Compiled & translated by: TechFlow TechFlow

Guest: Jeff Park, Partner and CIO of ProCap Financial

Host: Anthony Pompliano

Podcast source: Anthony Pompliano

Original title: Why the Bitcoin Narrative Is Shifting Right Now

Broadcast date: February 5, 2026

Key points summary

Jeff Park is a partner and chief investment officer at ProCap Financial. In this conversation, we discussed the recent price pullback in Bitcoin, analyzed whether the market has entered a true bear market, and discussed the current interest rate environment and the role of the Federal Reserve in the economy. We also talked about the possibility of Kevin Warsh being nominated as Federal Reserve Chairman, Jeff's outlook on the precious metals market, and his warning about a type of asset that investors should avoid in the future.

Summary of key viewpoints

- We are in a bear market. Even if policies become more relaxed, it may not necessarily propel us into a bull market.

- If you've already made a good profit from your silver investment, now might be the time to move your funds to Bitcoin.

- "Positively correlated Bitcoin" may be the truly important direction for the future, as Bitcoin will rise when interest rates increase.

- We initially chose Bitcoin because we believed that scarcity could solve the problem of artificially manipulated money supply.

- I remain very optimistic about the future of Bitcoin, but this is largely because I believe that the role of government will become more centralized in the future, and Bitcoin will once again become the ultimate hedge against this system.

- The position of Federal Reserve Chairman should not be held by a socialist or nationalist. What we need is a technically skilled official who is also pragmatic enough. Warsh and Bessant happen to possess these qualities.

- If interest rates are indeed cut in the future and liquidity increases further, I believe that price fluctuations in the precious metals market may become even more volatile.

- The market outlook for silver is not optimistic. Silver's performance in the precious metals market is very similar to that of Altcoin in the cryptocurrency market.

- Kevin Warsh firmly believes that blockchain technology is not magic, but a tool that can solve many practical problems and improve efficiency, and that Bitcoin is an important part of this technological culture.

Is the Bitcoin sell-off sustainable?

Anthony Pompliano :

Jeff, Bitcoin has been falling recently, and I personally think the market may continue to fluctuate or even decline further; we may have already entered a bear market. Bitcoin's 40% drop has attracted a lot of attention. What are your thoughts? Do you think we are currently in a bear market? Do you think the decline in Bitcoin is sustainable?

Jeff Park :

I believe we are indeed in a bear market, and it has been going on for some time now. One thing to remember is that in the past, people liked to view Bitcoin as a hedging tool, believing it was positively correlated with global liquidity—that is, increased global liquidity would generally be beneficial for Bitcoin. However, the truth is, this relationship has long been broken.

In the cryptocurrency space, we often tend to believe that history simply repeats itself. This idea is actually a compromise with behavioral biases, such as assuming that Altcoin always rise after Bitcoin, believing in the so-called "four-year cycle," or assuming that quantitative easing (QE) and low interest rates will always benefit Bitcoin. But the world is constantly changing, and many circumstances are different from the past. Now, we need to re-examine a crucial assumption: are quantitative easing, global liquidity expansion, and low interest rates truly beneficial to Bitcoin? While this may have been true in past cycles, the situation may be different now.

Currently, global liquidity is actually steadily increasing. According to data tracked by Michael Howell, global liquidity will reach approximately $170 trillion by 2025, originating from China and the United States, and may accelerate further in the future. We can see this trend in the general rise in asset prices, such as the strong rebound in the metals market and corporate credit spreads reaching historic lows. This suggests that Bitcoin should have participated in this rise, but it hasn't, indicating that some fundamental mechanisms may have changed. Therefore, I believe we are indeed in a bear market, and it may have started as early as mid-2025, when the Federal Reserve's balance sheet begins to shrink, especially as the Treasury begins to rebuild the Treasury General Account (TGA).

Looking ahead, we may need to accept the reality that even if policies become more relaxed, it may not necessarily propel us into a bull market. However, this actually makes me somewhat optimistic about potential catalysts for Bitcoin's future rise.

