Written by: Yuan Biao

In December 2025, discussions surrounding "tokenization of US stocks" surged in the US financial market.

This is mainly due to two things: first, Nasdaq's application to extend trading hours has led the market to speculate that "the era of 24/7 stock tokenization trading is coming"; second, the U.S. Securities and Exchange Commission ( SEC ) issued a "No Action Letter" to the U.S. Central Clearing Corporation ( DTC ), which has made it the focus of the global financial community.

However, behind the excitement, these two events are completely different from the actual connection between "tokenization of US stocks". We need to see through the surface to clarify the true development of the industry.

Nasdaq Extends Trading Hours: "Timeliness Optimization" in Traditional Securities, Not Directly Related to Tokenization

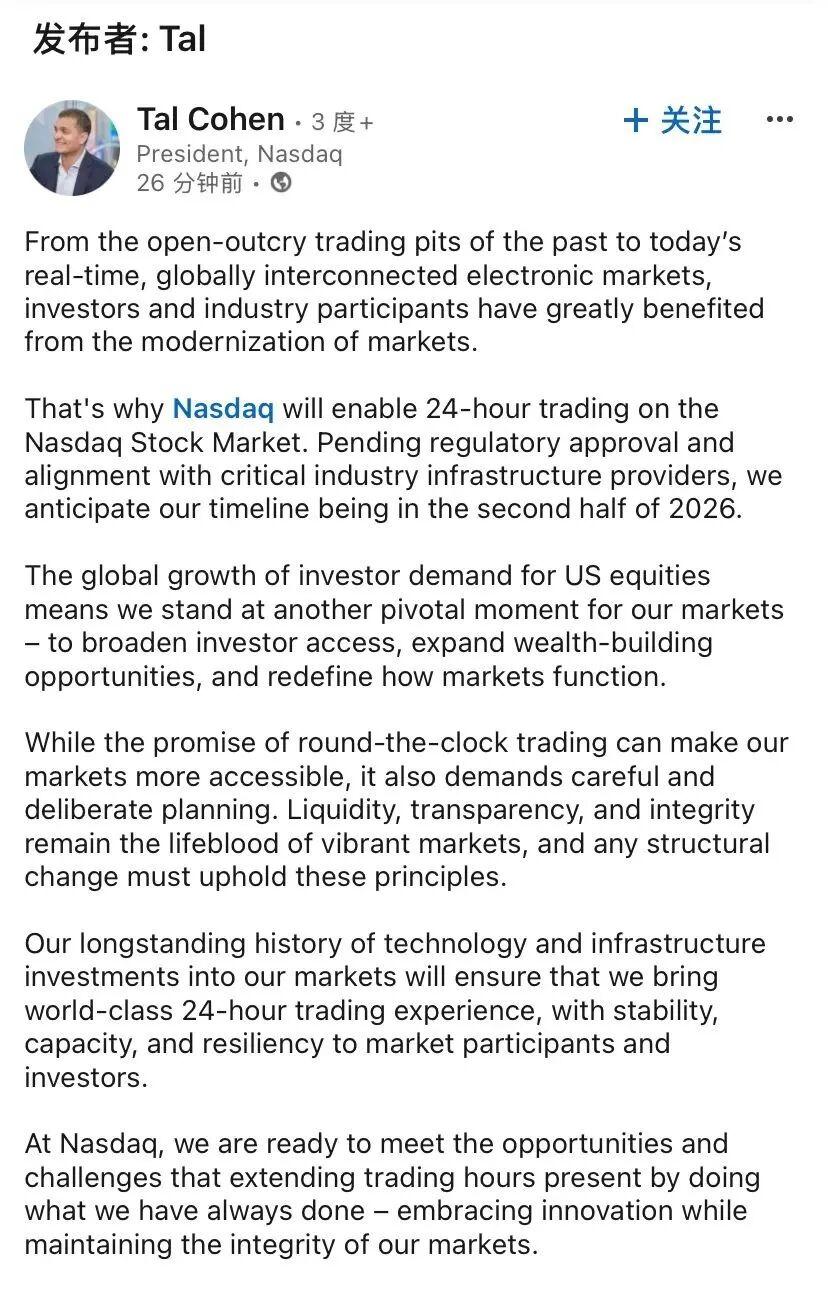

On December 15, Nasdaq filed Form 19 b-4 with the SEC, planning to extend trading hours for U.S. stocks and exchange products .

In short, the goal is to change the trading model to "5 days a week, nearly 23 hours a day". The specific arrangement is: the main trading period is "4:00-20:00 Eastern Time", and an additional night session is added "21:00-4:00 the next day". Trading is suspended from "20:00-21:00" to clear incomplete orders.

This news quickly sparked associations within the Web 3 field, with many believing it was "paving the way for the tokenization of US stocks, enabling stocks to be traded 24/7 like cryptocurrencies."

However, considering the details of the application documents, this interpretation seems more like wishful thinking —this adjustment has no direct connection with "tokenization" at all; it is essentially just an "efficiency upgrade" of the traditional securities trading system.

