Only 3% of the tokens were released in the airdrop, and some users who spent $200,000 only received 2,000 tokens.

Written by: ChandlerZ, Foresight News

Opinion, a rising star in the prediction market, is about to have its TGE moment, but this long-awaited token issuance has brought not celebration, but anger and loss lists from a large number of users.

According to its published OPN token economics, the airdrop in the first quarter accounted for only 3% of the total token supply, which was far from the market's previous expectations; the pre-market price of Opinion points plummeted from a high of $45 per point to $6 per point; bloggers such as @daidaibtc publicly stated that they burned through $200,000 to accumulate points, and ultimately only got 2,000 OPN tokens, equivalent to about $1,000.

This is one of the most controversial TGEs at the start of 2026.

Pre-market prices surged by over 30% in a short period, but airdrop users were left devastated.

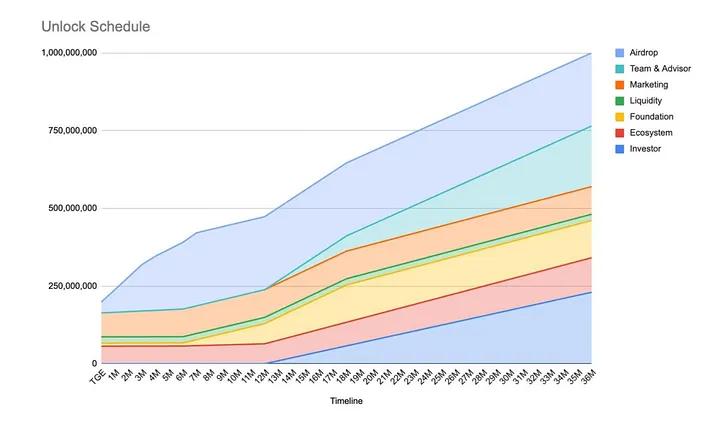

On the evening of March 2nd, the Opinion Foundation officially announced the tokenomics and roadmap for its native token, OPN. The total supply of OPN is 1 billion, with an initial circulating supply of 198.5 million, and it will be deployed on Ethereum and BNB Chain. Regarding token distribution, 23.5% (235 million tokens) will be airdropped, 3.5% will be released via TGE, and the remainder will vest over 7 months; investors will receive 23% (230 million tokens), and the team and advisors will receive 19.5% (195 million tokens), both with a 12-month lock-up period and a 24-month linear release period.

The Foundation accounts for 12% (120 million TGE), with 1% released in TGE; the Ecosystem and Incentives account for 11.1% (111 million TGE), with 5.65% released in TGE (including 3.5% locked airdrop rewards and 2.15% retroactive incentives); Marketing accounts for 8.9% (89 million TGE), with 7.7% released in TGE; Liquidity and Market Making account for 2% (20 million TGE), with 2% released in TGE.

Following Opinion's announcement of its airdrop tracking website, its pre-market price on Binance surged by over 30%, breaking through $0.57.

One blogger noted that before the announcement of the token economics, OPN tokens were priced at $45 per point on the secondary market. However, after the official disclosure that only 3% of the total tokens would be released in the first quarter airdrop, the pre-market price quickly plummeted to $6 per point, a cumulative drop of over 85%.

Even more bizarrely, the price movement itself was the complete opposite of what the airdrop users experienced. Precisely because of the extremely low initial circulating supply, the OPN price actually saw a brief surge before the market opened. The logic of low circulation and high control temporarily worked at the price level, but token holders had already been wiped out in the pre-market crash. According to feedback from several well-known studios, the cost of tokens ranged from $5 to $20 per token, and based on the airdrop value after TGE, almost none of them achieved a positive return.

The blogger "Daidaidabit" even publicly shared his loss details, revealing that he invested $200,000 to farm points and ultimately obtained 2,000 OPN tokens, which are worth approximately $1,000 at the current price. "$200,000 for 2,000 coins. Yes, you read that right." This statement quickly went viral in the Chinese crypto community.

Polymarket data shows that the probability of betting on "OPN exceeding $500 million in FDV within one day of its launch" is 64%, indicating that market expectations are not pessimistic. However, the anger of airdrop users lies mostly in the allocation logic itself.