I previously mentioned the concepts of "negatively correlated Bitcoin" and "positively correlated Bitcoin." The "negatively correlated Bitcoin" we're familiar with refers to a situation where, in an environment of low interest rates and loose monetary policy , the prices of risky assets rise , and Bitcoin rises accordingly. However, there's another possibility: "positively correlated Bitcoin," which I believe is the ultimate goal—that is, when interest rates rise, Bitcoin will actually rise as well . This scenario is completely opposite to the theory of quantitative easing, and its underlying logic questions the reliability of the risk-free rate. In this case, we are essentially saying that the risk-free rate is no longer risk-free, the dollar's hegemony is no longer absolute , and we can no longer price the yield curve in the old ways. This means we need a completely new model, such as a basket of currencies based on commodities, and Bitcoin may be precisely this hedging tool.

Therefore, I believe this "positive correlation" with Bitcoin may be the truly important direction for the future . The current money supply and financial system are already problematic, and we know that the cooperation between the Federal Reserve and the Treasury is insufficient to advance national security agendas. All of this makes me feel that to pull Bitcoin out of its current slump, we may need to abandon old perceptions and return to Bitcoin's essential value— we initially chose Bitcoin because we believed scarcity could solve the problem of artificially manipulated money supply . Therefore, while global liquidity is increasing, it is not actually a friend of Bitcoin.

Federal Reserve vs. White House: Is Bitcoin looking forward or backward?

Anthony Pompliano :

Jeff, I think there are two different perspectives that can be used to analyze the current economic situation.

First, historically, we have always considered monetary policy to be the primary driver of the economy and asset prices. However, the current US administration seems to be attempting to wrest control of the economy from the Federal Reserve . They are doing this through deregulation, tax cuts, tariffs, and attempts to depress the dollar. Simultaneously, they are leveraging the advancements in artificial intelligence to boost economic growth. The Federal Reserve, whether voluntarily or involuntarily, appears to be somewhat passive, trying to understand the various trends in the economy and how to respond.

Therefore, the economy now seems to be in a dynamic power balance between the Federal Reserve and the White House. We need to figure out whether the Federal Reserve or the White House is leading the direction of economic policy.

Secondly, I've also been pondering whether Bitcoin's market behavior is more forward-looking or reflects current or past economic conditions. When you mentioned the psychology of Bitcoin holders, you described them as "driving while only looking in the rearview mirror," believing that the past four-year cycles will always repeat themselves, so there's no need to look to the future, just look at past patterns. But I feel your viewpoint is more like a reminder that we should "look at the future through the windshield," which might be a better way to analyze the situation.

So the question arises: is Bitcoin's performance based on current economic conditions or predicting future developments? For example, in 2020, many investors bought Bitcoin and gold because they anticipated impending inflation; markets are often forward-looking. If Bitcoin is falling now, does this mean there's a greater risk of deflation? Or is it warning us of other potential problems ? How do you view the power balance between the Federal Reserve and the White House? And is Bitcoin looking to the future or looking back at the past? How should we interpret current price movements within a larger context?

Jeff Park :

