Coinbase Institutional released its "2026 Crypto Market Outlook," a comprehensive analysis of the key forces that will reshape the crypto economy in the coming year. The report covers the market prospects of BTC, ETH, and SOL, as well as regulatory, market structure, asset tokenization, technological upgrades, and long-term cyclical factors. The report also assesses the four-year Bitcoin cycle, the risks of quantum computing, and the potential impact of major platform upgrades such as the Ethereum Fusaka hard fork and Solana Alpenglow.

Article author and source: Coinbase Institutional

Article compiled by: Chang

Key themes for 2026

1. Drivers and a cautiously optimistic outlook for 2026

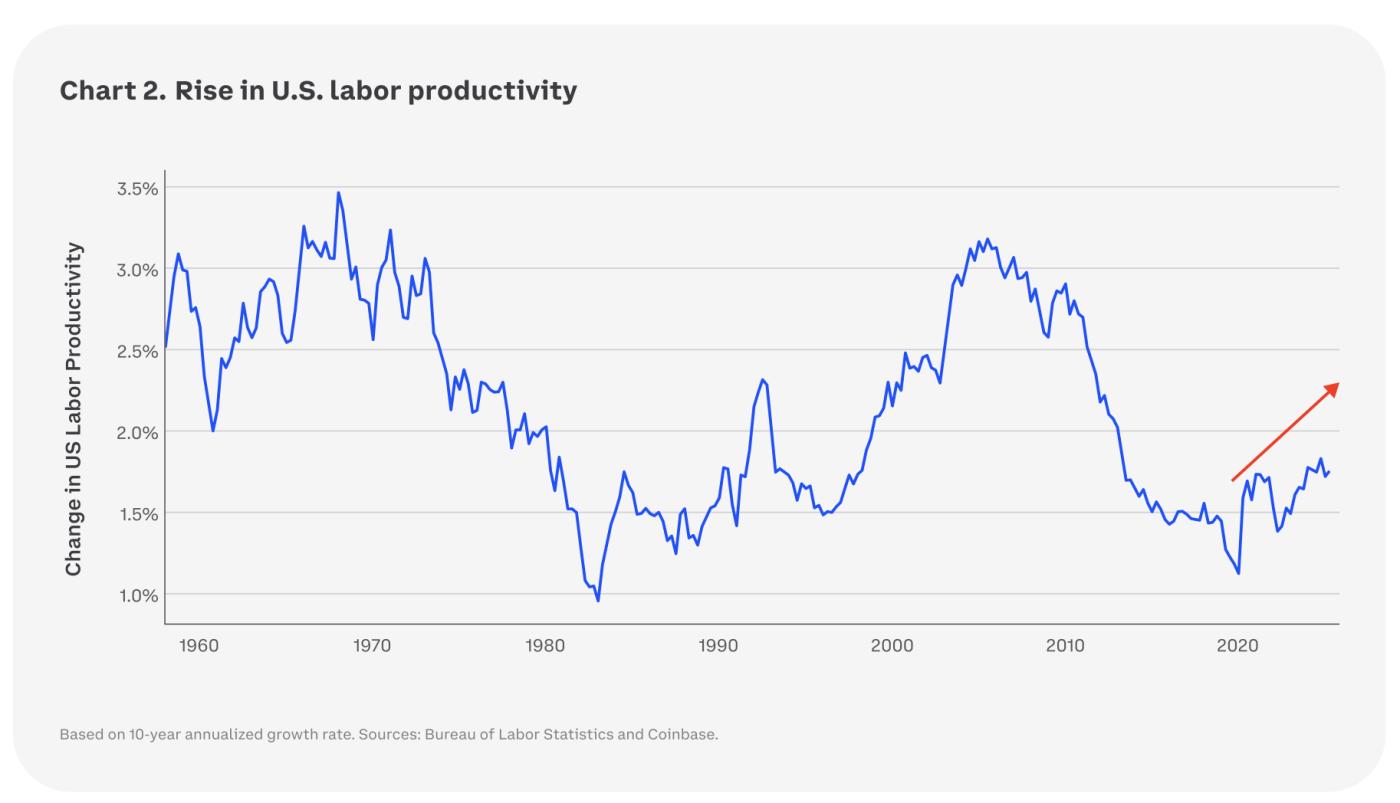

We remain cautiously optimistic about the U.S. economic outlook for 2026. While recent data may suggest an economic slowdown—manifested in widespread price increases and declining employment trends—we believe the U.S. economy is more resilient than many think. In fact, rising labor productivity appears to be a particularly important buffer, stemming from demographic changes and the rise of artificial intelligence.

We believe economists are currently collectively underestimating the productivity of artificial intelligence, partly because AI is improving the speed and efficiency of our workforce in ways not fully captured by official statistics. That said, labor market data is trending towards the lower end of its historical range, but slowing U.S. population growth (including declining immigration) may offset its impact on wages and consumption.

For the market, the key question is whether we are experiencing a boom similar to late 1996: the early stages of transformative technological expansion, or the over-speculation of 1999: a harbinger of a sharp correction. In our view, the economic impact of the current AI boom is likely to be very different from that of the dot-com boom, precisely because lessons have been learned from that period. Therefore, we lean towards the former rather than the latter, but there is no simple answer. This distinction has profound implications for how we navigate the coming year, particularly from the perspective of creative destruction and structural shifts reshaping capital allocation.

A decisive regulatory shift

In the United States, 2025 marked a decisive regulatory shift with the formal enactment of the GENIUS Act, which provides a federal framework for regulating dollar stablecoin issuers, and the CLARITY Act, which passed the House of Representatives with bipartisan support, outlining market structure rules.

The momentum behind these two pieces of legislation underscores a growing consensus among U.S. lawmakers that a clear and unambiguous regulatory environment is crucial for the responsible growth of digital assets and their integration into the broader financial system. Indeed, regulations are key to many crypto themes in 2025 and are likely to continue shaping the market next year.

For example, we anticipate a significant increase in the adoption and sophistication of crypto derivatives, providing investors with new avenues for risk management and price volatility speculation. With reduced regulatory uncertainty, we expect to see accelerated development and deployment of solutions leveraging crypto as the underlying technology for digital payments and on-chain financial transactions. Furthermore, we foresee increased revenue for token holders, potentially through various mechanisms including enhanced staking opportunities or protocol fees allocated to governance token holders.

Furthermore, as governments and financial institutions worldwide move towards clearer and more comprehensive regulatory frameworks, developers will be increasingly able to fully leverage the inherent potential of crypto. Internationally, Europe has fully implemented the Crypto Asset Markets Regulation (MiCA), while policymakers in the Middle East, North Africa, Asia, and Latin America are striving to provide a stable and predictable environment to foster innovation. We believe this combination of regulatory clarity and technological innovation will drive a transformative year for the cryptocurrency market in 2026.

Increased institutional adoption

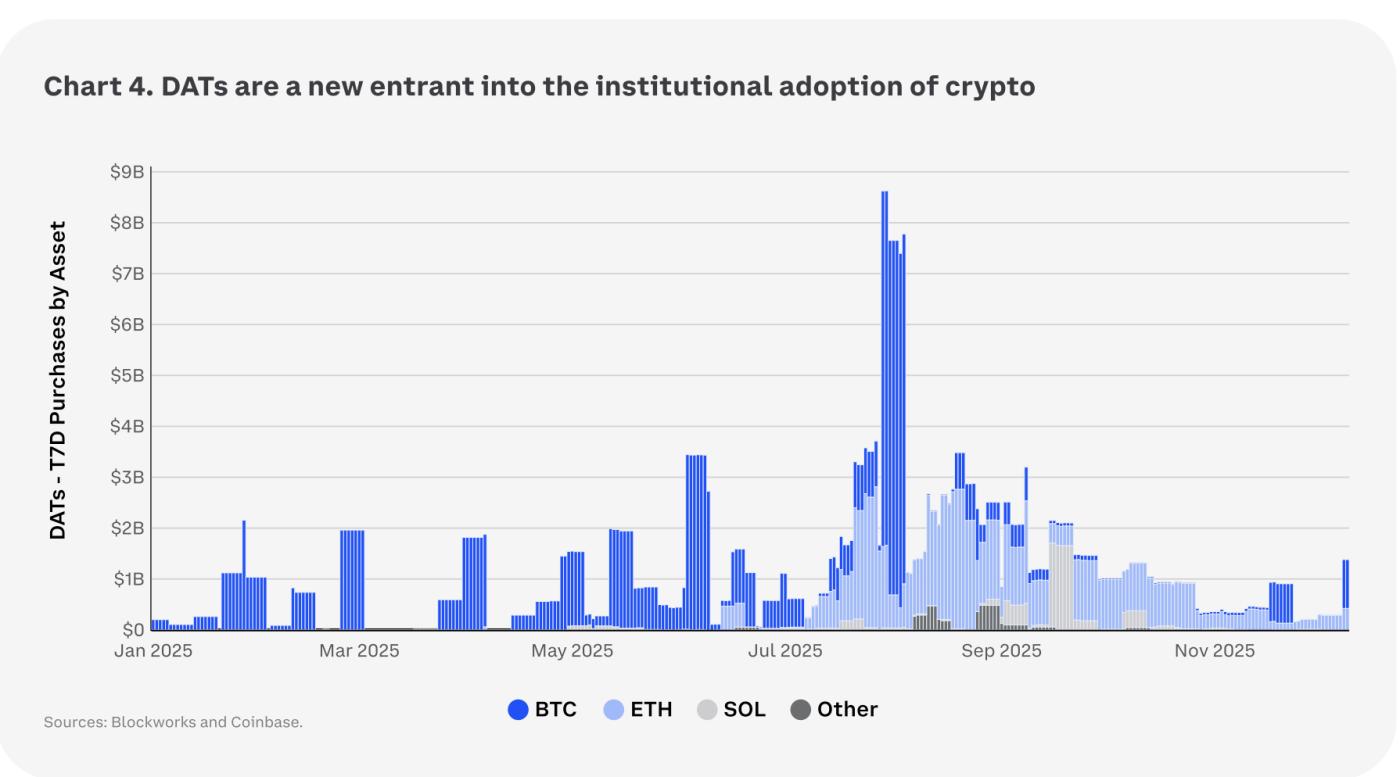

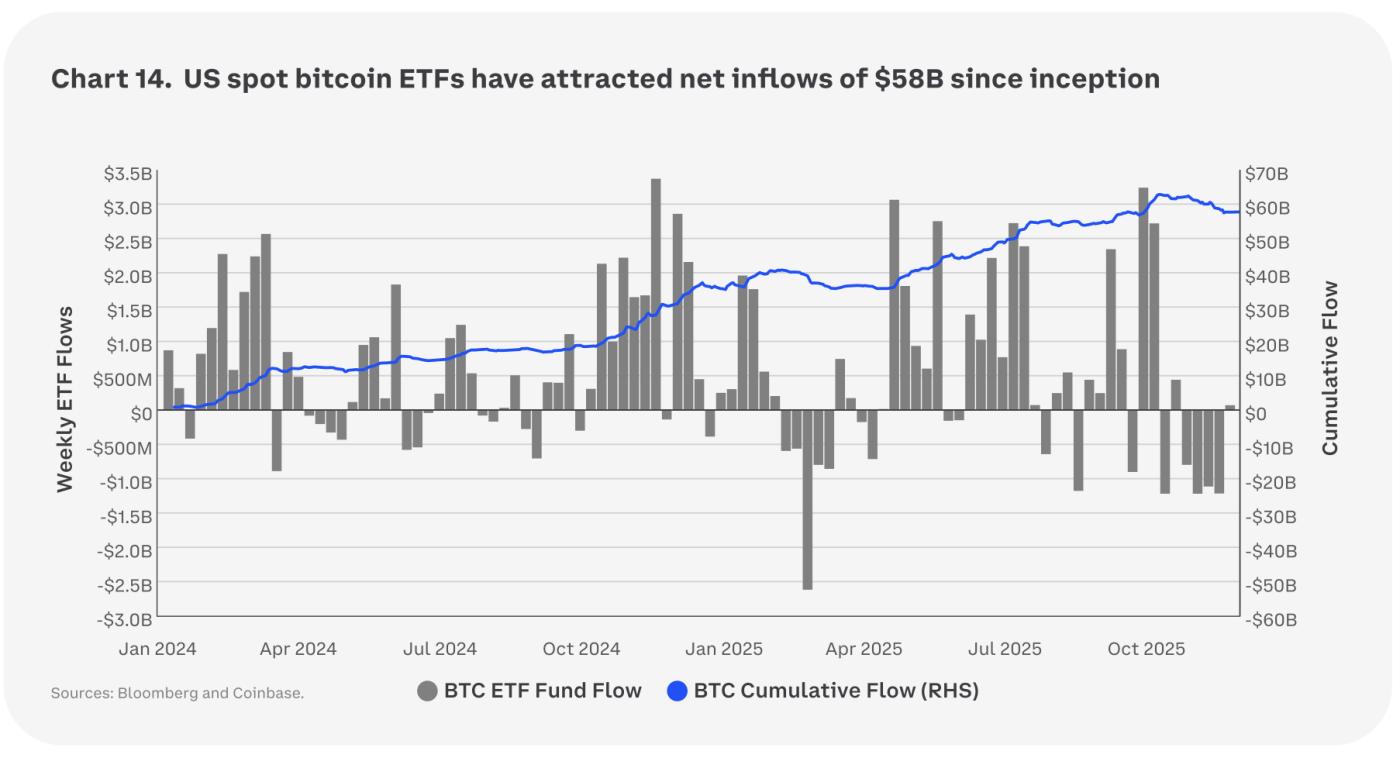

The current market cycle has witnessed unprecedented growth in institutional adoption, the emergence of crypto spot exchange-traded funds (ETFs), and the rise of Digital Asset Treasury (DAT) companies—publicly traded companies that dedicate a significant portion of their balance sheets to holding crypto assets. We expect ETFs to gain further attention following the SEC's approval of general listing standards for certain spot commodity exchange-traded products, including digital assets, thus reducing the need for case-by-case rule changes. In fact, the longest approval timeline for ETFs has already been shortened from 270 days to 75 days.

On the other hand, we believe that DAT is currently undergoing a consolidation phase focused on valuation, which is reflected in the general compression of its mNAV (market capitalization to net asset value) to parity (or in some cases below parity) in the fourth quarter of 2025. These instruments emerged in 2025, partly due to changes in crypto accounting standards that took effect in December 2024. However, the intense and sustained PvP activity in the second half of 2025 resulted in the emergence of clear leaders within the dedicated communities of each token.

In the DAT 2.0 model, we believe future DAT iterations will move beyond simple accumulation, specializing in the professional trading, storage, and acquisition of sovereign blockchain space. This shift is based on the view that blockchain space is a unique commodity and an essential structural input to the digital economy. Therefore, we believe a successful DAT business model will revolve around a deep understanding of the inherent term risks and cyclicality in the blockchain economy. Indeed, looking ahead, clearer regulations are crucial for expanding institutional adoption, and continued developments in the United States are paving the way for this. These advancements are fundamentally changing the landscape of financial markets, enabling broader and more sophisticated applications of blockchain technology.

Tokenized products are increasingly recognized and accepted as eligible collateral in various financial transactions. The integration of stablecoins into delivery-for-payments (DvP) structures significantly improves the efficiency and security of transaction settlement. More and more institutions are recognizing that regulated DeFi platforms not only offer high-yield opportunities but also come equipped with compliance and risk management tools. Such initiatives will encourage greater institutional participation and contribute to building a stronger and more widely available financial infrastructure.

Tokenomics 2.0: Value Capture, Buybacks, and Protocol Gains and Losses

A hallmark of the current crypto cycle is the increasing focus on projects creating tangible value for their token holders. A key feature of this evolution is the growing popularity of token economics models that directly link platform performance to its overall value. Starting in 2025, more projects began implementing mechanisms such as strategic token buybacks. These mechanisms are establishing a clear and direct relationship between the success and adoption of the underlying platform and the economic value of its native token. In our view, this shift towards "financial engineering" in the crypto lifecycle signifies a move towards more mature and sophisticated financial practices found in the traditional finance (TradFi) world.

2. Future Trends and Privacy Needs

Privacy has been a cornerstone of the crypto movement's enduring appeal, as many users still expect the inherent freedom to transact, retain ownership, and transfer value through such assets without institutional authorization. However, the problem lies in the fact that this somewhat contradicts Bitcoin's value proposition, as Bitcoin permanently records every transaction on its network on a public ledger. Indeed, while institutional adoption of crypto has been a major catalyst in the current market cycle, it has also made users of crypto channels more wary of who controls parts of the network.

Furthermore, the growing global awareness of digital surveillance and data utilization has increased the prominence of privacy-first payment solutions. This trend has extended beyond cryptographic mixer services to the development of sophisticated Layer-1 and Layer-2 protocols that embed privacy into their underlying network architecture. Zero-knowledge proofs (ZKPs)—especially zkSNARKs and STARKs—and technologies such as fully homomorphic encryption (FHE) are becoming central to this evolution. ZKPs allow users to prove the validity of transactions without revealing any underlying data, such as the sender, receiver, or amount.

