Original article | Odaily Odaily( @OdailyChina )

Author | Dingdang ( @XiaMiPP )

2025 will be a year of substantial breakthroughs for the cryptocurrency market at the institutional level, and a year in which it gradually moves away from its unregulated growth and towards the mainstream financial system. In terms of scale, the total global market capitalization of crypto assets has reached $3.2 trillion, while stablecoin trading volume exceeds $50 trillion—figures far surpassing traditional payment giants such as Visa and PayPal. Behind these figures lies the support of two key legislative advancements.

First, the legislation related to stablecoins has been officially implemented . The legislation clarifies the issuing entities, reserve requirements, and regulatory mechanisms, providing a clear legal definition for "on-chain dollars." This not only reduces policy uncertainty for stablecoin businesses but also directly stimulates investment and financing activity in stablecoin, payment, and settlement-related sectors. Second, the cryptocurrency market structure legislation is also progressing steadily, incorporating crypto assets into a categorized regulatory framework to avoid a "one-size-fits-all" approach and provide a predictable compliance path for projects and investors.

The combined effect of these two legislative developments will, to some extent , reshape how the primary market assesses risk and return .

However, in contrast to the improved institutional environment, the secondary market in 2025 did not respond strongly. Bitcoin prices fluctuated wildly, and altcoins performed poorly. Against this backdrop, the primary market did not experience the widespread frenzy of the previous bull market, but rather exhibited a cautiously active trend, with significant changes in the pace and preferences of fundraising .

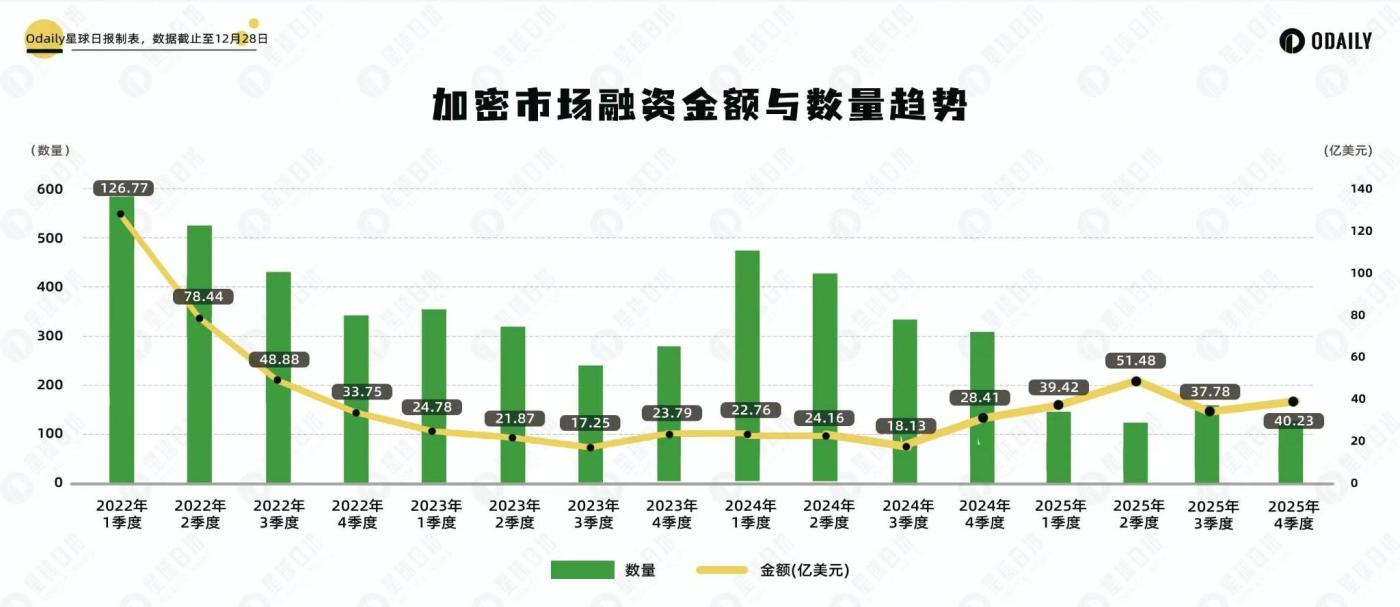

A Four-Year "Cycle" Review: Two Divergences Between the Number and Amount of Financing

Looking back at the crypto funding trends over the past four years, we can clearly see the evolution of the relationship between the primary market and the secondary market.

