Original title: Frowny Cloud

Original author: Arthur Hayes, co-founder of BitMEX

Original article translated by BitpushNews

(Disclaimer: All views expressed in this article represent the author's personal opinion only and should not be used as the basis for investment decisions or as advice for participating in investment transactions.)

The gods I worship have all transformed into adorable plush toys.

During Hokkaido's peak ski season in January and February, I pray to the "Frowny Cloud," the god of snowfall. The local climate dictates that during the peak ski season, snow falls almost non-stop, day and night, and you practically never see the sun. Fortunately, I also pray to the God of Vitamins—a cute little pony doll—who bestows upon me Vitamin D3 tablets and various other blessings.

While I love snow, not all snow is good and safe. The kind of carefree, high-speed skiing experience I enjoy requires a specific type of snow: low winds at night and temperatures between -5 and -10 degrees Celsius. Under these conditions, new snow can effectively blend with old snow, creating deep, powdery snow. During the day, gloomy clouds block specific wavelengths of sunlight, preventing slopes like south-facing slopes from being "cooked" and potentially causing avalanches.

Sometimes, the Frowny Clouds abandon us fearless skiers at night. Cold, clear nights cause the snow layer to "crack" as it warms and cools, creating persistent weak layers. This phenomenon can persist in the snowdrifts for a long time, and if the weight of a skier causes energy transfer leading to an avalanche, it can trigger a deadly avalanche.

As always, the only way to understand what kind of snowflakes Frowny Cloud creates is to study history. On a hillside, we do this by digging huge pits and analyzing the different types of snow that fall over time. But since this isn't an article about avalanche theory, our approach in the market is to study charts and the interaction between historical events and price fluctuations.

In this article, I hope to explore the relationship between Bitcoin, gold, stocks (especially US tech giants in the Nasdaq 100 index), and dollar liquidity.

Those who are either "Gold Bugs" or members of the financial establishment dressed in Hermès scarves and red-soled shoes (who firmly believe in "holding stocks for the long term"—I didn't get a high enough GPA to get into Professor Siegel's class at Wharton) (Bitpush note: Jeremy Siegel is a titan at Wharton and one of Wall Street's most respected economists), are ecstatic that Bitcoin will be the worst-performing mainstream asset in 2025.

These gold bugs scoff at Bitcoin enthusiasts: If Bitcoin is touted as a vote against the established order, why hasn't it performed as well as or even surpassed gold? Those dirty fiat currency stock salesmen also scoff: Bitcoin is nothing more than a "high beta" (high-risk) toy on Nasdaq, and it hasn't even kept up in 2025, so why consider cryptocurrencies in asset allocation?

This article will present a series of beautiful charts, along with my annotations, to clarify the interrelationships between these assets.

I believe Bitcoin's performance is entirely in line with expectations.

It follows the wave of fiat currency liquidity—especially dollar liquidity, as the Pax Americana credit pulse is the most important force in 2025.

The surge in gold prices is due to price-insensitive sovereign nations frantically hoarding it out of fear that their wealth will be plundered by the United States if they remain in U.S. Treasury bonds (as Russia experienced in 2022).

Recent US actions against Venezuela will only further intensify the desire of countries to hold gold rather than US Treasury bonds. Finally, the AI bubble and its related industries will not disappear. In fact, Trump must double down on state support for AI, as it is the largest contributor to the empire's GDP growth. This means that even if the rate of dollar creation slows, the Nasdaq can continue to rise because Trump has effectively "nationalized" it.

If you have studied China’s capital market, you will know that stocks performed very well in the early stages of nationalization, but subsequently underperformed significantly because political goals took precedence over capitalists’ returns.

If the price movements of Bitcoin, gold, and stocks in 2025 validate my market architecture, then I can continue to monitor the fluctuations in dollar liquidity.

I would like to remind readers that my prediction is that Trump will inject credit like crazy, making the economy "explode." A booming economy will help the Republicans win the election this November. The dollar's credit will expand significantly as central bank balance sheets expand, commercial banks increase lending to "strategic industries," and mortgage rates fall due to money printing.

In conclusion, does this mean I can continue to "surf" without worry—that is, aggressively deploy my earned fiat currency and maintain maximum risk exposure? Readers are free to judge for themselves.

A single map that provides an overview of the entire situation

First, let's compare the returns of Bitcoin, gold, and the Nasdaq in the first year of Trump's second term. How do these assets perform relative to changes in dollar liquidity?