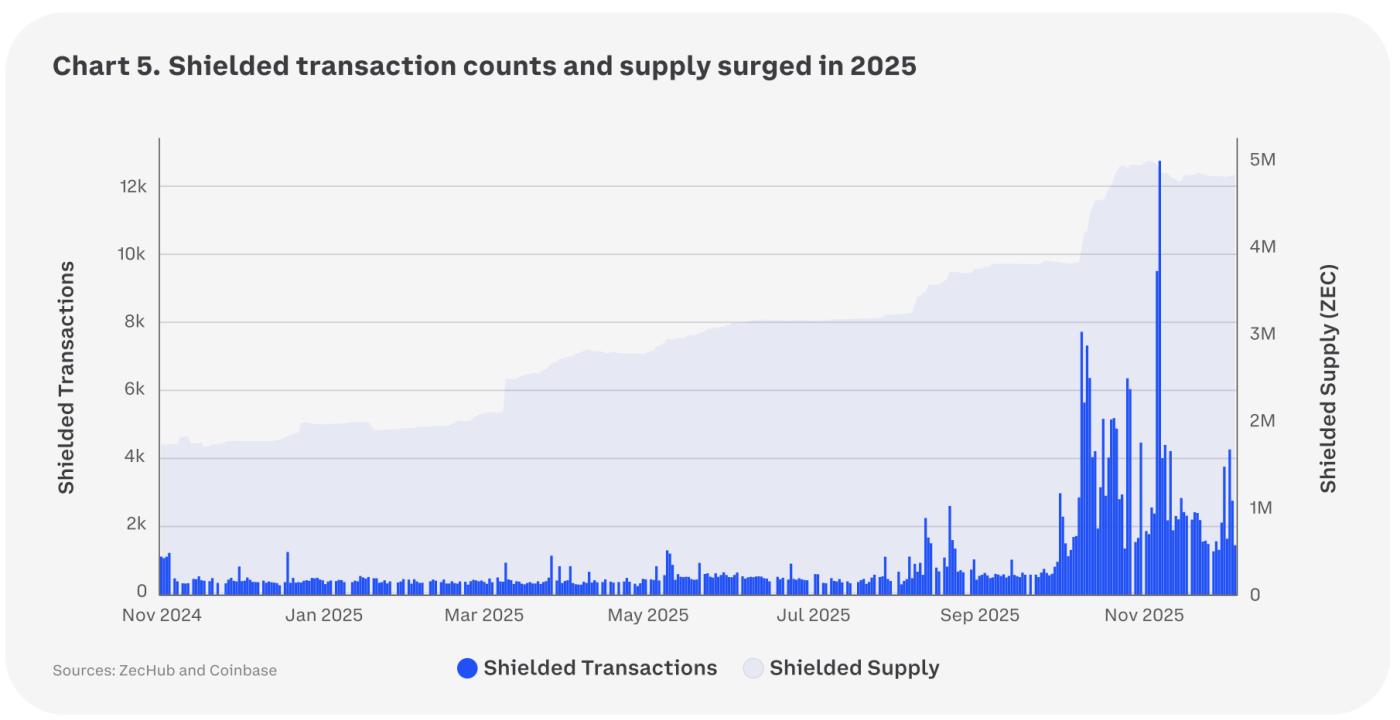

All of this has brought privacy-focused tokens like Monero and Zcash into the public eye, while the Ethereum Foundation has established a new privacy initiative called the "Privacy Cluster" to strengthen privacy within its ecosystem. Some investors believe that this topic will continue to grow before the EU implements stricter KYC and transaction monitoring rules, even though the EU will ban privacy coins and anonymous or self-custodied crypto wallets starting in July 2027.

However, price movements in this sector have also been supported by a significant surge in on-chain privacy usage. The number of shielded transactions has recently reached a new cyclical high, indicating that not only is more value being deposited into privacy pools, but it is also being actively used for transactions. The demand for privacy comes from both professionals and individuals: institutions and professional retail traders need confidentiality to prevent competitors from exploiting their strategies, while everyday users are generally reluctant to expose their full financial history on the blockchain. We believe this trend is likely to expand in the coming years as crypto sees wider adoption.

AI x Encryption is dead, AI x Encryption lives on.

Reports of the demise of the "AI x Crypto" theme have been greatly exaggerated. However, this theme has undergone several iterations over the past two to three years. Back in June 2023, when we first wrote about the intersection of AI and crypto, we discussed how blockchain could address the data and computing resource demands of generative AI by enabling decentralized data markets and networks of shared computing power (potentially through token incentives). We explored the opportunities presented by Worldcoin's "proof of humanity" system to combat the risks of misinformation and economic harm posed by increasingly realistic online bots.

In late 2024 and early 2025, AI agents emerged as a revolutionary topic, not only in the crypto space but also in the broader technology sector. Autonomous entities may eventually be able to manage assets, execute transactions, and perform complex governance functions by analyzing market news feeds and other external data. Adopting internet-native payment protocols like x402 could be a key step, enabling these systems to continuously settle large volumes of microtransactions without human intervention, potentially giving rise to new forms of online commerce. Indeed, as AI systems become more autonomous and transact with each other, we believe traditional financial systems may prove too slow, too costly, or geographically limited.

Furthermore, this intelligent agent tool also means that AI agents may be poised to revolutionize on-chain development, potentially allowing non-technical founders to launch businesses in hours or days instead of months or years. This accelerated timeline can be achieved through intelligent agents that write smart contract code, perform security reviews, and monitor ongoing risks. In other words, AI agents have the potential to catalyze a wave of innovation, potentially leading to the expansion of new on-chain applications and substantial improvements in user experience.

Therefore, despite the convoluted and evolving narrative, we see the continued prominence of the convergence of AI and cryptography not merely as a trend, but as a fundamental shift toward the next stage of technological advancement: a phase that delivers more transparent and democratic intelligent systems.

What is the end result of application-specific blockchains?

The proliferation of specialized blockchain networks—including L2, standalone L1, and application-specific chains—is rapidly reshaping the competitive landscape of crypto infrastructure. For example, platforms like Arc (built by Circle) are specifically designed to be the best, most compliant home for USDC-centric institutional use cases; while networks like Tempo (incubated by Stripe and Paradigm) focus on bridging institutional-grade payment channels, aiming to capture the massive cross-border commerce market. Projects like Canton are building private, permissioned environments specifically designed to unlock trillions of dollars in institutional capital locked up by asset tokenization and securities trading.

The resulting fragmentation is not random, but rather a strategic response to the fundamental reluctance of major institutional players to outsource their core business logic to competitor platforms. The core argument appears to be strategic control. Companies launch their own chains to maintain sovereignty over their data, their regulatory compliance environment, and the financial value accumulated from their network effects. In the short term, this trend is likely to accelerate further as these players continue to launch dedicated chains to capture high-value, regulated cash flows: prioritizing custom governance, fee structures, privacy controls, and compliance features over shared infrastructure.

However, we believe the end goal is not endless silos, but a “network of networks” architecture where these dedicated chains become highly composable through advanced interoperability layers such as native cross-chain messaging, shared security via staking/re-staking, and privacy-preserving bridges. The winners will be those who balance vertical optimization with seamless horizontal connectivity: achieving atomic multi-chain settlement, unified liquidity pools, and synchronized real-world assets, while laggards risk isolation in a market that increasingly rewards fluid, institutional-grade capital flows across compliant domains.

Another step forward in tokenization

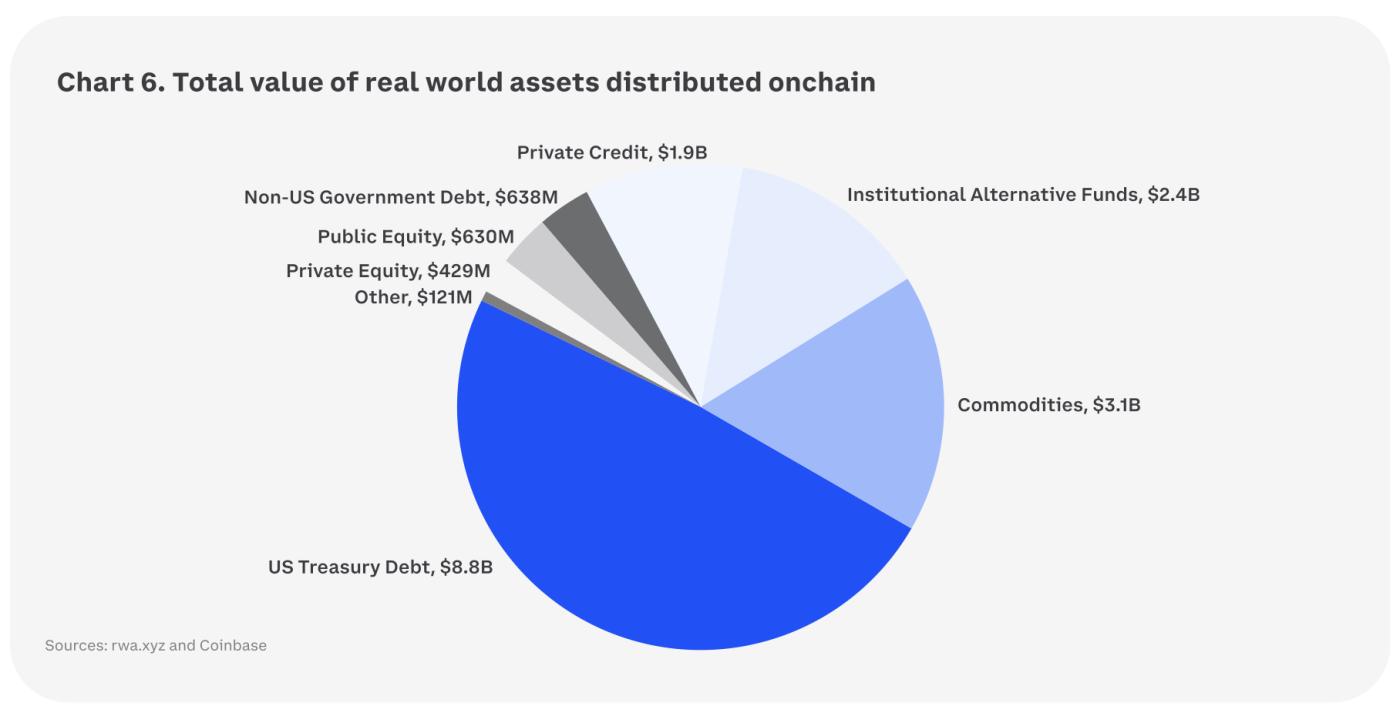

The booming trend of tokenized real-world assets (RWA) gained significant attention in 2025, with even major financial players like Nasdaq submitting a proposed rule change to the U.S. SEC to allow the trading and settlement of tokenized stocks and ETFs on its market.

In other words, most tokenized equity products currently in circulation do not offer direct ownership of shares; they are equity-linked notes or other derivatives, and many issuers construct distribution structures that are defined by Reg S to be aimed at offshore buyers rather than the U.S. market.

From the buyer's perspective, the appeal of tokenized stocks goes beyond 24/7 accessibility—it offers greater capital efficiency and atomic composability. Unlike traditional assets, the near-instant settlement of tokenized stocks enables rapid transfers across various decentralized finance (DeFi) platforms, significantly reducing idle capital and simplifying transfer processes that typically take days in traditional systems.

The net effect may be structurally superior to traditional finance. For example, compared to traditional margin frameworks (typically limited to around half the portfolio value), DeFi lending markets typically offer significantly higher loan-to-value ratio thresholds (75-80%) for high-quality crypto collateral. This difference in capital efficiency, coupled with programmable settlement, is what attracts institutional interest and innovation to these channels, whether platforms tend to build walled gardens or embrace greater transferability.

3. Composability of Crypto Derivatives in Emerging Markets

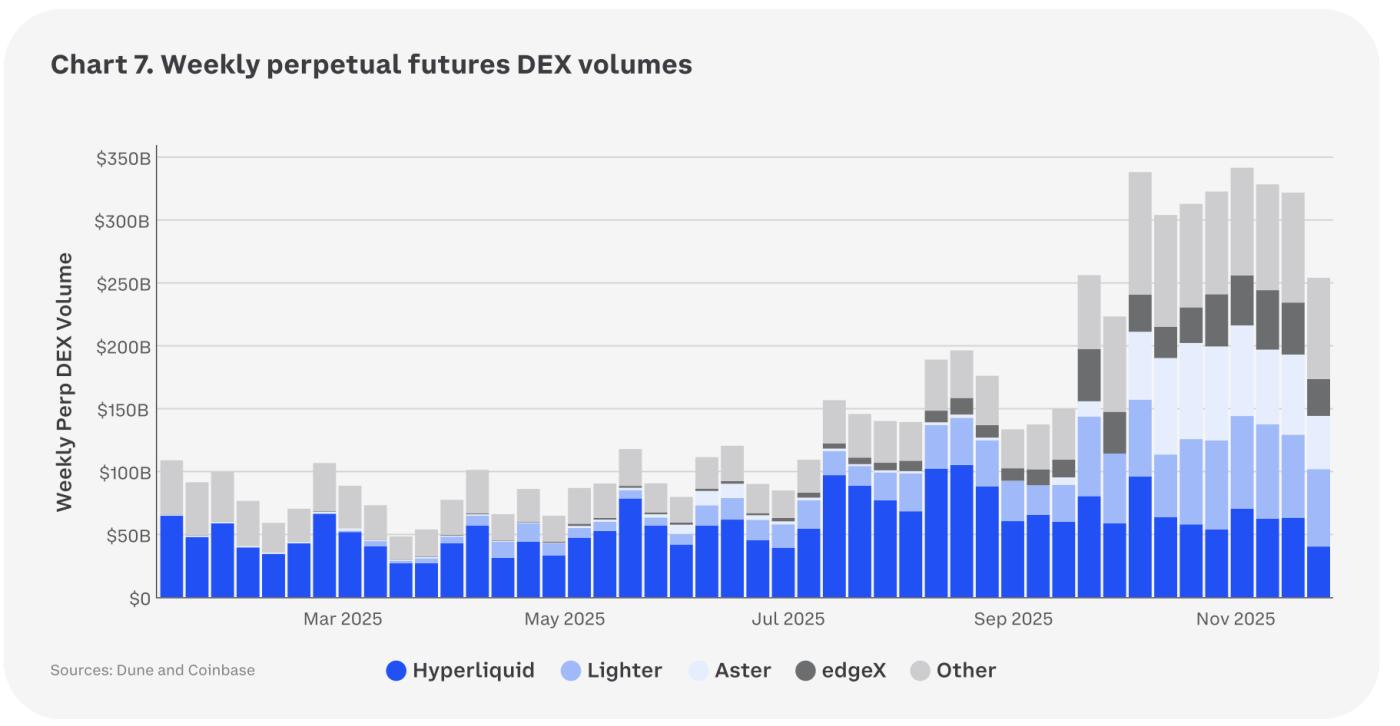

The surge in crypto derivatives in 2025, primarily perpetual futures (perps) but also including options, hints at a mainstreaming trend that could ultimately lead to their integration as a pillar of the global financial system. This is mainly driven by the rise of high-throughput decentralized exchanges (DEXs), followed by the increase in regulated U.S. trading venues. For example, by the end of 2025, DEXs were processing over $1.2 trillion in perpetual futures trading volume monthly, with Hyperliquid still holding a significant share of the market.

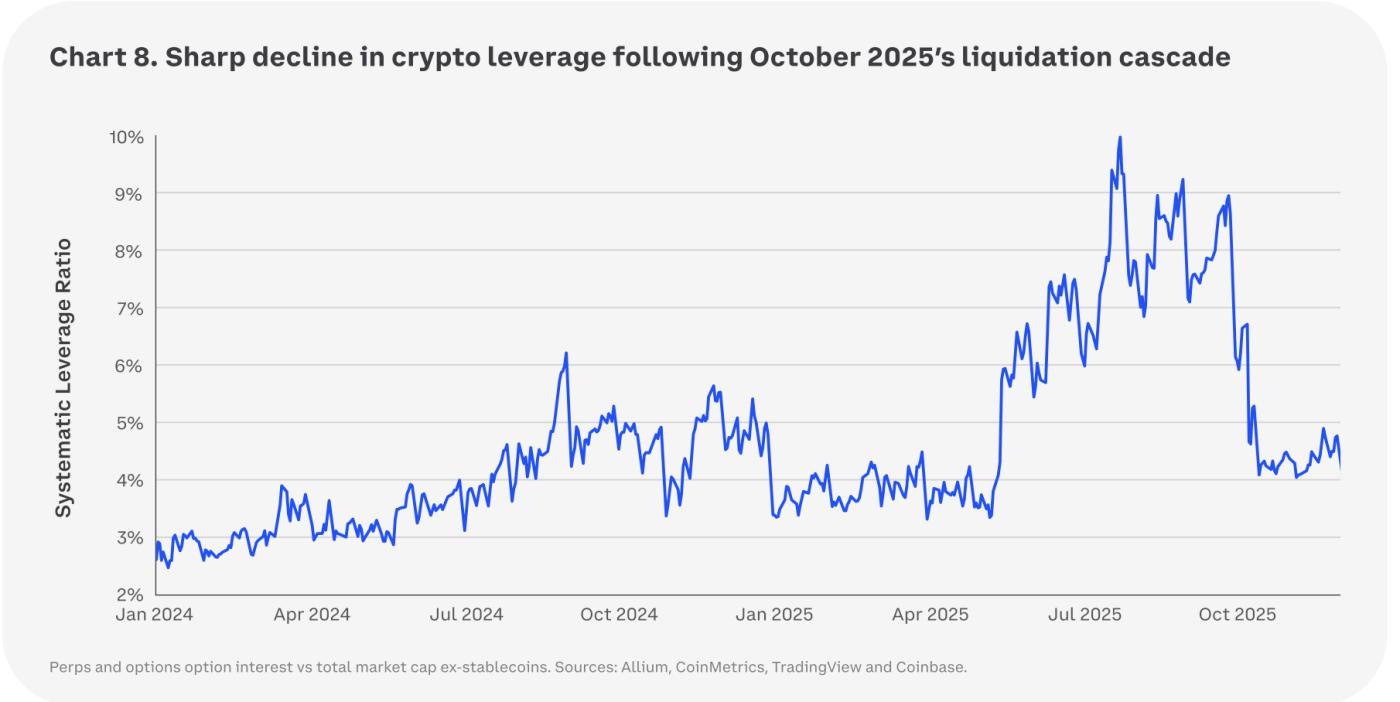

One possible theory driving this activity is that, in the absence of a traditional Altcoin season, many market participants have turned to perpetual futures as a means of generating excess returns. The unprecedented level of leverage offered by perpetual futures allows traders to amplify their exposure and potential profits (or losses) with a small amount of capital. We believe this appeal is particularly strong given the relative stagnation of the Altcoin spot market over the past year. That said, our systemic leverage ratio suggests that crypto instruments had nearly 10% purely speculative exposure (i.e., directional bets only, excluding hedging) at their peak in 2025, before the liquidation waterfall in October 2025 reduced it to 4%.