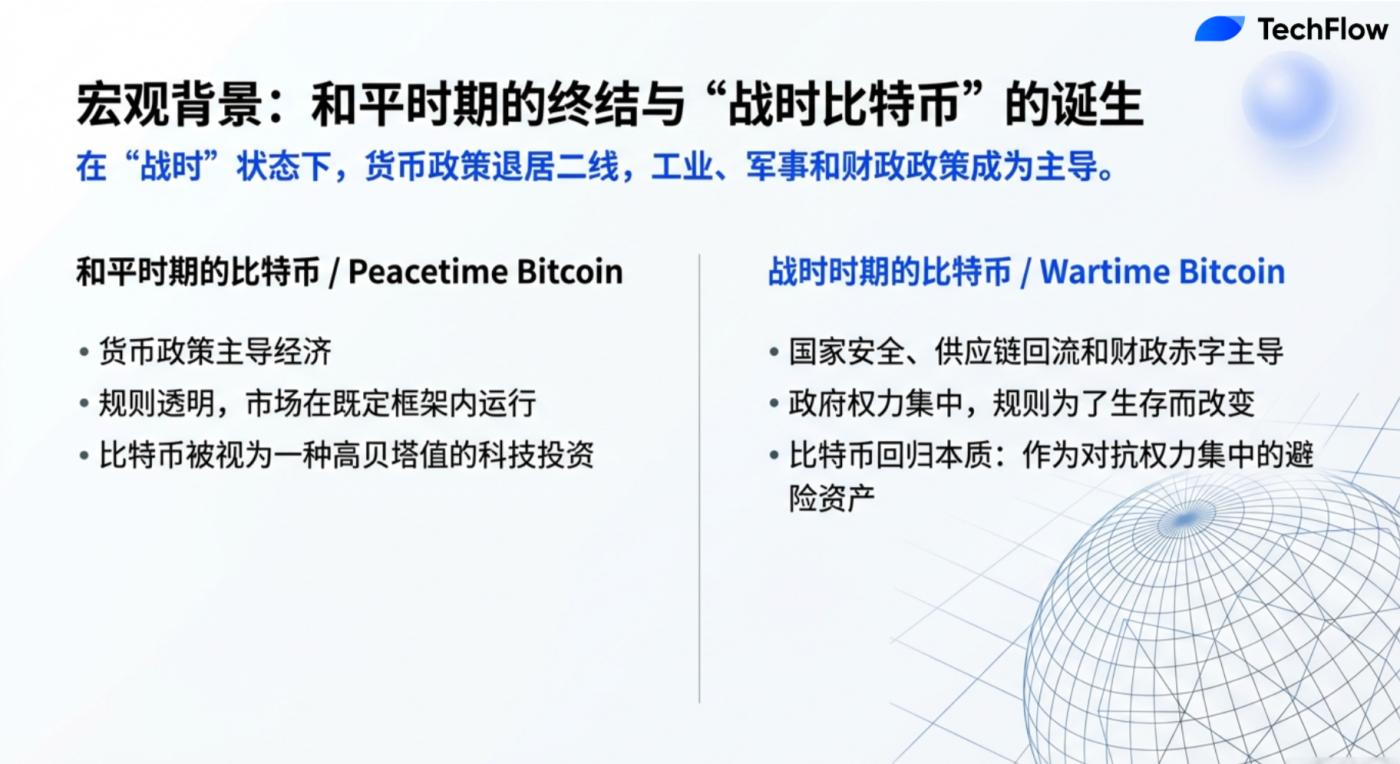

That's a great question. I have an interesting concept in mind that I call "peacetime Bitcoin" and "wartime Bitcoin." In times of peace and prosperity, we expect the monetary system to function properly and investment frameworks to operate in the traditional way. This is "peacetime Bitcoin," which is more closely linked to inflation and used as a hedge against it .

But "wartime Bitcoin" is entirely different. In "wartime," the main force driving economic growth is no longer monetary policy, but a combination of industrial, military, and fiscal policies . This has happened historically—in times of crisis between democracies and more authoritarian governments, the importance of monetary policy often gives way to the priority of power struggles.

Therefore, your point about Bitcoin's future positioning is correct. Part of the reason is that the world seems to have become more centralized during the Trump administration. In the past, we were full of hope for decentralization, viewing the distribution of resources and the establishment of checks and balances as virtues, and Bitcoin and cryptocurrencies embodied this idea. However, a closer look at recent US cryptocurrency policies reveals that it is actually moving towards a more centralized model. For example, stablecoins are bringing banks into the centralization of profits; tokenization is also being used more as stocks than long-tail assets; coupled with the centralized nature of the Trump administration itself, all of these factors have given Bitcoin a kind of "centralized" energy.

Bitcoin's value has always lay in its decentralization and censorship resistance; it represents a form of "free money." American investors have many other options, such as silver, metals, and AI-themed investments. Those who truly need Bitcoin are those living under oppression and facing capital controls. If you believe the future world will be more divided, more chaotic, and even subject to more capital controls, then Bitcoin's importance will become even more pronounced.

Therefore, I remain very optimistic about the future of Bitcoin, but this is more because I believe that the role of government will become more centralized in the future, and Bitcoin will once again become the ultimate hedge against this system.

Kevin Warsh and the Future of the Federal Reserve

Anthony Pompliano :

You mentioned Kevin Warsh, who is apparently the nominee for the new Federal Reserve Chair. He has expressed some very positive views on Bitcoin, believing it won't compete with the dollar but rather has a unique role to play in portfolios. What are your thoughts on his potential as Fed Chair? How might he influence the future development of Bitcoin?