I will elaborate on this later, but the basic assumption is that if dollar liquidity decreases, these assets should also fall. However, gold and stocks rose. Bitcoin performed as expected: terribly bad. Next, I will explain why gold and stocks bucked the trend and rose despite declining dollar liquidity.

[Chart: Comparison of Bitcoin (red), Gold (gold), Nasdaq 100 (green), and US Dollar Liquidity (purple)]

Not everything that glitters is gold, but gold certainly shines.

My cryptocurrency journey began with gold. In 2010 and 2011, as the Federal Reserve intensified its quantitative easing (QE), I started buying physical gold in Hong Kong. Although the absolute amount was pitifully small, it represented a surprisingly high percentage of my net worth at the time.

Ultimately, I learned a painful lesson about position management, as I had to sell my gold at a loss to buy Bitcoin for arbitrage in 2013. Fortunately, the ending was relatively positive. Even so, I still hold a significant amount of physical gold coins and bars in vaults around the world, and my stock portfolio is primarily composed of gold and silver mining stocks . Readers might wonder: since I'm a staunch follower of Satoshi Nakamoto, why do I still hold gold?

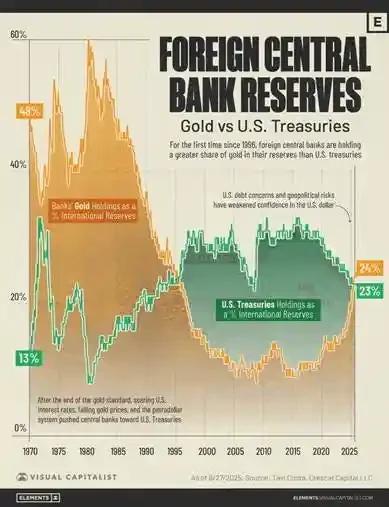

I hold gold because we are in the early stages of a global trend of central banks selling off US Treasury bonds and buying gold. Furthermore, countries are increasingly using gold to settle trade deficits, even when analyzing the US trade deficit.

In short, I buy gold because central banks are buying it. Gold has been the true currency of civilization for 10,000 years. Therefore, no major central bank reserve manager would choose to deposit Bitcoin when they distrust the current dollar-dominated financial system; they would be, and are, buying gold. If the proportion of gold in global central bank reserves returned to the levels of the 1980s, the price of gold would rise to $12,000. Before you think I'm being delusional, let me demonstrate it to you in a visual way.

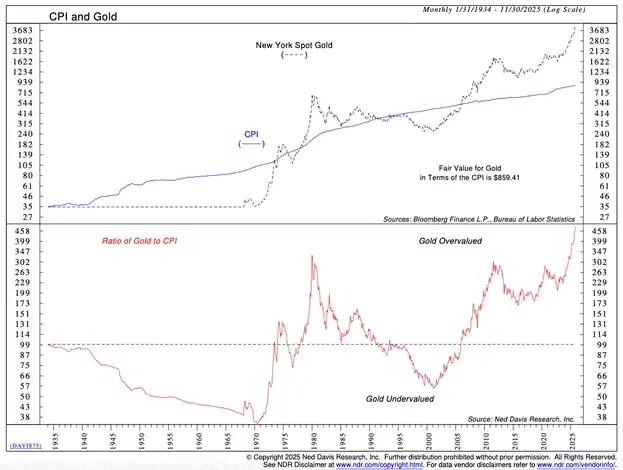

In the fiat currency system, gold is traditionally viewed as an inflation hedge. Therefore, it should roughly track the CPI index, which is manipulated by the empire. The chart above shows that gold has roughly tracked this index since the 1930s. However, since 2008, and accelerating after 2022, the price of gold has risen far faster than inflation. So, is there a gold bubble, poised to reap the profits of gamblers like myself?

[Chart: Gold Price vs. US CPI]

If gold were in a bubble, retail investors would flock to it. The most popular way to trade gold is through ETFs, with GLD being the largest. When retail investors frantically buy gold, the outstanding share of GLD increases. To compare across different periods and gold price systems, we must divide the outstanding share of GLD by the physical gold price. The chart below shows that this ratio is decreasing rather than increasing, meaning that a true gold speculative frenzy has not yet arrived.

[Chart: GLD circulating supply divided by spot gold price]

If it's not retail investors driving up gold prices, who are the price-insensitive buyers? Central bank governors around the world. There have been two pivotal moments in the past two decades that have made these people realize: the US dollar is only good for cleaning up messes.

In 2008, American financial giants created a global deflationary financial crisis. Unlike the Federal Reserve's inaction in 1929, this time the Fed violated its obligation to maintain the purchasing power of the dollar, printing money like crazy to "rescue" certain large financial players. This marked a watershed moment in the proportion of US Treasury bonds and gold held by sovereign nations.

