fiat currency system, true self-custody has long been impractical, forcing most people to rely on banks or other financial intermediaries to store their savings. Even traditional non-sovereign assets like gold are often ultimately stored in custodial vaults, reintroducing the same trust-based risks.

In reality, this means that once the custodian or the country makes a decision, your assets may be delayed, restricted, or even completely denied access.

Cryptomoney enables direct ownership, allowing individuals to hold and protect their assets independently without relying on any custodian. This capability is becoming increasingly important as various financial restrictions, from bank withdrawal limits to capital controls, become more prevalent globally.

Finally, cryptocurrencies are designed for a globalized, digital world. They allow for instant cross-border transfers of any amount without the need for any institutional permission. This gives them a significant advantage over gold—gold is difficult to divide, verify, and transport, especially in cross-border scenarios.

In contrast, cryptocurrencies can be transferred globally in minutes, are unlimited in scale, and do not rely on centralized intermediaries. This ensures that individuals, regardless of their location or the political environment, can freely allocate and use their wealth.

Overall, the value logic of cryptocurrencies is quite clear: they provide individuals with monetary choice, establish predictable operating rules, eliminate the risk of single points of failure, and allow value to flow freely globally without restrictions. In a system where government debt continues to rise and savers bear the costs, the value of cryptocurrencies will only continue to increase.

Bitcoin: The Most Dominant Cryptomonney

Bitcoin created the category of cryptocurrencies, so it's natural to start with it. Nearly seventeen years later, BTC remains the largest and most recognized asset in the entire industry.

Since the essence of currency ultimately depends on social consensus rather than technological design itself, the key to determining whether an asset has "monetary status" lies in whether the market is willing to continuously assign it a long-term premium.

By this standard, BTC's position as the leading cryptocurrency is quite clear.

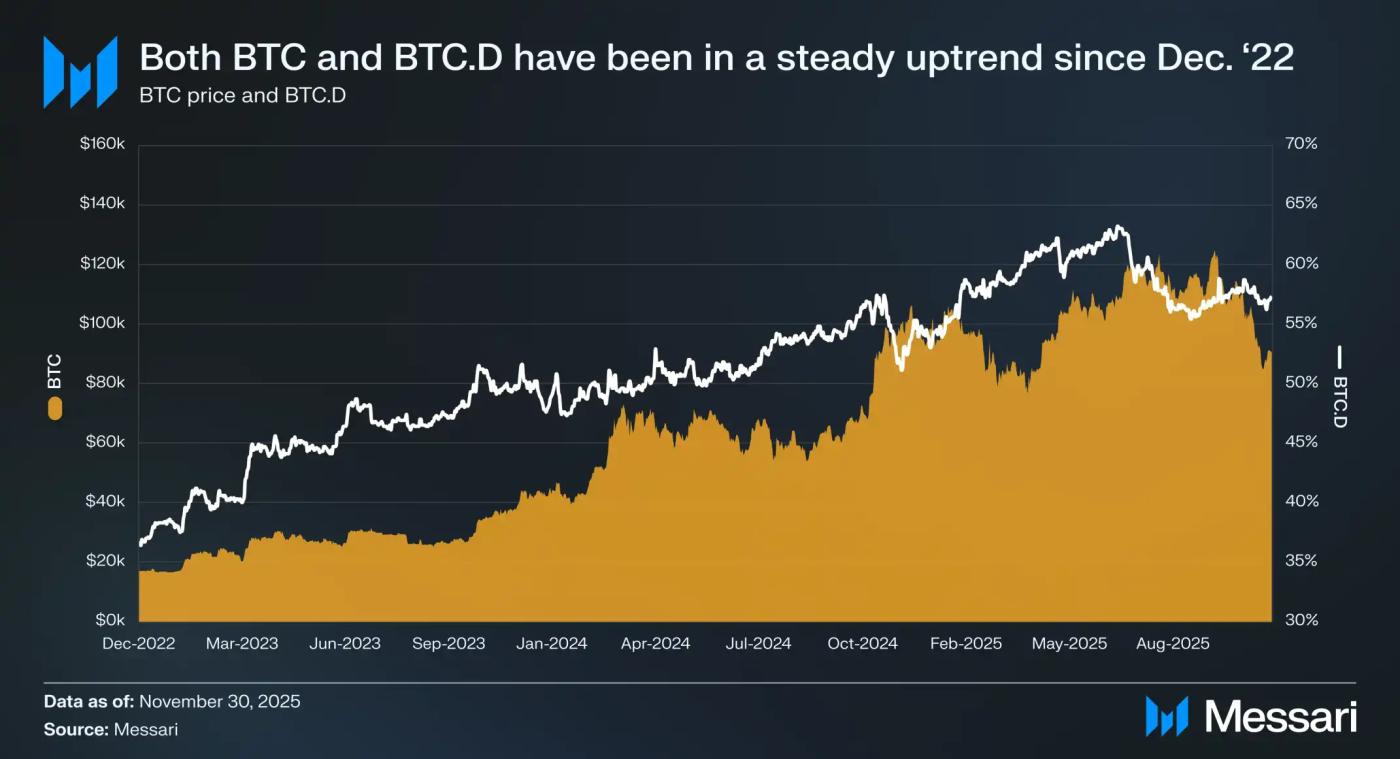

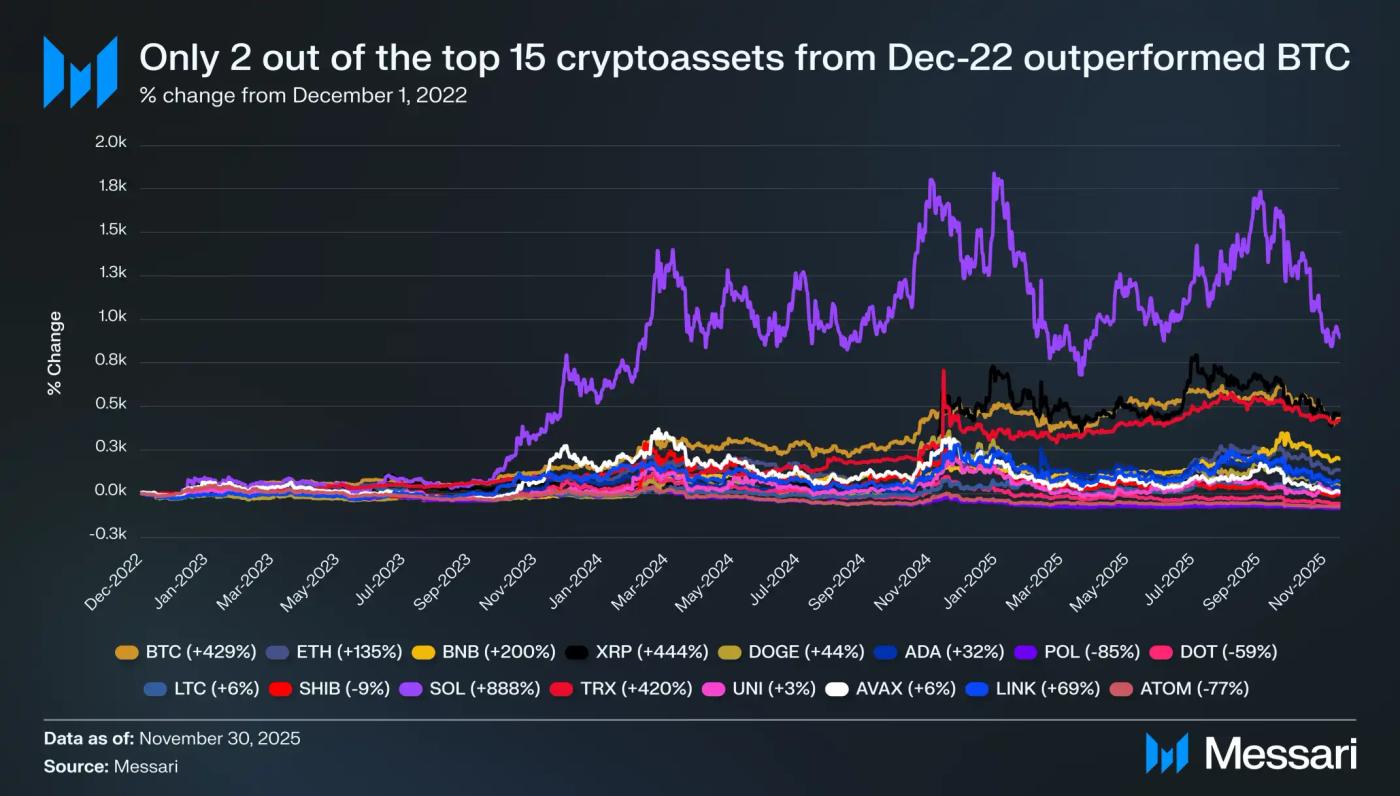

This is most clearly demonstrated in BTC's market performance over the past three years. Since December 1, 2022, BTC has risen by 429%, climbing from $17,200 to $90,400. During this process, Bitcoin has repeatedly broken its all-time high, most recently reaching $126,200 on October 6, 2025.

At the beginning of this market rally, BTC's market capitalization of approximately $318 billion was insufficient to rank it among the world's largest assets; however, it has now increased to $1.81 trillion, ranking as the ninth largest asset globally. The market has not only rewarded BTC's monetary attributes with higher prices but has also propelled it into the top tier of the global asset system.

But what is more indicative is the change in BTC's performance relative to the entire crypto market. Historically, during crypto bull markets, Bitcoin's market dominance (BTC.D) typically declines as funds migrate along the risk curve to higher-risk assets; however, in this BTC-centric bull market, this pattern has been completely reversed.

Over the same three-year period, BTC.D rose from 36.6% to 57.3% (including stablecoins). This indicates that BTC is showing a clear divergence from the broader crypto market.

Of the top 15 crypto assets by market capitalization on December 1, 2022, only two assets (XRP and SOL) outperformed BTC during this period, and only SOL achieved significant excess returns (up 888%, compared to 429% for BTC).

Most other market assets lagged significantly, with many large-cap tokens barely generating positive returns or even remaining in negative territory during the same period.

Among them, ETH rose by only 135%, BNB by 200%, and DOGE by 44%; while assets such as POL (-85%), DOT (-59%), and ATOM (-77%) are still experiencing deep pullbacks.

This phenomenon is particularly noteworthy because of BTC's sheer size. As an asset with a market capitalization exceeding one trillion dollars, its price fluctuations should theoretically require the most capital, yet it has still outperformed almost all mainstream tokens. This indicates that there is genuine and sustained buying demand for BTC in the market; while most other assets are more like "beta," passively following the trend only when BTC drives the entire market upward.

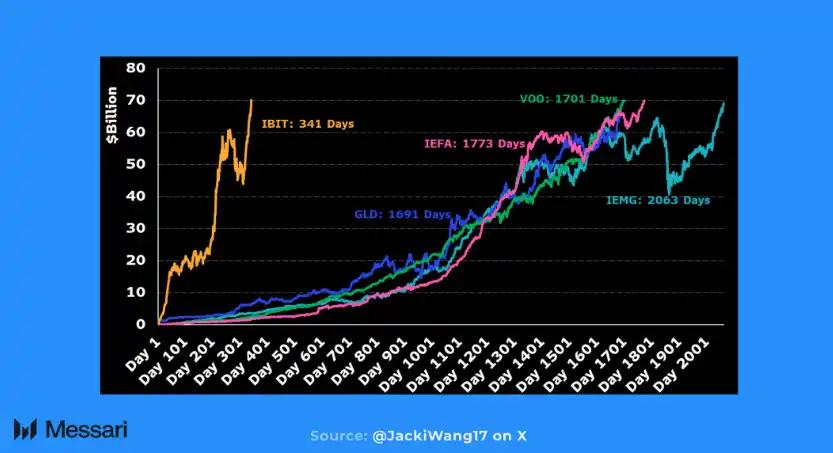

A key driver of the continued buying of BTC is the accelerated adoption by institutional investors. The most representative form of this round of institutional entry is the spot Bitcoin ETF.

The market demand for these products is so strong that it has almost reached the point of supply falling short of demand. BlackRock's iShares Bitcoin Trust (IBIT) has broken ETF historical records multiple times and has been hailed as "the most successful ETF issuance in history".

Just 341 days after its IPO, IBIT's assets under management (AUM) reached $70 billion, a milestone achievement, 1,350 days faster than the previous record set by SPDR Gold Shares (GLD).