Nevertheless, we believe perpetual futures are transcending high-leverage trading instruments to become a core, composable primitive tool within the DeFi market. This integration has the potential to unlock significant new areas of capital efficiency through integration with other DeFi primitives such as lending protocols. For example, such integrations could allow perpetual futures to be used in a wider range of strategies, such as providing a dynamic hedging layer for liquidity pools, serving as the basis for interest rate products, or acting as collateral in lending protocols with variable risk parameters. This composability creates a synergistic trading environment that allows market participants to hedge market risk while earning passive returns on assets.

Furthermore, we see a number of strong factors positioning perpetual equity futures as the next major retail trading instrument. As global retail participation in U.S. equities continues its long-term upward trend, the market is facing disruption from tokenized equities. Combining the 24/7 accessibility, censorship resistance, and capital efficiency of crypto derivatives with high demand for exposure to major global equities such as those on the S&P 500 or Nasdaq, perpetual equity futures could become the go-to option for a new generation of global retail traders seeking highly leveraged, low-friction access to traditional financial markets. These innovative derivatives promise to transform how equities are traded outside of traditional market hours, particularly on weekends and at night.

Essentially, perpetual futures are moving from the periphery of crypto trading to the core of composable DeFi, while simultaneously preparing for a new wave of global retail capital seeking more efficient exposure to traditional assets.

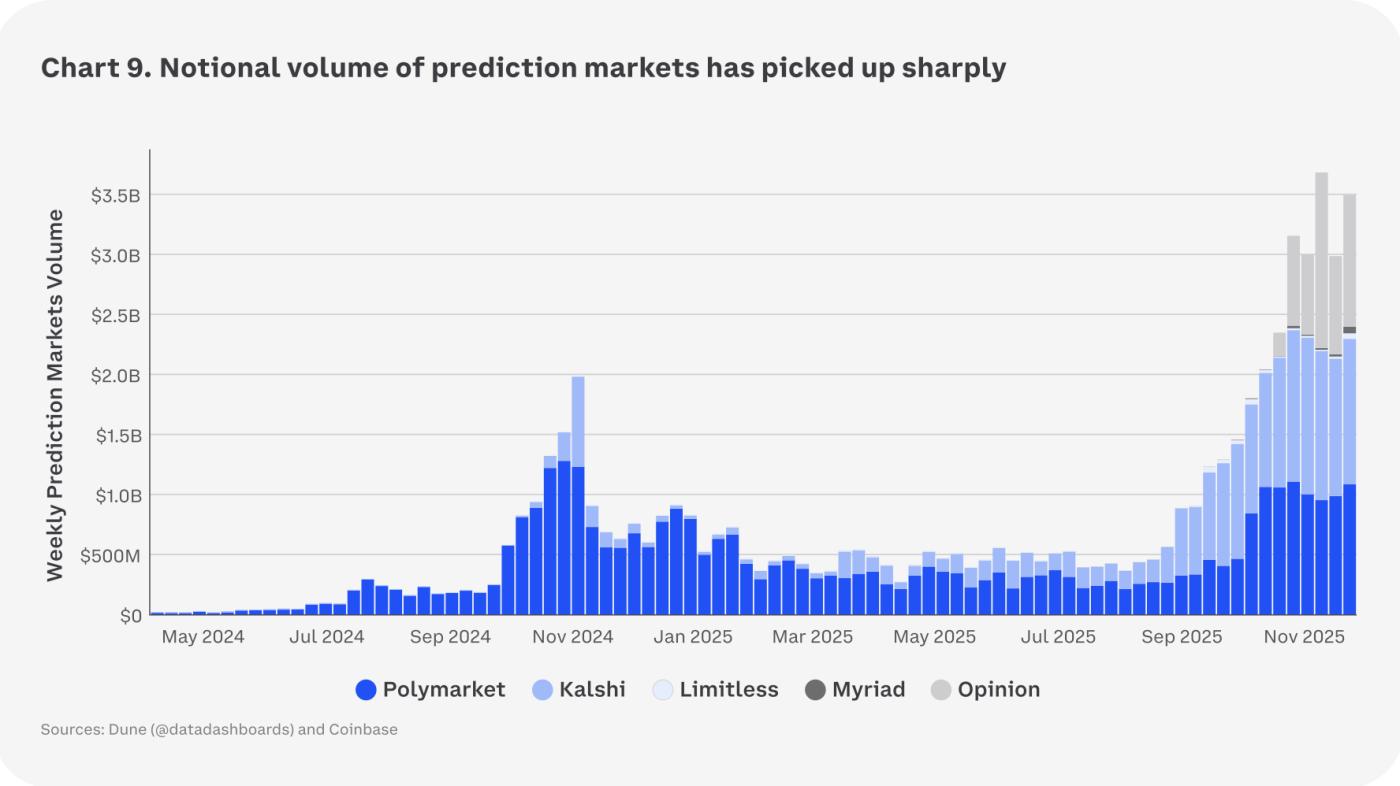

High-risk games of prediction markets

One of our major predictions in our 2025 Crypto Market Outlook was that prediction markets would continue to grow following the 2024 US election, contrary to the consensus view that trading volume would decrease after the election. At that time, we believed that prediction markets utilizing blockchain channels had already demonstrated significant advantages over non-blockchain variants, such as decentralized dispute resolution and outcome-based automated settlement. Since then, prediction markets have expanded into areas such as sports, economics, and entertainment, and as we predicted, this opportunity is poised to gain traction in 2026.

Starting in 2026, a provision in the One Big Beautiful Bill Act (signed in July 2025) will reduce the deductibility limit for gambling losses on winnings from 100% to 90%. While this change may seem harmless, it could result in taxpayers still having to pay taxes on "illusory" income even if the actual profit is small or there is a net loss. Therefore, prediction markets utilizing financial contracts similar to derivatives could become a more tax-advantaged alternative to traditional sports betting and casinos.

However, the proliferation of prediction market platforms could also lead to market fragmentation, reminiscent of the "DeFi Summer," when a plethora of new decentralized finance protocols emerged. This could foreshadow the rise of prediction market aggregators, which could become the dominant interface layer in the space. By connecting to major prediction market protocols through smart contract interfaces and APIs, aggregators will help consolidate billions of dollars in fragmented weekly trading volume and provide users with a unified, real-time view of event odds.

Looking ahead, we anticipate a period of transformation for forecasting markets in the coming years, with the potential for greater size and liquidity, potentially elevating their utility from niche speculative instruments to valuable markets offering insights into future events. This could drive further maturation in their market structure, governance, and regulatory oversight, solidifying their role within the broader financial ecosystem.

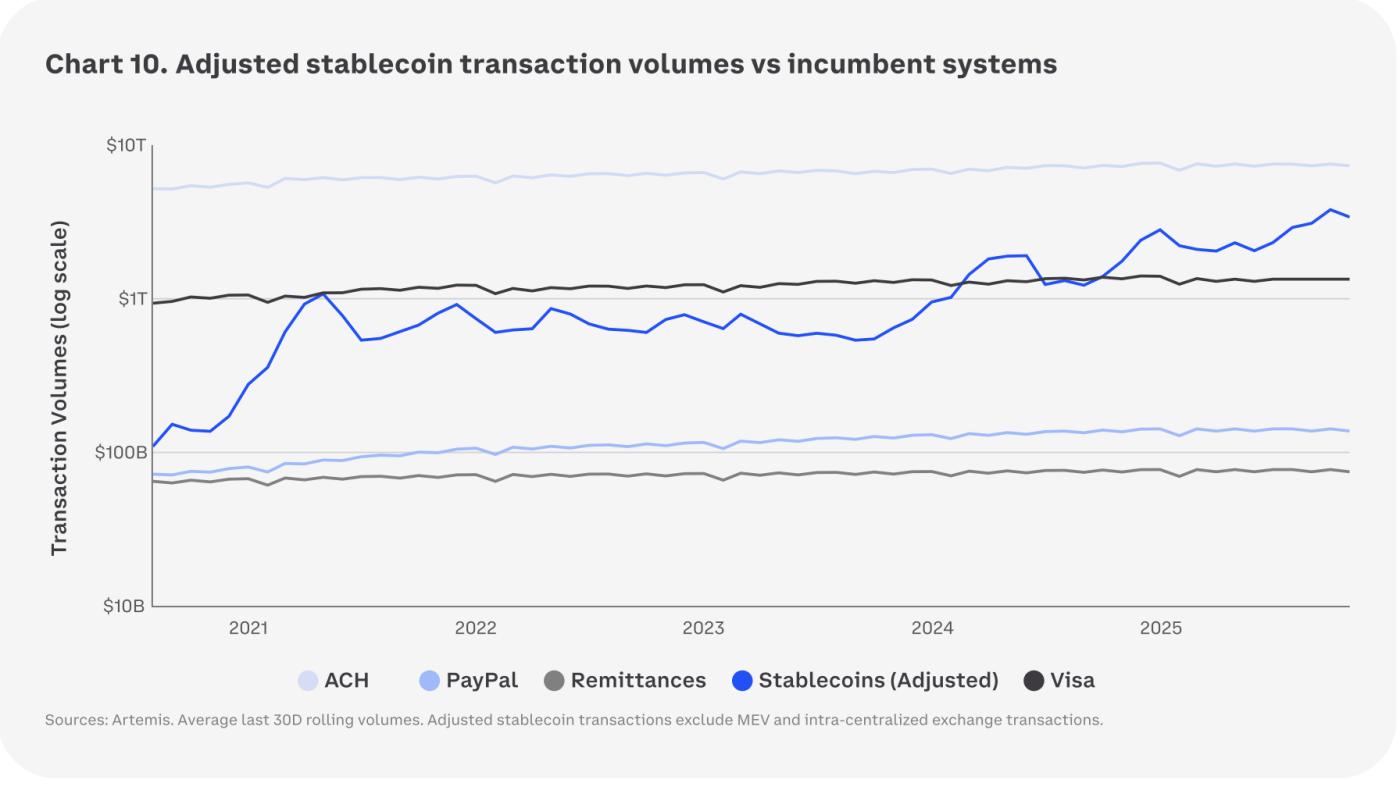

Stablecoins and payment speed

Stablecoins have solidified their position as the primary use case in the crypto ecosystem. This assertion is no longer speculation for the future, but a reality today. For years, industry analysts have argued that stablecoins, digital currencies pegged to stable assets like the US dollar, represent the true "killer application" for mainstream adoption of blockchain technology. However, with increased regulatory clarity, more traditional players are beginning to recognize their practical utility.

Our stochastic model predicts that the total market capitalization of stablecoins could reach around $1.2 trillion by the end of 2028. This projection reflects a combination of anticipated regulatory clarity, continued innovation in underlying blockchain infrastructure, and increasing institutional adoption of digital assets. Ultimately, these factors will drive the continued growth of stablecoins in cross-border transaction settlement, remittance, and payroll payment platforms, while their traditional utility in speculative trading and DeFi will remain.

In fact, we believe stablecoins may see massive expansion as a medium of exchange, driven by innovative protocols like x402, an open payment protocol developed by Coinbase that enables instant on-chain payments for online services. This protocol is specifically designed to enable a completely new economic model for the internet: truly scalable micropayments. It allows service providers to charge a fraction of a cent for accessing digital content, a single API call, or specific computing resources, potentially transforming the way internet services are monetized and consumed.

2 Bitcoin

Market Outlook

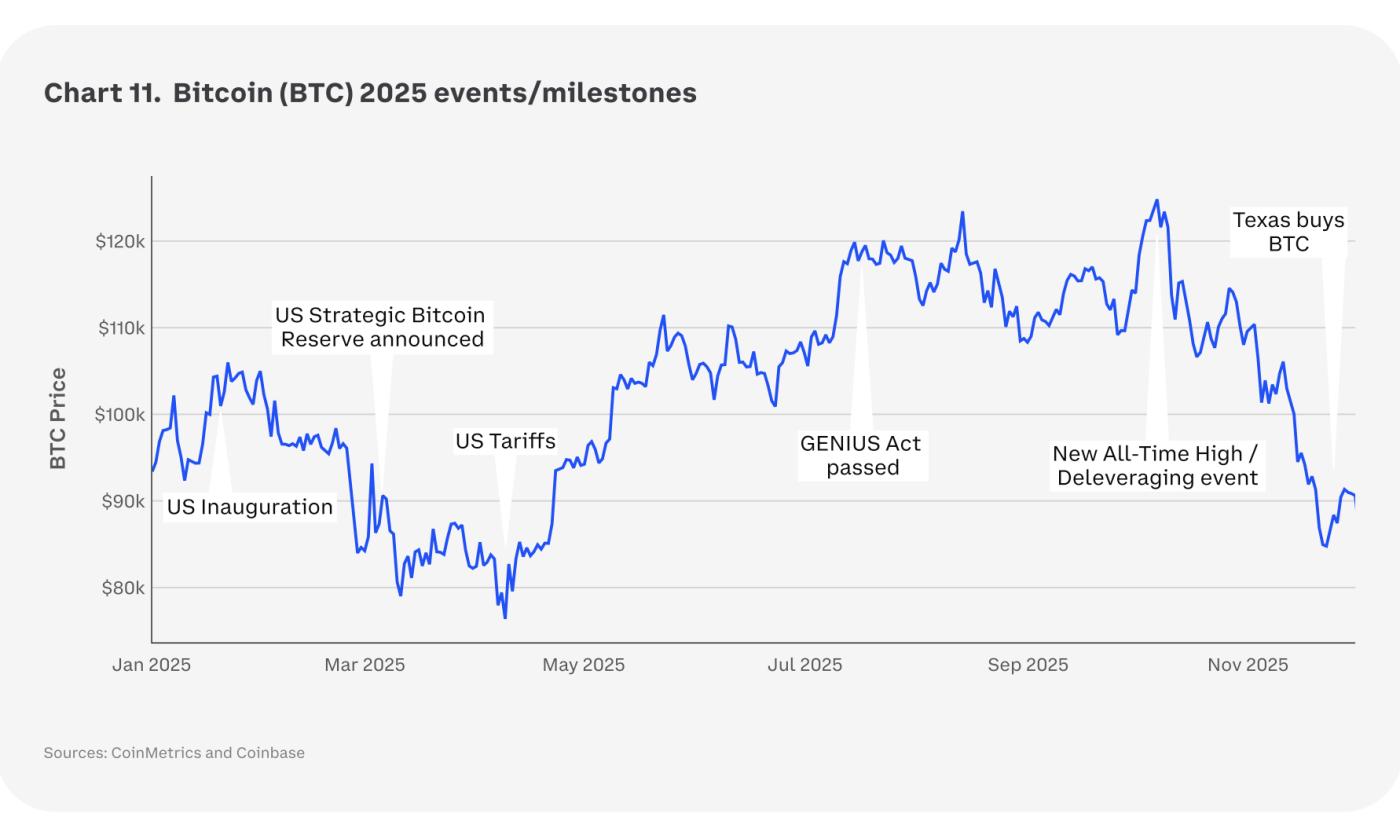

In 2025, Bitcoin experienced a period of relatively mild volatility and evolving market dynamics, continuing the trends observed in previous years. The token continued to solidify its position as a safe haven among assets, but also navigated a complex landscape of regulatory developments, technological advancements, and macroeconomic changes. Nevertheless, Bitcoin has been firmly established as a key component of the global financial discourse, despite still being subject to the evolving nature of a nascent but maturing asset class.