In early 2022, still benefiting from the lingering bull market momentum, the number and amount of financing events remained high. Subsequently, as Bitcoin entered a downward cycle, financing activities gradually shrank. Between 2022 and 2023, investment and financing activities were highly correlated with price movements, but were generally sluggish under the pressure of a bear market.

2024 marked a significant turning point, with the amount and number of funds raised diverging for the first time .

This year, with the resurgence of the Bitcoin halving narrative, the number of funding events rebounded significantly, but the amount raised remained restrained. Quarterly funding hovered between $1.8 billion and $2.8 billion , almost identical to the bear market period. The main reason was that the crypto market during this period was dominated by Bitcoin and meme stocks , a stark contrast to the previous cycle. In the previous cycle, VC projects were typically the core of market trends, but in 2024, VC projects generally performed poorly, failing to have a substantial impact on the market, which to some extent suppressed large-scale funding rounds.

Entering 2025, the divergence reappeared , but this time the direction was reversed.

The number of funding rounds declined significantly, but the amount raised rebounded. Quarterly funding rose back to the $3.7 billion to $5.1 billion range. This indicates a significant increase in the size of individual funding rounds, as investors are actively reducing their investment frequency and instead focusing their bets on a few projects deemed to have certainty and room for expansion.

12 tracks, $17.89 billion: Structural changes in the primary market

According to incomplete statistics from Odaily Odaily, the total investment and financing amount in the primary market reached US$ 17.89 billion in 2025, with a total of 569 financing events. To more accurately depict changes in financing preferences, we have subdivided all projects with disclosed financing (the actual closing time is often earlier than the announcement) into 12 sectors based on dimensions such as the business type, target audience, and business model of the financing projects. These sectors include: CeFi, Infrastructure, RWA, AI, DeFi, SocialFi, Prediction Markets, PayFi, DePIN, BTCFi, L1, and GameFi.

Looking at the financing situation in specific sub-sectors:

- CeFi and infrastructure rank among the top in terms of both funding amount and number. Underlying capabilities such as trading, custody, clearing, security, and cross-chain remain the focus of continued capital investment, and the market consensus on " infrastructure first " has not wavered.

- DeFi projects remain highly active, and the market continues to have a strong demand for innovative new DeFi protocols. In particular, the success of Hyperliquid has directly demonstrated to the market that decentralized exchanges can effectively handle large-scale capital inflows, making perp DEX a new hot spot for fundraising .

- AI and RWA have become new narrative pillars. The former aligns with the main thread of the global technology cycle, while the latter directly benefits from the institutional dividends of putting traditional financial assets on-chain. Both paths share a common characteristic: the growth logic no longer relies entirely on the native crypto market, but extends to the broader technology and traditional financial systems.

- The real breakout comes from prediction markets . Although the number of projects in this sector is not particularly outstanding, the amount of funding has jumped to become the second largest sector after infrastructure. This means that funds are being highly concentrated on a few top projects.

- In contrast, while many projects still emerge in once-popular sectors such as DePIN and GameFi , their fundraising appeal has sharply diminished , with funds shifting towards areas that offer greater certainty and economies of scale.

Overall, the primary market is shifting from a "wide net" approach to a "detailed cultivation" approach.