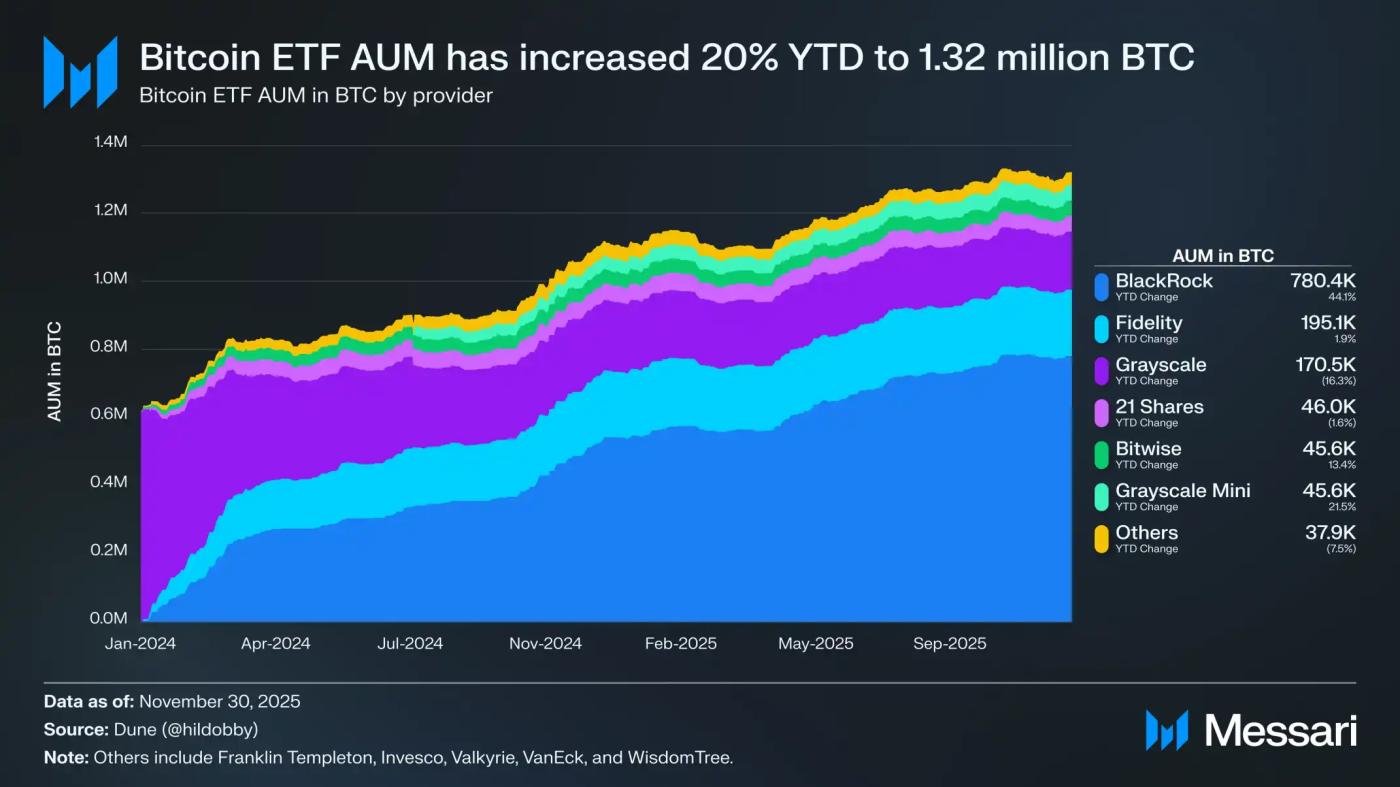

The momentum generated by the ETF launches in 2024 has almost seamlessly continued into 2025. As of now, the total assets under management (AUM) of Bitcoin ETFs have grown by approximately 20% year-to-date, with holdings increasing from approximately 1.1 million BTC to 1.32 million BTC. At current prices, this equates to over $120 billion worth of Bitcoin being held by these products, representing more than 6% of the maximum BTC supply.

Unlike the initial hype that gradually faded after their initial release, the demand for ETFs has evolved into a continuous source of buying interest, with these products steadily accumulating BTC regardless of market conditions.

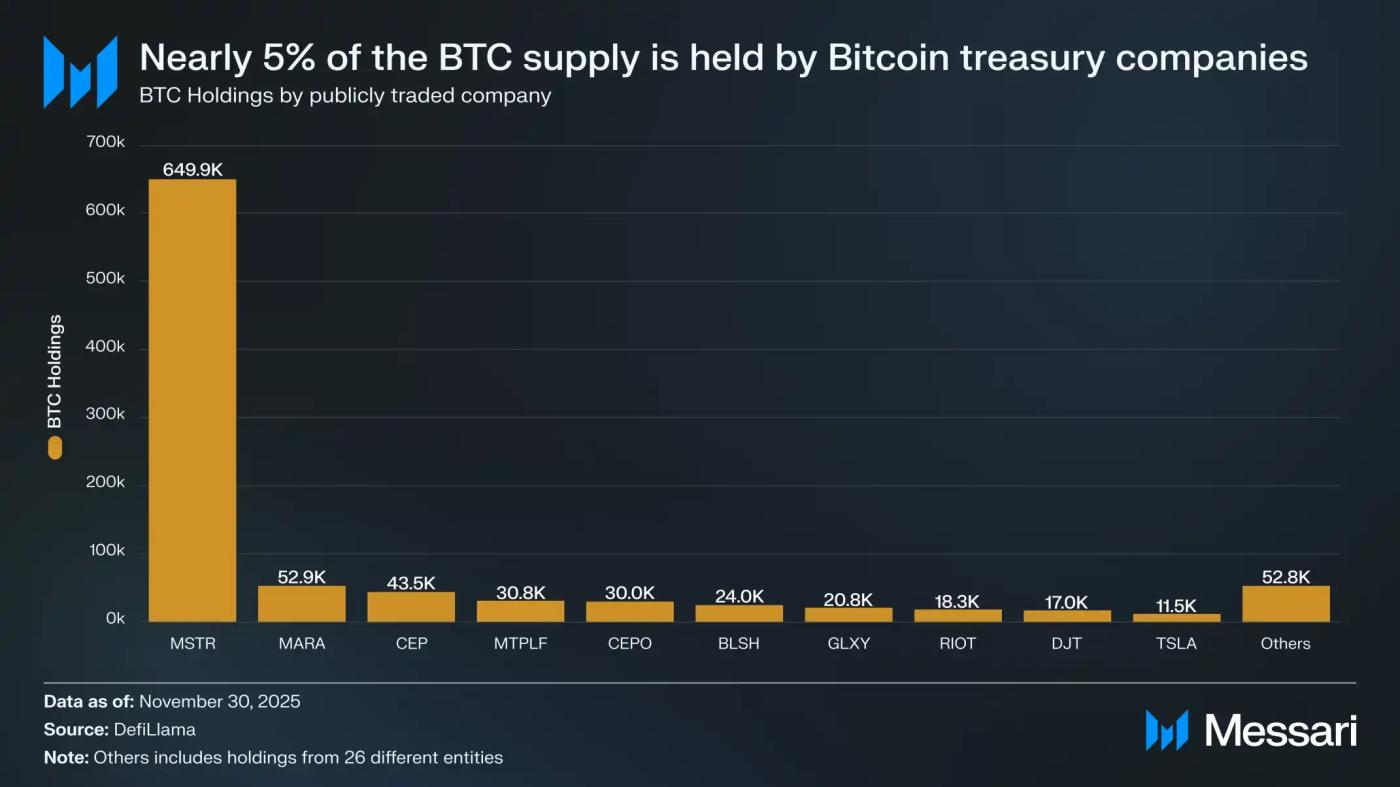

Furthermore, institutional participation is no longer limited to ETFs. Digital asset vaults (DATs) became significant buyers in 2025, further reinforcing BTC's role as an enterprise-grade reserve asset. While Strategy, led by Michael Saylor, has long been the most representative case of corporate Bitcoin hoarding, nearly 200 companies globally now hold BTC on their balance sheets.

As for publicly listed companies alone, they collectively hold approximately 1.06 million BTC, accounting for about 5% of the total Bitcoin supply; among them, Strategy holds 650,000 BTC, far ahead of all companies, occupying the largest share.

Perhaps the most crucial and clearest event in 2025 to distinguish BTC from other crypto assets was the formal establishment of the Strategic Bitcoin Reserve (SBR). The SBR institutionally confirmed the long-standing market consensus: BTC is not categorized in the same way as other crypto assets. Within this framework, BTC is treated as a strategic monetary commodity, while other digital assets are uniformly incorporated into a separate asset pool and managed in a conventional manner.

In its official announcement, the White House described BTC as a "unique store of value in the global financial system" and likened it to "digital gold." More importantly, the executive order also requires the Treasury Department to develop a potential strategy for future BTC acquisitions. Although no actual purchases have yet occurred, the mere existence of this "policy option" sends a clear signal: federal policymaking has begun to examine BTC from a forward-looking, reserve asset perspective.

If the acquisition plans are implemented in the future, Bitcoin's monetary status will not only be consolidated within the crypto asset class, but will also be further established across all asset classes.

Is BTC a "good currency"?

Despite Bitcoin's established dominance among various cryptocurrencies, 2025 has also sparked a new round of discussions about its monetary attributes. As the largest non-sovereign monetary asset currently in existence, gold remains the most important benchmark for evaluating Bitcoin.

Gold recorded one of its strongest annual performances in decades amid escalating geopolitical tensions and growing market expectations for future monetary easing. In contrast, Bitcoin failed to follow suit.

Although the BTC/XAU ratio hit an all-time high in December 2024, it has since retreated by about 50%. This retreat is particularly noteworthy because it occurred against the backdrop of gold prices continuously hitting new all-time highs in dollar terms. Year-to-date, gold prices have risen by more than 60%, reaching $4,150 per troy ounce.

With the total market capitalization of gold approaching $30 trillion, while BTC still only accounts for a small fraction of it, this divergence in price movements naturally raises a reasonable question:

If BTC fails to rise in tandem with gold during one of its strongest periods, how secure is its status as "digital gold"?

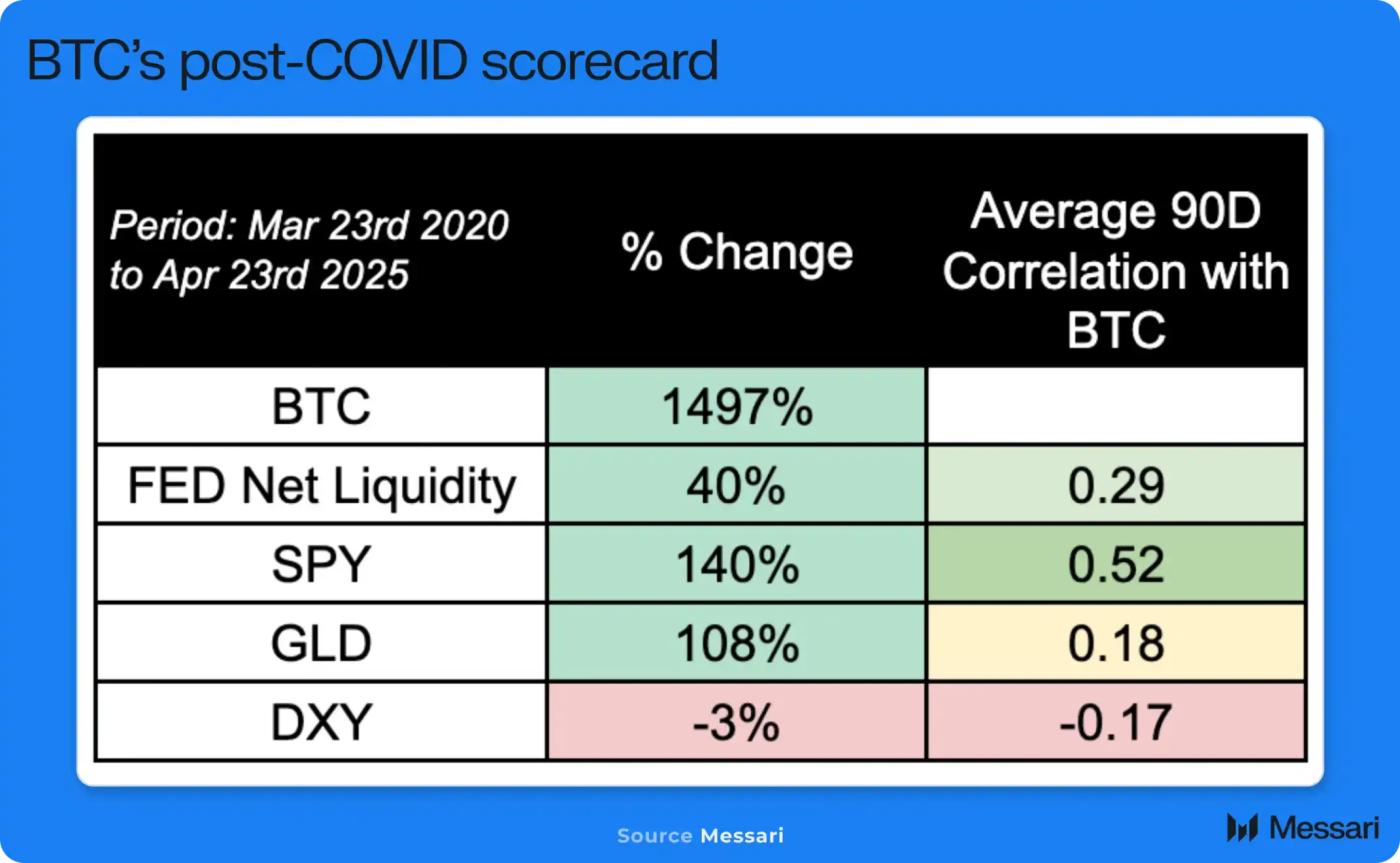

If Bitcoin's price action doesn't mirror that of gold, then the next benchmark to observe is its performance relative to traditional risk assets. Historically, BTC has shown some correlation with stock indices at several points, including the SPY and QQQ.

For example, during the period from April 2020 to April 2025, the average 90-day rolling correlation coefficient between BTC and SPY was approximately 0.52, while the correlation with gold was relatively weak, at only 0.18. Based on this historical characteristic, if the stock market as a whole weakens, then BTC's lagging performance relative to gold might be logically understandable.

But this is not the case. Year-to-date, gold (XAU) has risen by about 60%, SPY by 17.6%, and QQQ by 21.6%, while BTC has fallen by 2.9%. Considering that BTC's market capitalization is much smaller than that of gold and major stock indices, and its volatility is much higher, its significant underperformance relative to these benchmark assets in 2025 has inevitably raised legitimate questions about its monetary narrative.

With gold and stocks hitting record highs, one might expect BTC to follow a similar trajectory based on its historical correlation with other cryptocurrencies. However, this has not been the case. Why?

