Author: Liu Lei's Legal Team

Original link: https://mp.weixin.qq.com/s/D4JrfyYjGespAnqVx-_2og

Disclaimer: This article is a reprint. Readers can obtain more information through the original link. If the author has any objection to the reprint format, please contact us and we will modify it according to the author's request. This reprint is for information sharing only and does not constitute any investment advice, nor does it represent Wu Blockchain views or positions.

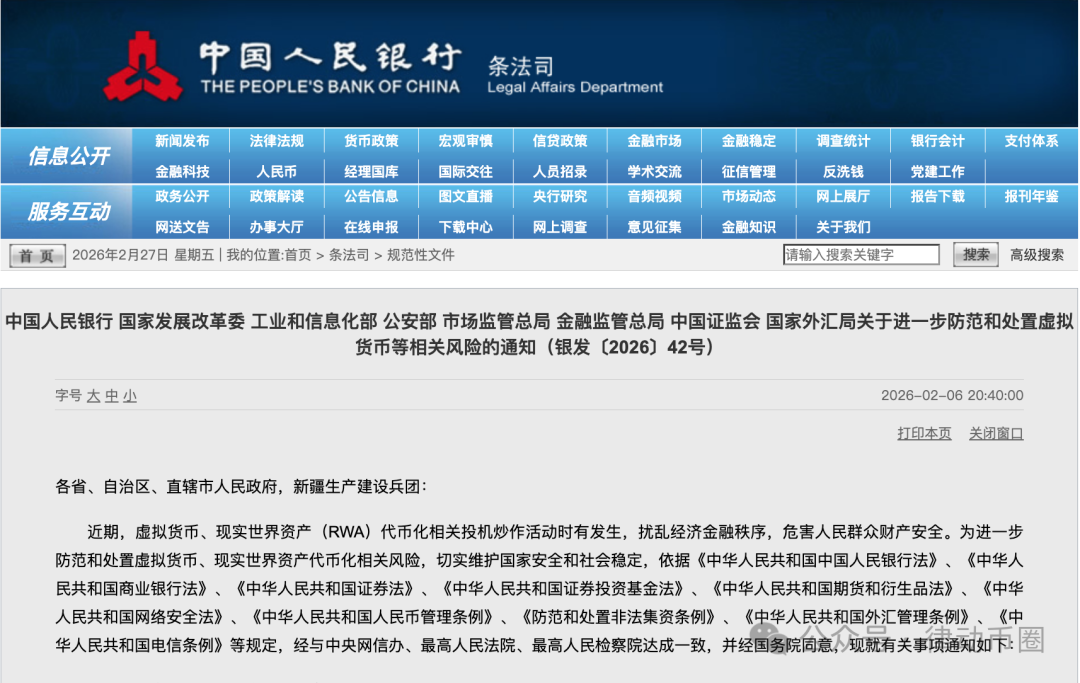

In a previous article, Attorney Liu interpreted the financial characterization of RWAs in the "February 6th Notice" and the domestic regulatory landscape. However, RWAs often possess global liquidity. This time, we will delve into how the "February 6th Notice" uses the "boundary regulation logic of subject and rights boundary" to identify "five compliance checkpoints" for market participants in the era of strong regulation.

I. Cross-border approach: From "prohibition of providing services to domestic residents" to "entity penetration and rights penetration"

(a) The "personal jurisdiction" rule for overseas currency issuance

The "2.6 Notice" explicitly states that without consent, domestic entities and their controlled overseas entities are prohibited from issuing virtual currencies overseas. The practical power of this provision lies in the fact that "overseas issuance locations" no longer constitute a natural safety net. When projects adopt structures such as foundations, DAOs, or offshore SPVs, the key to compliance assessment becomes: who initiates the project, who controls governance, who decides on the token economy, who controls funds and critical infrastructure, and who enjoys the primary benefits. In other words, the more substantial the control relationship, the more likely it is to be identified by regulatory authorities as "a domestic entity issuing virtual currencies overseas through a control chain."

(II) Categorized supervision of offshore RWAs: Foreign debt type, ABS/equity type, and other forms are respectively included in different regulatory categories.

