The rapid adoption of AI agents is a strong long-term tailwind for blockchain activities.

Article by: Cosmo Jiang & Sam Lehman

Article compiled and sourced from: TechFlow TechFlow

Disclaimer: This article is a reprint. Readers can obtain more information through the original link. If the author has any objection to the reprint format, please contact us and we will modify it according to the author's request. This reprint is for information sharing only and does not constitute any investment advice, nor does it represent Wu Blockchain views or positions.

February 27, 2026 | Cosmo Jiang, Sam Lehman

The viral rise of OpenClaw (formerly Clawdbot) marks a generational leap in autonomy. As these AI agents begin to interact with each other—negotiating and transacting in some cases—the agent-driven future transforms from science fiction into reality.

OpenClaw is just the beginning of an accelerated journey. Trillions of dollars are pouring into the AI field. AI spending by US hyperscale cloud vendors alone is projected to exceed $650 billion by 2026, roughly ten times the inflation-adjusted cost of the Apollo program.

Starting with simple chatbots, AI systems are rapidly evolving into fully autonomous agents. These AI agents are not merely content generators, but economic agents—capable of reasoning, acting, trading, debating, and coordinating, all without real-time human oversight. The impact of this transformation will be ubiquitous, but the business world may be the most profound.

It is estimated that by 2030, the global consumer business involving AI agents will reach $3 to 5 trillion. Even if only 10% of this evolves into agent-to-agent programmatic transactions, the annual machine-native settlement traffic will still reach hundreds of billions of dollars.

This naturally raises the question: what kind of financial and coordination infrastructure is truly suitable for AI Agent native business?

Today's business is designed for humans, involving identity verification, banking intermediaries, legal contracts, settlement cycles, and human oversight. Autonomous software cannot open accounts at bank counters, sign documents in person, or wait days for ACH (Automated Guided Transactions) to arrive. The infrastructure required for agents must be programmable, always-on, globally accessible, permissionless, and machine-verifiable by default.

Blockchain can meet these constraints, and we are already seeing this dynamic emerge.