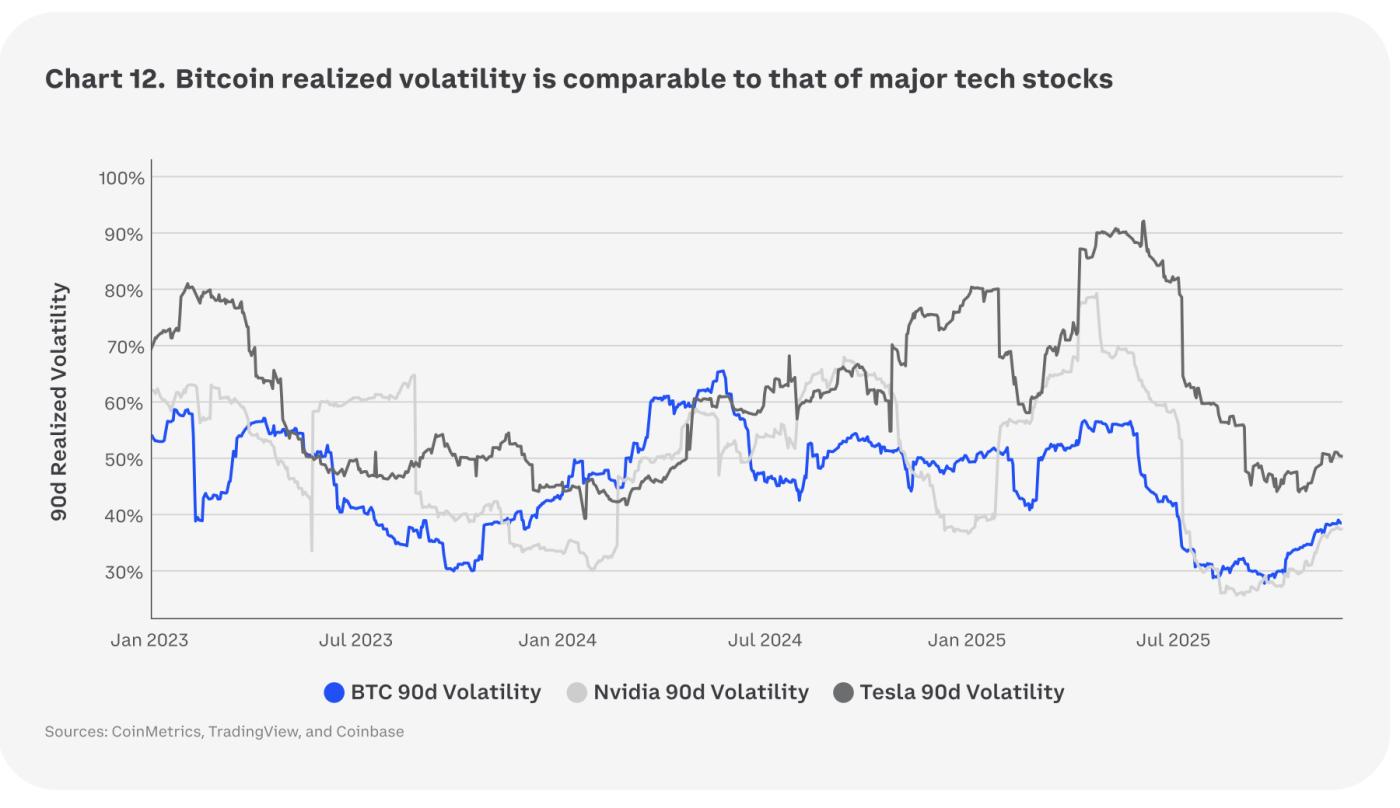

It's worth noting that Bitcoin's volatility is no longer an outlier among investment assets; it's now on par with major high-growth tech stocks. For example, its 90-day historical volatility hovers around 35-40% as of the end of 2025. Regulatory scrutiny is intensifying in several key markets, with governments grappling with how best to integrate digital assets into existing financial frameworks. This has resulted in a patchwork of regulations, creating some uncertainty for investors and businesses operating in the crypto space. Furthermore, macroeconomic factors, such as central bank interest rate adjustments and concerns about global economic growth, cyclically influence investor sentiment across all risk assets, including Bitcoin.

From a technical perspective, Bitcoin's underlying infrastructure continued to advance in 2025. Layer 2 solutions, such as the Lightning Network, gained further attention, improving transaction speed and reducing costs, which enhanced Bitcoin's usability in everyday payments. Advances in privacy-enhancing technologies and multi-signature solutions also addressed some long-standing concerns about security and fungibility. The 2024 halving event continued to have an impact, with analysts gradually beginning to incorporate reduced supply pressure into their price models.

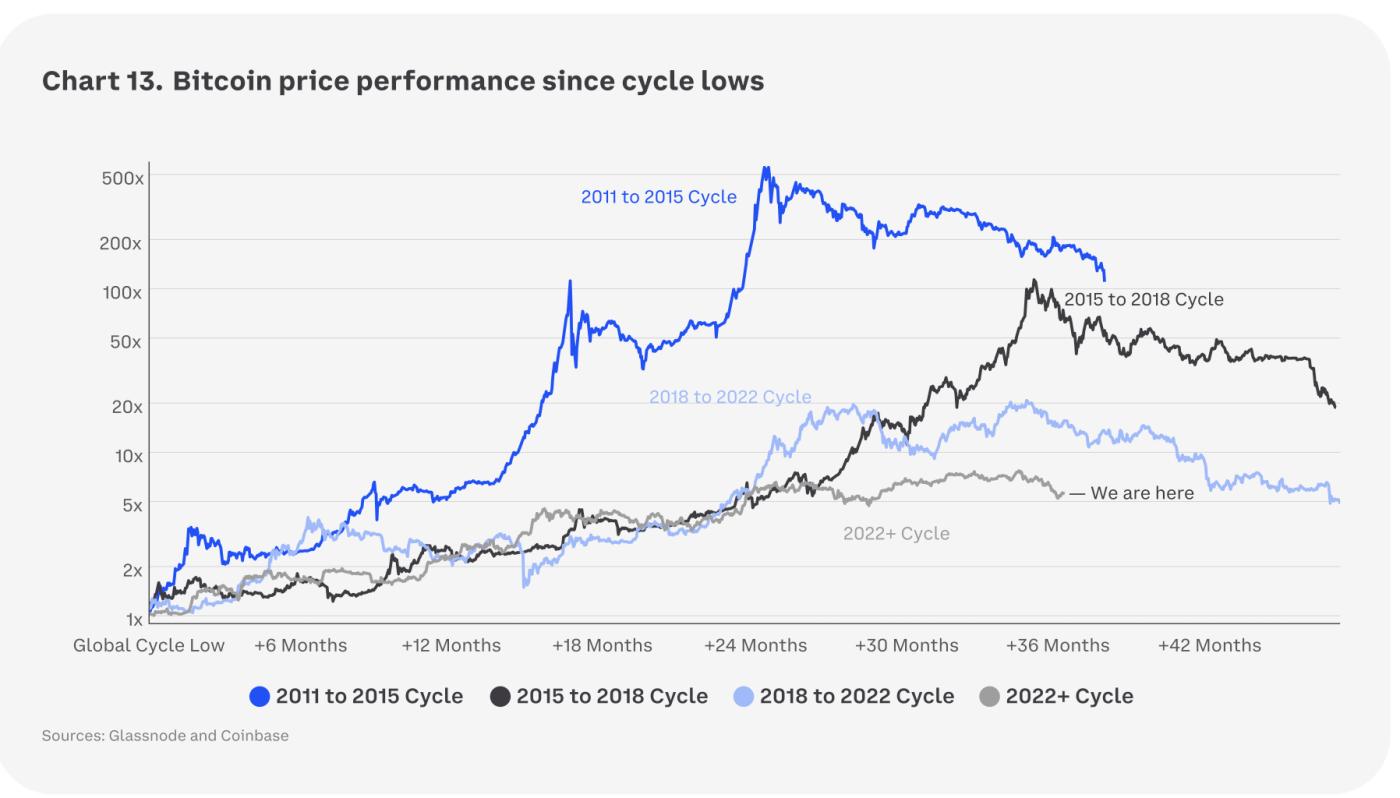

Is the four-year cycle still valid?

Bitcoin's price action in 2025 was somewhat awkward for the token's narrative, as asset classes like US stocks and gold outperformed crypto assets on a risk-adjusted basis, fueling assertions that Bitcoin might be nearing a classic cycle peak. The concept of a four-year cycle has long been a cornerstone of the Bitcoin market discourse, largely influenced by Bitcoin's procedural reduction of block rewards for miners (known as "halvings," which occur every 210,000 blocks).

This pattern has become very important from a behavioral trading perspective due to its success in predicting local market peaks and troughs.

However, we believe the economic relevance of Bitcoin block reward halvings is somewhat dubious. With only four halving events recorded in Bitcoin's history, real evidence on how the market reacts to these milestones remains limited.

Specifically, the challenge in determining the statistical significance of these events lies in the difficulty of separating the unique nature of halvings from external factors such as global liquidity, interest rates, and changes in the multilateral dollar index. For example, previous Bitcoin halvings have coincided with significant historical monetary and fiscal developments.

In 2012, the Federal Reserve began purchasing mortgage-backed securities and long-term Treasury bonds as part of QE3. In 2016, Brexit likely exacerbated fiscal concerns in the UK and Europe, providing a catalyst for Bitcoin purchases. In 2020, global central banks and governments responded to the COVID-19 pandemic with unprecedented stimulus measures, driving a sharp increase in liquidity. Separating Bitcoin price movements from changes in these factors helps to clarify the situation, but apart from the third halving, the evidence for whether these halving events, apart from the third halving, support or undermine Bitcoin price movements is not entirely clear.

Furthermore, we believe that this historical framework has become less relevant to understanding Bitcoin's performance due to a host of new factors fundamentally reshaping its demand and market dynamics. Traditionally, Bitcoin's price movements have often been analyzed through early adoption cycles and retail investor sentiment. For example, miners used to be a significant source of indiscriminate selling pressure to cover operating costs. However, as the landscape has evolved, their influence on overall market dynamics has significantly diminished.

One of the most impactful changes is the increase in institutional adoption. Major financial institutions, including asset management firms, hedge funds, and even some traditional banks, are now actively participating in the Bitcoin market. Even in 2025, publicly traded companies (i.e., DATs or Digital Asset Treasurys) began adding Bitcoin to their balance sheets on a massive scale. This new category of "bigger players," with their substantial financial resources and long-term investment strategies, now has a greater influence on market sentiment and price movements, effectively dwarfing the cumulative impact of miner sell-offs.

This influx of sophisticated capital has also brought a different set of investment objectives, risk management strategies, and long-term perspectives compared to individual retail investors. Institutional investors typically view Bitcoin as a hedge against excessive money supply creation or as a diversification asset in their broader portfolios, which we believe contributes to a more stable and less volatile demand profile over time. In short, institutional commitment tends to lead to larger, more sustained investments rather than speculative short-term trading.

Overall, increased accessibility to Bitcoin, through regulated exchanges, investment vehicles such as ETFs, and user-friendly platforms, has played a key role in expanding the appeal of crypto. These new demand drivers have collectively contributed to a more mature and complex Bitcoin market, rendering historical frameworks that may not have taken into account these evolving dynamics less effective in predicting future performance.

Definition of the quantum threat problem

Bitcoin's long-term security may be entering a new phase, even as advances in quantum computing advance, even if the "quantum threat" is not imminent. Indeed, investors are increasingly concerned that the risks of quantum computing may be approaching sooner than previously thought. This is highlighted, for example, by BlackRock in its revised prospectus for the iShares Bitcoin Trust ETF (IBIT) (filed May 9, 2025), while US and EU agencies have been guiding the migration of critical infrastructure to post-quantum cryptography (PQC) by the end of 2035.

The reality is that quantum computing promises to solve some of the world's most complex problems—from medical discoveries to climate modeling. But it also requires upgrades to many of the cryptographic systems we rely on today. Traditional finance may be one of the hardest hit sectors due to its reliance on closed systems, but open protocols like Bitcoin and Ethereum are also actively preparing.

The core risk emerges on "Q Day," when cryptographically correlated quantum computers (CRQCs) could potentially run the Shor and Grover algorithms, thereby breaking Bitcoin's cryptographic signatures. In other words, Bitcoin's security relies primarily on two cryptographic pillars: the Elliptic Curve Digital Signature Algorithm (ECDSA) used for transaction signing and SHA-256 used for the proof-of-work mining process. This means that quantum computers effectively pose two separate threats. They could potentially break the cryptographic security of private keys, allowing attackers to steal funds from vulnerable addresses; they could also mine blocks more efficiently, undermining Bitcoin's economic and security model.

In other words, given the scalability limitations, we believe that quantum mining itself is currently a lower priority issue, making signature migration the core problem. In fact, the first threat has two dimensions: "remote attacks" targeting outputs where the public key is already exposed on-chain, and "short-range attacks" that could preempt transactions when the public key appears in the mempool.

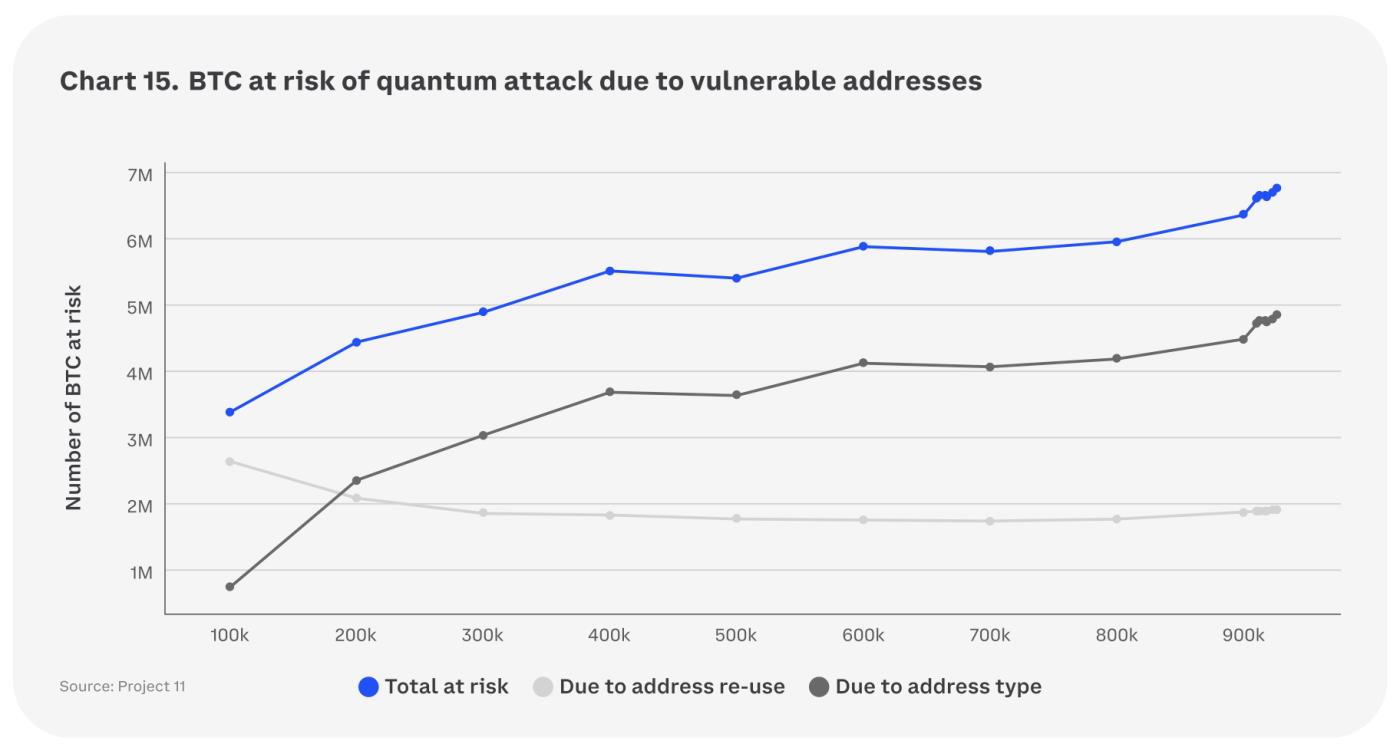

As of block 900,000, approximately 6.51 million BTC—about 32.7% of the total supply—appear vulnerable to remote quantum attacks, primarily due to address reuse and the types of scripts that expose public keys on-chain. These include "pay to public key" (P2PK), naked multisignature (P2MS), and Taproot (P2TR), with the Nakamoto-era coins being a known subset of old-style P2PK outputs. Simultaneously, each output is vulnerable to short-range attacks when spent, increasing the urgency for a widespread migration to quantum-resistant signatures, even though the probability of a successful attack in the short term remains low.

Mitigating quantum risks

A sound roadmap is emerging to address these vulnerabilities. The main long-term strategy is to integrate post-quantum cryptography into networks—using new algorithms resistant to quantum attacks. The National Institute of Standards and Technology (NIST) has a shortlist of PQC protocols, including CRYSTALS-Dilithium, SPHINCS+, and FALCON. Also noteworthy is the formation of the Coinbase Quantum Computing and Blockchain Independent Advisory Committee, a group of world-renowned experts dedicated to assessing the impact of quantum computing on the blockchain ecosystem and providing clear, independent guidance to the wider community.

Guidance from Chaincode Labs (a Bitcoin research and development center) outlines two multi-year processes to mitigate risk. First, in the event of a sudden breakthrough in quantum computing, a short-term contingency plan can be implemented within two years, rapidly deploying safeguards and ensuring cybersecurity by prioritizing migration transactions.

On the other hand, if a quantum breakthrough doesn't occur, a longer-term path can be used to standardize quantum-resistant signatures via a soft fork. While post-quantum signatures are larger and slower to verify than today's signatures, wallets, nodes, and fee economics will need time to adapt. This could take up to seven years to fully implement. Fortunately, today's most advanced quantum machines have fewer than 1,000 qubits, far from the level needed to jeopardize blockchain cryptography like Bitcoin.

Promising technological proposals for addressing the quantum threat include:

• BIP-360 (Pay to Quantum-resistant Hash) keeps public keys off-chain and paves the way for post-quantum signatures.

• BIP-347 (Re-enable OP_CAT to support hash-based one-time signatures)

• Hourglass (rate-limits the cost from vulnerable outputs to ensure a stable transition)

Best practices include avoiding address reuse, moving vulnerable UTXOs to a single destination, and developing customer-oriented materials to institutionalize quantum-ready operations. Current understanding supports this approach, namely that vulnerable scripts are not used in production and per-address funding constraints reduce centralization risk.

Overall, we do not view quantum computing as an imminent threat because today's machines are too small—orders of magnitude smaller—to break Bitcoin's cryptography. Nevertheless, we are pleased that the open-source community remains vigilant regarding engineered quantum transfer paths.