Jeff Park :

To be honest, I really admire Kevin because I think he's an expert with a deep understanding of how things work. He understands that sometimes you need to break existing patterns to take the next step, and he knows that you can only find solutions by truly understanding the root of a problem and diagnosing it correctly. You can't just change for the sake of change, and those who truly understand things are often reluctant to change the status quo easily. Having this kind of innovative thinking requires immense courage, and Kevin happens to possess this quality.

Furthermore, he is an outstanding technology expert . In one of my conversations with him, I vividly remember his passion for cryptocurrency. He mentioned that there are many "hypocrites" in the world who believe technology is something magical, but don't actually understand its essence; they blindly bet without sound reasoning. In contrast, Kevin firmly believes that blockchain technology is not magic, but a tool that can solve many practical problems and improve efficiency, and that Bitcoin is an important part of this technological culture.

This is crucial because many technologists don't truly understand how technology works. For them, imagining the space for technological innovation is counterintuitive. For example, when we talk about productivity growth, the Federal Reserve might not realize the deflationary effects of artificial intelligence. This cognitive gap exists because many people cannot envision the future as drastically different from the past as Kevin Warsh does. Therefore, I believe he is first and foremost a technology expert, and this is especially important today. I think we need more leaders with his technological vision in the field of monetary policy.

Furthermore, Kevin has extensive experience working at the Federal Reserve. A review of his past actions reveals that he genuinely believes in the value of the Fed as an institution. He is not one to advocate ending the Fed's independence, but he understands why that independence is challenged and knows how to reshape the institution to regain public trust. He once said something that impressed me : "Inflation is a choice." In contrast, we see current Fed Chairman Powell and others seemingly always looking for external excuses for inflation, such as "inflation is because of tariffs" or "inflation is because of the Ukraine war." They are almost unwilling to admit that inflation is a choice for the Fed, when in fact, inflation is a policy choice and one of the core missions of the Fed.

Regarding inflation, it's important to clarify that inflation and nominal price changes are two different things . Many people confuse the two, thinking that a 5% increase in the price of a good constitutes inflation. However, that's merely a price change, and price changes can be caused by various factors, such as war or tariffs. True inflation is a dynamic concept; it's the long-term trend of the rate of price change, not a one-off price fluctuation. The Federal Reserve's role is not to monitor monthly price changes, but to manage the long-term trend of these price changes. This point is often overlooked.

I strongly agree with Kevin Warsh's point that "inflation is an option," because the Federal Reserve actually has all the tools to control inflation, if they are willing to take action.

Anthony Pompliano :

Interestingly, two seemingly contradictory situations can actually coexist. I think everyone always wants to find a simple answer, such as inflation or deflation? High inflation or low inflation? But in reality, economic systems are extremely complex, and Bitcoin seems to simplify these complex economic relationships. You don't need to learn all these complex economic principles; you only need to understand supply and demand: if more people want something, its price will rise; if demand decreases, its price will fall. Bitcoin's philosophy seems to be reimagining the monetary system. If so, are they trying to make this system simpler? Are they hoping to simplify this complex economic machine into a system that anyone can easily understand?

Jeff Park :

Yes, the system is inherently very complex, and I'm not sure it can truly be simplified. However, I think they should make it more transparent and honest. Americans have lost confidence in the current monetary system not only because it has become complex, but also because of its lack of transparency. I believe one of Kevin Warsh's tasks is to change the way the Federal Reserve uses its balance sheet while addressing the glaringly obvious transparency issues in the current system.

For example, at the Federal Reserve meeting in January of this year, Powell was asked a question about the relationship between the value of the dollar and the interest rate setting mechanism. Given the significant strengthening of the dollar, this was clearly an important question, as the core of interest rates is that the value of the benchmark currency directly affects long-term yields and interest rates. However, Powell's answer was: "We don't focus on the level of the dollar when we make policy." To some extent, he may have been trying to simplify the issue, as this wasn't his area of expertise. However, this statement overlooks an important reality: the value of the dollar is indeed closely related to interest rate policy. But in fact, both can be considered simultaneously.

This is why I am optimistic about the possibility of a new agreement between the Federal Reserve and the Treasury. Bessant and Warsh have an opportunity to redefine this agreement. At the heart of the matter, we return to the Triffin Dilemma: the inherent contradiction exists between the US dollar, as the global reserve currency, needing to meet international reserve demands and ensure domestic economic stability.