First, it's important to point out that this underperformance is not a long-term phenomenon that persists throughout the year, but rather a relatively recent change. As recently as August 14, 2025, BTC still outperformed XAU, SPY, and QQQ in terms of absolute year-to-date returns. Its relative weakness only began to emerge in October. What's truly noteworthy is not the duration of this underperformance, but the magnitude of the decline.

While multiple factors may have contributed to this outcome, we believe the most critical driver lies in the changing behavior of early, large-scale holders. As BTC has become increasingly institutionalized over the past two years, its liquidity structure has undergone a substantial transformation. The deep, regulated markets established through channels such as ETFs now allow large holders to sell without causing significant market shocks—something virtually impossible in previous cycles.

For many of these holders, this marks the first real window of opportunity for them to realize their gains in an orderly and low-impact manner.

Whether from numerous market anecdotes or on-chain data, there are ample indications that some long-dormant token holders are taking advantage of this window of opportunity to reduce their exposure.

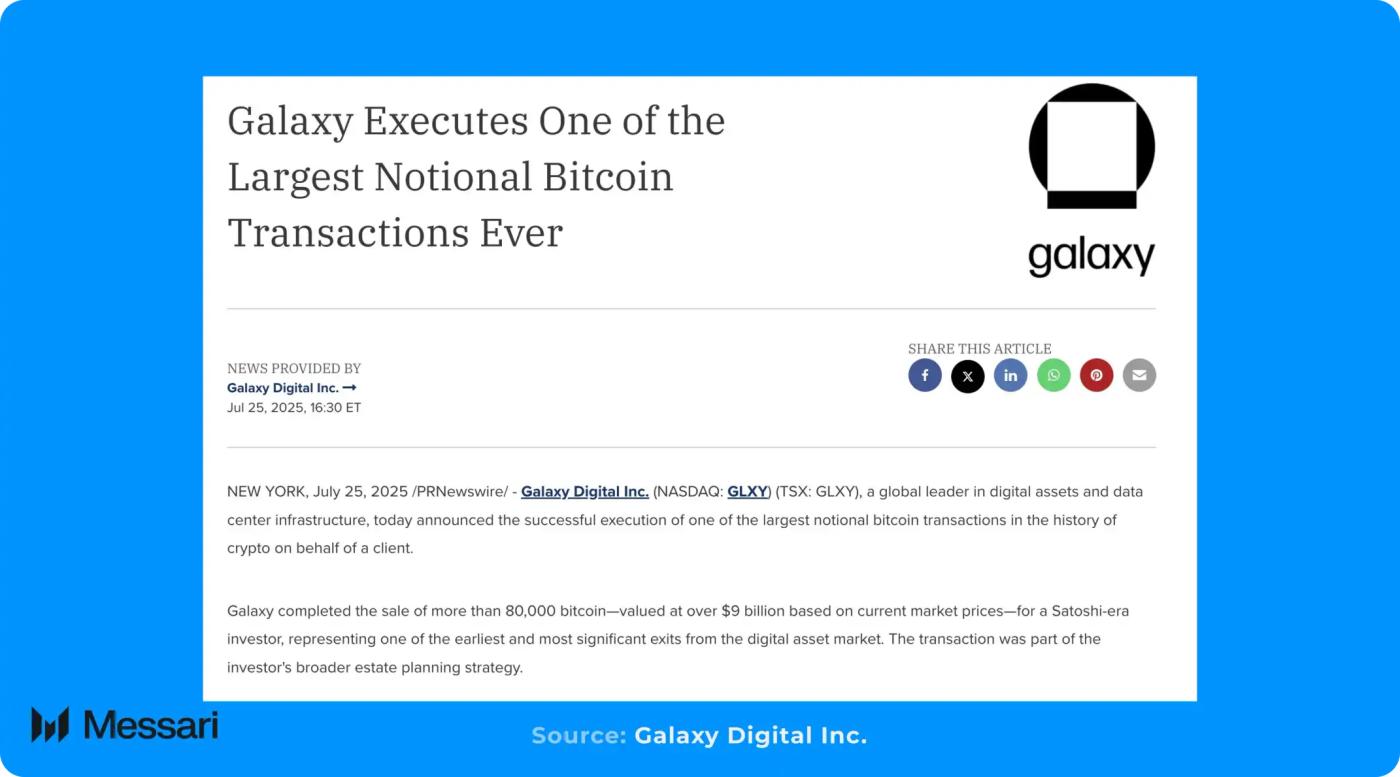

Earlier this year, Galaxy Digital assisted an investor from the "Satoshi era" in selling 80,000 BTC. This transaction represented approximately 0.38% of the total Bitcoin supply and originated entirely from a single entity.

Such a size is enough to exert significant pressure on prices in any market environment.

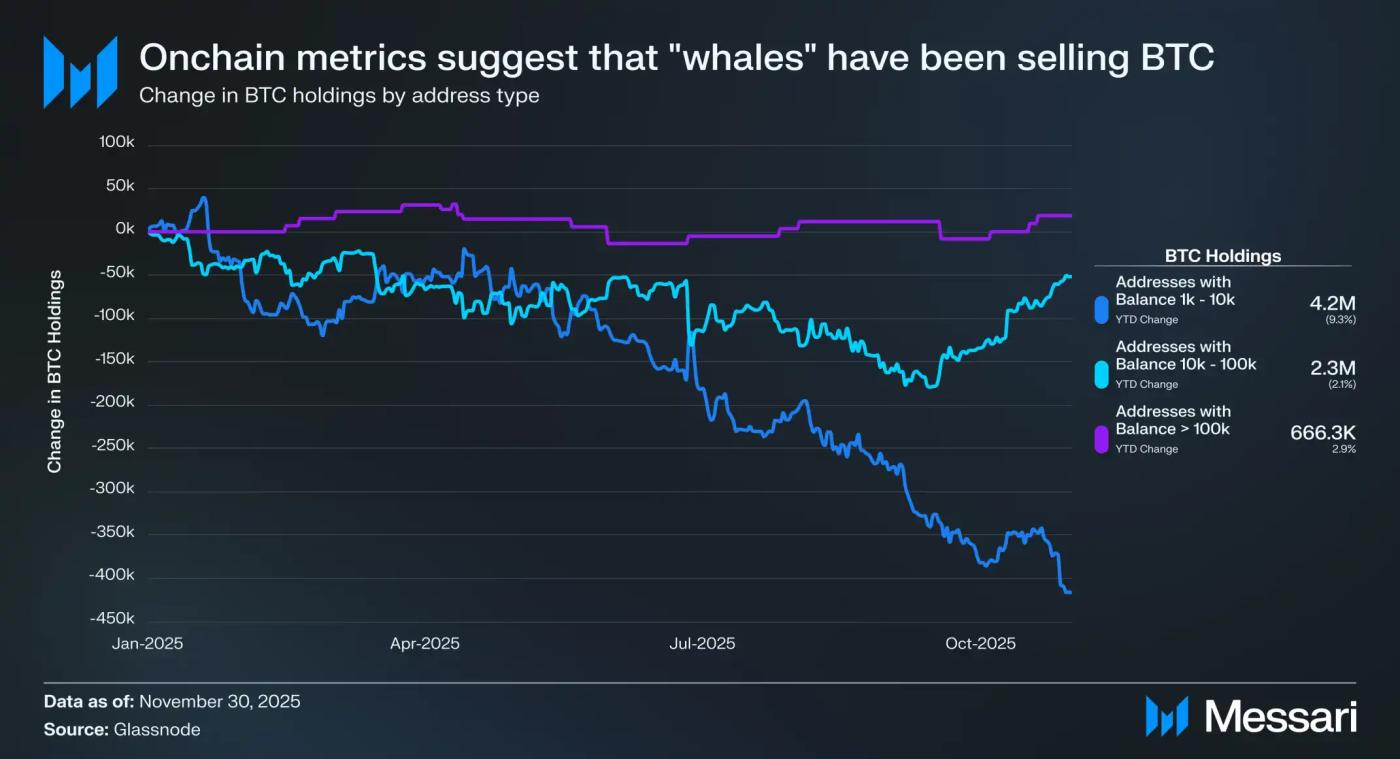

Bitcoin's on-chain metrics also show a similar trend. Since 2025, some of the largest and longest-held addresses—those holding between 1,000 and 100,000 BTC—have consistently been net sellers. These addresses held a total of approximately 6.9 million BTC at the beginning of the year, nearly one-third of the total circulating supply of Bitcoin, and continued to release tokens into the market throughout the year.

Specifically, addresses in the 1,000–10,000 BTC range have seen a net outflow of 417,300 BTC year-to-date (-9% YTD); while addresses in the 10,000–100,000 BTC range have also seen an additional net outflow of 51,700 BTC (-2% YTD).

As Bitcoin becomes increasingly institutionalized and more transactions and fund flows shift to off-chain channels, the information value carried by on-chain data itself will inevitably decline gradually. Even so, combining this on-chain data with market examples such as "investors selling BTC in the Satoshi era" still provides ample reason to conclude that in 2025, especially in the second half of the year, early large holders of Bitcoin will generally be in a net selling state.

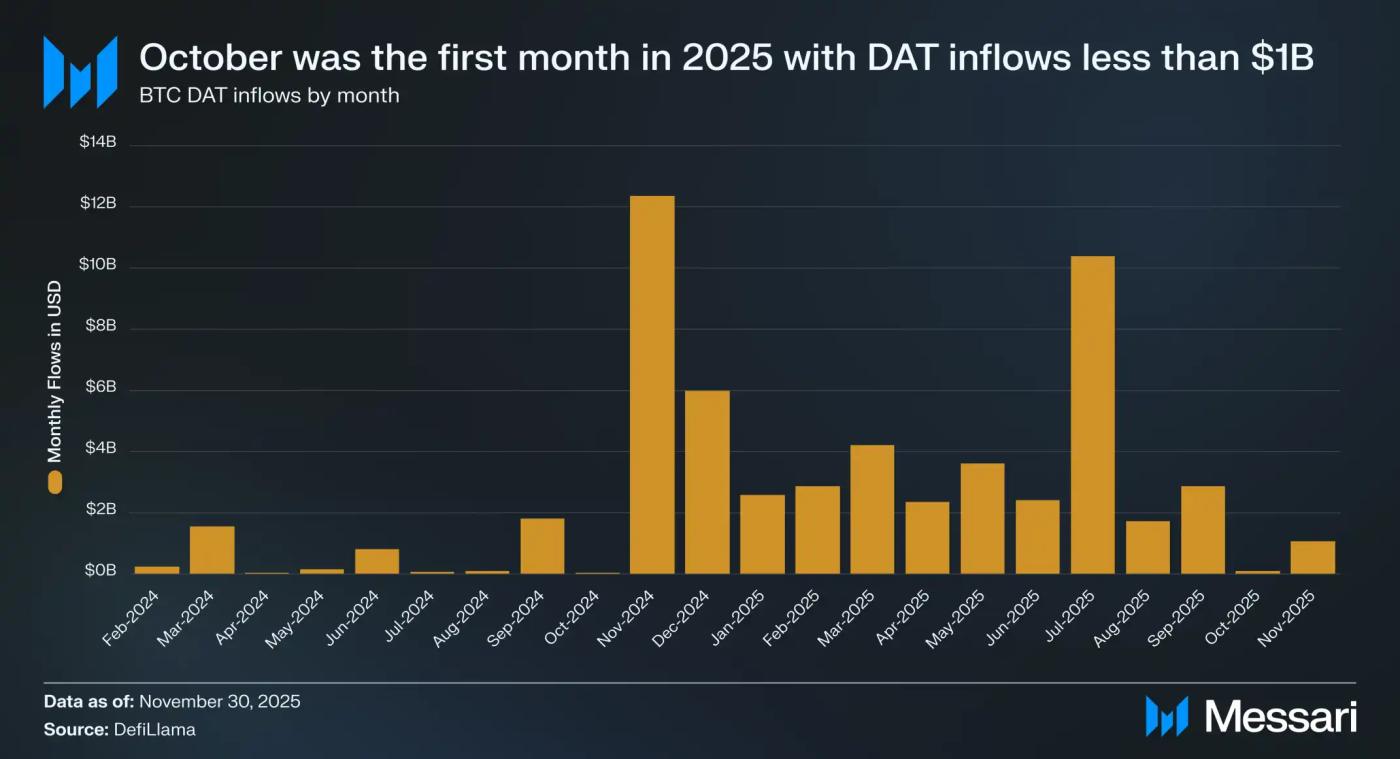

This round of supply release coincided with a significant slowdown in the core buying power that had driven BTC price increases over the past two years. Inflows into DAT fell sharply in October, marking the first time since 2025 that monthly net inflows into DAT did not exceed $1 billion. Meanwhile, spot Bitcoin ETFs—which had been net buyers throughout the year—turned into net sellers starting in October.

When both DAT and ETF, two stable sources of demand, show signs of weakness in the short term, the market is forced to absorb concentrated selling pressure from early large holders as buying activity decreases. The combined effect of these two forces naturally puts significant pressure on prices.

So, is this something to worry about? Has BTC's "monetary" nature been disproven by its recent underperformance?

In our view, the answer is no. As the old saying goes, "When in doubt, look at the bigger picture." A weak performance of only about three months is hardly enough to negate the long-term logic of BTC. Historically, BTC has experienced longer periods of relative underperformance, but ultimately not only rebounded but also reached new highs against the US dollar and gold. While the current underperformance is certainly a temporary setback, we do not consider it a structural problem.

Looking ahead to 2026, the situation becomes even more complex. As BTC is increasingly viewed as a macro asset, the importance of traditional analytical frameworks (such as the "four-year cycle") is declining. BTC's performance will be shaped more by macroeconomic variables, so the truly critical question becomes:

Will central banks around the world continue to increase their gold holdings?