3 Ethereum

Market Outlook

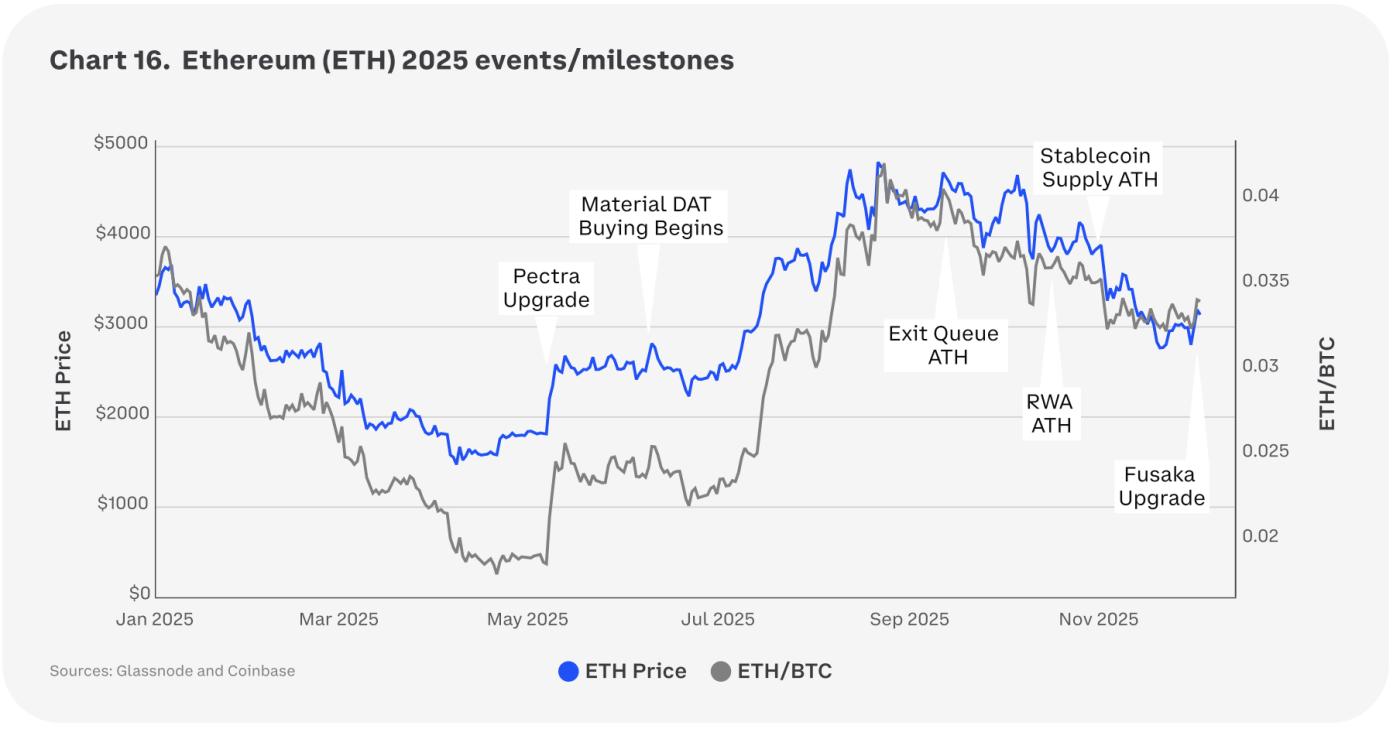

ETH's price action in 2025 was like a rollercoaster: after falling approximately 60% from January to early April, with ETH/BTC hitting a five-year low, the price surged by about 250% in late summer due to a surge in institutional demand—first from enterprise DAT demand, followed by an acceleration of spot ETF inflows. We believe that the Pectra upgrade decisively shifted the ETH trend to bullish one day later. We believe this upgrade resonated with sophisticated buyers in four ways:

1. Throughput and cost mitigation achieved through blob expansion and dynamic blob targets (EIP-7691), which increases data capacity and helps keep rollup costs low;

2. Account Abstraction User Experience (EIP-7702) allows External Owner Accounts (EOA) to temporarily act as smart accounts for bulk transactions and pay gas fees in non-ETH tokens, eliminating friction between consumer applications and institutional workflows;

3. Clearer staking operations are achieved through a higher maximum validator balance (EIP-7251) and contract-controlled withdrawals and on-chain deposit processing (EIP-7002, EIP-6110), which improves the efficiency and operational control of pooled/custodial staking.

4. Enhanced security from upgraded cryptographic safeguards.

We believe that all of these together constitute a more scalable, less frictional, and more institutionally oriented settlement layer.

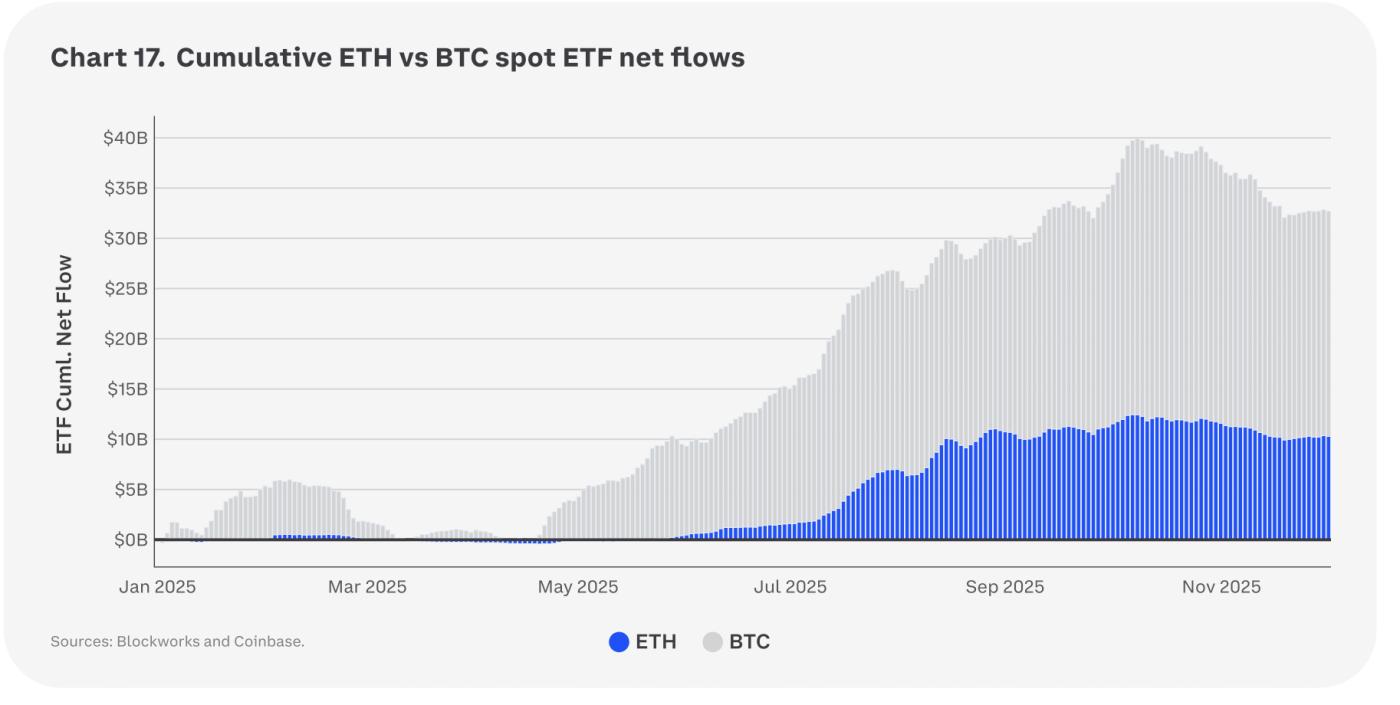

Fund flows accelerated immediately after the Pectra upgrade but cooled in October as a broader risk reset occurred. The US spot ETH ETF recorded several exceptionally strong inflow days in the mid-to-late 2025, including a record weekly inflow of approximately $2.8 billion in mid-August, driving an unusually rapid increase in inflows from June to September. By late October, ETH's cumulative spot inflows for 2025 reached approximately $12 billion, roughly double that of BTC, consistent with a "BTC-first" adoption pattern, but still representing a historically significant base of incremental demand for ETH. In fact, ETH spot ETF inflows surpassed those of BTC in Q3 2025.

Following the deleveraging shock on October 10th (the largest crypto liquidation event on record), momentum stalled, with net outflows occurring as prices weakened. Looking ahead to 2026, we believe a return to an upward trend in ETF inflows will likely depend on macro tailwinds (lower interest rates, stronger risk appetite, and more accommodative financial conditions) to re-attract the ETF buyer base.

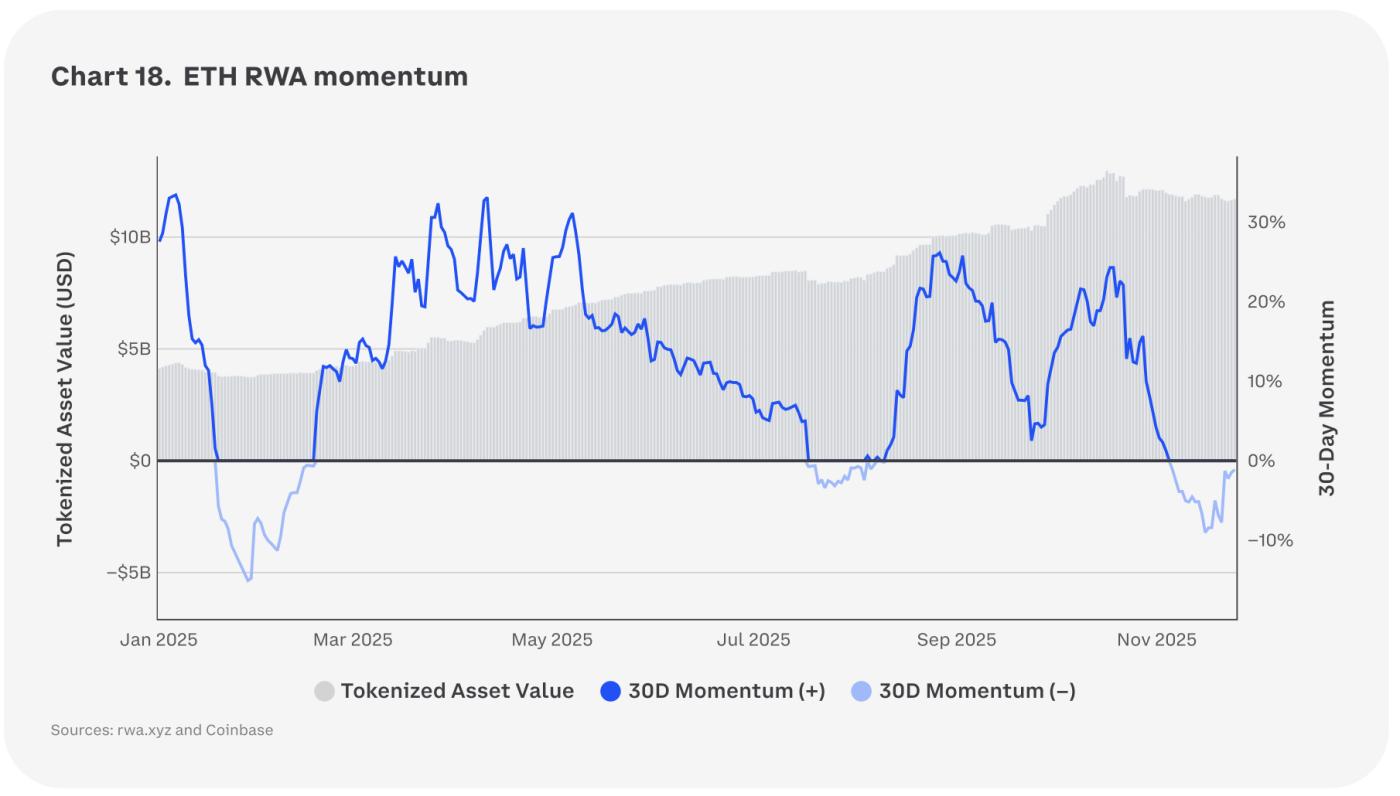

Meanwhile, Real-World Assets (RWAs) have become a wedge for “persistent demand” on Ethereum and continue to grow compounded. Tokenized Treasury bonds and on-chain funds saw substantial growth in 2025, pushing the total amount of tokenized assets on Ethereum to a peak of $12.7 billion. BlackRock’s BUIDL fund alone reached approximately $2.5 billion on Ethereum in October, after which some of the funds were reallocated to other chains. However, as of November 3, Ethereum still holds approximately 52% of the RWA market share—highlighting its role as a regulated yield settlement channel. Looking ahead to 2026, we believe that continued growth in on-chain cash and tokenized credit, even when speculative activity subsides, can anchor to underlying block space usage and fee generation, providing stable, fundamentally driven buying for ETH.

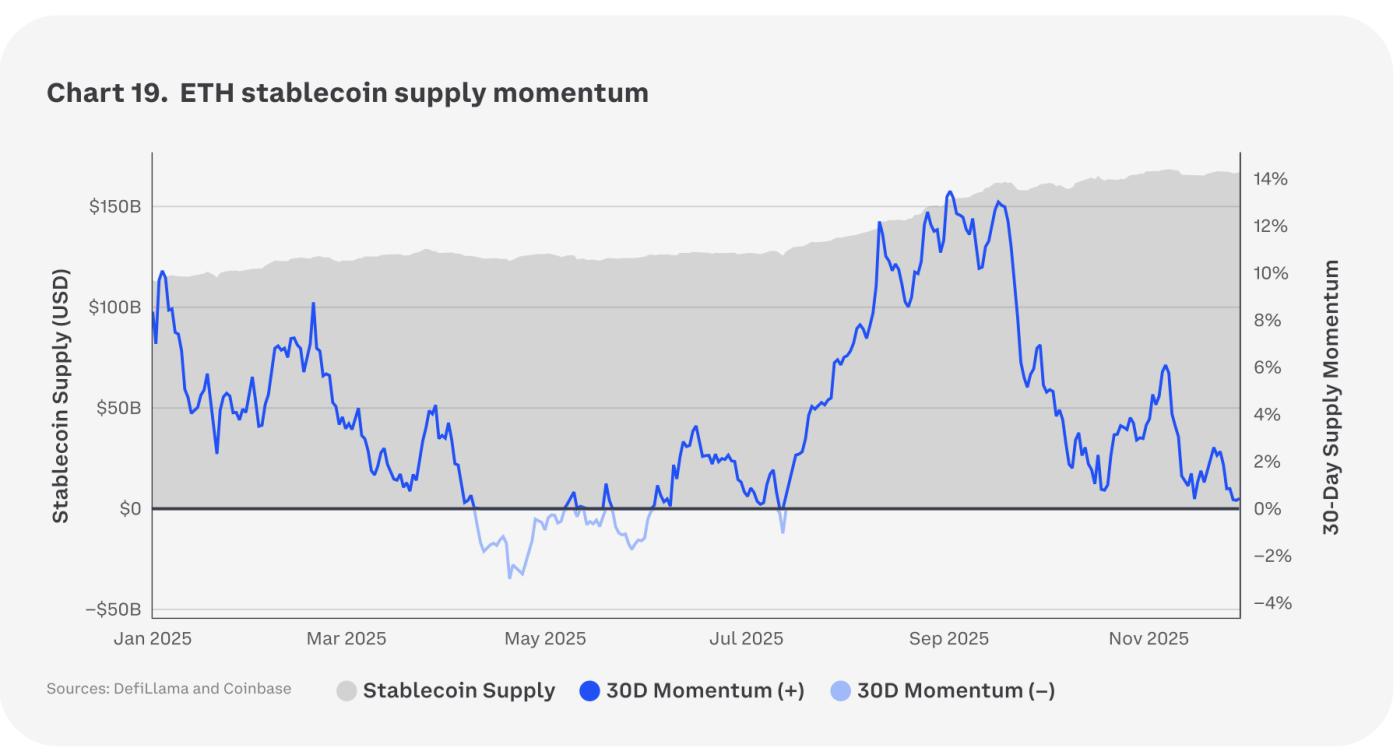

Stablecoin supply on Ethereum hit a new high in November (currently accounting for approximately 60% of the DeFi stablecoin market share), but the 30-day growth momentum has cooled since the risk reset in October. Looking ahead to 2026, the next phase may not just be "more the same," but rather selective fragmentation: Circle's Arc (an EVM L1 with USDC as its native gas, featuring sub-second finality and a built-in FX engine) and Stripe's Tempo (an EVM Payments L1) aim to centralize USDC settlement on dedicated channels, potentially diverting payment-related funds from USDC-dominated retail throughput on-chain. We believe Solana is structurally more susceptible to this (USDC-based, payments/TPS-oriented), while Ethereum's combination (USDT-based, RWA/DeFi collateral, lower TPS, higher fees) is less sensitive to USDC-specific migrations and more reliant on institutional channels.

Therefore, we believe that Ethereum's stablecoin share appears quite resilient, even as growth rotates across different venues. In our view, the renewed expansion of circulating supply should still support ETH activity (especially in L2 and RWA staking cycles), while Arc/Tempo is likely to primarily reroute USDC payments from high-TPS chains rather than erode Ethereum's institutional-oriented foundation.