There are two main reasons:

In terms of content, the entire application document did not mention concepts such as "tokenization" or "blockchain" . All the rules were designed around traditional stocks, ETFs and other instruments. The core objective was very practical - to meet the trading needs of institutional investors in different time zones by extending the trading window, rather than adapting to the trading characteristics of digital assets.

Functionally, the newly opened nighttime trading market is not a "full version" of the market. Many complex order rules (such as algorithmic trading and special settlement terms for block trades) are not applicable during this period, and some risk control functions are also limited. Therefore, the nighttime session is essentially a "time extension" of the traditional trading system, rather than a prelude to the transformation to a "24/7 uninterrupted, full-featured trading" market for digital assets.

The SEC sent a "No Action Letter" to the DTC: a "compliance trial" for tokenization of US stocks, not a "full approval."

What is truly directly related to the tokenization of US stocks is the "No Action Letter" issued by the SEC on December 11 to the DTC (a subsidiary of the American Depositary Receipts Corporation (DTCC) and the core custodian and clearing institution for the US stock market). It's important to clarify that this letter does not constitute a complete approval of tokenization technology; it is merely a regulatory adjustment permission of a "special case" nature.

Why does the DTC need this "license"?

Under current regulations, self-regulatory organizations like the DTC must submit applications to the SEC and wait for lengthy approval processes, which can take up to 240 days, when changing business rules or making significant arrangements. To advance its tokenization pilot program, the DTC applied to the SEC for an exemption from certain procedural reporting obligations during the pilot period . This letter from the SEC essentially grants the DTC a temporary "compliance trial window," meaning that, under certain conditions, enforcement action against its tokenization pilot program can be temporarily suspended.

How was this pilot program designed?

Its core principle is very cautious, which can be summarized in one sentence: focus only on efficiency upgrades, without touching the financial foundation. This aligns with China's approach to blockchain technology applications, which emphasizes "prioritizing technological exploration without altering the core system," and has the following three key points:

1. The token is merely a "record of ownership," not a representation of "stock rights." The pilot program does not use blockchain to replace the existing DTC stock ledger system. It simply provides brokerages with an "additional option"—allowing them to generate an additional "digital token" on the blockchain for a portion of their stock holdings. This token is merely a record of ownership; it is not a stock in itself, does not grant voting rights or dividend rights, and cannot be used to directly buy or sell stocks. The actual stocks remain in the old DTC system.

2. Transaction flow is monitored throughout. Even though these tokens can be transferred peer-to-peer between approved wallets, every transaction is monitored in real time by DTC's off-chain monitoring system (LedgerScan) to ensure that every transaction is traceable throughout.

3. Triple compliance constraints

To avoid risks such as money laundering and asset de-anchoring common in tokenization, this pilot program has set strict constraints:

Scope restrictions : Tokens can only be transferred between wallets of compliant institutions approved by the DTC, and are prohibited from circulating to third parties or individuals who have not completed due diligence/anti-money laundering (KYC/AML) compliance.

Permission constraints : DTC retains the permission to "force transfer or destroy tokens" to deal with risk scenarios such as abnormal transactions and asset de-pegging;

System constraints : The entire tokenization system is completely isolated from the DTC core clearing system to prevent technical or operational risks from being transmitted to the traditional financial system and to safeguard the bottom line of financial stability.

The future of tokenization in US stocks: primarily incremental upgrades, with cross-market collaboration remaining a long and arduous journey.

So, what does the future hold for the tokenization of US stocks?

In summary, it will not be a "revolution that can be accomplished overnight," but rather a "gradual upgrade of infrastructure that works silently and imperceptibly," similar to the gradual logic of "crossing the river by feeling the stones" in China's reform and opening up.

In the short term , the DTC pilot program may begin with a few highly liquid stocks and gradually expand to more stable, standardized, and lower-risk assets such as ETFs and government bonds . However, at this stage, the participants will primarily be professional institutions such as banks and securities firms, with retail users finding it difficult to participate directly. Meanwhile, the SEC will also develop more detailed rules based on data from these pilot programs , such as clarifying information disclosure standards for tokenized assets and standards for the division of custody responsibilities, providing the industry with clearer compliance guidance.

In the long run, the ultimate value of tokenizing US stocks may lie in achieving "cross-market collaboration" —for example, connecting the settlement systems of different markets such as US stocks, Hong Kong stocks, and crypto assets to achieve " one-click global asset allocation." However, to achieve this goal, two core obstacles still need to be overcome:

First, there are differences in global regulatory rules : the EU's MiCA regulations, Hong Kong's virtual asset policies, and the regulatory details of various US states differ significantly, and how to form a coordinated regulatory framework remains a challenge.

Secondly, the security and compatibility of cross-chain technology : Different blockchain networks have significant differences in technical standards and consensus mechanisms. How to achieve secure and efficient cross-chain asset transfer still requires continuous exploration by the industry.

In short, these two hot topics at the end of 2025 are essentially landmark signals that the tokenization of US stocks has moved from "conceptual discussion" to "compliance pilot" . However, this is only the starting point of a long road. There is still a long way to go before the "tokenization of US stocks" can truly change the global capital market landscape.