Will AI-driven stock trading continue to accelerate?

Will Trump fire Powell?

If this happens, will Trump push the new Federal Reserve chairman to start buying BTC?

These variables are extremely difficult to predict, and we do not claim to be able to provide a definitive answer.

But what we are confident about is BTC's long-term monetary trajectory. On timescales spanning years and even decades, we expect BTC to continue appreciating in its monetary sense—whether relative to the US dollar or gold. Ultimately, this judgment can be simplified to one question: "Is cryptocurrency a superior form of currency?"

If the answer is yes, then the long-term direction of BTC is self-evident.

Beyond BTC: How should we view L1?

BTC has clearly established itself as the leading cryptocurrency, but it is not the only crypto asset with a currency premium. The valuations of some Layer 1 (L1) tokens also reflect a certain degree of currency premium, or at least include the expectation of a future currency premium.

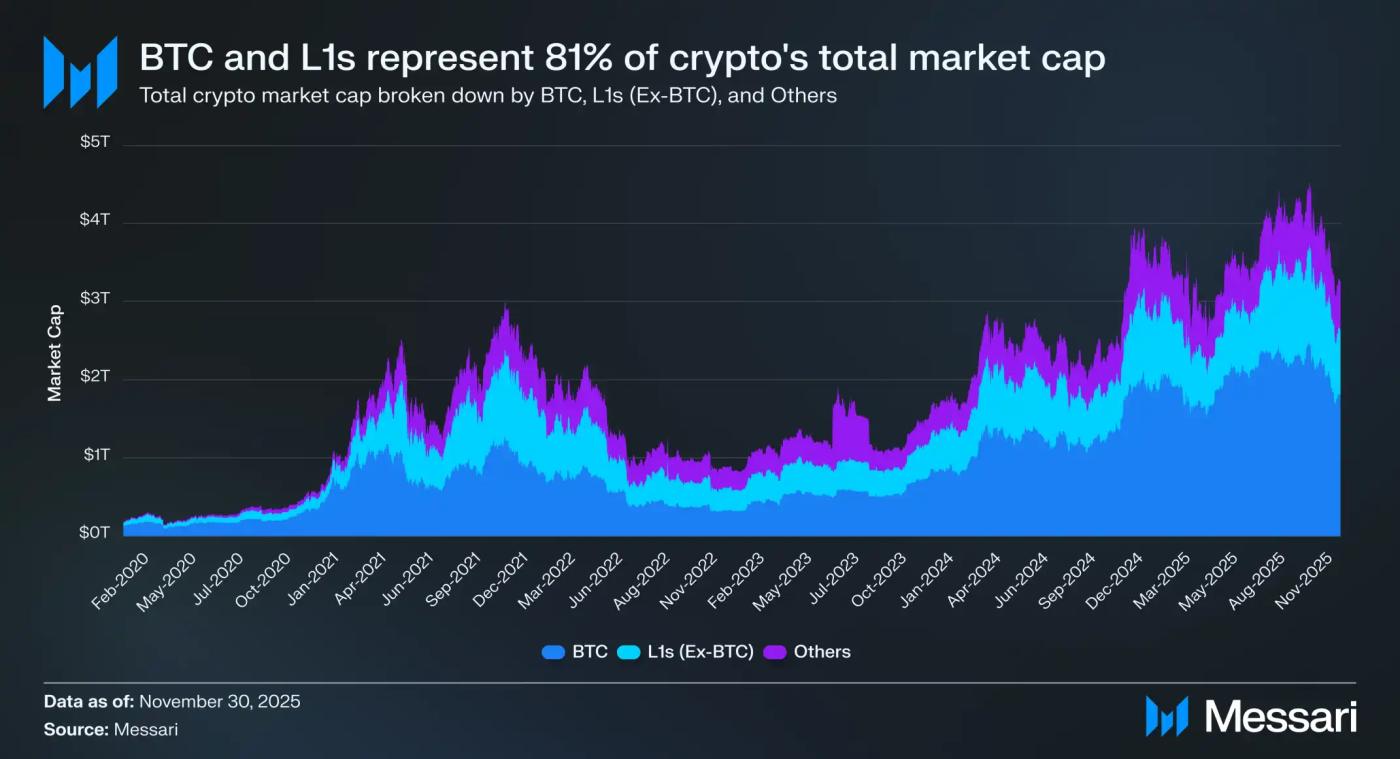

Currently, the total market capitalization of the crypto market is approximately $3.26 trillion. Of this, Bitcoin accounts for about $1.80 trillion; of the remaining $1.45 trillion, about $0.83 trillion is concentrated in various alternative Level 1 cryptocurrencies. Overall, approximately $2.63 trillion, or about 81%, of the crypto market's funds are allocated to assets that the market already considers to be currencies, or believes they may receive a currency premium in the future.

Therefore, whether you are a trader, investor, fund allocator, or portfolio builder, understanding how the market assigns or takes back currency premiums is crucial. In the crypto industry, nothing influences an asset's valuation level more than whether the market is willing to treat it as "currency." Consequently, predicting where future currency premiums will flow is arguably the single most important variable in portfolio construction within this industry.

As mentioned earlier, we expect BTC to continue gaining market share from gold and other non-sovereign value stores in the coming years. But the question then arises: where will L1 stand?

Will the rising tide lift all ships? Or, as BTC "fills the gap" with gold, will some of the currency premium be drawn from other L1 contracts?

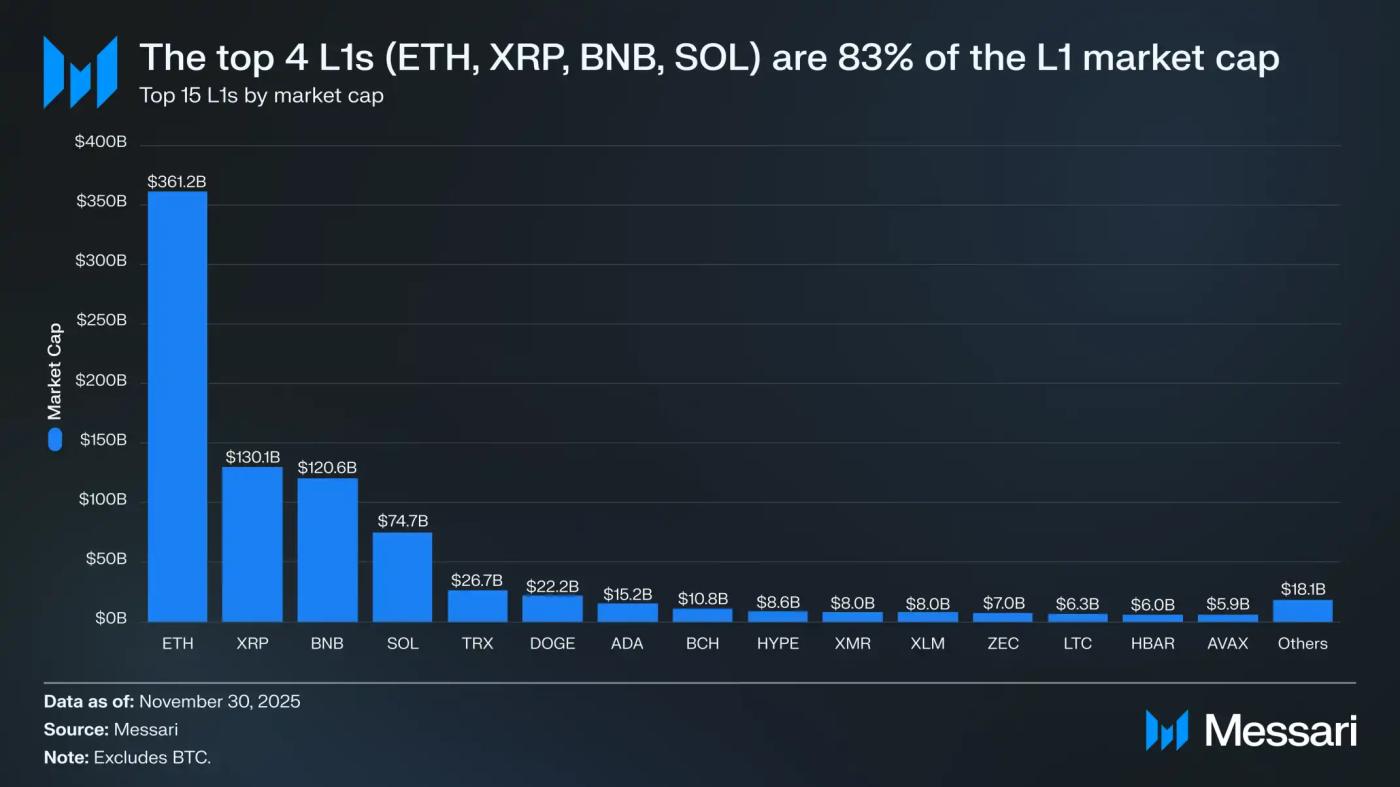

First, it's essential to understand the current valuation position of L1 cryptocurrencies. Currently, the top four L1 cryptocurrencies by market capitalization are ETH ($361.15 billion), XRP ($130.11 billion), BNB ($120.64 billion), and SOL ($74.68 billion), with a combined market capitalization of $686.58 billion, representing approximately 83% of the entire alternative L1 market.

After the top four, there is a significant gap in valuation (for example, TRX's market capitalization is approximately $26.67 billion), but the overall size is still considerable. Even L1—AVAX, ranked fifteenth in market capitalization, still has a valuation exceeding $5 billion.

It is important to emphasize that the market capitalization of L1 loans is not equivalent to their implied currency premium. The current mainstream valuation logic for L1 loans can be summarized into three main categories:

(i) Monetary Premium

(ii) Real Economic Value (REV) and (iii) Demand for Economic Security.

Therefore, the market value of a project does not simply stem from the market's perception of it as "currency," but is the result of multiple overlapping value logics.

Despite the existence of multiple competing valuation frameworks, the market is increasingly pricing L1 from a "currency premium" rather than a "revenue-driven" perspective. Over the past few years, the overall price-to-sales ratio (P/S) of all L1 companies with a market capitalization exceeding $1 billion has slowly risen from approximately 200x to 400x. However, this apparent figure is somewhat misleading because it includes TRON and Hyperliquid.

Over the past 30 days, TRX and HYPE contributed 51% of the revenue in this sample, but their combined market capitalization accounted for only 4%. These two significantly dragged down the overall P/S ratio.

Once these two outliers are removed, the truth becomes very clear: while revenue continues to decline, L1 valuations are constantly rising. The adjusted P/S ratio shows a continuous upward trend.

November 30, 2021: 40 times

November 30, 2022: 212 times

November 30, 2023: 137 times

November 30, 2024: 205 times

November 30, 2025: 536 times

From a REV (Real Economic Value) perspective, one explanation might be that the market is pricing in future revenue growth expectations. However, this explanation fails under basic tests. Using the same L1 group as a sample (excluding TRON and Hyperliquid), its revenue declined almost every year, with only one exception:

2021: US$12.33 billion

2022: $4.89 billion (down 60% year-on-year)

2023: $2.72 billion (down 44% year-on-year)

2024: US$3.55 billion (31% year-on-year growth)

2025: US$1.7 billion (annualized, down 52% year-over-year)

In our view, the simplest and most direct explanation is that these valuations are primarily driven by currency premiums, rather than current or foreseeable income levels.

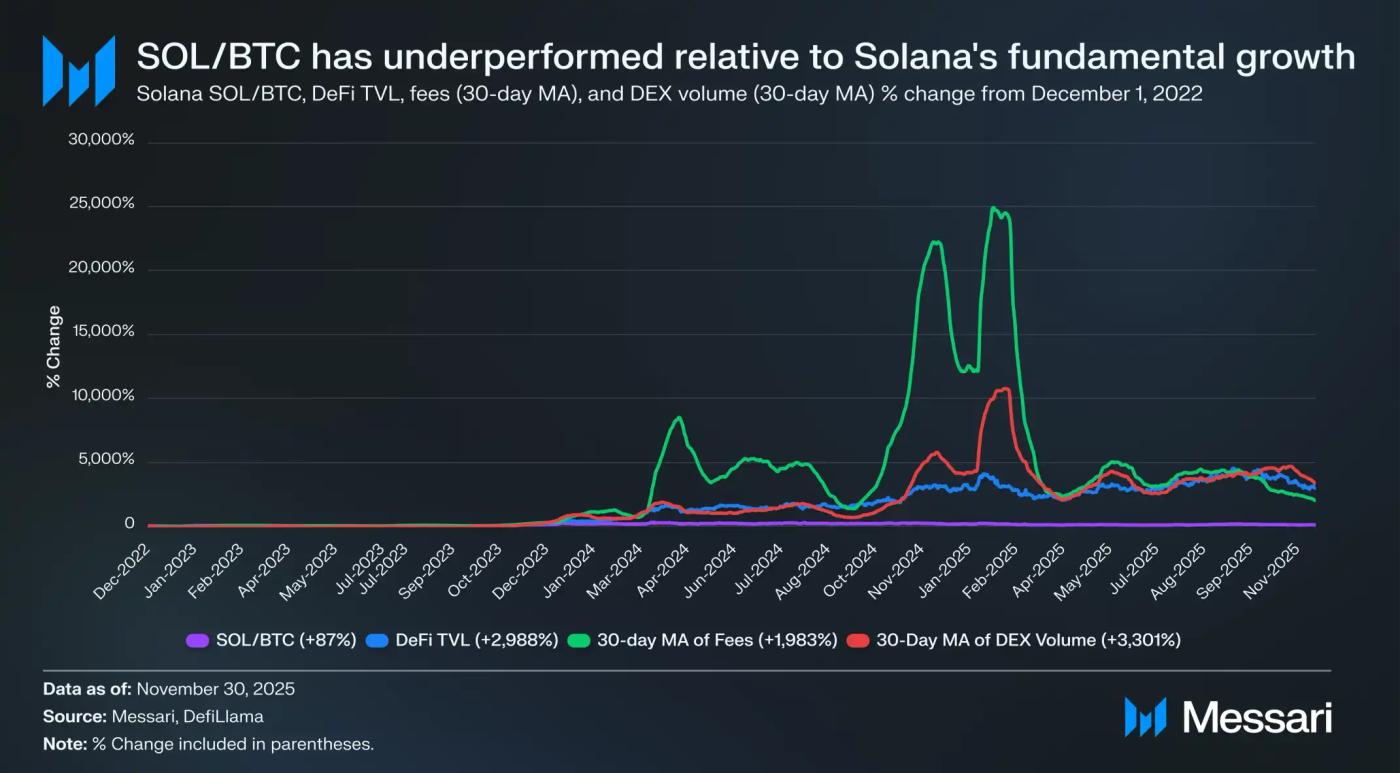

Further examination of SOL's outperformance reveals that its price increase may even lag behind the growth rate of its ecosystem fundamentals. During the same period that SOL outperformed BTC by 87%, Solana's fundamentals experienced explosive growth: DeFi's TVL increased by 2,988%, transaction fees increased by 1,983%, and DEX trading volume increased by 3,301%. By any reasonable measure, the Solana ecosystem has grown by 20 to 30 times since December 1, 2022.

