"This year, we have been able to fully meet the needs of every customer."

South Korean chip giant SK Hynix stated that its current DRAM and NAND inventory is only about four weeks' worth, at historically low levels. From cloud providers like Google and Microsoft to AI companies like OpenAI, and consumer electronics manufacturers, all customers are unable to obtain sufficient supplies.

Price increases are inevitable. Starting in the third quarter of 2025, SK Hynix raised its HBM3E prices by 15%-20%, with DDR5 16Gb chips seeing a single-month price increase of up to 102%. From November, all DRAM categories saw price increases, with NAND contract prices rising accordingly. In January 2026, prices will rise again significantly, by 20%-60%.

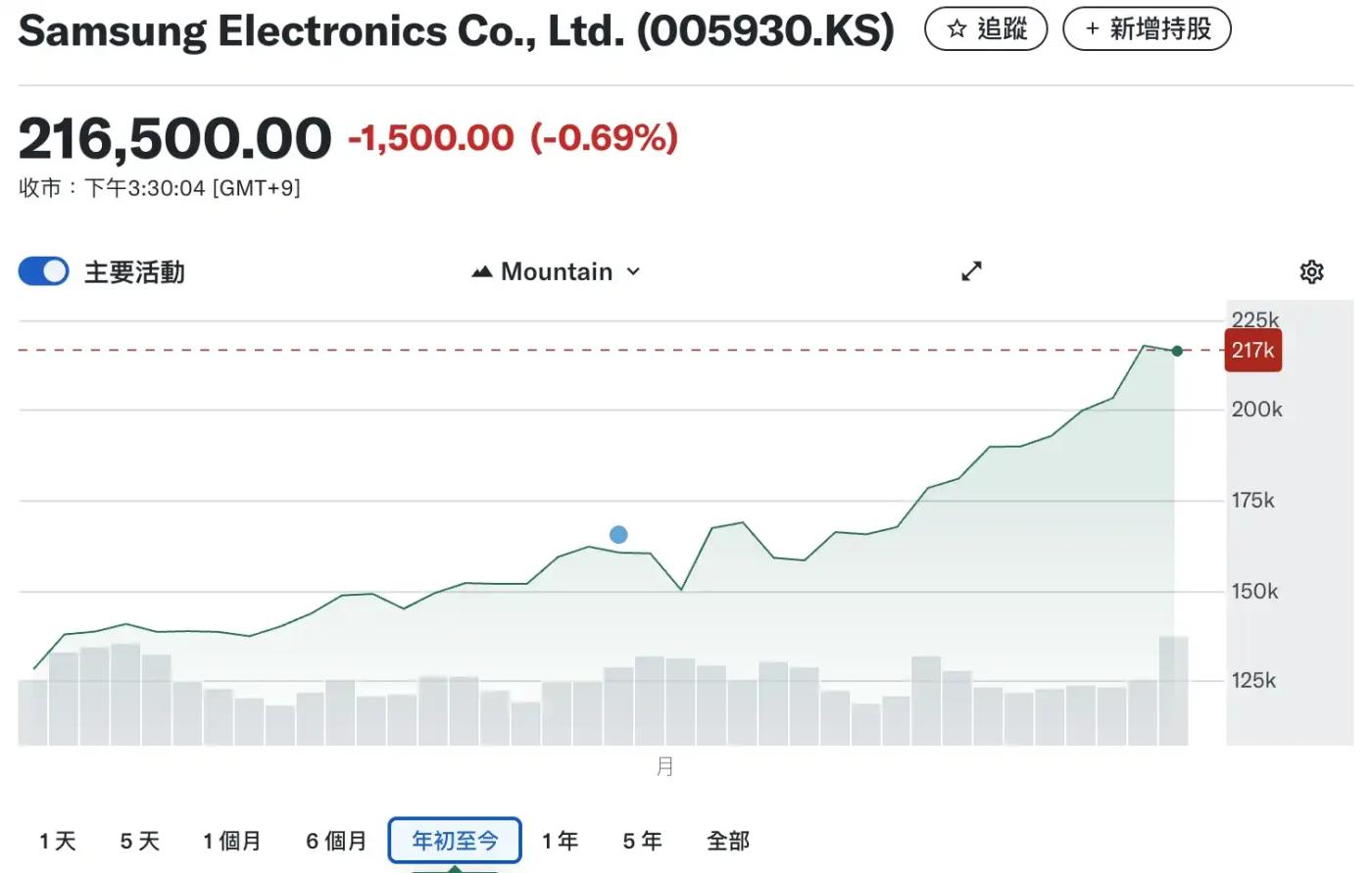

The rise in stock prices was inevitable. Since the beginning of 2025, SK Hynix's stock price has surged approximately sixfold, while the stock price of another South Korean chip giant, Samsung Electronics, has increased nearly fourfold.

This led to the South Korean stock market's KOSPI index surpassing the 6,000-point mark for the first time, and the total market capitalization of the South Korean stock market exceeding US$3.76 trillion, an increase of approximately US$2.23 trillion since the beginning of 2025. It surpassed both the German and French stock markets, historically entering the top ten globally, rising to ninth place. Since 2026, the index has accumulated a gain of nearly 45%, making it one of the best-performing major stock markets globally.

South Korea, a small country, whose stock market had long been neglected by overseas funds due to its low valuation, has now become the focus of the global capital market, and has also taken away the attention of South Korea's young people who were originally crazy about crypto.

Samsung and Hynix repricing

In the era of consumer electronics, the industry paradigm represented by Apple dominated for two decades.