"DaiDaiDaiBit" stated, "Of course I accept being exploited and then exploited in return. Who says exploiting is always profitable? You have to accept the consequences of your bet. What angers me is the backstabbing. You could learn from Lighter and simply not distribute any points. If you don't distribute points, do you think there won't be any bots to help you manipulate the data? But you distributed points, told everyone to come and mess with you, help you manipulate the data, and then, after you've used up the community, you tell them at TGE, 'The points I gave you were just for fun, they don't count anymore.' Does that make any sense?"

The project team actively recruited users to generate data and build buzz through a points system, but unilaterally reset the implicit agreement when it came to rewarding them. Losses are common nowadays, but the "use and discard" operational logic crossed the line of basic trust within the community.

Founded by several well-known capital firms with a background in Hong Kong and Wall Street.

Opinion (Opinion Labs) is an on-chain prediction market protocol. Unlike the binary settlement mechanisms of mainstream platforms such as Polymarket and Kalshi, Opinion focuses on a continuous prediction market model. Users do not need to wait for event settlement and can buy, sell, and adjust positions at any time as the topic evolves. The market price continuously reflects changes in collective expectations. The platform uses a CLOB (Central Limit Order Book) architecture and introduces AI-assisted market creation functionality, supporting any user to initiate structured prediction markets. The coverage extends from macro-financial events to Asia-Pacific-specific content such as esports, entertainment, and regional politics.

Regarding the founding team, Opinion CEO Forrest Liu is a graduate of Columbia University and previously worked as a corporate finance advisor at CMB International Capital, possessing a background in traditional financial institutions. The co-founder team also includes former JPMorgan members. The project aims to fill the gap in the Asia-Pacific content market left by Western platforms (Polymarket, Kalshi) and is currently one of the few on-chain protocols in the prediction market sector with Asian users as its core audience.

Opinion has completed two rounds of financing, raising over $25 million in total. In March 2024, Yzi Labs announced that Opinion was among the 13 early-stage projects selected for the 7th season of the MVB Accelerator Program. In March 2025, Opinion announced the completion of a $5 million seed round of financing, led by Yzi Labs, with other investors including angel investment community Echo, Animoca Ventures, Manifold Trading, and Amber Group.

YZi Labs' endorsement meant that Opinion directly gained access to Binance's ecosystem resources, and subsequently launched on Binance Launchpool and the Binance Wallet Booster program as scheduled. CZ tweeted in October 2025 that "YZi Labs is only a small investor in the prediction market for Opinion, but will do its best to help increase its strategic value."

In February 2026, Opinion announced the completion of a $20 million Pre-Series A funding round, co-led by Hack VC and Jump Crypto, with participation from Primitive Ventures, Decasonic, and Continue Fund.

On the other hand, high growth is accompanied by OI/Vol anomalies and data being questioned.

However, Opinion's narrative of rapid growth has never escaped the question of whether the trading volume is genuine.

