With quarterly settlements reaching $11.9 trillion, the USDC's size is approaching half of the US GDP.

Written by: Mahe, Foresight News

On February 25th, Circle announced total revenue and reserve income of $2.7 billion for fiscal year 2025, a 64% increase. Following the announcement, CRCL shares surged by as much as 35% from $61, closing at $83, marking its largest single-day gain since October 2nd of last year. The market voted with its own money, acknowledging the significance of this financial report.

It's worth noting that after reaching a high of $298 following its IPO last June, CRCL's stock price steadily declined, even hitting a historic low of $49.90 on February 5th. This strong rebound is, to some extent, a correction of the market's previously excessive pessimism.

The circulating supply of USDC is projected to reach $75.3 billion by the end of 2025, representing a year-on-year increase of 72%.

Let's look at the most crucial metric: USDC's circulating supply reached $75.3 billion at the end of the year, a year-on-year increase of 72%. What does this figure mean? Against the backdrop of a slowdown in the overall stablecoin market, Circle's market share actually expanded by 4.26 percentage points, reaching 28%.

The logic behind this ebb and flow is simple: Tether's compliance controversies have given USDC an opportunity, while Circle's long-term investment in regulatory compliance is translating into market share.

On-chain USDC transaction volume reached $11.9 trillion in Q4, a staggering 247% year-over-year increase. This figure is almost half of the US GDP. While there is a significant amount of wash trading and arbitrage activity in on-chain transactions, the 247% growth rate still demonstrates the rapid increase in USDC's penetration as a settlement infrastructure.

On the revenue side, total revenue in Q4 was $770 million, a year-over-year increase of 77%, exceeding the average analyst estimate of $748 million from FactSet. Reserve income, at $733 million, a year-over-year increase of 69%, contributed the vast majority of revenue.

Here's an explanation of the logic behind reserve income: Circle uses the USD deposited by users to purchase low-risk assets such as short-term US Treasury bonds, earning interest rate differentials. The reserve return rate in Q4 was 3.8%, a decrease of 68 basis points year-over-year, but the doubling of USDC circulation completely offset the impact of declining interest rates.

What truly excited the market was the explosive growth in profits. Adjusted EBITDA reached $167 million, a staggering 412% year-over-year increase, far exceeding analysts' expectations of $130 million. The RLDC profit margin (revenue minus distribution costs) jumped from 30% to 40%, a full 10 percentage points increase.

Economies of scale are beginning to emerge, and the marginal cost of issuing an additional US dollar (USDC) is rapidly decreasing.

The Arc mainnet is expected to launch within 2026.

There are several noteworthy business signals in the financial report.

First, let's look at the progress of the Arc public testnet. With over 100 institutions participating, nearly 100% uptime, 0.5-second transaction finality, and an average of 2.3 million transactions per day, these figures may seem like technical specifications, but they reflect the real demand for on-chain settlement from traditional financial infrastructure. Visa's announcement that US issuers and acquirers can use USDC to settle with Visa signifies that USDC is beginning to penetrate the underlying layers of the traditional payment system.

It's worth mentioning that Circle mentioned in its report that it plans to launch the Arc mainnet within 2026.

Secondly, there's the expansion of the Circle Payment Network (CPN). 55 financial institutions are registered, with an annualized transaction volume of $5.7 billion. This number is still small, but the direction is crucial—Circle is transforming from a simple stablecoin issuer into a payment network operator, a business model with far greater potential than simply collecting interest.

Regarding the Euro stablecoin EURC, its circulating supply reached €310 million, a year-on-year increase of 284%. The demand for Euro stablecoins is being activated following the implementation of the MiCA regulatory framework. The assets under management of USYC (tokenized US Treasury bonds) reached $1.5 billion, a month-on-month increase of 111%, indicating increased institutional acceptance of on-chain yield products.

The financial report wasn't all good news. For the full year, Circle recorded a net loss of $69.5 million, primarily due to $424 million in share-based compensation expenses triggered by the IPO. Excluding these non-cash expenses, adjusted EBITDA for the full year was $582 million, a 104% year-over-year increase.