Therefore, what we need is not absolute independence for the Federal Reserve, but rather a functional interdependence between the Fed and the Treasury. I believe we need to move away from the notion that "the Fed's independence is being challenged" and instead accept that "the Fed must establish a functional collaborative relationship with the Treasury" to formulate more rational policies. Once we achieve this, the Fed will have taken a significant step and regained public trust in its role.

Anthony Pompliano :

What do you think of Warsh and Bessant's backgrounds? They both come from the same system and studied under the same mentor, so they can be said to have the same way of thinking and working philosophy. Perhaps they are among the greatest risk-takers of all time.

Jeff Park :

This excites me greatly. I've expressed my opinion publicly online many times, and since last year, I've consistently maintained that Warsh must become Chairman of the Federal Reserve. This is a historic moment because you find two people who trust and know each other deeply, who have both worked under arguably the greatest market practitioners of all time, and now they have the opportunity to make real difference. The importance of trust at this level cannot be underestimated.

This reminds me of some previous situations, like when Warsh was a candidate, then Hasset came along and became a candidate, and then it was Rick Reer's turn, but actually, throughout the whole process I kept thinking, "You guys are ignoring the bigger picture."

This may seem like a decision by Trump, but in reality, who ultimately controls this decision? It's Bessant. Who will he choose to cooperate with? Who will he trust? Who can realize his vision and changes for the country's future? The answer has always been only one: Warsh. When you realize this, you see a very clear and powerful moment. Because of this relationship of trust, we are now able to accomplish things on the global stage that were previously impossible. I am very excited about this.

Of course, I know many people are prejudiced against billionaires, believing they only care about their own interests and don't consider ordinary people, but I hold the opposite view. I believe we should expect these people with enormous resources to do something meaningful. Because if it's not these resourceful individuals driving change, it might be some ill-intentioned people taking control. Rather than that, let those who no longer need to make money for themselves drive systemic improvement. I believe that for Bessant and Warsh, the last thing they care about is how to make more money for themselves; what they're truly focused on is how to fix the entire system.

That's why I'm very optimistic about them. They have a deep understanding of the market because they are practitioners in the capital markets themselves. They know that while the Federal Reserve has its advantages as an institution, many problems still exist. And their intelligence, integrity, and clear communication skills enable them to drive change—this combination is truly ideal.

In my view, the position of Federal Reserve Chair should not be held by a socialist or nationalist. What we need is a technically skilled official who is also pragmatic enough. Warsh and Bessant happen to possess these qualities, and I have high hopes for their future.

Anthony Pompliano :

What I find interesting is the collaboration between Warsh and Bessant. They not only have a deep understanding of the American financial system but also a global perspective. For example, some of the measures Bessant took in Argentina proved to be very wise. Although they caused considerable controversy at the time, with some even questioning why money was being spent on such matters, in retrospect, those decisions were indeed farsighted.

The United States has always been a nation steeped in adventure, always embracing a "let's build" mentality. However, from a monetary policy perspective, the US is also attempting to cut unnecessary spending and implement reforms. This mindset requires people who truly understand probability and risk. I think that's the key point you mentioned: these are the people who dedicate their lives to studying these issues, right?

When Bessant was nominated, I wasn't sure how many people thought he would be exceptional. People might have thought he was intelligent, but there wasn't necessarily an overwhelming consensus that he would be outstanding. However, looking back objectively now, he is probably one of the best Treasury Secretaries I've ever seen in my lifetime. Warsh, on the other hand, complemented his weaknesses, creating a synergistic effect. Warsh served as a Federal Reserve Governor during the global financial crisis, possessing a deep understanding of the Fed's inner workings. He later applied that experience as a trader. Now, he returns to the system, bringing a different perspective and experience, and their existing trust bridges their differences.

Jeff Park :

Yes, I think a key point you raised is that leaders need the ability to think systematically. Because in economic policy, actions in one area can influence outcomes in another. To understand the probability of such interactions, one must realize that monetary policy is not isolated. It is actually closely related to fiscal policy and industrial policy . For example, Trump wanted to bring manufacturing back to the US and increase investment in the semiconductor industry. These three are like a symphony orchestra; they must coordinate to achieve the ultimate goal, and to do so requires multi-dimensional thinking.

