Written by Eric, Foresight News

On March 5, 2026, Culper Research, a well-known short firm, released a short report targeting Ethereum, pointing the finger at the Fusaka upgrade completed in December 2025. This technical upgrade, intended to improve network capacity, not only failed to solidify Ethereum's position but also pushed the network to the brink of a "death spiral" by undermining the foundations of token economics.

The report states bluntly, "You may not believe me, but you have to believe Vitalik, who sold an extra 3,000 Ethereum. We followed his lead."

At the end of January, Vitalik Buterin announced that the foundation would enter a period of "mild austerity," and then immediately sold 19,326 ETH instead of the planned 16,384—16% more than announced. This is like a boss saying "the company needs to tighten its belt" at an all-hands meeting, then taking the monitor from his desk and selling it on a second-hand marketplace, while also taking two potted plants from the reception desk.

Where does Ethereum's "death spiral" come from?

Before introducing Culper Research's perspective, it may be necessary to first introduce Culper Research itself.

While not as well-known as Muddy Waters, Culper Research, founded in 2019, was named one of the top 5 most aggressive short firms on Wall Street by Activist Insight in 2021. It is known for exposing misleading or fraudulent practices by listed companies in their operations, risk disclosures, and use of funds.

While some investors believe its reports are often subjective or opportunistic, Culper has a number of success stories. In February 2025, Culper released a short report on AppLovin, accusing it of using an app backdoor to forcibly install other apps on users' phones to increase revenue. AppLovin's stock price fell 12.2% on the day the report was released.

Returning to the topic of Ethereum, Culper attributes the "death spiral" problem to a series of chain reactions triggered by the unexpected drop in gas prices caused by the Fusaka upgrade:

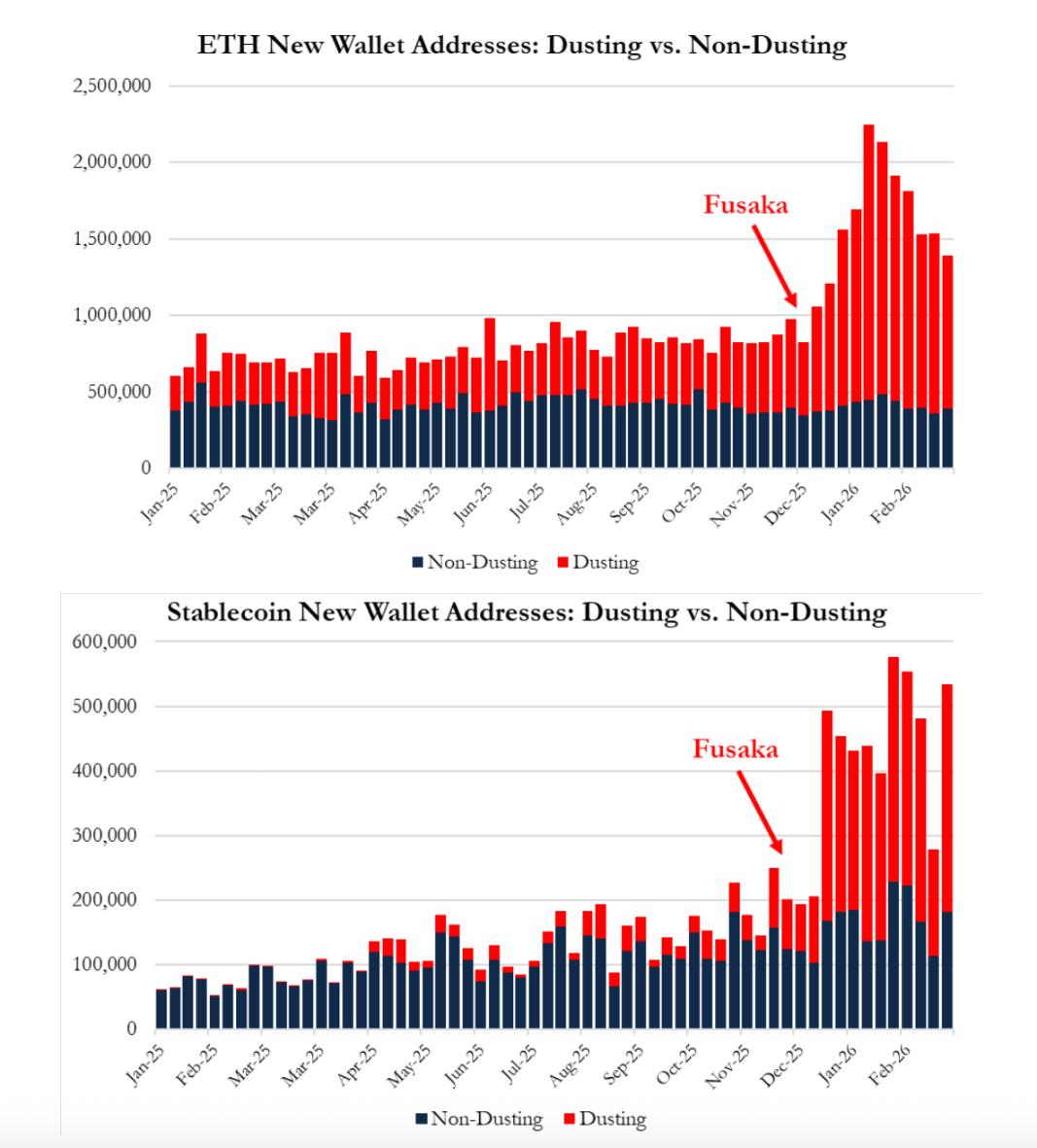

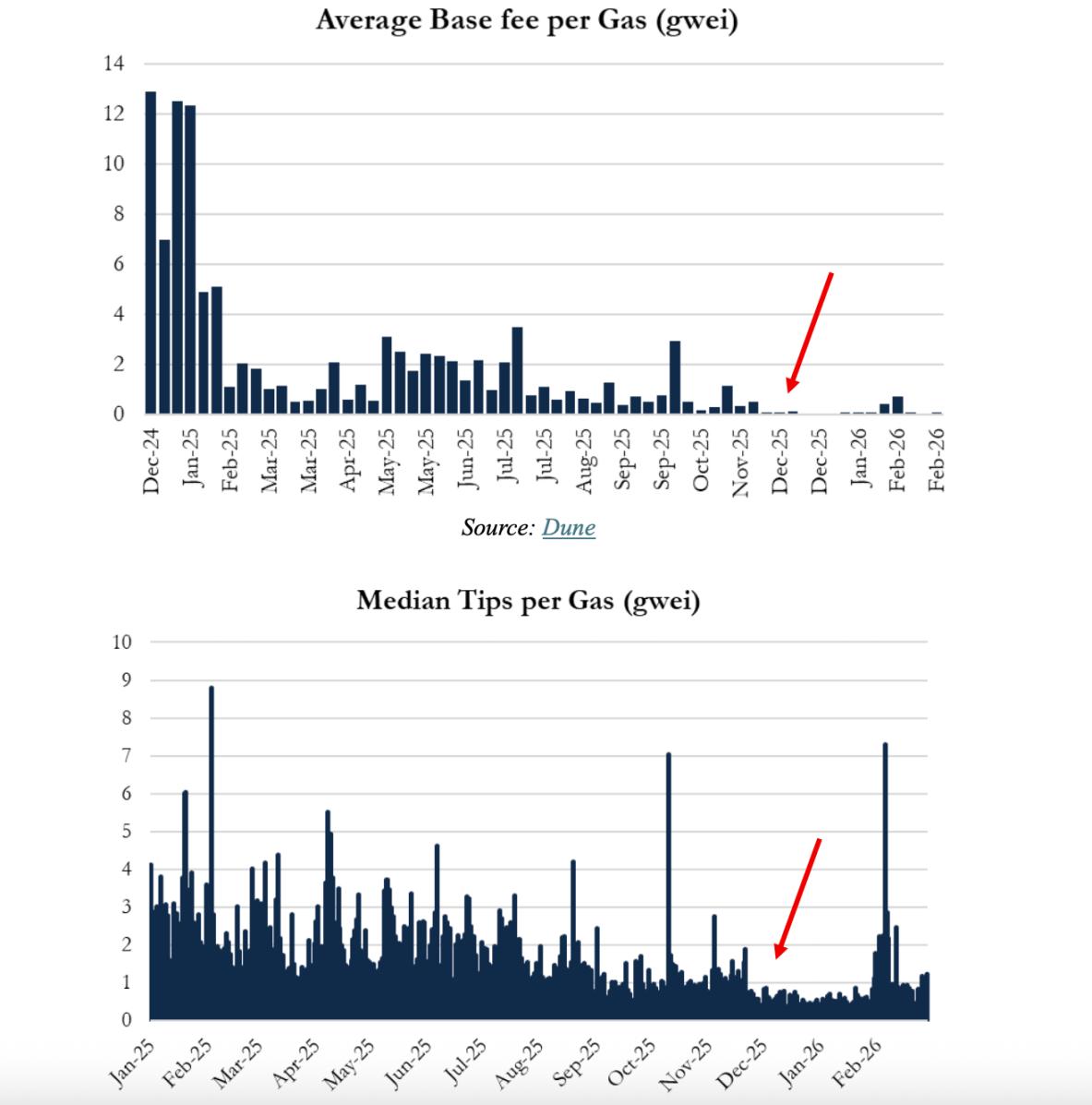

By increasing Ethereum's Gas Limit from 45 million units to 60 million, the Ethereum Foundation originally hoped that the Fusaka upgrade would reduce transaction fees by 10% to 30%, thereby stimulating L1 adoption and strengthening ETH's deflationary properties by increasing fee burning. However, instead of the expected moderate decrease, gas fees plummeted by about 90%, from approximately 25 GWei before the upgrade to 0.5 GWei (Ethereum gas fees have now fallen to 0.032 GWei).

The Ethereum Foundation originally intended to deflate the tires, but the dealership simply removed them.

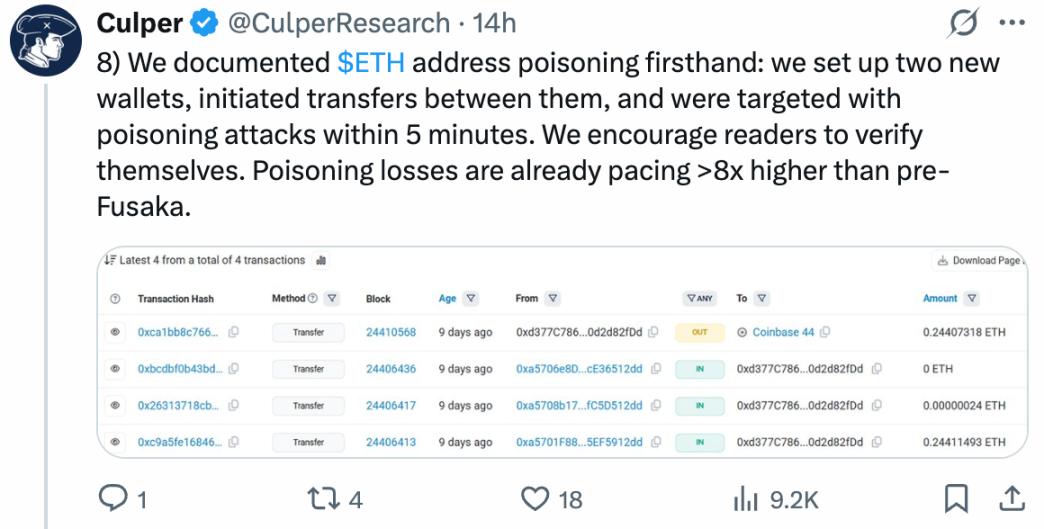

The collapse of this fee structure triggered a catastrophic chain reaction. According to Culper's analysis of full-chain transaction data from January 2025 to February 2026, address poisoning attacks (the kind of scam that transfers 0.0001 USDT to your wallet to trick you into copying the wrong address) saw explosive growth after the upgrade. Data shows that after the Fusaka upgrade, a staggering 22.5% of transactions on the Ethereum mainnet were actually due to address poisoning attacks; 95% of new wallet growth can be attributed to such fraudulent activities; and in the first two months of 2026 alone, the annualized losses from related scams were estimated at $348 million, more than eight times the level previously estimated.

Field tests showed that the two newly created addresses were attacked with malware within just 5 minutes of each other transferring funds.

The report argues that the increase in active addresses and trading volume, which bulls perceive as having "strong fundamentals," is actually a manifestation of a systemic security crisis.