However, as the core asset that carries and reflects this growth, SOL only outperformed BTC by 87%.

Please read this sentence again.

For an L1 token to generate meaningful excess returns for BTC, it doesn't just need its ecosystem to grow by 200%–300%; it needs to grow by 2,000%–3,000% to achieve high double-digit relative excess performance.

Based on all the above facts, we believe that although L1's valuation is still based on the expectation of a "potential future currency premium," market confidence in these expectations is quietly eroding. At the same time, the market's belief in a BTC currency premium has not wavered; in fact, it could be said that BTC's lead is still widening.

Furthermore, while cryptocurrencies, strictly speaking, do not require fees or revenue to support their valuation, these metrics are crucial for L1. Unlike BTC, L1's narrative heavily relies on its ecosystem—applications, users, throughput, and economic activity—to "support" the token's value.

However, if an L1 token experiences a year-over-year decline in ecosystem usage, reflected in lower transaction fees and revenue, it will lose its only competitive advantage over BTC. In the absence of real economic growth, these L1 cryptocurrency narratives will become increasingly difficult for the market to accept.

Looking ahead, we do not believe this trend will reverse in 2026 or longer. With very few potential exceptions, we expect alternative L1 to continue ceding market share to BTC. Their valuations are primarily driven by expectations of future currency premiums, and these valuations will continue to be compressed as the market gradually recognizes BTC as the most compelling candidate for cryptocurrency among all assets.

While Bitcoin will continue to face challenges in the coming years, these issues are either too far in the future or overly reliant on unknown variables to support the premium of other L1 currencies in the present. The burden of proof has shifted for L1 currencies: their narratives are no longer sufficiently convincing when compared to BTC, and they cannot rely on overall market sentiment to endorse their valuations in the long run.

Opposing Perspective: Why Could L1 Still Counter BTC?

While we don't expect L1 to outperform BTC in the short term, assuming its currency premium will inevitably converge to zero would also be a misjudgment. The market rarely assigns valuations of hundreds of billions of dollars to assets without underlying logic; the very existence of such valuations indicates that investors believe certain L1 assets may occupy a long-term position within the broader cryptocurrency ecosystem.

In other words, although BTC has clearly established its position as the dominant monetary asset in the crypto space, if Bitcoin fails to address certain structural challenges in the longer term, some L1 cryptocurrencies may still carve out their own long-term monetary niches.

Quantum Threat

The most pressing potential threat to Bitcoin's monetary status is the so-called "quantum threat." If quantum computers become powerful enough, they could potentially crack the Elliptic Curve Digital Signature Algorithm (ECDSA) used by Bitcoin, allowing attackers to deduce private keys from public keys. Theoretically, this would compromise all addresses whose public keys are exposed on-chain, including reused addresses and older UTXOs generated before best practices became widespread.

According to Nic Carter's estimates, approximately 4.8 million BTC (about 23% of the total supply) are stored in these exposed addresses, theoretically vulnerable to quantum attacks. Of these, about 1.7 million BTC (8% of the total supply) are located in early p2pk addresses; these coins are almost certainly "dead coins"—their holders are no longer alive, inactive, or have lost control of their private keys. This portion of assets constitutes the most intractable and unresolved issue.

If quantum computing truly poses a real risk, Bitcoin must introduce quantum-resistant signature schemes. Failure to achieve this transformation could lead to a collapse in BTC's monetary value, even reversing the classic adage: "Having the key doesn't guarantee you're the coin." Therefore, we believe the Bitcoin network will inevitably upgrade to address the quantum threat.

The real challenge lies not in the upgrade itself, but in how to handle these "dead coins." Even with the introduction of new quantum-resistant address formats, these coins may never be able to migrate, thus remaining vulnerable in the long term. Currently, two paths are most frequently discussed:

Doing nothing: Ultimately, any entity with quantum capabilities could seize these coins, injecting up to 8% of the supply back into the market, likely into the hands of those who weren't originally holders. This would almost certainly depress the price of BTC and undermine market confidence in its monetary nature.

Directly destroying these coins: After a predetermined block height, these vulnerable coins can no longer be spent, effectively removing them permanently from the supply. However, this approach also presents a significant trade-off—it violates Bitcoin's long-standing principle of censorship resistance and could set a dangerous precedent: coins could be "voted" to determine their existence.

Fortunately, quantum computing is unlikely to pose a real threat to Bitcoin in the short term. While forecasts vary widely, even the most aggressive estimates typically place the earliest potential risk window around 2030. Based on this timeline, we do not expect substantial progress on quantum issues by 2026. This remains a long-term governance issue, rather than an imminent engineering challenge.

The longer-term trajectory is even more difficult to predict. The biggest unresolved question is: how will the network ultimately handle dead coins that cannot be migrated to quantum-resistant address formats? We cannot be certain which path Bitcoin will choose, but we are confident that the network will ultimately make decisions that are conducive to maintaining and maximizing the value of BTC.

Both of these main approaches can actually be seen as serving this goal: the former maintains censorship resistance, but at the cost of introducing potential new supply; the latter sacrifices some of the censorship resistance narrative, but avoids BTC potentially falling into the hands of malicious actors.

Regardless of the path ultimately chosen, the quantum problem represents a real and long-term governance challenge. If quantum computing becomes a real threat and Bitcoin fails to upgrade, BTC's monetary status will cease to exist; and if this happens, alternative cryptocurrencies with stronger resistance to quantum paths could seize the opportunity to take over BTC's once-exclusive monetary premium.

Lack of Programmability

Another structural limitation of the Bitcoin network is its lack of general programmability. Bitcoin deliberately chose a non-Turing-complete design, and its scripting language is strictly limited in functionality, thus constraining the complexity of on-chain transaction logic.

Unlike other ecosystems where smart contracts can natively verify and execute complex signature conditions, Bitcoin currently cannot directly verify external messages and struggles to achieve low-trust cross-chain collaboration without relying on off-chain infrastructure.

This is why almost no applications, such as DEXs, on-chain derivatives, and privacy tools, can be natively built on Bitcoin L1.

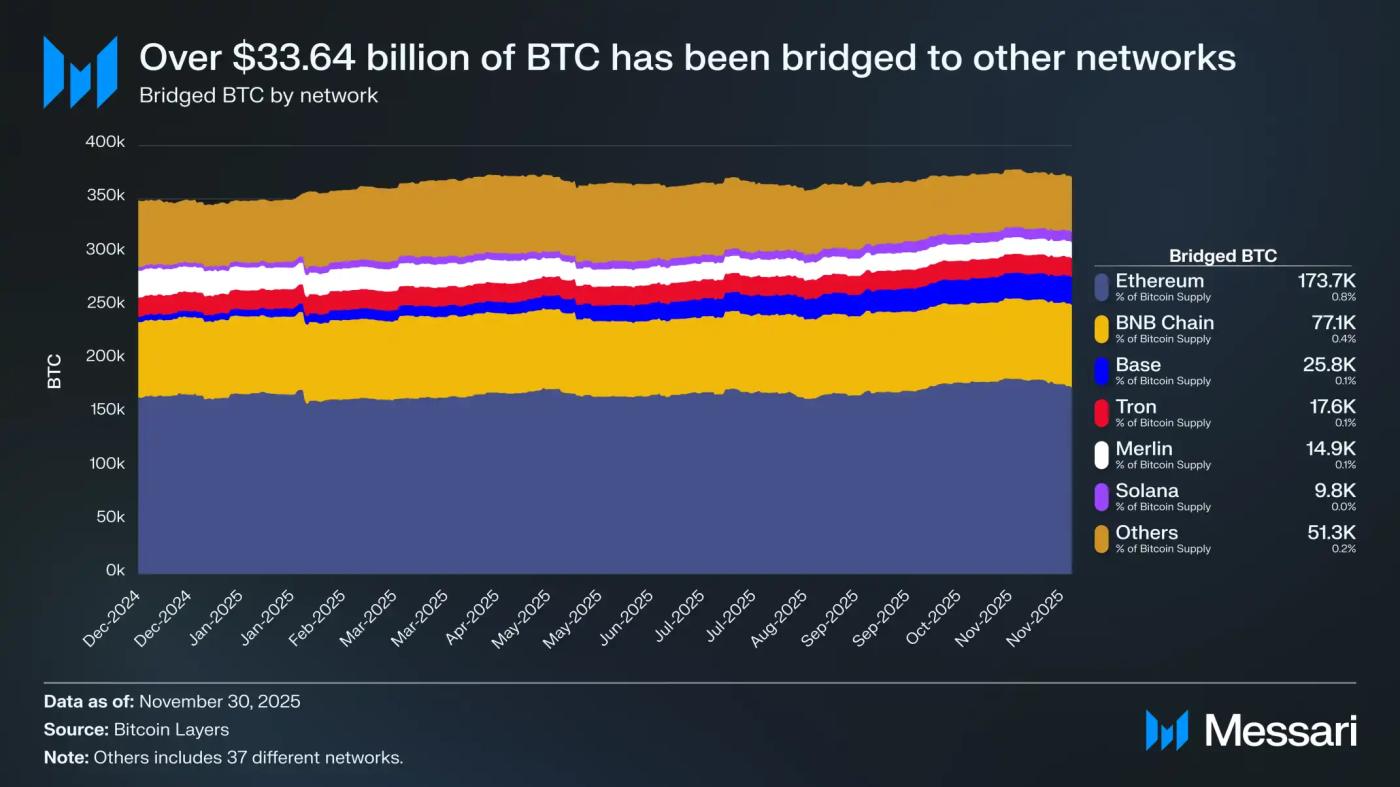

While some proponents argue that this design helps reduce the attack surface and maintain Bitcoin's simplicity as a currency, it's undeniable that a significant portion of BTC holders desire access to programmable environments. As of this writing, 370,300 BTC (approximately $33.64 billion) have been bridged to other networks. Of these, 365,000 BTC (approximately 99% of all cross-chain BTC) rely on custodial solutions or introduce trust-based assumptions. In other words, in order to use BTC in a more expressive ecosystem, users are effectively reintroducing the very set of risks that Bitcoin originally aimed to eliminate.

Within the Bitcoin ecosystem, attempts to address this issue—including consortium sidechains, early L2 solutions, and low-trust multisignature mechanisms—have not substantially reduced the reliance on critical trust assumptions. Users do want to deploy BTC in a more programmable environment, but in the absence of truly trustless cross-chain methods, they often have to settle for centralized custodians.

As Bitcoin's market capitalization continues to grow and it increasingly resembles a macro asset, the demand for "how to use Bitcoin efficiently" will only continue to rise. Whether using Bitcoin as collateral, for lending, for exchanging it for other assets, or for interacting with a more expressive and programmable financial system, users naturally want to do more than just hold the currency; they want to be able to use it.

However, under Bitcoin's current design, these use cases introduce significant long-tail risks—because using BTC in a programmable or leveraged environment almost inevitably requires entrusting asset custody to a centralized intermediary.

For these reasons, we believe that the Bitcoin network will eventually need to fork to support these use cases in a trustless and permissionless manner. We do not believe this means Bitcoin needs to transform into a smart contract platform; rather, a more reasonable path might be to introduce new opcodes, such as OP_CAT, to achieve trustless cross-chain and composability of BTC.

OP_CAT is noteworthy because it requires only a small consensus layer modification to potentially unlock trustless transfers of BTC between different chains. This doesn't mean transforming Bitcoin into a smart contract platform, but rather introducing a relatively simple opcode; when used in conjunction with Taproot and existing script primitives, it allows Bitcoin to directly execute and constrain spending conditions at the base layer.

This capability will enable BTC cross-chain bridges that do not require custody, eliminating reliance on custodians, consortium mechanisms, or external validator sets, thus directly addressing the core risks of the current problem—the very risks that have led to hundreds of thousands of BTC being encapsulated in custodial assets today.

Unlike the quantum threat, Bitcoin's lack of programmability does not pose an existential risk to its "monetary" nature. However, it does limit the accessible market size of BTC as cryptocurrency. The demand for "programmable money" is already clearly visible: more than 370,000 BTC (approximately 1.76% of the total supply) are currently stored in cross-chain environments, and the assets deployed within the DeFi ecosystem have exceeded $120 billion.