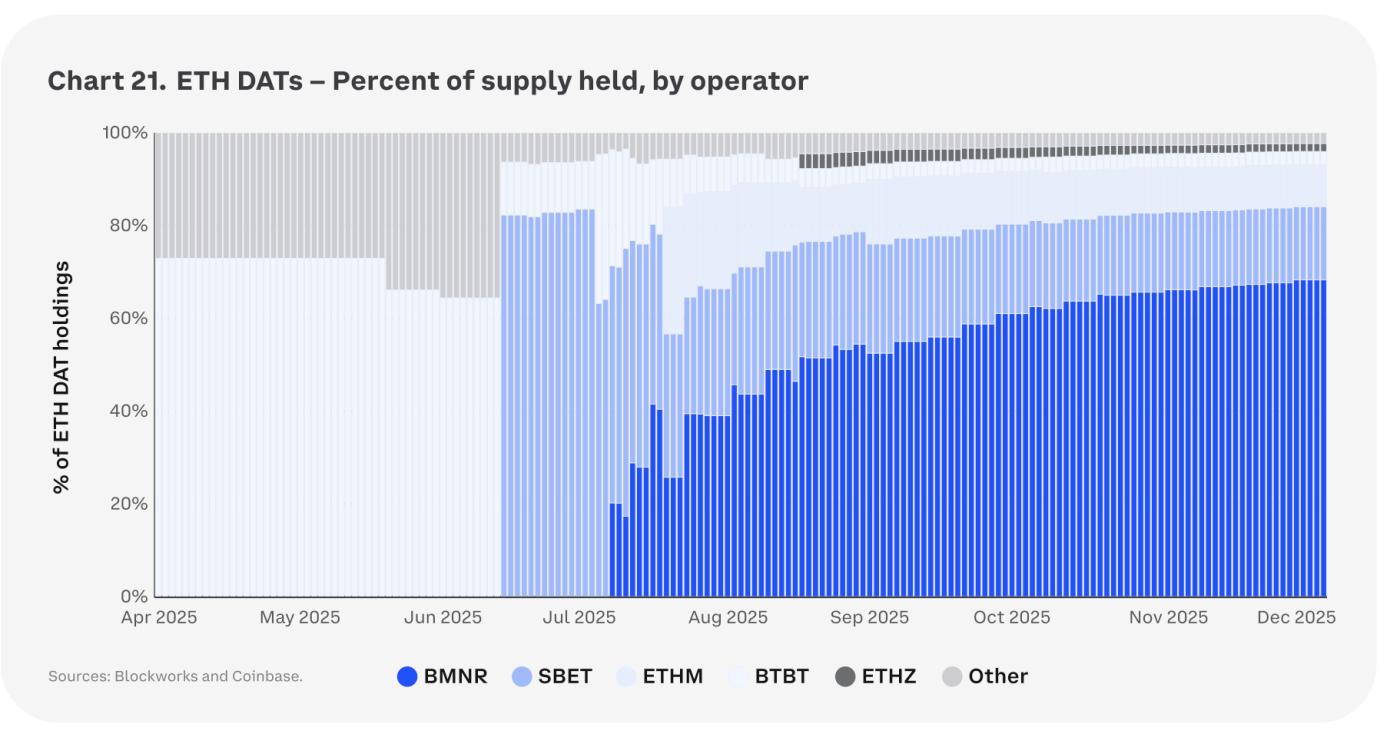

DAT demand drivers

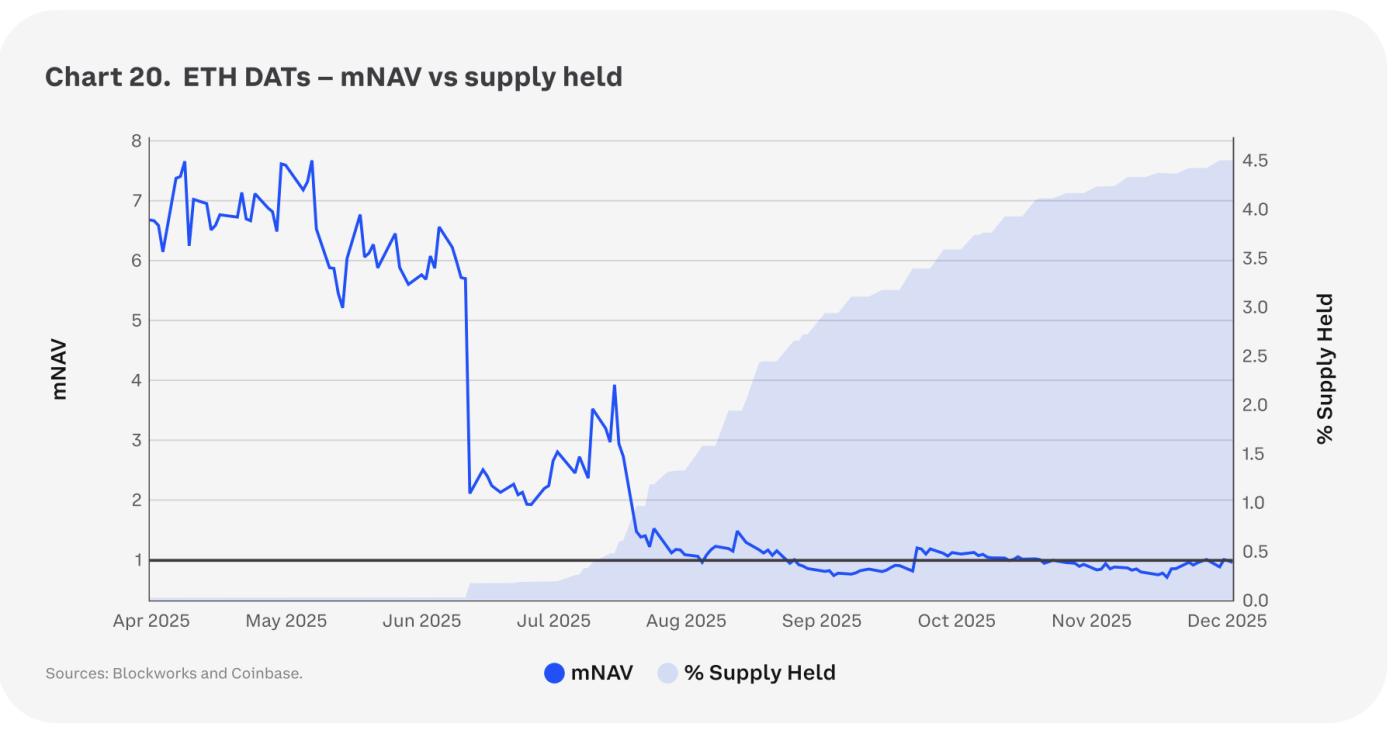

Digital Asset Treasurys (DATs) were a significant new player supporting ETH demand in 2025. They aggressively accumulated ETH, holding just over 4% of the circulating supply by year-end, providing sustained buying even during periods of significant overall liquidity volatility. As ETH's parabolic price action cooled, DATs' mNAV (market capitalization divided by the value of crypto assets held) compressed sharply, reflecting a waning frenzy and a tighter risk budget.

However, even after the significant compression of mNAV, the percentage of supply held by ETH DAT continued to climb. This is because, entering the fourth quarter, incremental DAT buying became concentrated, with most new ETH purchases coming from BitMine (BMNR), while other DAT remained relatively sidelined.

Looking ahead to 2026, we believe DAT will remain a meaningful “sticky” supply absorption pool for ETH, but future support is likely to be narrower and more price-sensitive unless (1) ETH prices regain momentum or (2) new corporate treasuries join the ranks of buyers. In other words, we believe DAT support will still be a tailwind—just not the broad, multi-sponsored tailwind that was at its 2025 peak.

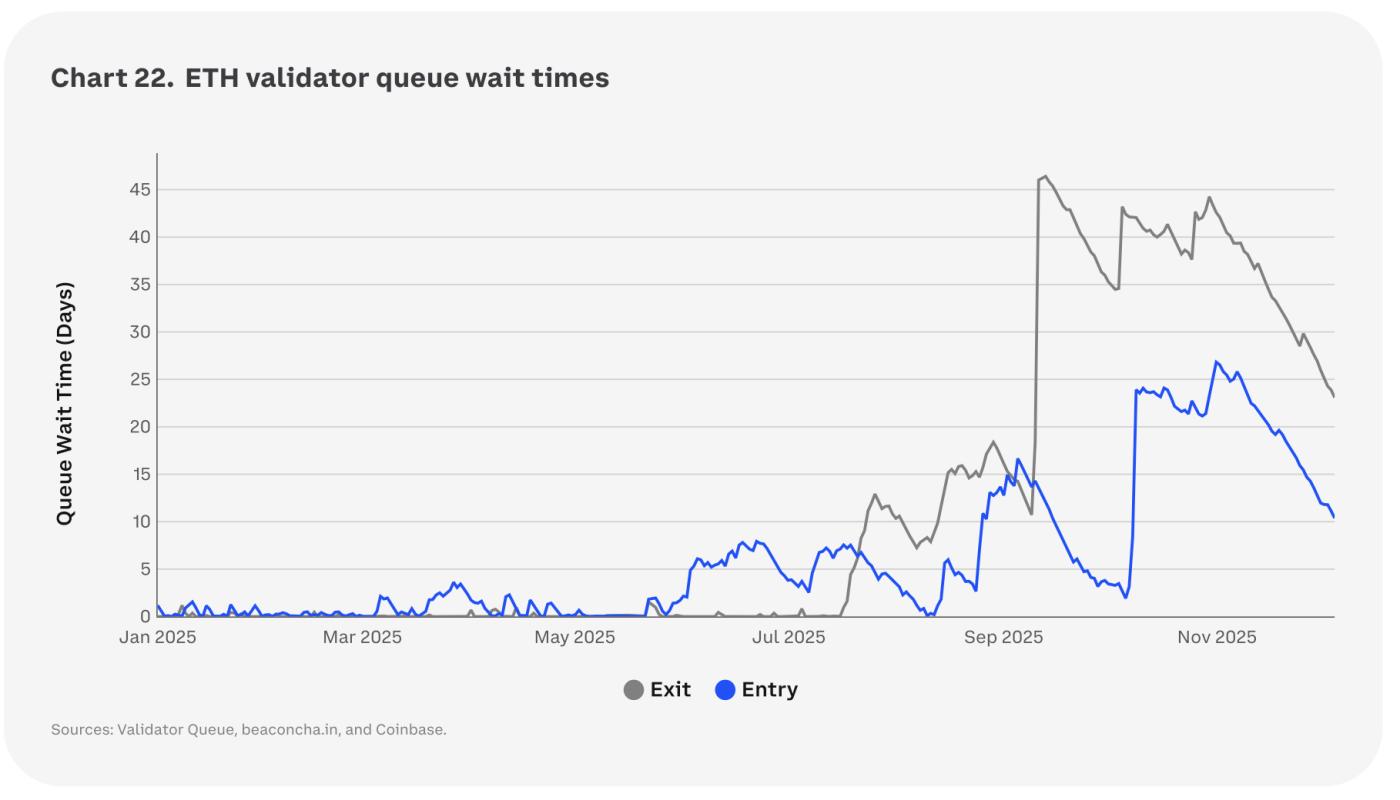

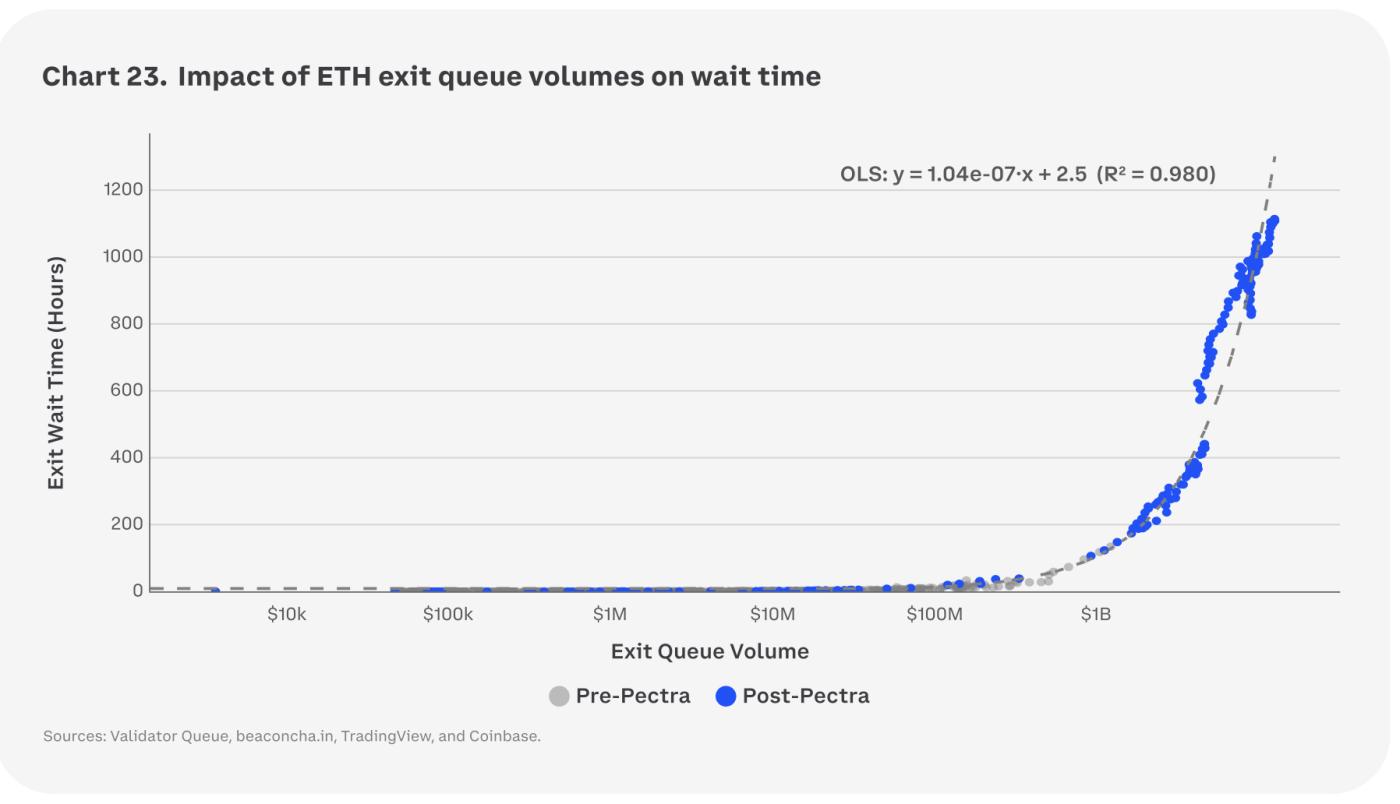

Crowded exit queue

In the second half of 2025, the exit time for unstaking Ethereum extended to weeks instead of days. By September, the Ethereum validator exit queue surged to approximately 45 days, with about 2.6 million ETH queued, with preventative exits (such as Kiln's exit after the SwissBorg incident) pushing the backlog to record levels. Following the liquidation event on October 10, more ETH joined the queue, while entry demand also jumped (primarily from Grayscale enabling staking in its US spot fund), making the surge appear as a two-way routing rather than a one-way derisking. Nevertheless, the fact that wait times could extend to more than a month is problematic: during periods of stress, liquidity stuck in the queue is liquidity that cannot be used to meet redemption or risk management needs.

Queuing Mechanism: For medium-sized exits, wait times remain close to hours, but could rise to weeks in the event of large-scale events. This is important for anyone who needs to manage daily liquidity based on potential exit queue times. In particular, we believe this will have the following significant implications for staking ETH ETFs:

• Daily Liquidity Design: A well-functioning collateralized ETF can meet daily redemptions by holding uncollateralized liquidity reserves (cash and/or uncollateralized ETH) and controlling the pace of creation/redemption. This reserve is the first line of defense, so under normal circumstances, investors will not "feel" the presence of queues.

• Real-world testing: Pectra has not eliminated exit latency (although it is not necessarily intended to). Loss of consensus layer data still limits exits. A variable exit queue and approximately 1 day of withdrawability latency remain. Withdrawal cleanup congestion (cleaned old-style 0x01 validators) and a partially queued withdrawal mean there is no fast track during large-scale, simultaneous redemptions.

• Liquidity Reserve Size: Reserves should cover typical daily outflows plus a prudent stress buffer, with the shortfall covered by credit lines and/or validator transfer instruments. Specific percentages vary by issuer, but the black swan event of 2025 demonstrates that ETF structures must account for extreme, related shocks (e.g., the waterfall liquidation of October 10th) and exceptional events (e.g., Kiln's exit pushing the queue to approximately 40 days).

We also see the potential for systemic risk. A larger institutional staking base could amplify queue friction during a sell-off. The same group of allocators who maintain stable cash flows in a calm market could become synchronized sellers in a liquidation crash. If staking ETFs and large custody schemes grow significantly in 2026, price shocks could cause many to simultaneously seek exits, extending queues, delaying redemptions, widening the discount of Liquidity Staking Tokens (LSTs) relative to net asset value, and forcing second-order derisking elsewhere while funds are stuck in queues. In short, we believe institutional adoption raises the floor for the supply of staked ETH, but also raises the ceiling for “one-off” exits.

Fusaka Upgrade

The Fusaka upgrade launched on December 3, 2025. It is one of the largest hard forks in terms of scope, containing approximately a dozen Ethereum Improvement Proposals (EIPs) focused on enhancing the scalability and efficiency of the Layer-2 network. Most EIPs aim to improve Rollup scalability and node efficiency, which may not immediately drive ETH price movements, but we have listed some of the changes we believe are most critical below:

• EIP-7594: This EIP allows nodes to verify the data availability of binary large objects (blobs) by sampling, rather than downloading each blob, thus significantly reducing bandwidth and laying the foundation for future increases in blob capacity (which helps reduce L2 costs). This is a network layer step towards full Danksharding.