In 2022, President Biden shocked the world by freezing the Treasury holdings of Russia, the world's largest commodity exporter with a massive nuclear arsenal. If the US was willing to strip Russia of its property rights, it could do the same to any weaker or less resource-rich nation. Unsurprisingly, other countries could no longer comfortably increase their exposure to US Treasury bonds at risk of confiscation. They began accelerating their gold purchases. Central banks are price-insensitive buyers. If the US president stole your money, your assets would instantly vanish . Since buying gold eliminates counterparty risk, what does a slightly higher price matter?

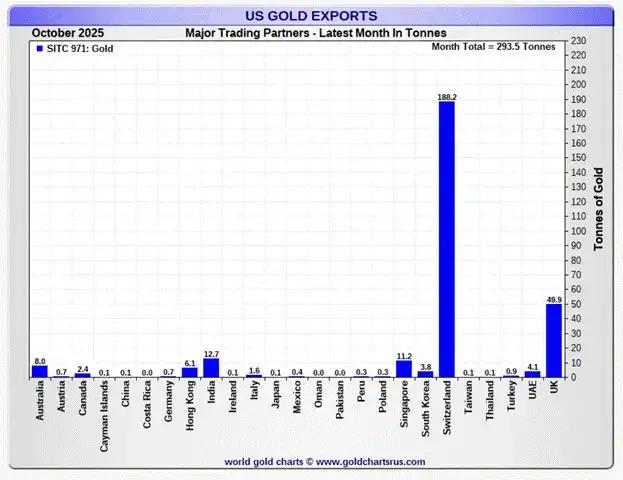

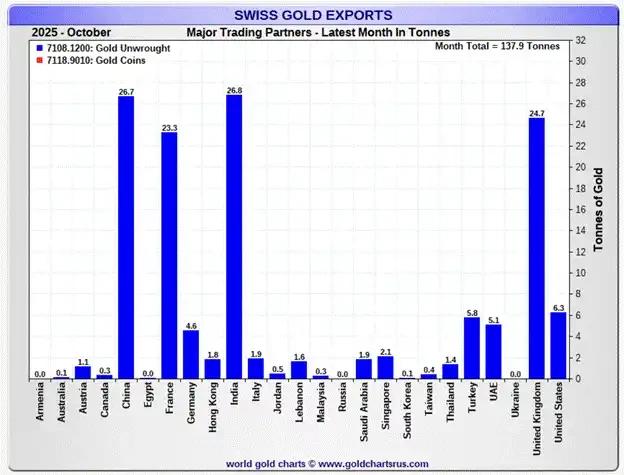

The fundamental reason why sovereign states have an insatiable appetite for this "barbaric relic" is that net trade settlements are increasingly being conducted through gold. The record contraction of the US trade deficit in December 2025 is evidence of gold's re-establishment as the global reserve currency. More than 100% of the change in the US net trade balance is attributed to gold exports.

"According to data released by the U.S. Commerce Department on Thursday, the merchandise trade deficit fell 11% from the previous month to $52.8 billion. This brings the deficit to its smallest level since June 2020… Exports rose 3% in August to $289.3 billion, mainly driven by non-monetary gold." —Source: Financial Times

The flow of gold is as follows: the United States exports gold to Switzerland, where it is refined and recast, and then shipped to other countries. The chart below shows that China, India, and other emerging economies that manufacture physical gold or export commodities are primarily purchasing this gold. The physical gold ultimately flows to the United States, while the gold flows to more productive regions of the world.

By "productivity," I don't mean these places are better at writing rambling reports or using complicated email signatures, but rather that they export energy and other key industrial commodities, and that their people manufacture steel and refine rare earth elements. Gold is still rising despite declining dollar liquidity because sovereign nations are accelerating the return to the global gold standard.

[Chart: Gold Import/Export Flows by Country]

Long-term investors love liquidity

Every era has its share of high-flying tech stocks. During the roaring bull market of the 1920s in the United States, radio manufacturer RCA was the darling of the tech world; in the 1960s and 1970s, IBM, which manufactured new mainframe computers, became the focus of the market; and today, AI hyperscale service providers and chip manufacturers are in high demand.

Humans are inherently optimistic. We love to predict a rosy future: every penny a tech company spends today will create a social utopia in the future. To realize this vision in investors' minds, companies burn money and take on debt. When liquidity is cheap, betting on the future becomes easy. Therefore, investors are happy to squander cheap cash today on tech stocks in exchange for the opportunity to generate huge future cash flows, thus driving up price-to-earnings ratios. So, during periods of excess liquidity, tech growth stocks experience exponential growth.