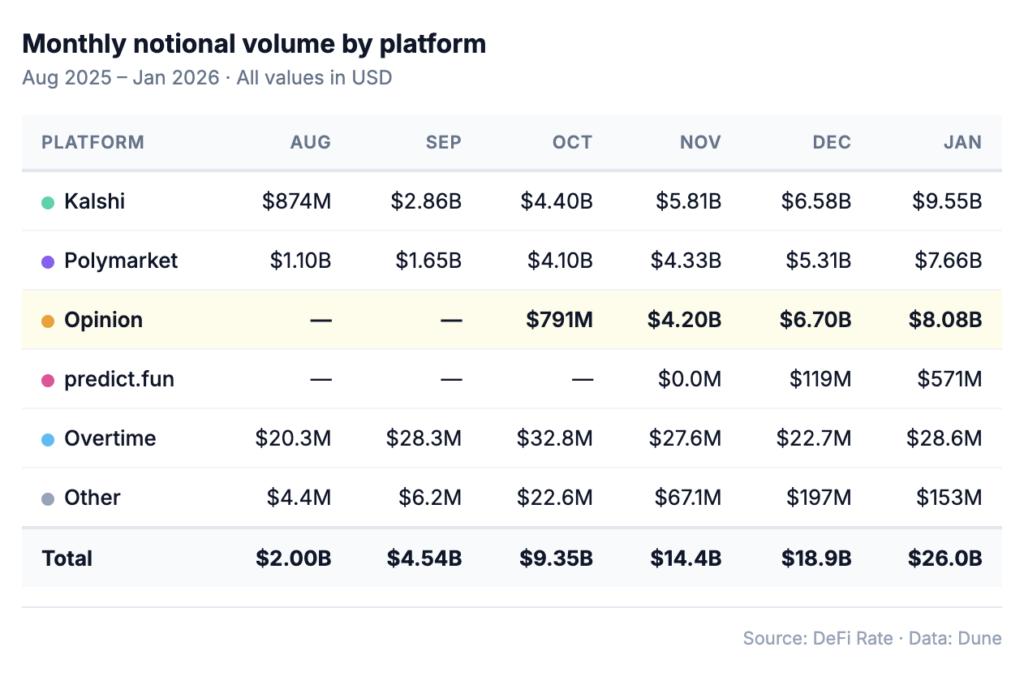

According to a report by DeFi Data, Kalshi's monthly trading volume surged 11-fold from $874 million in August to $9.55 billion in January, primarily driven by sporting events. Polymarket's trading volume also increased sevenfold, from $1.1 billion to $7.66 billion, reflecting a more diversified business portfolio encompassing sports, cryptocurrency, and politics.

Opinion launched on October 23 and achieved $791 million in revenue in its first month (less than a month). It reached $4.2 billion in November and $6.7 billion in December, surpassing the monthly revenue of Kalshi and Polymarket.

While trading volume is a key metric, the actual number of trades reveals different patterns. In January 2026, Opinion's trading volume was $8.08 billion, with 3.2 million trades executed, averaging approximately $2,525 per trade. In the same month, Kalshi's trading volume was $9.55 billion, with 54.5 million trades executed (averaging $175 per trade). Polymarket's trading volume was $7.66 billion, with 52 million trades executed (averaging $147 per trade).

Opinion, with less than 3% of the total number of transactions in the industry, accounted for 31% of the total transaction value. Its average transaction value was $2,525, 17 times that of Polymarket and 14 times that of Kalshi.

This kind of deviation is almost impossible to occur with organic user behavior. The report further points out two other anomalies: First, Opinion's active user count fluctuated dramatically by up to six times within a few weeks, while the user base of organically growing platforms typically tends to stabilize; second, as the platform scaled up, Opinion's average transaction volume per user not only did not decrease, but continued to rise. This is contrary to the pattern of almost all normally growing platforms.

The root of the problem lies in Opinion's Points-Based Incentive System (PTS). PTS distributes 100,000 points weekly, allocated proportionally among all users based on their contribution. The core weighting of this "contribution" includes three factors: transaction size, holding duration, and the proximity of the order to the market midpoint. Transaction size directly impacts the score; larger single transactions carry higher point weighting.

DeFi Rate concludes that while these transaction volumes are indeed occurring on-chain, structural incentives create a data pattern that is highly distorted from organic demand. Opinion's data may not necessarily be fake, but it likely records points-driven funding behavior rather than genuine market demand predictions.

With the launch of TGE, the points-based incentive program has come to an end. The fuel that drove the $8 billion monthly transaction volume has been extinguished. Whether this portion of funds will remain on the platform will directly determine the true strength of Opinion's user base.

Two suspenseful questions

Opinion emerged at an opportune juncture: user education in the prediction market was largely complete, regulatory attitudes were becoming clearer, and the potential market size in the Asia-Pacific region was enormous. However, choosing to complete the TGE during a market downturn and employing a token economics approach that triggered a large-scale community backlash—this combination of timing and stance inevitably led to higher friction costs for user retention in the post-airdrop era.

Opinion faces two unanswered questions: after removing the points incentive, how much of the 8 billion monthly trading volume will remain? And of the early users who were "cheated," how many will choose to stay, and how many have already permanently left? The answers to these two questions will jointly determine how much real value OPN will have before the token unlocking wave arrives.