As the crypto ecosystem continues to expand and more financial activities migrate on-chain, this demand will only grow further. However, the reality is that Bitcoin currently does not offer a trustless path for BTC to securely participate in the programmable ecosystem. If the market ultimately deems the associated risks unacceptable, then programmable Level 1 assets such as ETH and SOL will become the primary beneficiaries of this demand.

Security Budget

The last structural problem facing Bitcoin is its security budget. This issue has been discussed for over a decade, and although opinions on its severity vary widely, it remains one of the most contentious issues surrounding Bitcoin's long-term monetary integrity.

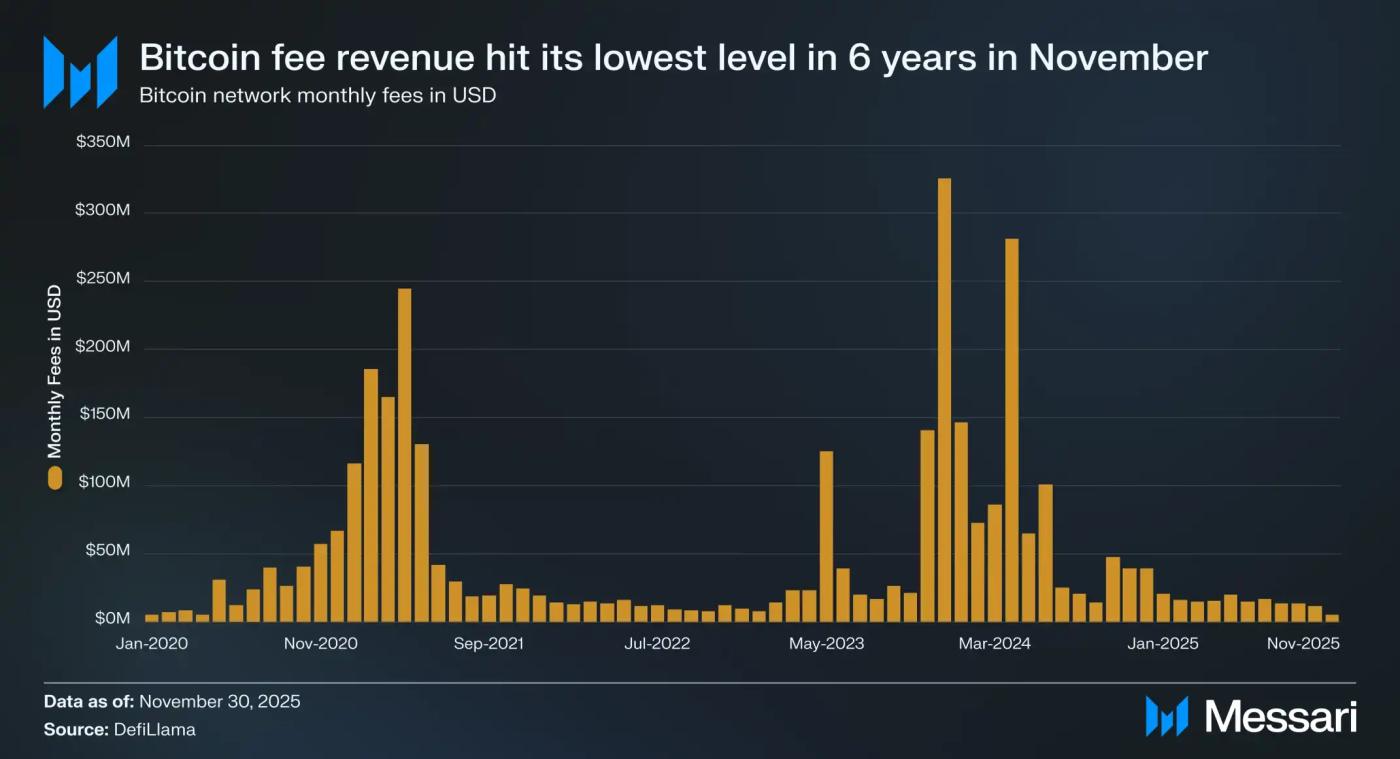

Essentially, the security budget refers to the total compensation miners receive for maintaining network security, currently consisting of two main parts: block rewards and transaction fees. With block rewards halving every four years, Bitcoin will eventually have to rely primarily on transaction fees, and in the more distant future, entirely on them, to incentivize miners to continue providing security for the network.

At one point, amidst the soaring popularity of Ordinals and Runes, the market seemed to see a possibility: transaction fees alone might be enough to compensate miners and maintain network security. In April 2024, Bitcoin's on-chain transaction fee revenue reached $281.4 million, the second-highest monthly level in history. However, just a year and a half later, transaction fee revenue experienced a precipitous decline. In fact, on-chain transaction fees in November 2025 were only $4.87 million, the lowest monthly level since December 2019.

While the sharp drop in transaction fees is alarming, it doesn't necessarily pose an immediate risk. Bitcoin's block subsidies continue to provide a significant incentive for miners, and will remain so for decades to come. Even by 2050, the network will still be adding approximately 50 BTC per week, a substantial issuance for miners. As long as block subsidies remain the dominant source of miners' revenue, network security is unlikely to be threatened.

Nevertheless, the likelihood of on-chain fees completely replacing block subsidies is becoming increasingly lower.

It's important to note that the discussion surrounding security budgets is not simply a matter of whether transaction fees can completely replace subsidies. Transaction fees do not need to be equivalent to current subsidy levels; they only need to be higher than the cost of launching a trusted attack. This cost itself is difficult to measure precisely and may change significantly with the evolution of mining technology and the energy market.

If mining costs decrease significantly in the future, the minimum transaction fee requirement will also decrease accordingly. This change could occur in several scenarios: in a moderate scenario, incremental improvements in ASICs and lower-cost access to idle renewable energy will reduce miners' marginal costs; in an extreme scenario, energy breakthroughs such as the commercialization of controlled nuclear fusion or ultra-low-cost nuclear energy could cause electricity prices to drop by orders of magnitude, fundamentally changing the economic structure for maintaining computing power.

Even acknowledging that there are too many variables to precisely calculate the level at which Bitcoin's security budget "needs" to reach, it is still necessary to consider a hypothetical scenario: that miner rewards ultimately become insufficient to economically guarantee network security. In this case, the incentive mechanisms supporting Bitcoin's "trust neutrality" will begin to loosen, and network security will increasingly rely on social expectations rather than enforceable economic constraints.

One possibility is that certain participants—exchanges, custodians, national entities, or large holders—may choose to mine at a loss to protect the assets they depend on. However, while this "defensive mining" may technically maintain network security, it could also undermine the social consensus on BTC as a currency. If users begin to perceive BTC as relying on the coordinated actions of a few large entities for security, its monetary neutrality, and consequently its monetary premium, could face pressure.

Another equally possible scenario is that no entity is willing to incur economic losses to maintain the network. In this scenario, Bitcoin could face the risk of a 51% attack. While a 51% attack does not permanently destroy Bitcoin (Ethereum Classic, Monero, and other PoW chains have survived 51% attacks), it undoubtedly raises serious questions about Bitcoin's security.

With so many uncertainties shaping Bitcoin's long-term security budget, no one can provide a definitive answer regarding the system's evolution decades from now. This uncertainty doesn't pose a real threat to BTC, but it does create a long-tail risk that needs to be priced in by the market. From this perspective, the residual monetary premium of some L1 assets can also be seen as a hedge against the extremely low probability event that "Bitcoin's long-term economic security may be challenged."

The ETH debate: Is it a cryptocurrency?

Of all major crypto assets, none has sparked such long-term, sustained debate as ETH. While BTC's position as the dominant cryptocurrency is virtually unchallenged, ETH's role is far from settled.

Some people see ETH as the only asset besides BTC that possesses the attributes of a credible non-sovereign currency; while others see ETH as a "business" with declining revenue, narrowing profit margins, and constant competition from faster and cheaper L1 cryptocurrencies.

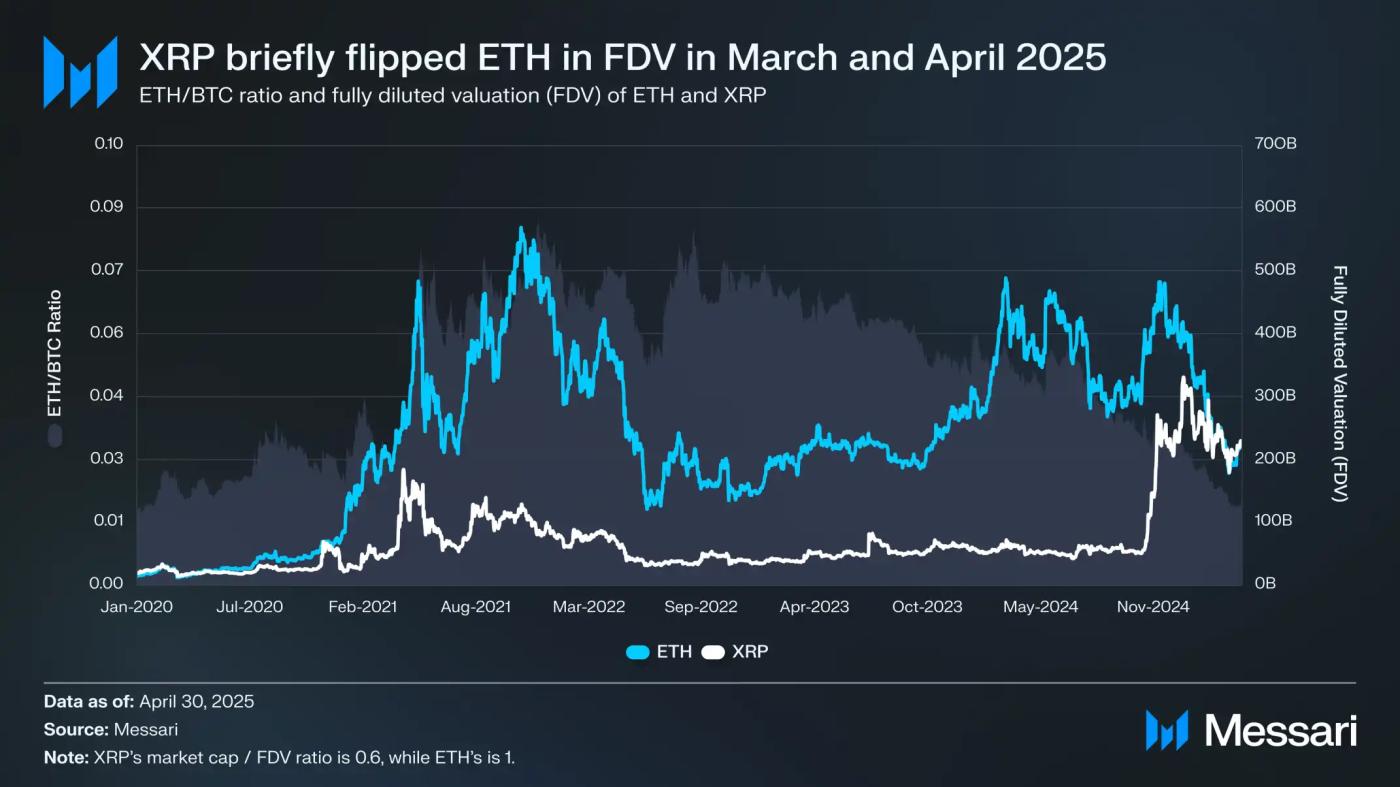

This debate seemed to reach its climax in the first half of the year. In March, XRP briefly surpassed ETH in fully diluted value (FDV) (it should be noted that ETH is fully circulating, while XRP currently has only about 60% of its supply in circulation).

On March 16th, ETH's FDV was approximately $227.65 billion, while XRP's FDV reached $239.23 billion—a result almost no one would have thought possible a year ago. Then, on April 8th, 2025, the ETH/BTC exchange rate fell below 0.02, the first time since February 2020. In other words, all of ETH's excess performance relative to BTC in the previous cycle has been completely reversed.

By that time, market sentiment surrounding ETH had fallen to its lowest level in years.