• EIP-7935: This update increases the default block gas limit for clients to 60 million, allowing for more complex transactions and higher throughput at the base layer. It benefits L2 scaling by supporting heavier workloads while maintaining network stability.

• EIP-7951: This EIP natively supports the secp256r1 elliptic curve, which is commonly used in security standards such as hardware wallets and Transport Layer Security (TLS). It simplifies integration with off-chain systems, enables cryptographic key-based authentication (such as Face ID), and enhances the user experience of account abstraction without costly conversions.

• EIP-7642: This proposal adds a historical service window, enabling nodes to publish which block ranges of services they provide, and removes the Bloom field from receipts on the line to reduce synchronization costs. This reduces node storage requirements, saves significant disk space, and speeds up the synchronization of new nodes.

In addition, a number of EIPs also focus on network hardening, such as EIP-7892 for the Blob Parameter-Specific (BPO) hard fork, which allows for flexible adjustment of the number of blobs without a full upgrade, and optimizations like EIP-7939, which adds new CLZ opcodes to reduce gas costs in bitwise operations. These changes aim to enhance Ethereum's modularity, reduce risk, improve development efficiency, and also lay the foundation for future scaling work (such as Verkle trees) without breaking existing contracts.

Glamsterdam Upgrade

The planned Glamsterdam upgrade, aimed at a 2026 release, is currently in the planning and governance phase, with EIP proposals under review. It represents a significant step in Ethereum's ongoing evolution, focusing on scalability, efficiency, and reduced centralization risks. While the final scope is still being determined, several key proposals have emerged due to their potential impact on network performance and user experience.

• EIP-7732: This feature aims to directly separate block proposers and builders in the protocol, reducing the risks associated with Maximum Extractable Value (MEV) and builder centralization. By making this separation a native feature of Ethereum, it enhances censorship resistance, improves block building efficiency, and promotes a more decentralized verification process.

• EIP-7928: This EIP introduces a block-level access list that records all accounts and storage locations accessed during block execution. This enables parallel transaction processing, significantly improving throughput and reducing gas costs for complex operations. It also helps optimize state access, making the network more efficient overall.

• EIP-7782: This proposal seeks to halve Ethereum's slot time from 12 seconds to 6 seconds, effectively reducing on-chain latency and epoch duration. This change will accelerate transaction finality and improve the responsiveness of decentralized applications, benefiting Layer-2 networks and the overall user experience.

Additionally, other potential EIPs under discussion could further improve the EVM, such as increasing contract size limits or making additional optimizations to data availability. These changes aim to make Ethereum more scalable, secure, and developer-friendly, supporting future innovations such as full Danksharding and stateless clients, without disrupting existing deployments.

4 Solana

Market Outlook

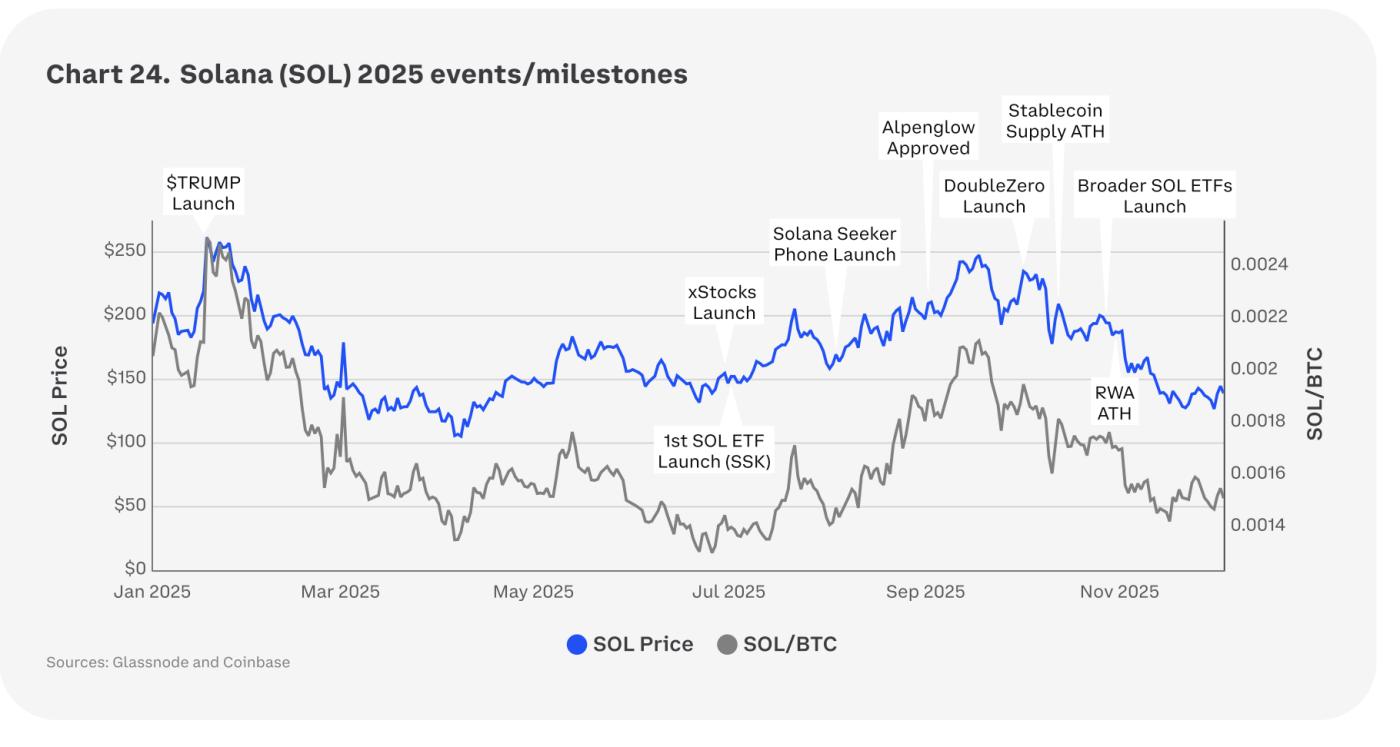

Solana got off to a bang in 2025: the launch of $TRUMP in January marked the explosive top of the Solana meme supercycle, which was also a local top for SOL itself. Since meme activity is a significant revenue driver for Solana, the unwinding process was swift. SOL fell approximately 68% from its January peak before finding support near $100. It's worth noting that the bottom for SOL/BTC came much later. After several months of underperformance, the SOL/BTC exchange rate only bottomed out before two concrete catalysts arrived in July: 1) the launch of the first SOL-staking ETF, and 2) xStocks (tokenized stocks) on Solana. The launch of the SOL ETF expanded the addressable buyer base, while xStocks brought traditional finance onto the blockchain. These catalysts (along with a host of other developments such as the launch of the Solana Seeker phone, approval of Alpenglow, and increased SOL DAT participation) helped support the SOL/BTC exchange rate into the summer.

However, despite Solana continuing to witness genuine upgrades and strong fundamental catalysts in Q4 2025, macro factors outweighed micro factors. BTC's trend was disrupted by macro concerns (tariff policy uncertainty, tightening dollar liquidity, persistent inflation, etc.), dragging down the entire crypto market. Therefore, despite the following catalysts: 1) the launch of DoubleZero, significantly improving Solana's performance; 2) the launch of a wider and cheaper SOL ETF instrument; and 3) record highs in stablecoin supply and net RWA inflows. We believe this price action boils down to a key takeaway for 2026: on average, Altcoin are likely to continue to follow BTC's price action, regardless of fundamental catalysts, and without a decisive breakout of Bitcoin's dominance.

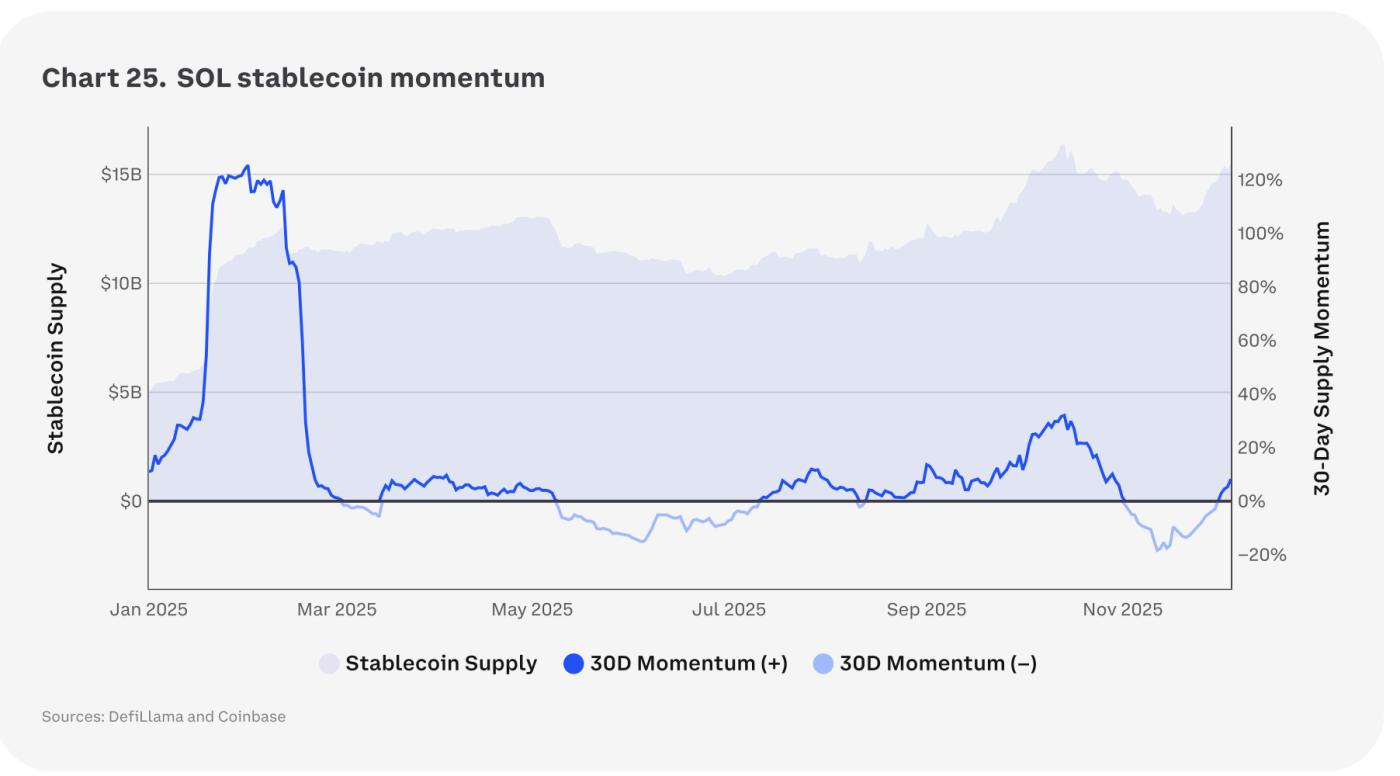

Solana's stablecoin story follows a mixed path. On-chain stablecoin activity surged in January with the meme frenzy, but flattened out after a decline in meme activity. Since the liquidation event on October 10th, Solana's stablecoin momentum has turned negative, while Ethereum's has remained positive. Looking ahead to 2026, we believe Solana may continue to face pressure from the launch of new L1 tokens. As we mentioned in the "Ethereum" section, the launch of USDC-native, payment-optimized L1 tokens (Circle's Arc and Stripe's Tempo) in 2026 could reroute some merchant/wallet cash flows. Given Solana's USDC-dominated structure (approximately 60%) and its payment/TPS positioning, this competition directly targets Solana's comparative advantage more than the competition against Ethereum (whose foundation is more USDT-pegged and institutionally oriented).

Memecoin craze subsides

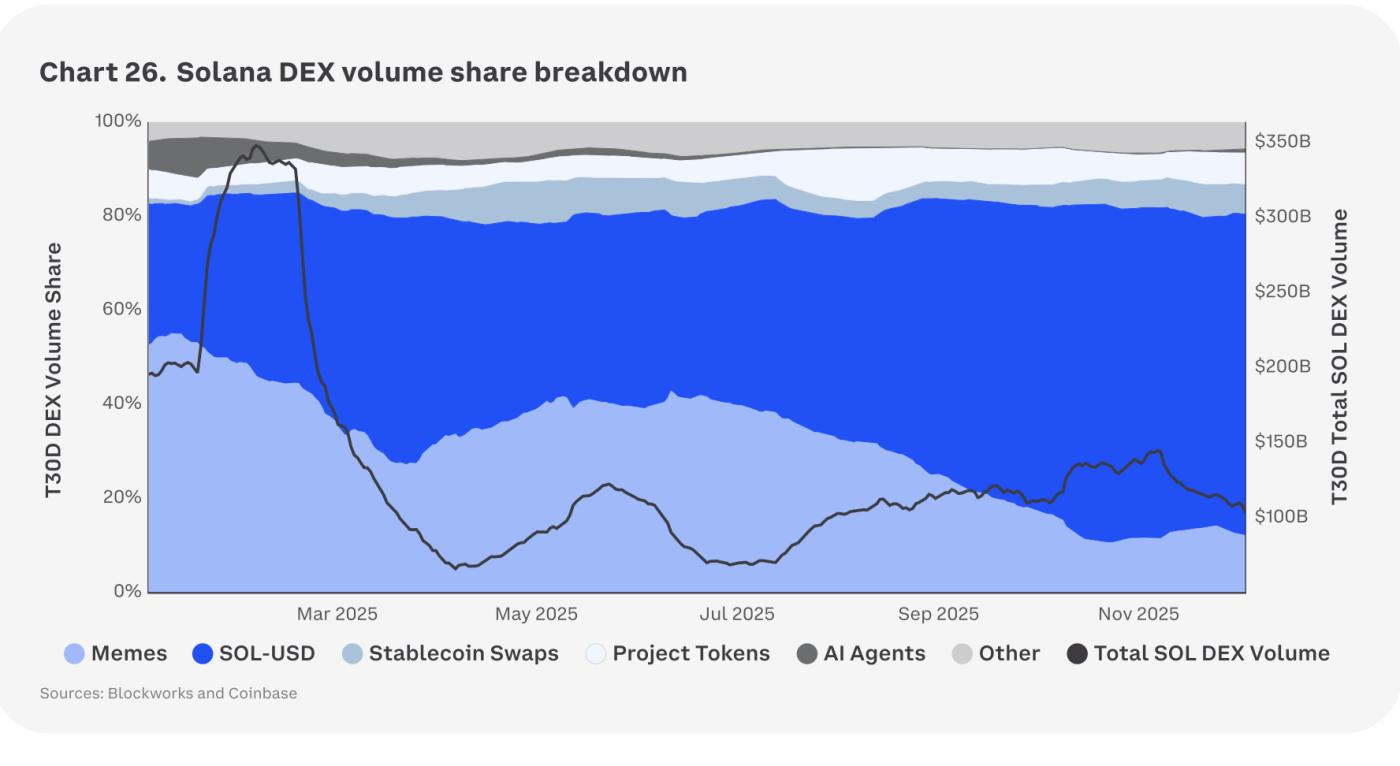

While the memecoin craze dominated Solana's narrative in 2024, activity subsided in 2025, dragging down Solana DEX's total trading volume. Activity surged during the launch of $TRUMP/$MELANIA, pushing fees and throughput to congestion thresholds, resulting in latency, failed/queued transactions, and higher priority fees. While this was beneficial for short-term revenue, it was detrimental to user experience. As the year progressed, returns from new token issuances were compressed due to dilution from too many tokens, more "rug pulls," and aggressive profit-taking. Liquidity was scattered across numerous trading pairs, and speculators quickly rotated to other narratives. The result was a significant shift in activity from memes on Solana, and a clear downward trend in Solana DEX's total trading volume throughout the year.

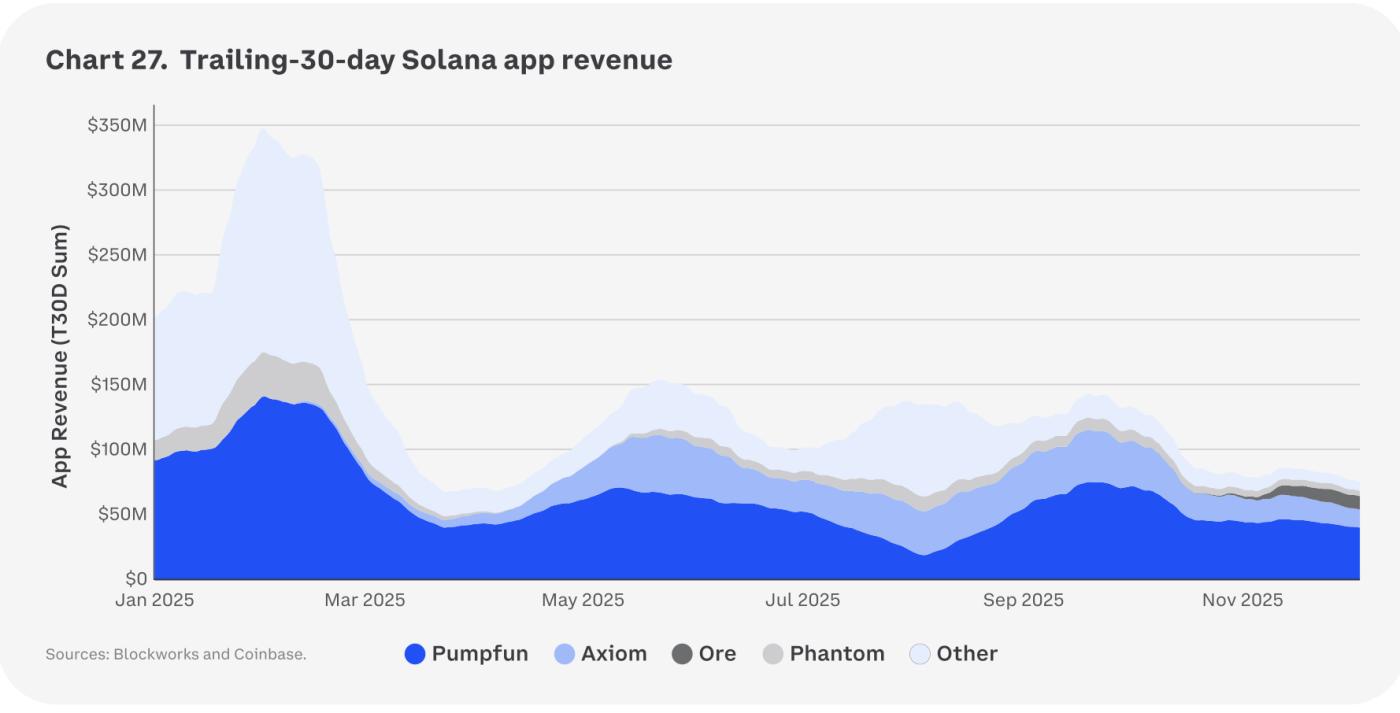

Application-level revenue trends paint a similar picture. Solana's total application revenue plummeted from over $300 million per month at the peak of Memecoin in early Q1 2025 (when PumpFun, Phantom, and other consumer apps combined generated revenue) to less than a third of that by the end of Q4 2025. In this decline, PumpFun proved to be the most resilient revenue engine on-chain: even as overall Memecoin volume shrank, its launch channel and fee model continued to capture an excessively high proportion of the remaining speculative flow, while revenue from other applications was compressed even more significantly. This centralization highlights both a strength and a vulnerability for Solana in 2026: while its leading consumer apps can still generate substantial cash flow, the application revenue base is largely tied to a single, narrative-driven product vertical.