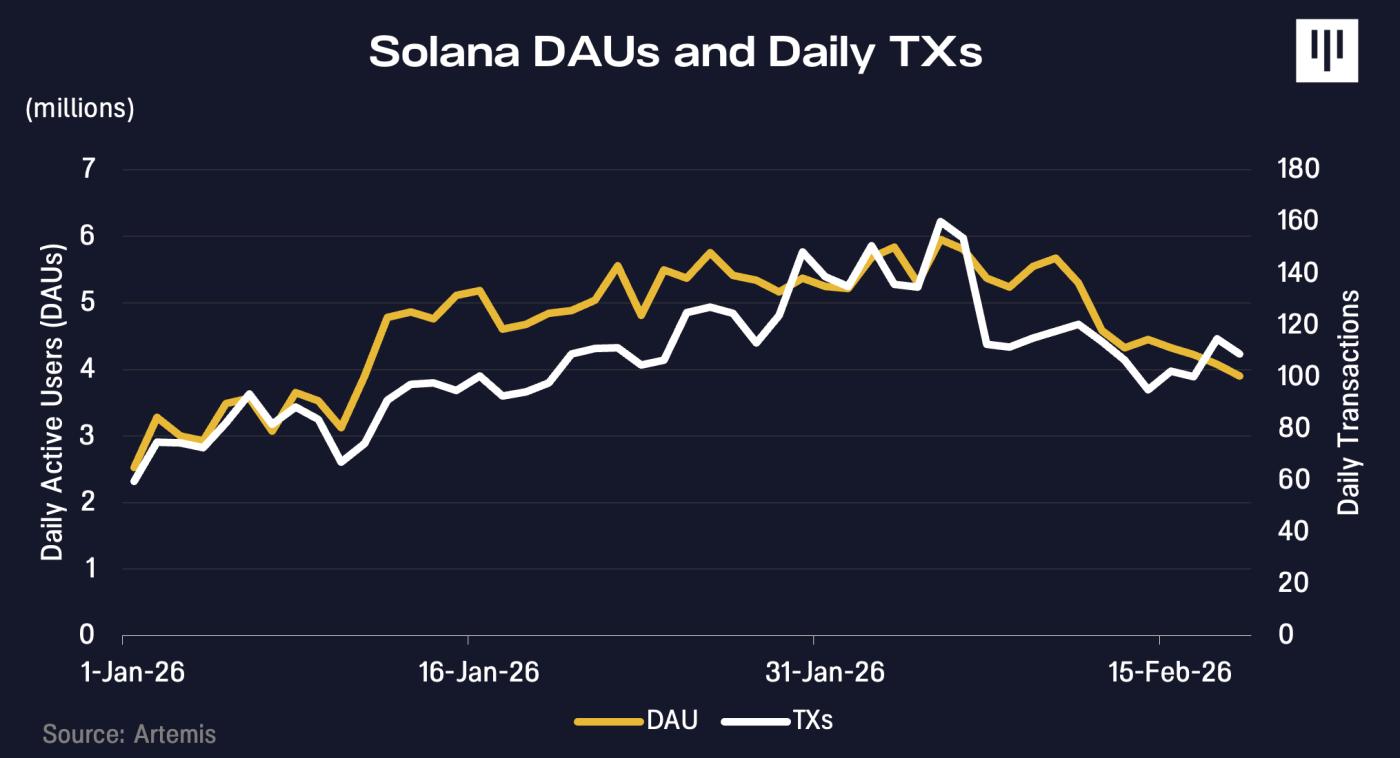

Around the same time that OpenClaw gained popularity in January, Solana's transaction volume and active addresses also began to climb. Evidence on its AI agent social network, Moltbook, suggests that agent activity may be one of the contributing factors to this growth.