Bitcoin is a monetary technology. The value of this technology is solely relative to the devaluation of fiat currencies. The innovation of the Proof-of-Work (PoW) blockchain is brilliant, as it inherently guarantees that Bitcoin's value is greater than zero. However, for Bitcoin to approach a value of $100,000, sustained devaluation of fiat currencies is necessary. Bitcoin's asynchronous growth is a direct result of the explosive growth in the supply of the US dollar following the 2008 global financial crisis.

Therefore, I say: Bitcoin and the Nasdaq will rise when dollar liquidity expands.

The only point of contention at present is the recent divergence between Bitcoin's price and Nasdaq's.

[Chart: Bitcoin vs. Nasdaq Price Movement]

My theory for why the Nasdaq will not correct in 2025 as dollar liquidity declines is that AI has been "nationalized" by both China and the United States.

AI tech giants have been peddling this idea to the world's two largest leaders: AI can solve everything. AI can reduce labor costs to zero, cure cancer, increase productivity, and most importantly, achieve global military dominance. Therefore, whichever country "wins" in AI will rule the world. China has already bought into this, as it perfectly aligns with its five-year plan.

This kind of analysis is new in the US, but industrial policy is just as deeply ingrained as in China, only marketed differently. Trump has taken the "drug" of AI, and "winning the AI race" has become his economic agenda. The US government has effectively nationalized any component deemed helpful in "winning." Through executive orders and government investment, Trump is sluggish market signals, allowing capital to flow into AI-related fields without regard to returns. This is why the Nasdaq will decouple from Bitcoin and declining dollar liquidity by 2025.

[Chart: Nasdaq vs. Dollar Liquidity Decoupling]

Regardless of whether there's a bubble, increased spending to "win" AI is driving the US economy. Trump has pledged to keep the economy running hot, and he can't stop just because the return on these expenditures might fall below the cost of capital in a few years.

US tech investors should proceed with caution. Industrial policies aimed at "winning AI" are a prime example of burning through cash. Trump's (or his successor's) political goals will diverge from the shareholder interests of strategic companies. This is a lesson Chinese stock investors have learned the hard way. As Confucius said, "Learn from the past to understand the future." Clearly, given Nasdaq's outstanding performance, this lesson has yet to be learned by US investors.

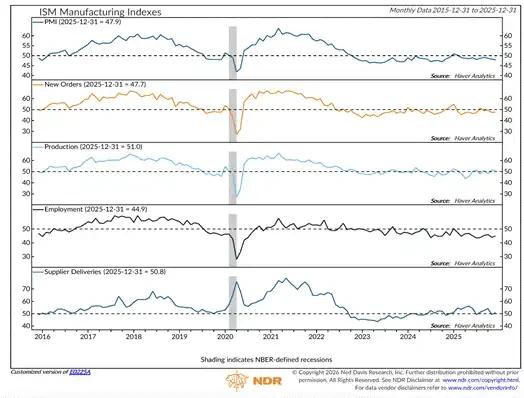

[Chart: US PMI and Economic Growth Data]

A PMI reading below 50 indicates contraction. All that GDP growth hasn't translated into a manufacturing revival. I thought Trump was doing this for white blue-collar workers? No, man, Clinton sold your jobs to China, Trump brought the factories back, but now the factory floors are covered in AI robotic arms owned by Musk. Sorry, you've been fooled again! However, U.S. Immigration and Customs Enforcement (ICE) is hiring (a hellish joke)!

These charts clearly show that the Nasdaq's rise is backed by the US government. Therefore, even with weak overall dollar credit growth, the AI industry will have all the capital it needs to "win." The Nasdaq has thus decoupled and outperformed Bitcoin. I don't believe the AI bubble is about to burst. This extraordinary performance will continue to be a feature of global capital markets until it is no longer so, or most likely until the Red Team loses the House in 2026 (as Polymarket predicts). If the Republicans are *The Jason Statham* (tech-oriented), then the Democrats are *The Flintstones* (retro-oriented).

If gold and the Nasdaq both have momentum, how can Bitcoin regroup? Dollar liquidity must expand. Clearly, I believe this will happen in 2026; let's discuss how to achieve it.

Make the economy explode

As I mentioned at the beginning, there are three main pillars supporting this year's surge in dollar liquidity:

The Federal Reserve's balance sheet will expand due to money printing.

Commercial banks will lend to strategic industries.