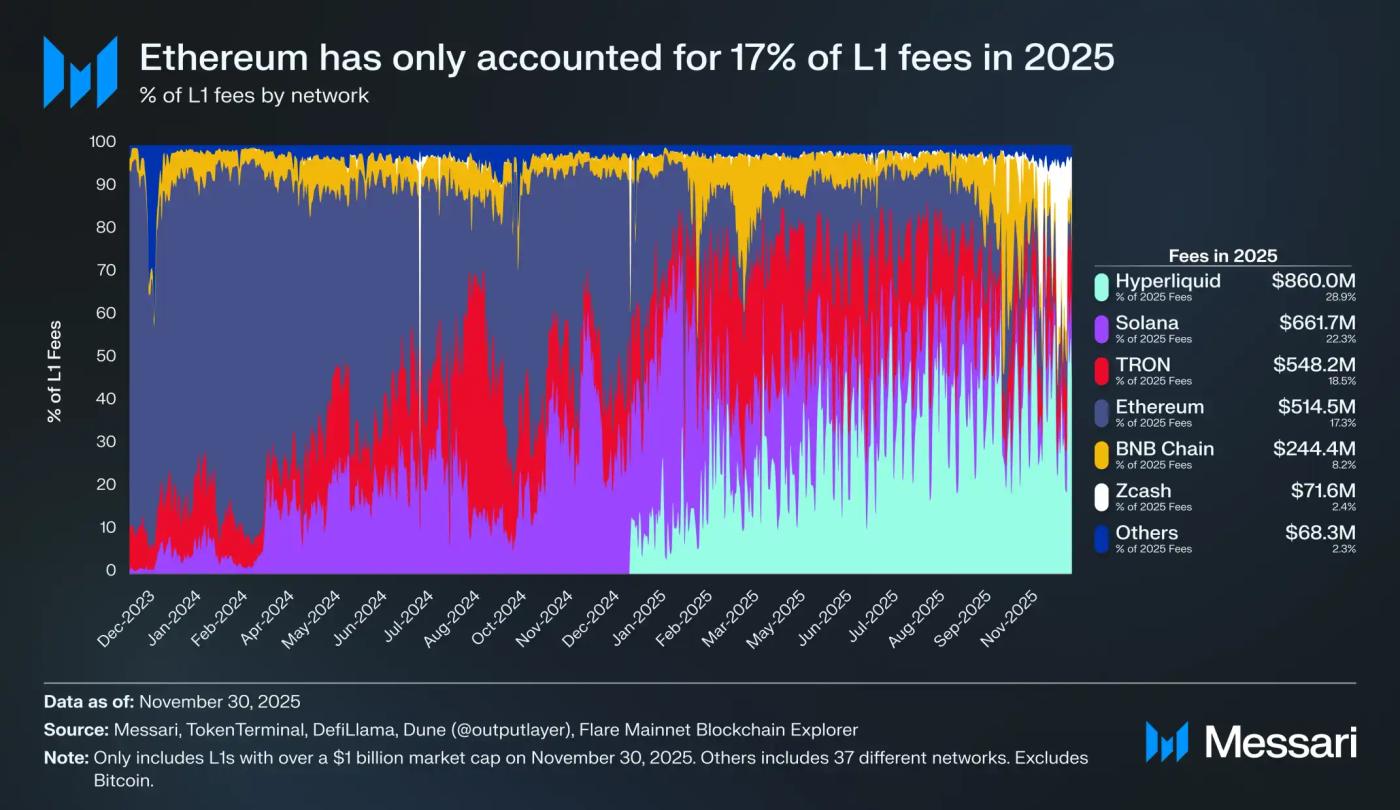

Worse still, price performance is only part of the problem. As the competitive ecosystem continues to grow, Ethereum's share of L1 transaction fees has been steadily declining. Solana regained its footing in 2024, and Hyperliquid made a breakthrough in 2025, together squeezing Ethereum's share of transaction fees to 17%—ranking only fourth among all L1 tokens, a dramatic drop from its dominant position a year earlier.

Transaction fees are not the only measure of everything, but they are undoubtedly a clear signal of where economic activity is moving in. And right now, Ethereum is facing the most intense competitive environment in its development history.

However, history has repeatedly shown that the most important reversals in the crypto market often occur during the most pessimistic moments. When ETH was widely regarded as a "failure asset" and abandoned by the market, many of its perceived "problems" had already been fully priced in.

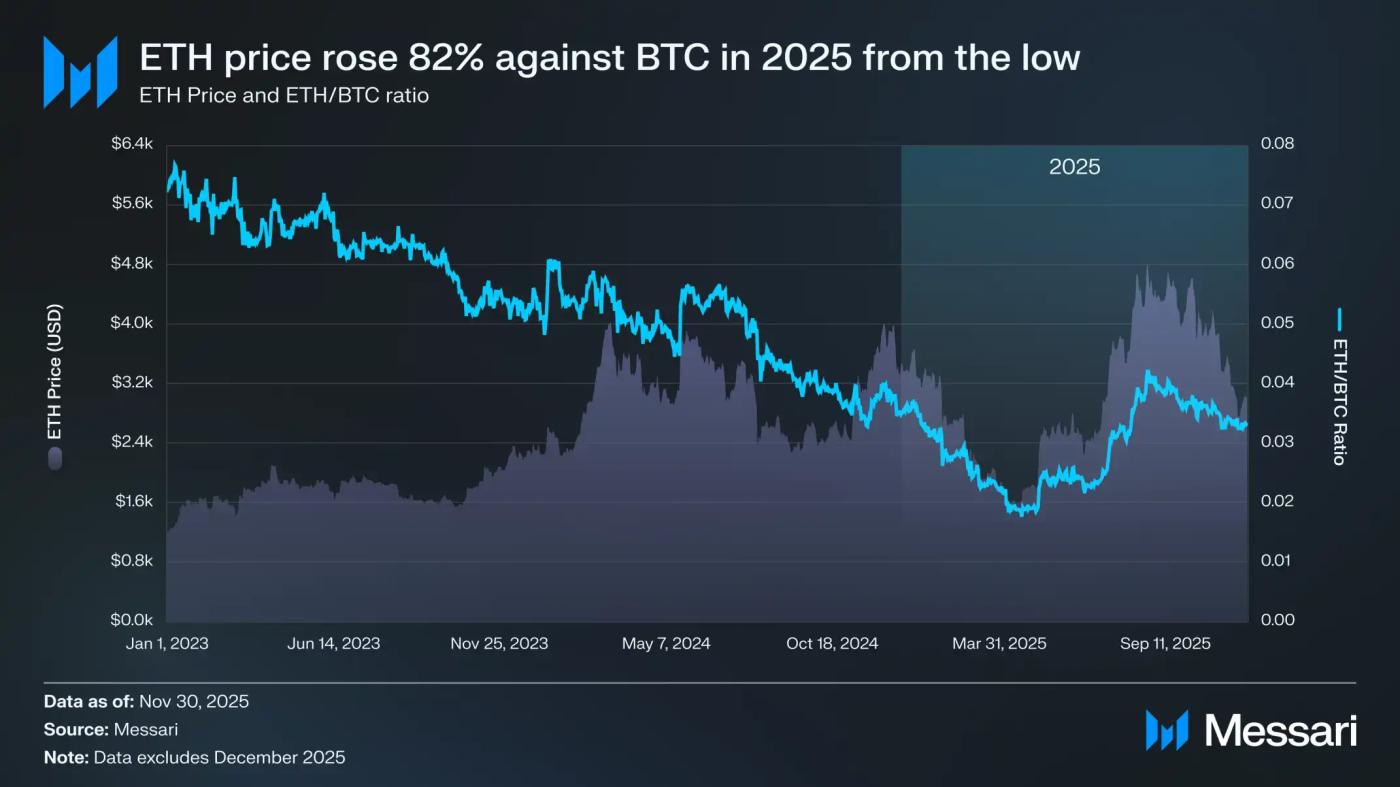

In May 2025, signs of excessive market pessimism first emerged. Since then, both the ETH/BTC ratio and the USD-denominated price of ETH have begun a clear reversal. The ETH/BTC ratio rose from a low of 0.017 in April to 0.042 in August, an increase of 139%; simultaneously, ETH itself rose from $1,646 to $4,793 during the same period, a cumulative increase of 191%. This momentum finally culminated on August 24, with ETH hitting a new all-time high of $4,946.

Following this repricing, the market gradually realized that ETH's overall trajectory had shifted towards renewed strength. The leadership changes at the Ethereum Foundation (discussed later) and the emergence of ETH-centric digital asset treasuries injected a sense of certainty and confidence into the market that had been noticeably absent over the previous year.

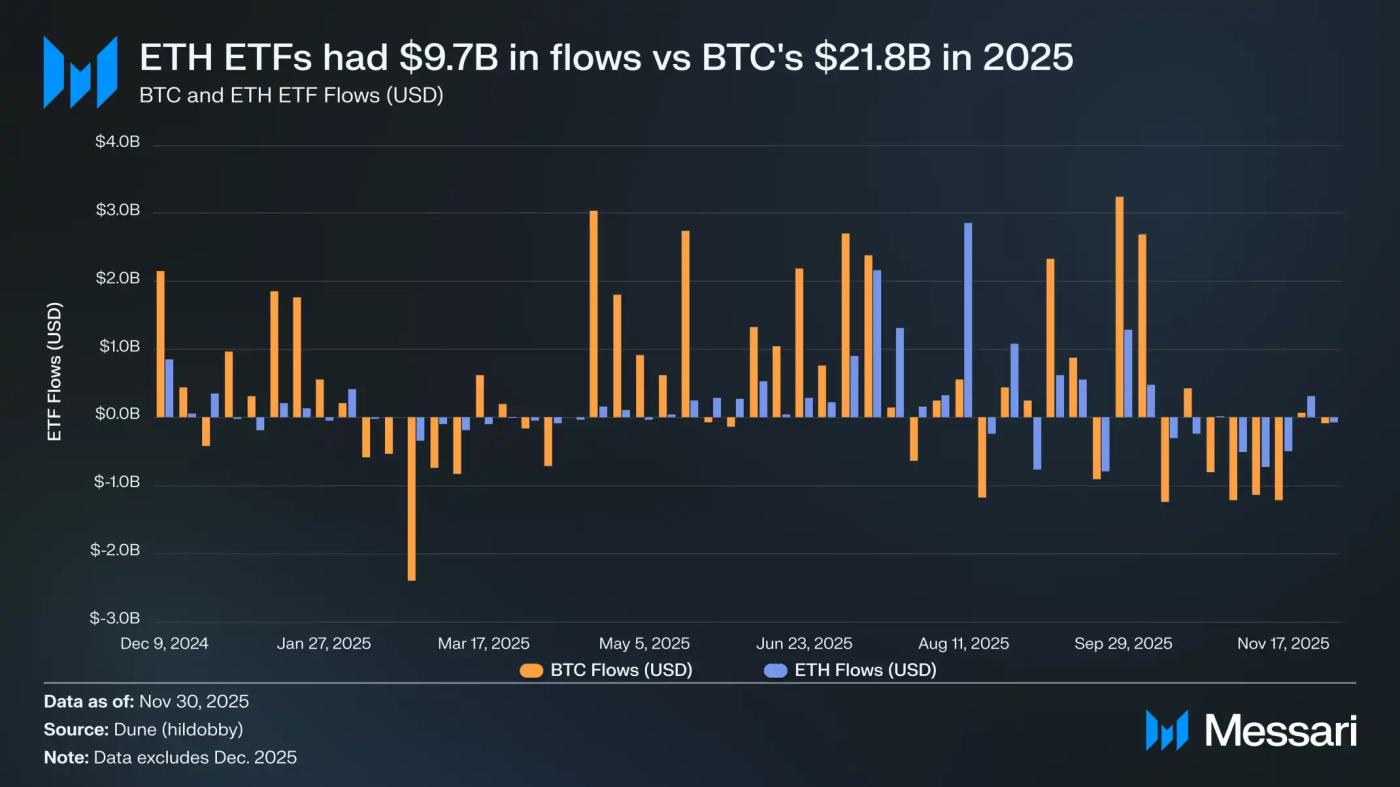

Prior to this rebound, the disparity between BTC and ETH was particularly evident in their respective ETF markets. When the spot ETH ETF launched in July 2024, inflows were extremely weak. In its first six months, it saw a cumulative net inflow of only $2.41 billion, a rather lackluster performance compared to the record-breaking performance of the BTC spot ETF.

However, with the recovery of ETH, concerns surrounding ETF fund flows were completely reversed. In the following year, the spot ETH ETF attracted a total of $9.72 billion, while the BTC ETF saw inflows of $21.78 billion during the same period. Considering that BTC's market capitalization is almost five times that of ETH, the difference in fund inflows was only 2.2 times, a result far lower than the market's previous expectations.

In other words, after adjusting for market capitalization, the demand for ETH ETFs is actually higher than that for BTC, a stark reversal of the previous narrative that "institutions have no real interest in ETH." At certain points, ETH even outperformed BTC across the board.

From May 26 to August 25, ETH ETF saw inflows of $10.2 billion, exceeding BTC's $9.79 billion during the same period. This was also the first time that institutional demand clearly shifted towards ETH.

From the perspective of ETF issuers, BlackRock has further solidified its dominant position in the ETF market. By the end of 2025, BlackRock held 3.7 million ETH, representing approximately 60% of the entire spot ETH ETF market. This figure represents a 241% increase compared to 1.1 million ETH at the end of 2024, ranking first in annual growth among all issuers.

Overall, the spot ETH ETF held a total of 6.2 million ETH at the end of the year, accounting for approximately 5% of the total ETH supply.