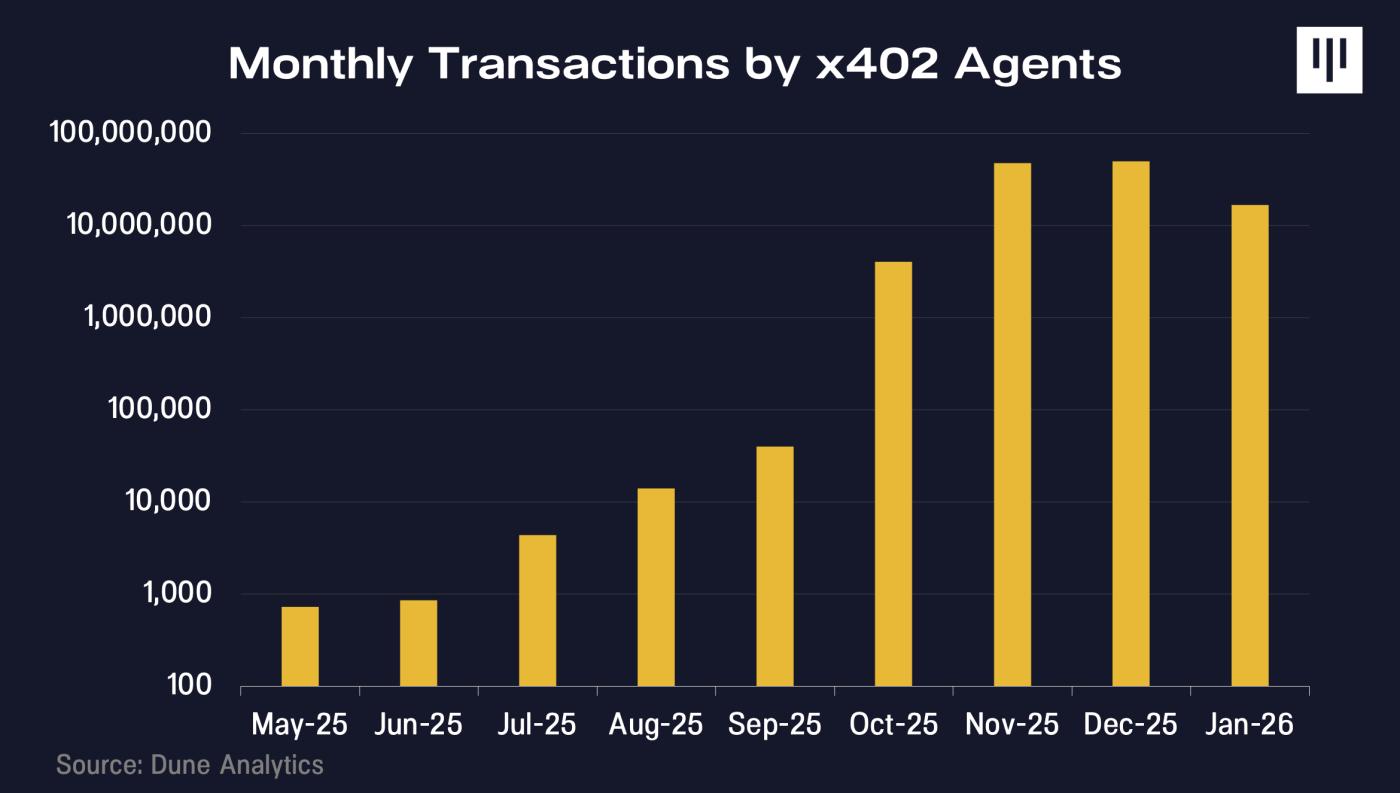

x402 is an internet-native payment protocol developed by Coinbase that allows AI agents to pay for digital resources in real time without an account or complex, high-friction authentication processes. Since its launch in 2025, its transaction volume has continued to accelerate.

We are still in the early stages, and today's cases are more directional than decisive. But if investors are excited about the potential of AI innovation, they shouldn't overlook why we believe the blockchain track will be the foundation for unlocking a fully autonomous agent world.

Many would correctly point out that today's AI agents do not need blockchain. This may be true in the near term, but we believe this is a short-sighted view.

McKinsey recently released a framework that categorizes the level of automation in AI-driven business into six levels: from basic subscription assistants (Level 0) to fully autonomous agent-to-agent commerce (Level 5). The core insight is that levels 0 through 4 do not require new financial tracks. In each case, a human identity is behind the transaction. The user has already verified their identity and linked their credit card on platforms like ChatGPT, Amazon, or Perplexity. When the agent transacts, they are acting on behalf of this human, inheriting their identity, payment credentials, and legal status.

![]()

The infrastructure for this type of business—shared payment tokens, chargeback systems, fraud detection infrastructure—already exists through Visa or Stripe and works quite well.

Blockchain tracks become critical at levels 5 and above: when agents transact directly with other agents without human instructions; when no human identity can be inherited; when payments must be programmatic, conditional, and settled in milliseconds; and when agents need portable reputation across platforms.

As long as humans continue to bear economic responsibility, the traditional framework will suffice. Once agents become independent economic entities, the constraints will fundamentally change.

To understand where value accumulates and why blockchain is important, we must imagine the logical final state of Agent AI. We are moving towards a world where agents are not merely human assistants, but independent economic entities. Some are created by companies or individuals, while others are generated by the agents themselves, forming increasingly independent systems capable of reasoning, allocating capital, and trading without real-time human supervision.

Without human-designated transaction channels (such as going to a bank, using Stripe, or opening a blockchain wallet), agents will rationally choose the fastest, most reliable, globally accessible, and least frictional and dependent pathways. When the alternative is to open a bank account and wait for ACH settlement during limited bank hours, agents will naturally choose the permissionless, 24/7 blockchain pathway.

We believe there are three core constraints that will drive agents toward blockchain:

Identity and Access: How to track the unique identity of AI entities that transact with each other and register for services? What should the new reputation system look like when traditional credit scoring and fraud detection systems are built for humans with physical footprints and operating within jurisdictions?

Currency and Payments: What form of currency is needed when agents are making countless micropayments, enforcing conditional payments, and experiencing a significant increase in cross-jurisdictional business needs? What form of account is needed when agents cannot go to a bank counter to open an account?

Transactions that minimize trust: How can AI agents avoid disputes and friction that require human arbitration or other forms of centralized trust—systems that they may not be able to access or are unwilling to access?

Identity and Access

Before an agent makes a payment, the counterparty must know who—or what—it is dealing with.

Traditional identity systems are designed for humans. They rely on government identification documents, physical signatures, and other credentials, assuming that the other end is a person in a legal sense.

Autonomous AI agents lack these capabilities. They cannot open a bank account or legally sign contracts. However, if we want agents to trade autonomously, they need some way to prove that they are acting legally and authorized.

Connecting the agent to your bank account exponentially increases the risks. How do you audit the software for money laundering? Who is responsible if the agent acts autonomously? What if it's manipulated?