Unfortunately, most academics and those who have never worked in the for-profit sector often lack this kind of systemic thinking. The nonprofit sector doesn't operate by assessing the resilience of multiple variables, let alone building complex systems. In fact, I even believe that centralized, top-down government models often mechanically execute orders and allocate resources, lacking accountability . They simply spend money without truly reflecting on whether these investments have yielded any real results. This capacity for reflection and critical thinking is typically cultivated through experience in the for-profit sector. Frankly, it also requires a great deal of self-awareness.

Repeating past practices won't solve future challenges; we need to forge a completely new path. To achieve this, leaders must possess sufficient credibility, which stems from their authority as systemic thinkers. This cannot be cultivated from a closed, rigid institution. The combination of Warsh and Bessant fills me with confidence for the future. They are not only technology-expert leaders but also pragmatic and experienced in the markets. They understand market dynamics, know the strengths and weaknesses of the Federal Reserve as an institution, and are capable of driving change through clear communication and integrity. This combination is ideal. In my view, the position of Federal Reserve Chair should not be held by someone with an overly extreme ideology. What you need is a leader who is both technically savvy and pragmatic, and Warsh and Bessant perfectly fit that description.

Why are precious metal prices soaring?

Anthony Pompliano :

The precious metals market has been very active recently, with gold, silver, and even copper and platinum experiencing significant price fluctuations, sometimes surging, and sometimes rising again after a slight pullback. What exactly is happening behind the scenes?

Jeff Park :

This reflects a current market frenzy, which I believe is one reason why we need to rethink our Bitcoin investment logic. While this surge hasn't directly impacted Bitcoin, it has been particularly pronounced in the precious metals market. The reason, I think, is the currently very loose global liquidity environment. Frankly, if interest rate cuts do occur in the future, further increasing liquidity, I believe price volatility in the precious metals market could become even more volatile. Some funds may flow into Bitcoin, or they may not, but the key point is that this market phenomenon is already happening.

Silver, in particular, seems to be a primary target for retail investors right now, a situation that reminds me of the Altcoin market. In fact, silver and Altcoin share many similarities; silver's position among precious metals is analogous to Ethereum's position among cryptocurrencies. While I don't intend to offend the Ethereum community, this analogy does hold some merit.

Analyzing the price fluctuations of most commodities can be attributed to two fundamental factors: supply and demand . From the supply side, silver is actually a byproduct of mining other metals. Many people may not know that there are almost no mining companies in the world that specialize in mining silver; most silver is produced as a byproduct of mining metals such as zinc or copper—it's essentially a "freebie." In the world of cryptocurrency, this is similar to when you're doing yield mining. You're initially investing in Ethereum, but because you use Ethereum to participate in mining activities on certain chains, you receive some random tokens as extra rewards. These tokens, like silver, represent additional income.

Therefore, miners don't specifically mine silver because of its price; it's merely a byproduct of mining other metals. From this perspective, the supply of silver is actually quite large. Unlike the scarcity of Bitcoin, the supply of silver is relatively abundant. Ultimately, the market will find a reasonable price for silver, and because silver is just a byproduct of other metals, its price may be suppressed due to ample supply.

From the demand side, while some have mentioned the promising applications of silver in industries such as artificial intelligence and solar panels, silver is actually a commodity that can be replaced. Silver is favored for its high conductivity, but copper's conductivity is only about 5% lower than silver's. This means that although silver has superior performance, its high price is not enough to make it the only choice. In fact, due to the rising price of silver, many solar panels have begun to use copper instead of silver.

Furthermore, silver is not a reserve asset, and no central bank buys it. From a supply perspective, silver production is not entirely determined by its market price; rather, it is a byproduct of mining other metals. Therefore, all things considered, I believe the market outlook for silver is not optimistic.

This reminds me of the Altcoin market. Silver prices are highly volatile and strongly correlated with gold prices, a relationship similar to how Altcoin performance often depends on Bitcoin's rise. However, most Altcoin prices eventually revert to supply-demand equilibrium. For investors who have participated in the cryptocurrency market over the past few years, there's a lesson to learn: silver's performance in the precious metals market is remarkably similar to that of Altcoin in the cryptocurrency market.

Anthony Pompliano :

So you mean the price of silver might see a significant pullback?

Jeff Park :

Yes, if you've already made a good profit from your silver investment, now might be the time to move your funds to Bitcoin.