Mortgage rates will fall due to money printing.

[Chart: Size of the Federal Reserve's Balance Sheet]

The Federal Reserve's balance sheet will shrink in 2025 due to quantitative tightening (QT). QT ends in December, and a new money-printing program called Reserve Management Purchases (RMP) was launched at the meeting that month. I've discussed this in detail in previous articles. The charts clearly show that the balance sheet bottomed out in December. The RMP injects at least $40 billion per month, and its size will expand as the funds needed to finance the US government increase.

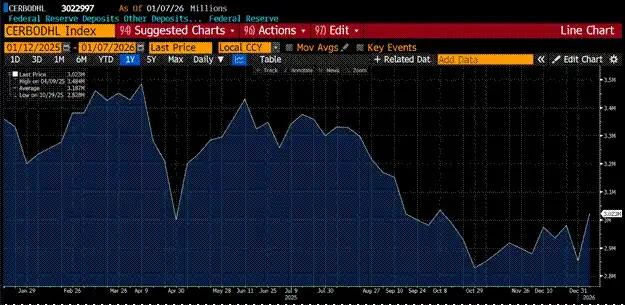

[Chart: US Bank Loan Growth (ODL)]

The chart above shows the Federal Reserve's Loan Growth Index (ODL). Starting in the fourth quarter of 2025, banks issued more loans. When banks issue loans, they create deposits out of thin air, which in turn creates money. Banks like JPMorgan Chase are very willing to lend to government-backed companies. JPMorgan Chase launched a $1.5 trillion lending program for this purpose. The process is as follows: the government invests in a company, and banks see that government backing reduces default risk, so they are happy to create money to finance that strategic industry. This is exactly what China has been doing. Credit creation shifts from the central bank to the commercial banking system, with a higher money multiplier initially, thus creating above-trend nominal GDP growth.

The United States will continue to project military power, and the production of weapons of mass destruction requires financing from the commercial banking system. This is why bank credit growth is expected to see a structural increase in 2026.

Trump is a real estate businessman; he knows how to finance the housing market. His new order allows Fannie Mae and Freddie Mac to use capital on their balance sheets to purchase $200 billion in mortgage-backed securities (MBS). This represents a net increase in dollar liquidity. If successful, Trump won't stop there. By lowering mortgage rates to boost the housing market, he will enable Americans to borrow based on home equity. This wealth effect will put voters in a good mood on Election Day, potentially leading them to support the Republican Party. More importantly, it creates more credit to purchase financial assets.

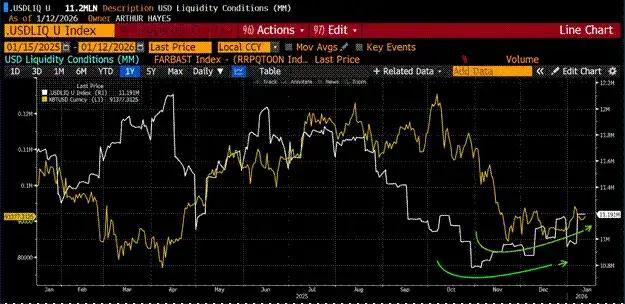

[Chart: Bitcoin and USD liquidity bottom coincide]

Bitcoin and dollar liquidity bottomed out almost simultaneously. As dollar liquidity rapidly increases for the reasons mentioned above, Bitcoin will take off. Forget about its performance in 2025; that was due to insufficient liquidity.

Trading Strategies

I am an aggressive speculator. Although my fund, Maelstrom, is nearly fully invested, I still want to increase my risk exposure because I am extremely bullish on the growth of dollar liquidity. Therefore, I am gaining leveraged exposure to Bitcoin by long on MicroStrategy (MSTR) and Metaplanet (3350 JT) without trading complex options or perpetual contracts.

[Chart: Price ratios of MSTR and Metaplanet relative to Bitcoin]

I divided the stock prices of these two companies by the price of Bitcoin, and they are currently at the bottom of their trading range over the past two years.

If Bitcoin can regain the $110,000 mark, investors will be tempted to go long on Bitcoin using these instruments. Given the leverage embedded in these companies' balance sheets, they will likely outperform Bitcoin during any upward move.

Furthermore, we continue to increase our holdings in Zcash (ZEC). The departure of the ECC developers is not a negative factor; I believe they can deliver more impactful products within their own profitable entities. I am grateful for the opportunity to buy discounted ZEC from a "weak" position.

Keep going, crypto adventurers. This world is fraught with danger, so please remain vigilant. May peace be with you—and also, a prayer to the "Cloud Fairy."