Foxconn, Apple's largest contract manufacturer, employs over 1.4 million workers in China, placing it at the bottom of the "smile curve." Design, branding, and sales occupy the two ends of the curve, with profits rising upwards. This results in a stable profit distribution structure: downstream (OEMs/platforms) reap the rewards, while upstream gets the scraps. This is because upstream suppliers are numerous and easily substitutable; product definition is controlled by brand manufacturers; demand is concentrated in the end-user market; and switching costs are low.

Many Chinese manufacturers take pride in being "Apple accessory manufacturers," but from an investment perspective, there is a consensus that it's better to buy Apple products than Foxconn products.

However, when all four conditions—highly concentrated technology, slow capacity expansion, strong downstream dependence, and no short-term alternatives—appear simultaneously, the upstream supplier transforms from a "component supplier" into a "system bottleneck." Consequently, the upstream gains pricing power.

This is exactly what is happening in the current AI industry, specifically in the HBM (High Bandwidth Memory) sector.

For over a decade, the semiconductor industry has accepted the premise that the bottleneck to computing power lies in the computing chip itself. However, large-scale model training has shattered this perception. As the scale of parameters grows from billions to trillions, GPUs have encountered a more pressing issue: no matter how fast they compute, they still need data to be fed in. HBM (High Bandwidth Memory) determines whether a GPU can operate at full capacity; whether cluster efficiency is maximized; and whether the cost per unit of computing power can be reduced. It has become the "vascular system" of AI chips.

The more advanced the GPU, the deeper its reliance on storage. Taking NVIDIA as an example, from the A100 to the H100, then to the H200 and subsequent generations, the capacity and bandwidth of HBM (Hardware Bus) tied to each generation of GPUs have increased progressively. As computing power doubles, HBM usage almost doubles in tandem. The cost of HBM accounts for an increasingly larger proportion of the overall card's Bill of Materials (BOM).

Globally, only a handful of players truly possess the capability for large-scale mass production: Samsung Electronics, SK Hynix, and (relatively smaller) Micron Technology. Apple needs Samsung, and Nvidia needs Hynix.

When demand grows exponentially while supply cannot be released quickly enough, price elasticity is amplified infinitely. In the traditional PC era, CPUs/GPUs took the lion's share of profits, while storage had strong cyclicality and weak pricing power. However, in the AI server era, HBM has become an irreplaceable component. When a component is both irreplaceable and has limited supply, it means it has absolute pricing power, and it almost inevitably obtains excess profits.

The repricing of Samsung and SK Hynix became the main theme in most financial markets, including South Korea. This theme was even more alluring than cryptocurrencies.

South Korean retail investors plunge into semiconductors

If you opened a chat window among young people in South Korea late at night in 2023 or 2024, Bitcoin would definitely be a frequent topic of conversation. South Korea has long been one of the world's most retail-driven cryptocurrency markets, playing a pivotal role.

2026 will be the fourth year since LUNA's collapse. Do Kwon, the last person to bring South Korea's financial industry to its forefront, has already been sentenced to 15 years in prison. This year, the Year of the Fire Horse (丙午火马), is a year of intense fire, and the AI industry is still experiencing explosive growth. South Korea, geographically associated with fire, is clearly experiencing an excess of this fire element.

When the editor of BlockBeats recently opened Naver's investment forum, most of the posts were about "삼성전자" and "SK하이닉스". Samsung and SK Hynix.

South Korean investors, who were once keen on highly volatile Altcoin, are now reallocating their funds to domestic and international stocks, especially those related to artificial intelligence and robotics.

According to Bloomberg, trading volume on South Korean cryptocurrency exchanges plummeted by approximately 65% year-on-year in January. In stark contrast, the KOSPI, a core benchmark for the South Korean stock market, saw a 221% surge in trading volume during the same period. Margin balances at securities firms have exceeded 30 trillion won (approximately US$20.8 billion).

South Korean youths haven't changed their speculative nature, but they've shifted their focus.

This sign was already evident by the end of 2025.

Upbit's trading volume in 2025 fell by 80% compared to the same period in 2024, and the activity of the Bitcoin-Korean Altcoin every day are now talking about "AI semiconductor concept stocks".

This migration also subtly resonated with the political atmosphere. During his campaign, incumbent President Lee Jae-myung boldly proposed the "KOSPI 5000" goal. Rumors circulate that he repeatedly lost money in the stock market during his youth, and this experience of being "fleeced" became a driving force behind his push for financial reforms.

Furthermore, Lee Jae-myung was very clear about one thing: whether the stock market could reach 5000 ultimately depended on whether corporate profits could improve. Since the South Korean stock market's weighting was highly concentrated in leading technology and semiconductor companies, he focused his investment on these sectors.

Upon taking office, he quickly released strong signals of support for the capital market: establishing the "KOSPI 5000 Special Committee"; pushing for amendments to the Commercial Code; strengthening rules for equalizing shareholder rights; and reinforcing board accountability. On his eighth day in office, he made a special trip to the Korea Exchange. His goal was singular: to ensure that South Korean residents' money remained in the stock market long-term.

As for how high the South Korean stock market can rise, some analysts believe that in addition to the influence of the AI sector, the political sphere also hopes that the upward trend will continue until the eve of the local elections in June this year.

This atmosphere has also profoundly affected liquidity in the crypto.

On February 11, 2026, the Lighter exchange launched the world's first batch of on-chain perpetual contracts for South Korean stocks, including Samsung Electronics, SK Hynix, Hyundai Motor, and the KOSPI index, with leverage up to 10x. A few days later, Trade XYZ listed Samsung and SK Hynix, also with 10x leverage.

This is also a highly symbolic scene: the trading platform that once hosted the Altcoin frenzy is now hosting South Korean stocks.

After all, in this era where AI is reshaping the world, semiconductors are more attractive than Altcoin.