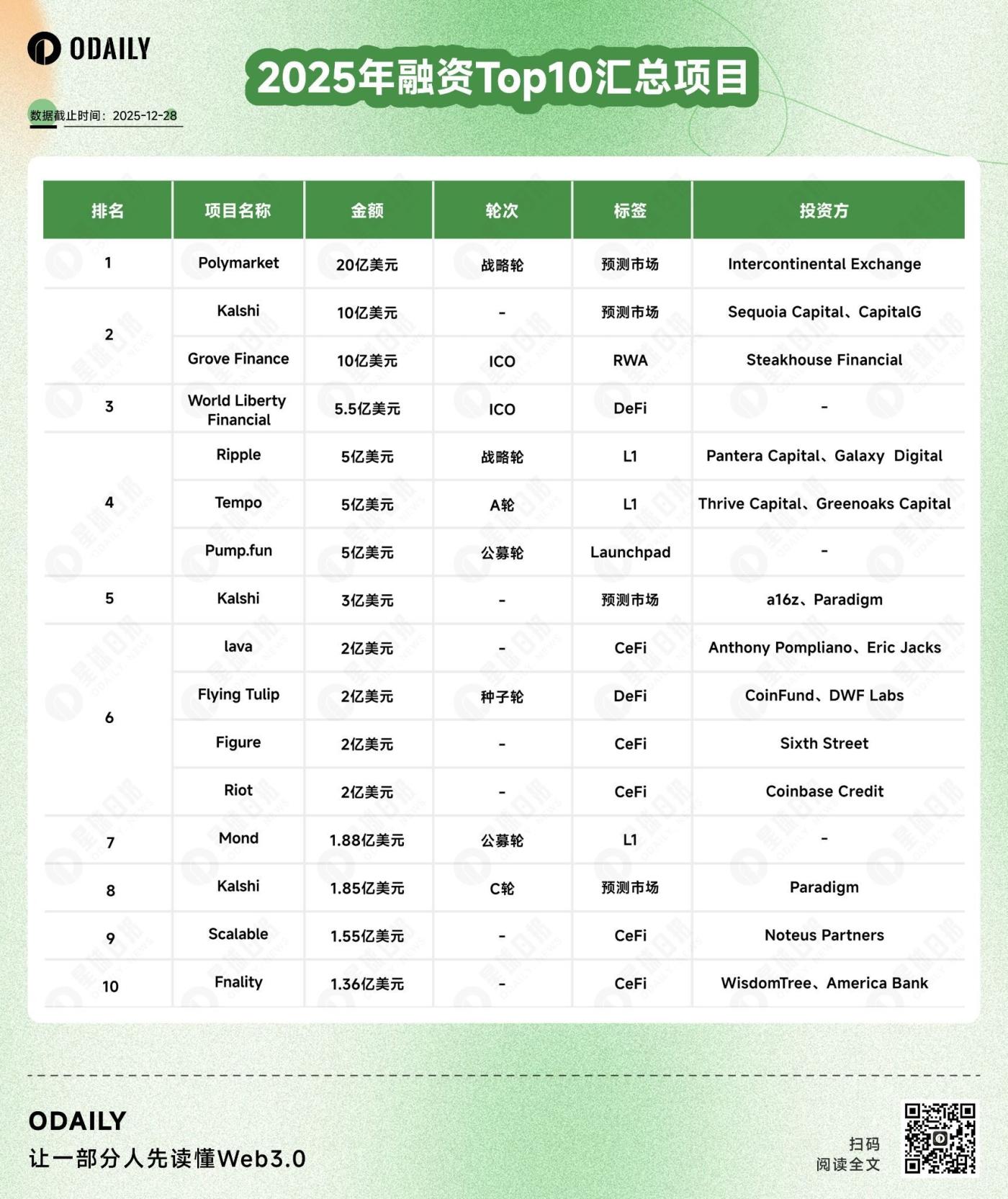

Polymarket: The Consensus Shift Behind the Top Funding Source in 2025

The list of the top 10 companies by funding amount in 2025 shows that Polymarket and Kalshi almost constitute the entire narrative of funding in 2025.

Polymarket has raised nearly $ 2.5 billion in multiple funding rounds , with investors including well-known crypto venture capital funds such as Polychain, Dragonfly, and Coinbase. Kalshi, which began its expansion in 2025, has raised approximately $ 1.5 billion , backed by Paradigm, a16z, and Coinbase. Unlike Polymarket, Kalshi places greater emphasis on federal regulatory compliance. However, both are viewed as a financial form with real demand, and have become one of the most dynamic and positive growth areas.

In the L1 blockchain sector, the investment preference remains consistent. Aside from established public chains like Ripple, other projects on the list, such as Tempo and Mond, are newer generation projects. Mond has already issued its token, while Tempo has not yet. This reflects investors' continued investment in underlying infrastructure, with high-performance L1 still considered a long-term cornerstone for ecosystem expansion .

Conclusion

Overall, the primary market in 2025 did not cool down, but rather underwent proactive contraction and restructuring .

Funds are still flowing, but they are no longer chasing quantity; instead, they are being concentrated on certainty, compliance, and scale potential. This change does not necessarily mean fewer opportunities; rather, it may indicate that the crypto market is entering a more rational and mature phase.