The rate of return on reserves has fallen from 4.1% to 3.8%, and this trend is likely to continue.

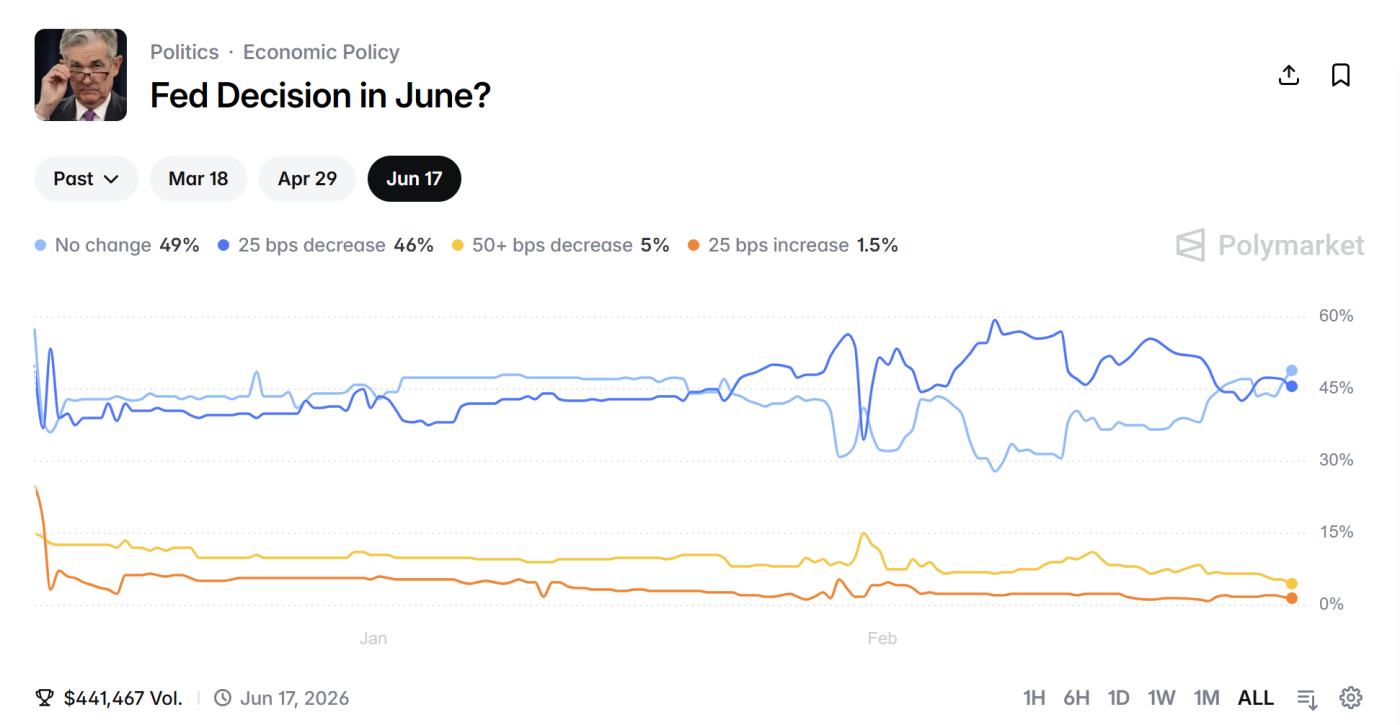

According to the latest data from Polymarket, the probability of the Federal Reserve not cutting interest rates was 97% in March, 86% in April, and 46% in June.

If the Federal Reserve chooses to cut interest rates again in June this year, Circle's interest rate spread income will inevitably be under pressure.

The management's guidance for 2026 also reflects this—the revenue margin guidance after deducting distribution costs is 38%-40%, basically maintaining the status quo, indicating that the room for profit margin expansion may already be limited.