In simple scenarios, an agent can inherit the owner's credentials (e.g., ChatGPT Checkout). However, this model is not feasible at scale. Multiple agents require separable permissions and spending limits. It's essential to be able to isolate problematic behavior without freezing all agents. These scenarios require agents to have their own verifiable identities, rather than borrowing human identities.

This is precisely where blockchain-based identity comes into play. Through cryptographic technology, an agent can prove that they are authorized to act on behalf of a specific individual or company without revealing the individual's sensitive information. Think of it as a digital authorization letter that anyone, anywhere, can verify instantly without contacting a lawyer or querying a database.

Emerging standards such as Ethereum's ERC-8004 introduce on-chain registries where agents can build verifiable credentials and accumulate transaction history and reputation over time. An agent that has successfully completed thousands of uncontroversial transactions will create a meaningful difference between itself and a completely new agent with no history—and this reputation is portable across platforms.

![]()

This is crucial because trust is a prerequisite for business. Merchants have spent years building systems to shield themselves from bots and web crawlers. In an agent-driven economy, they now need to figure out how to allow the right bots to run. Cryptographically secure and verifiable identities allow merchants to build trust without human guarantees.

Programmable money and micropayments

Traditional payment systems are designed for human-scale transactions. When you pay for a cup of coffee or a pair of jeans, credit card fees (usually 2-3% plus about 30 cents per transaction) are negligible.

But agent-to-agent commercial operations operate on a completely different scale. An agent writing code might make 10,000 API calls in a single task. An agent comparing prices might query hundreds of data providers. Payments need to be completed within milliseconds, repeatedly, in amounts measured in cents.

Credit card networks are not optimized for this behavior. Minimum transaction fees make micropayments economically unviable. Fraud systems freeze accounts exhibiting high-frequency bot-like behavior. Transaction speeds are significantly slower compared to high-performance blockchain protocols.

Stablecoins and programmable money are truly useful here. On-chain transactions can be broken down to extremely small units, with settlement costs approaching a fraction of a cent. More importantly, because payments are programmable, they can be conditional: X is paid only when the API returns valid data; funds are released only when the computational task is completed; and payments are streamed in real time as services are consumed, rather than prepaying a block of funds that you may not use.

Programmability also improves capital efficiency. Today, you typically need to pre-deposit funds for your agent to access new services, requiring you to estimate usage and lock up capital in advance. With smart contracts and on-chain collateral, the agent can prove solvency before service delivery without transferring payments.

Blockchain enables financial infrastructure that matches the way agents work: autonomous, high-frequency, conditional, and capital-efficient.

Transactions that minimize trust

Traditional commerce embeds trust into intermediaries. Payment processors manage chargebacks. Banks provide settlement guarantees. Courts adjudicate disputes. Contracts ultimately rely on the human legal system for enforcement.

This framework becomes inefficient when billions of low-value transactions occur across multiple jurisdictions. An AI agent transacting with another AI agent may lack access to the legal system of a particular jurisdiction or choose not to rely on it. Cross-border enforcement can be slow, expensive, and have uncertain outcomes.

Blockchain reduces reliance on unreliable trust systems by directly encoding execution logic through smart contracts. For example, smart contracts allow funds to be held in escrow programmatically, released only when preset conditions are met. Settlement is deterministic and unaffected by the risk of non-payment. Rules are transparent and verifiable in advance to both parties. No legal remedies are required.

For large-scale autonomous agents, reducing reliance on centralized intermediaries and human arbitration can lower friction, increase predictability, and enable programmatic commerce. This lower-friction infrastructure could expand the boundaries of economic activities that are uneconomical under traditional law enforcement models. Agent commerce supported by blockchain has the potential to accelerate global GDP growth.

The question is not whether agent-based businesses will emerge, but on what infrastructure they will run on.

As AI agents become autonomous economic entities, the number of economic entities in the global economy will grow exponentially. These agents will require a digitally native financial framework—a technology stack capable of handling programmatic settlements, high-frequency micropayments, permissionless coordination, and minimally trusted identity systems. These principles are precisely the fundamental starting point for blockchain design.

We believe it's reasonable to say that the rapid adoption of AI agents is a strong long-term tailwind for blockchain activity. Preliminary evidence already exists, and we believe most investors are underestimating the value creation opportunities inherent in this.