From deflation to inflation

The deeper crisis triggered by the Fusaka upgrade lies in its disruption of the validator economic model. In Ethereum's Proof-of-Stake (PoS) mechanism, validators rely on priority fees and the revenue generated from burning base fees to maintain operations. However, when blocks are filled with low-value spam transactions and poisoning attacks, legitimate transactions can be included without bidding, causing a precipitous drop in validator rewards.

Currently, the ETH staking yield is around 3%, while the yield on the benchmark 10-year US Treasury bond is approximately 4.1%-4.2%. Meanwhile, Ethereum's annualized inflation rate over the past 30 days has exceeded 0.8%, and since the merger, the circulating supply of Ethereum has increased by nearly 1 million, compared to a minimum decrease of over 450,000. These figures are not optimistic.

Even more serious is the fact that Ethereum's planned Glamsterdam upgrade intends to further increase the Gas Limit to 100 million or even 200 million, perpetuating this vicious cycle. According to Culper, as long as Ethereum cannot replicate the on-chain activity of the DeFi and NFT era, the death spiral is unavoidable.

sophisticated taunts

Vitalik selling an extra 3,000 Ethereum isn't a big deal in itself; it might just be a way to raise more funds for Ethereum's development. However, Culper interprets this inconsistency as: while Vitalik talks about building Ethereum, his actions don't match his words.

Using Vitalik's selling of more tokens as a reason for his bearish view on Ethereum is far-fetched. Culper may simply be using this to mock Ethereum's staunch bull, Tom Lee. In his report, Culper titled it "What Vitalik Knows, and Tom Lee Doesn't," which translates to: The founder knows the ship is sinking, so he's looking for lifeboats; while the analyst is playing "My Heart Will Go On" on deck.

Culper Research, in its report, draws a parallel between Ethereum and the former Netscape and Nokia—both companies that once defined industry standards but whose economic models could spiral out of control due to the failure of their token value capture mechanisms. Furthermore, Ethereum's competitors are performing exceptionally well. In 2025, the number of Solana developers grew by 29%, far exceeding Ethereum's 6%; financial giants such as Stripe, Visa, and Citigroup have chosen Solana as their infrastructure for stablecoin settlement and asset tokenization. Meanwhile, the trading volume on Solana's DEXs is now more than double that of Ethereum.

Judging from Ethereum's price movement, Culper's short report did not trigger a strong market reaction. This could be because the issue has already been priced in, or perhaps people believe the problem is currently manageable. Looking at the comments on Culper's tweets, many are mocking him and suggesting that this kind of "outsider" FUD (fear, uncertainty, and misunderstanding) could be a signal that the market bottom has arrived.

Good things aren't cheap.

Four years ago, when Yuga Labs announced that it would be developing a game, I saw a very unique perspective on X: if BAYC is a limited-edition luxury item that represents status, its value has no upper limit, but if you forcibly add the narrative of GameFi, its valuation has an upper limit.

Culper applied this logic to Ethereum, arguing that while Ethereum's initial intention to reduce gas fees was good, it seemed to have gone too far.

Yes, Ethereum's gas fees are cheaper, sometimes even lower than L2, but this low cost has been targeted by hackers before it can attract truly valuable applications. It's like how platform subsidies haven't attracted real users, but instead have drawn in a large group of "wool-gathering" (exploiting promotional offers).

Vitalik and the Ethereum Foundation have high expectations for Ethereum, and have spared no expense in improving the performance of this pioneering public chain in recent years. However, they may have overlooked a crucial point: Ethereum is an organic economy, and large-scale infrastructure development that is not adapted to the level of economic development could potentially devastate the entire local economy.

From my perspective, the problems described by Culper are objectively real. The core reason for the sustained low price of Ethereum over the past two or three years is the lack of high-quality applications leading to inactivity on the chain. The significantly reduced gas fees have indeed exacerbated these economic problems, and these factors will undoubtedly continue to suppress the price of Ethereum for some time to come.

But what Culper may not understand is that Web3 is not a rational market. As long as these issues don't shake the foundations of Ethereum, the emergence of any single concept can be enough to turn the tide. Ethereum has also experienced the despair of plummeting from $2,000 to tens of dollars, with its blockchain seemingly lifeless. At worst, we can start over with a more robust infrastructure.

Culper laughs at us for not understanding economics, we laugh at Culper for not understanding Web3.