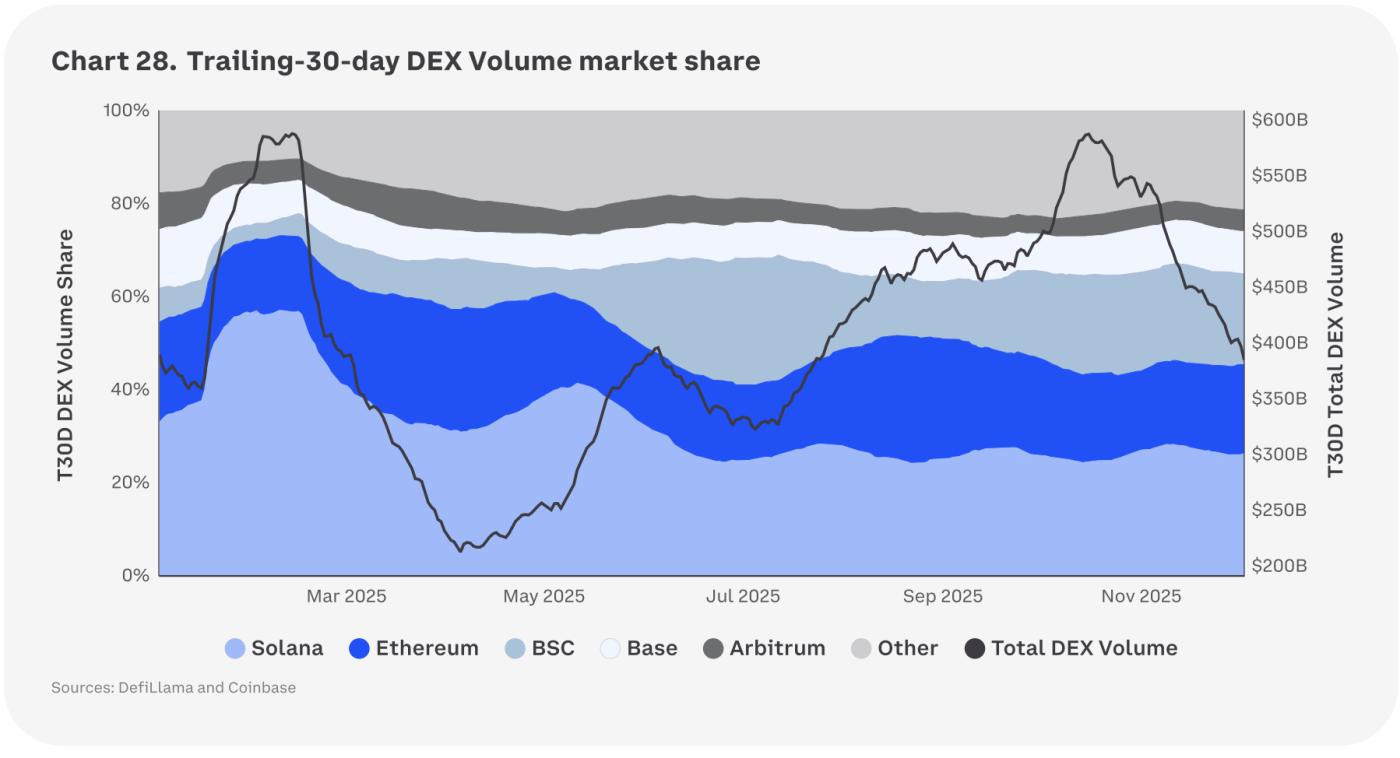

However, not every chain shared Solana's fate. As Solana DEX activity cooled, funds rotated to BNB Chain, where an Asian-led memecoin issuance boom, fueled by BNB price momentum and relentless social hype, sparked a new memecoin season, diverting retail liquidity and attention away from Solana. This rotation was so significant that even though Solana's DEX volume declined by approximately 60% from January to November, total cross-chain DEX volume remained roughly flat as BNB Chain absorbed this idle capital. This feedback loop was also reflected in BNB's price action: while most Altcoin fell by over 70% in the October 10 liquidation shock, BNB briefly hit new highs afterward before retreating along with the rest of the crypto market as the BTC trend broke down.

We believe that memecoin trading volume is highly susceptible to (1) narratives and (2) severe market liquidity glut. Solana's base still holds the deepest share of single-chain DEX trading volume, but maintaining this advantage may depend on new catalysts that create repeatable cash flows outside of pure memecoin (e.g., tokenized stocks, AI agents, RWA, DePIN, etc.). If memecoin buying remains fragmented across chains, Solana's relative share could drift even if absolute DEX trading volume rises in a broad risk-averse environment. Conversely, a resurgence of single-chain memecoin supercycles on Solana or a killer consumer protocol like PumpFun would quickly refocus cash flows and benefit the $SOL token.

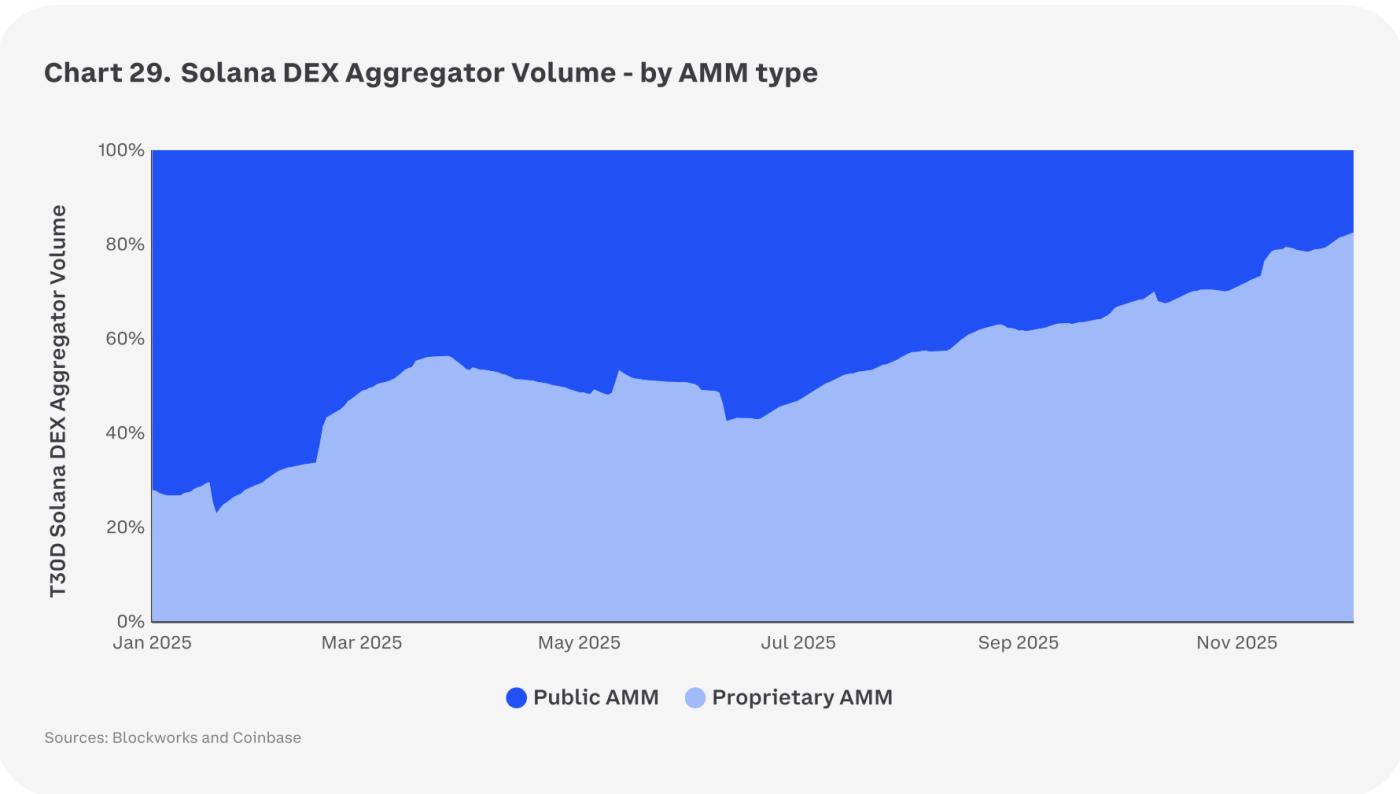

The rise of proprietary AMM

The proprietary Automated Market Maker (AMM) has become the default execution layer in Solana, replacing the public AMM in less than a year.

Public AMMs offer classic DeFi designs:

• Anyone can provide liquidity to the transparent binding curve

Anyone can trade directly with him.

• Prices only change when transactions are consumed or liquidity is added.

Proprietary AMMs disrupt this model, tending towards a centralized approach:

• Liquidity is owned and managed by a single company

• Prices are driven by fast oracles and proprietary algorithms.

Users typically can only access these through aggregators, not through public front-ends.

During 2025, the share of aggregator-routed swap transactions processed by these dedicated venues increased from approximately 25% to approximately 80%. This means that most transactions are now settled with actively managed, company-owned liquidity, rather than with passive public liquidity pools.

The proprietary AMM works because Solana's microarchitecture is particularly well-suited for on-chain, high-frequency market making. Low fees and high throughput make streaming oracle updates economically viable (at a fraction of the cost of a normal swap transaction), and Jito's relatively inexpensive per-compute tipping allows these lightweight updates to be processed before takers. Therefore, market makers can refresh quotes multiple times per second, tightly concentrating liquidity around the oracle price while still paying modest fees. We believe this provides Solana with a strong structural advantage, enabling lower slippage on deep, high-turnover trading pairs, potentially facilitating a shift of more spot trading volume for blue-chip pairs from centralized exchanges (CEXs) to the Solana DEX in 2026.

However, the efficiency gains also come with clear trade-offs: liquidity and decision-making power are now concentrated in the hands of a small, opaque group of operators. Proprietary AMMs use closed-source procedures, self-managed treasuries, and scalable strategies. There are no permissionless liquidity providers (LPs), and typically no public interface. From an opaque perspective, this is a characteristic—it can reduce harmful order flows and front-running—but it also means that end users and the protocol are heavily reliant on the risk control and due diligence of a few companies and aggregators. If the primary proprietary venue fails, swap routing must adapt rapidly.

Looking ahead to 2026, we believe Solana is likely to operate as a two-tier market: a proprietary AMM for core liquidity and a public AMM for speculation on micro-cap tokens. Based on Q4 trends, we expect proprietary venues to maintain a majority share on large-cap trading pairs, while public AMMs will remain a testing ground for micro-cap tokens. If spot trading volume continues to migrate from CEXs to DEXs, we believe value capture will increasingly favor chains like Solana, where proprietary AMMs can compete with CEX spreads and liquidity.

Demand drivers

By 2025, Solana's demand diversity had matured significantly, shifting from retail-driven memecoins to balance sheet buyers, ETFs, and on-chain funds. Three new channels took on most of the burden: (1) corporate digital asset treasuries, (2) US spot ETFs, and (3) tokenized real-world assets. Together, they broadened the buyer base beyond purely speculative flows and created a more sticky source of demand that could withstand volatility.

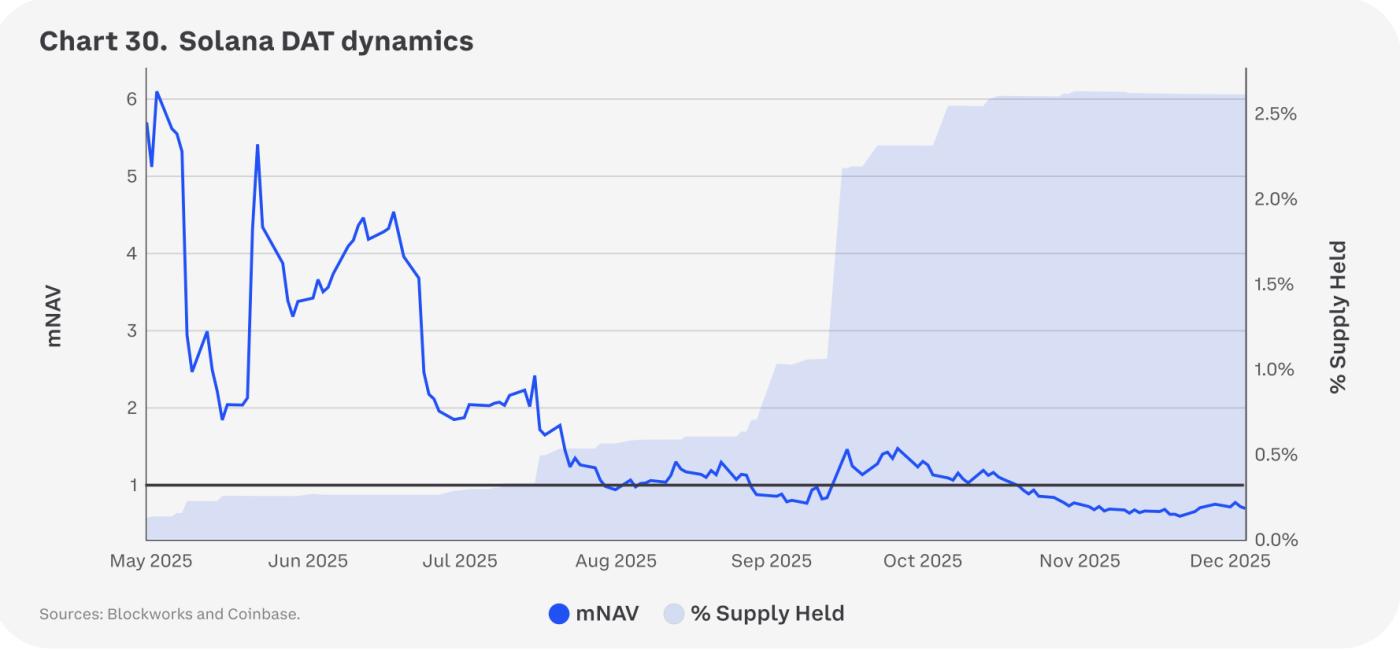

DAT projects steadily accumulated ahead of Q3 2025, pushing Solana DATs' supply share above 2.5% by November, even as mNAV compressed from approximately 6x in May to below 1x in November. This pattern suggests sustained corporate buying, while stock market pricing discipline penalizes overvalued stocks. The entry of DATs as Solana holders is significant because they represent a more sustainable and less speculative source of funding. Corporate treasury plans are subject to board-approved position management, are written into investment policies, and are typically implemented as part of a long-term accumulation strategy, naturally deterring impulsive selling.

Holding positions in institutional custody with segregation, access controls, and audit trails makes rapid exits both operationally and reputationally costly. Because many treasuries map crypto assets to long-term goals (strategic reserves, balance sheet diversification, or ecosystem alliances), these timeframes are measured in years rather than weeks. Furthermore, the Financial Accounting Standards Board (FASB)'s fair value accounting, implemented after 2024, has reduced penalties for short-term declines, diminishing the incentive for mechanical risk-averse strategies.

Conversely, if DATs continue to trade below net asset value, their ability to increase value through equity issuance will be limited, thus offsetting the flywheel effect of "selling equity at a premium to buy crypto assets." A persistent discount also increases financing costs and attracts activist pressure to "realize net asset value" through tender offers or asset sales, transforming DATs from stable accumulators into potential net suppliers during periods of stress. In leveraged structures, depressed equity values could further tighten collateral buffers and force defensive risk-averse measures, amplifying downside risk.

The spot US SOL ETF opened a second capital channel in the second half of 2025, with its assets under management (AUM) and cumulative net inflows trending upward from July to early November, accelerating towards the end of the year with the launch of low-fee products. For example, Bitwise's Solana Staking ETF (BSOL) set a record for the highest first-day trading volume of any Altcoin ETF th