This article is machine translated

Show original

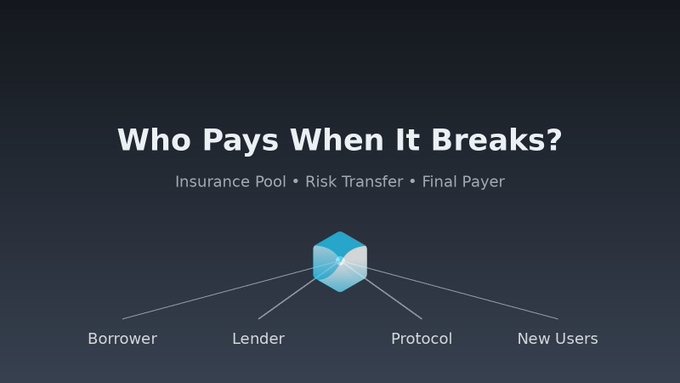

The proposed bad debt insurance pool raises the question: if a crisis occurs, who will be left holding the bag?

Recently, the atmosphere on Twitter has been somewhat somber.

Market volatility, tightening liquidity—everyone is contemplating a solution.

On this stage, some are anxious, some are numb, and some have given up. Humans are actually quite fragile; the body only needs a little energy to survive, but what's truly difficult to settle is your—corrupted soul.

We used to discuss returns; now, more people are discussing who will bail us out if things go wrong.

After working in DeFi for a while, you'll find that what truly determines your long-term survival is never the annualized return. It's who, when bad debts occur in the system, is ultimately footing the bill.

@TermMaxFi's recently recurring discussion about insurance pools is actually focused on this point. It's not a new approach; it's an endgame question.

1. First, clarify the current risk hierarchy.

TermMax's risk path is currently clear and traceable.

Fixed-rate lending + maturity structure:

When pressure arises, the collateral bears the risk first, then liquidation waterfall occurs.

Only in extreme cases is physical delivery and time-lock buffering triggered.

The order is simple:

Borrowers bear the risk first, then collateral assets, then market liquidity, and finally the agreement layer.

In other words, the risk is not hidden, but layered and placed in different locations.

2. If an insurance pool is added, the risk will not disappear, but will only be redistributed.

The role of the insurance pool is to smooth out extreme situations, but it will not create safety out of thin air.

It only changes who bears the risk last. Different sources of funds lead to completely different results:

From borrowers → increased borrowing costs

From lenders → diluted actual returns

From the agreement treasury → using future growth as a safety net

From new users → postponing and transferring historical risks.

The insurance pool itself is neutral; the key is where the money comes from.

3. A frequently overlooked detail: Risk is transferred, not eliminated.

Once an insurance pool exists, the risk in the system begins to migrate.

From explicit losses to implicit sharing,

From individual positions to collective sharing.

Many traditional financial products operate this way:

They appear more stable on the surface, but long-term returns are gradually eroded.

The advantage of the on-chain world is inherent transparency.

Therefore, who provides the funds and who bears the consequences must be clearly stated on the chain.

4. If an insurance pool is indeed introduced in the future, at least three things must be recalculated:

Triggering conditions:

Must be verifiable on the chain, not subjectively determined.

Payment order:

Is it intervention before liquidation or a last-minute guarantee after liquidation?

These two designs are completely different.

Where does the funding come from?

Is it continuously injected?

Will it be misappropriated?

All of these must be traceable.

5. A statement I've been pondering recently:

The maturity of a protocol isn't determined by the level of returns.

It's determined by whether each participant knows their position in advance when the system incurs losses.

6. Why this kind of discussion is important:

Many projects avoid the endgame issue, but systems that truly want to exist long-term must face it.

When a protocol begins to publicly discuss who will ultimately pay the price, it means it has moved from focusing on returns to pricing risk. This step is difficult but necessary. This is also why I've recently been seriously revisiting #TermMax.

#ProjectResearch This tweet does not constitute any investment advice. Cryptocurrency involves risk; invest with caution!

twitter.com/Domingo_gou/status...

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content