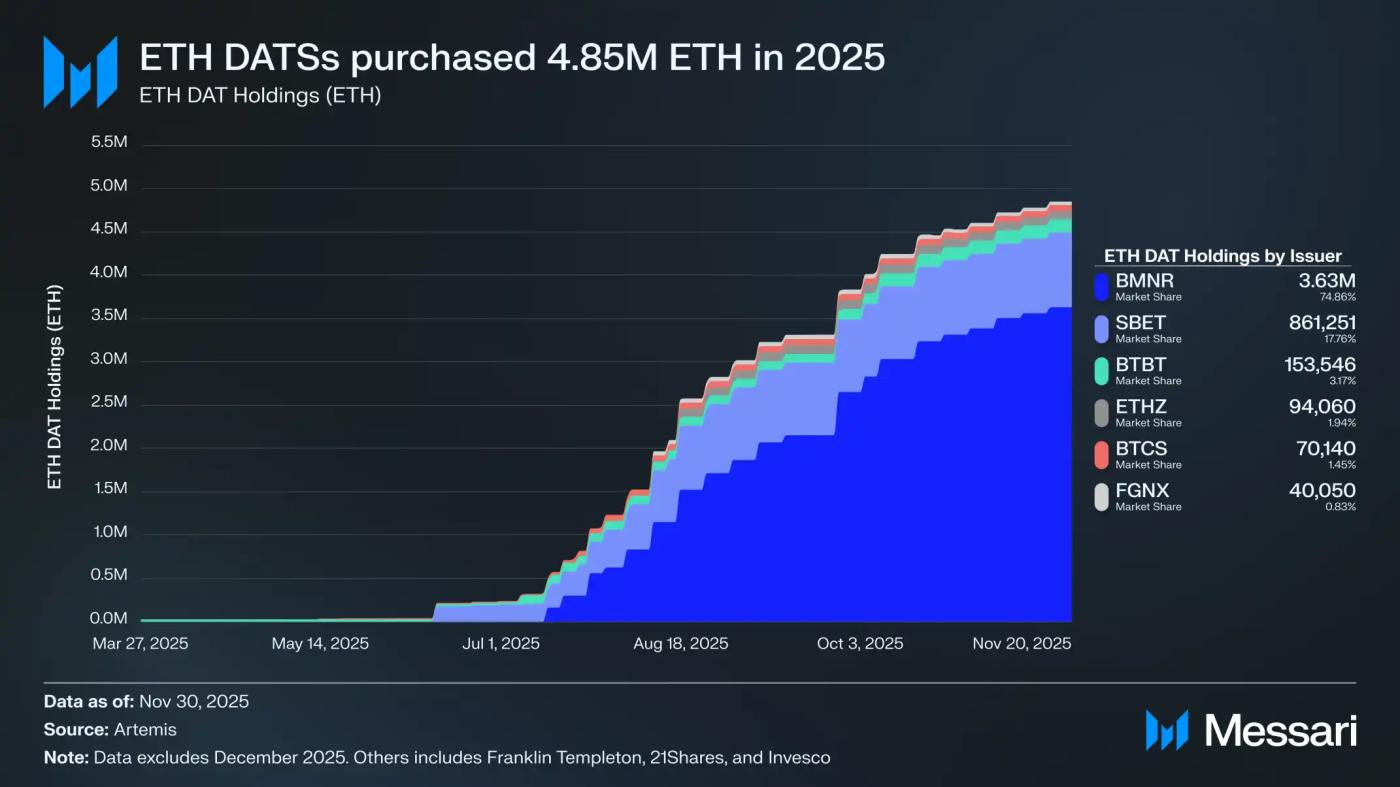

Behind ETH's strong rebound, the most crucial change is the rise of Digital Asset Treasuries (DATs) centered around ETH. DATs have brought ETH a stable and repeatable source of demand never before seen, anchoring the asset price in a way that narratives or speculative funds cannot achieve. If ETH's price movement marks a superficial turning point, then the continued accumulation of DATs represents the deep structural change that has driven this shift.

DAT has had a significant impact on the price of ETH. Throughout 2025, DAT collectively increased its holdings by approximately 4.8 million ETH, equivalent to 4% of the total ETH supply. The most aggressive ETH DAT was Bitmine (BMNR), owned by Tom Lee—a company originally engaged in Bitcoin mining—which began shifting its treasury and capital structure towards ETH in July 2025. Between July and November, Bitmine purchased a total of 3.63 million ETH, accounting for 75% of all DAT holdings, becoming the undisputed leader in the sector.

Despite the powerful reversal of ETH, this rally eventually cooled down. By November 30th, ETH had fallen from its August high to $2,991, significantly lower than both the current high and the all-time high of $4,878 in the previous cycle. Compared to April, ETH's overall situation has improved significantly, but this rebound has not eliminated the structural concerns that initially fueled the bearish sentiment. If anything has changed, the debate surrounding ETH has become more intense than ever before.

From the perspective of its supporters, ETH is exhibiting many similar characteristics to BTC in its process of establishing its monetary status: ETF inflows are no longer sluggish; digital asset vaults are becoming a source of continuous demand; and more importantly, a growing number of market participants are beginning to view ETH as a special asset distinct from other L1 tokens—in the eyes of some, it has been incorporated into the same monetary framework as BTC.

However, the core concerns that dragged down ETH at the beginning of the year remain. Ethereum's fundamentals have not fully recovered; its share of L1 transaction fees continues to be squeezed by strong competitors such as Solana and Hyperliquid; and on-chain activity at the base layer remains significantly lower than the peak of the previous cycle. Meanwhile, despite ETH's strong rebound, BTC has firmly established itself above its all-time high, while ETH has yet to recover its previous high. Even during ETH's strongest months, a significant number of holders viewed the rise as an exit from liquidity rather than a confirmation of the long-term monetary narrative.

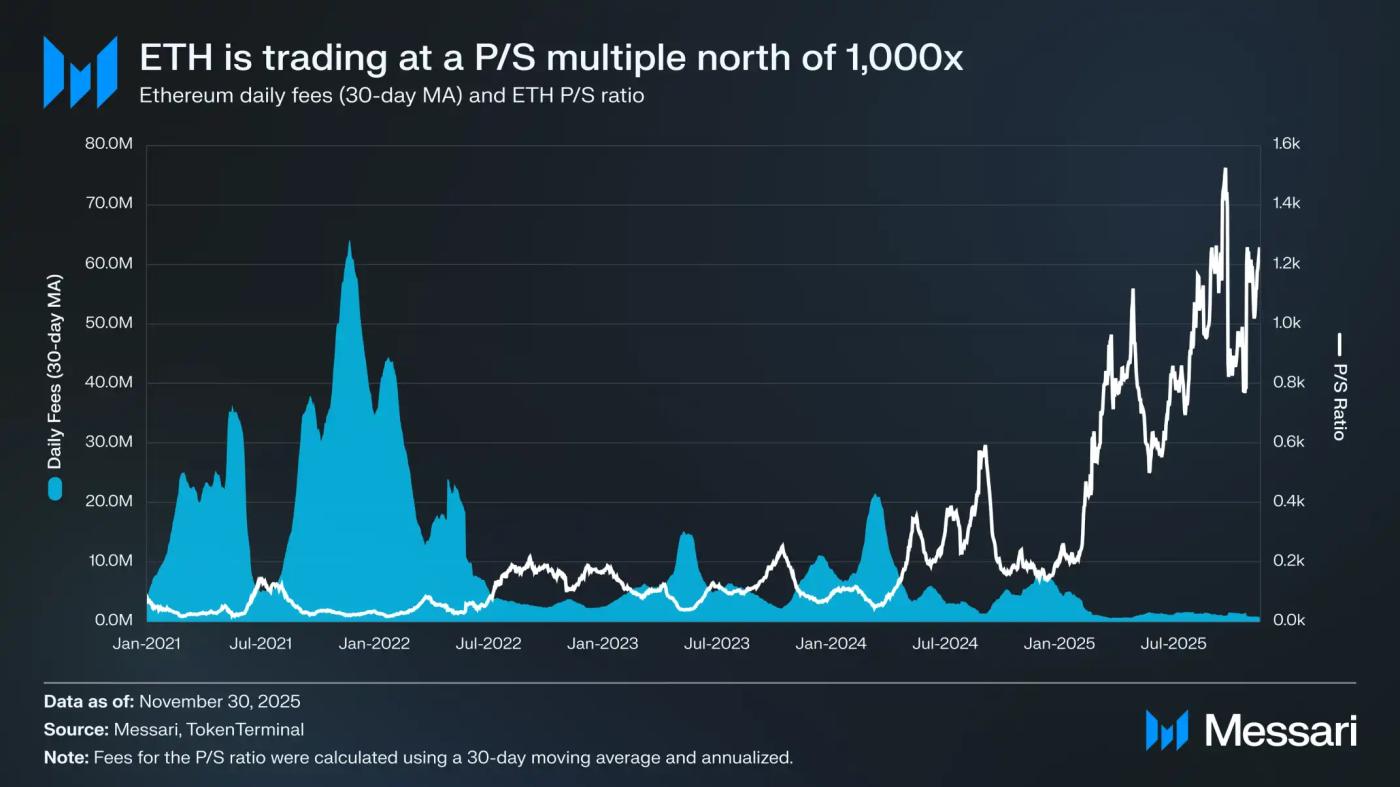

The core issue in this debate is not whether Ethereum "has value," but rather: how exactly does the asset ETH derive value from the Ethereum network?

In the previous cycle, the market generally assumed that ETH would directly capture value from Ethereum's success. This was a key component of the "Ultrasound Money" narrative: as Ethereum became more useful, the network would burn large amounts of ETH, making it a deflationary value vehicle.

Today, we can say with considerable confidence that things will not unfold as previously anticipated. Ethereum's transaction fee revenue has declined significantly, with no clear signs of recovery; and its most important current growth drivers—RWA and institutional participation—are primarily based on the US dollar, not ETH, at the usage level.

In this context, ETH's value will depend on its ability to indirectly capture value from Ethereum's success. However, compared to direct, mechanical value capture, indirect value capture is far more uncertain. It relies on the expectation that as Ethereum's importance at the system level continues to grow, more users and capital will choose to view ETH as a cryptocurrency and a store of value.

However, unlike direct value capture mechanisms, this process offers no guarantees. It depends entirely on social preferences and collective beliefs—this in itself is not a flaw (a whole section has already explained how BTC accumulates value in this way), but it also means that ETH's price performance is no longer directly and deterministically linked to Ethereum's economic activity.

All these factors ultimately bring the debate surrounding ETH back to its core tensions. While ETH may indeed be accumulating a monetary premium, this premium remains subordinate to and after BTC. The market is once again viewing ETH as a leveraged expression of the BTC monetary narrative, rather than an independent monetary asset.

In 2025, the 90-day rolling correlation coefficient between ETH and BTC mostly remained in the range of 0.7 to 0.9, while its rolling beta value soared to multi-year highs, even exceeding 1.8 at times. This means that ETH's volatility has significantly exceeded that of BTC, but its price movement remains highly dependent on BTC.

This is a subtle yet extremely important distinction. Currently, ETH's monetary relevance holds true because BTC's monetary narrative remains robust. As long as the market continues to believe in BTC's status as a non-sovereign store of value, some marginal participants will be willing to extrapolate this belief to ETH.

If BTC continues to strengthen in 2026, ETH will have a relatively clear path to further narrow the gap with BTC.

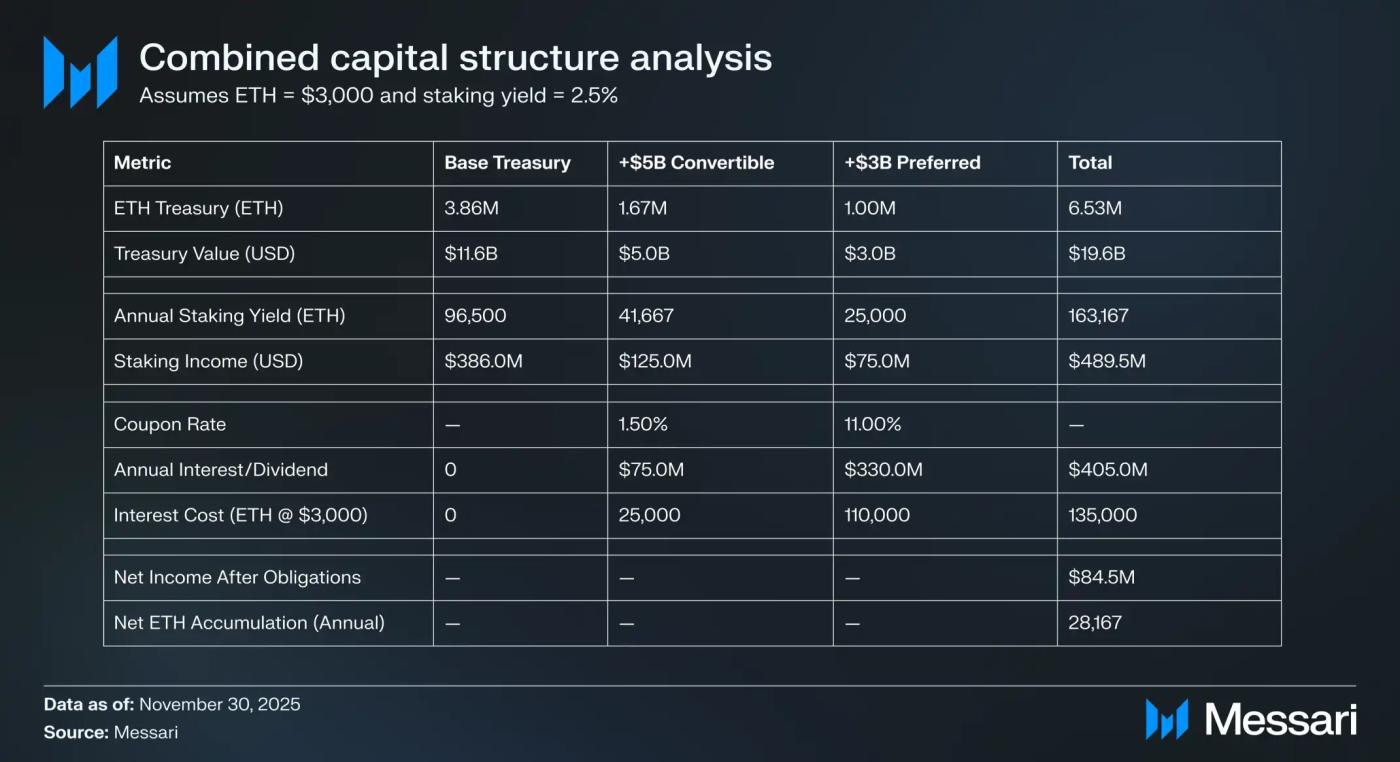

Ethereum DAT is still in the early stages of its lifecycle, and to date, its ETH accumulation has primarily been achieved through common equity financing. However, in the next crypto bull market, these entities could very well explore more capital structure tools, replicating the path Strategy took when expanding its BTC exposure, including convertible bonds and preferred stock.

For example, DATs like BitMine can issue low-coupon convertible debt with higher-yield senior capital and use the raised funds directly to purchase ETH, while staking that ETH to generate continuous returns. Un