We believe that the "February 6th Notice" and its accompanying "Answering Questions from Reporters on the Notice on Further Preventing and Handling Risks Related to Virtual Currencies" by relevant officials of the People's Bank of China and the China Securities Regulatory Commission have clearly outlined the regulatory structure for domestic entities conducting RWA-related business overseas: Following the principle of "same business, same risk, same rules," domestic entities conducting RWA in the form of foreign debt, or RWA based on domestic equity and involving asset securitization or equity-related activities, will be strictly regulated by the National Development and Reform Commission, the China Securities Regulatory Commission, and the State Administration of Foreign Exchange in accordance with laws and regulations; other forms will be regulated by the China Securities Regulatory Commission in conjunction with relevant departments; no entity or individual may conduct such activities without consent or filing. The key here is not the "classification terms," but the regulatory anchor. As long as "domestic entities/domestic equity" enter the structure, domestic regulation is triggered, and "consent/filing" becomes a prerequisite for overseas business operations.

(III) Comparison with Hong Kong's "Licensed Closed-Loop" System: Two Regulatory Models Reflecting Two Market Forms

To fully understand mainland China's regulations, a comparative analysis with a control group is often necessary. Hong Kong's regulatory approach to RWA, particularly in licensing tokenized securities and virtual asset trading platforms, provides a clear mirror for the mainland: Hong Kong tends to embed tokenization activities into its existing securities regulatory system through licensing and intermediary responsibilities, and imposes specific requirements on intermediaries' risk management in tokenized securities activities. Simultaneously, Hong Kong has established a dedicated licensing system for virtual asset trading platforms, with anti-money laundering regulations serving as a crucial legal foundation.

Therefore, mainland registration and Hong Kong licensing are more like two forms of compliant products under two different institutional objectives. The mainland system focuses on preemptively addressing the risks of tokenizing domestic assets for cross-border transactions, ensuring compliance of the entities involved, verifiable assets, verifiable cash flow, and auditable issuance documents, emphasizing information disclosure and accountability. The Hong Kong system, on the other hand, embeds the issuance, distribution, custody, and trading processes into the responsibility chain of licensed institutions and market infrastructure, emphasizing closed-loop governance and continuous supervision. There is no simple comparison of superiority or inferiority between the two; rather, they serve different constraints related to "controllable cross-border risks" and "sustainable market ecosystem."

In practice, the most crucial point is that if the project's goal is to create sustainable secondary market liquidity and inter-institutional trading order, Hong Kong's "licensed closed loop" is naturally more suitable; while if the project's goal is to enable domestic assets to complete overseas financing in a controllable manner, the path of "filing in the mainland, clarifying the negative list, and continuous reporting" is the institutional foundation that remains sound even after penetration.

II. Practical Implementation: Under the framework of the "February 6th Notice," what else can the market do?

If we read the "2.6 Notice" together with the accompanying "Guidelines", we can arrive at a more actionable conclusion: an "open RWA market" will not emerge in China; the space for discussion is mainly in the narrow path of "domestic assets, overseas issuance, prior filing, and post-reporting", as well as a very small number of domestic pilot programs "relying on specific financial infrastructure and approved by the competent authorities".

Based on this assessment, we recommend using the following "five compliance checkpoints" to screen project feasibility in practice:

The first hurdle: Are the relevant ownership relationships clear and can they be enforced against third parties? The ownership, source of income rights, transfer and restrictions on the creation of rights of the underlying assets must be able to support the arrangement of "repayment supported by cash flow"; if there are major ownership disputes or if the assets are legally prohibited from being transferred, it will directly trigger the prohibition.

The second hurdle: Is the cash flow verifiable, sustainable, and auditably traceable? The project must answer the questions: "Where does the cash flow come from? Who collects it? How is it segregated? How is it allocated? How are expenses and default scenarios covered?" Any structure that cannot be explained as "ABS-like" will lose its footing on the compliance path.

The third hurdle: Can the entity pass the compliance and negative list screening? Criminal offenses in the past three years, conclusions of major illegal investigations, national security review risks, prohibited circumstances for capital market financing, and negative lists of underlying assets will all become hard thresholds in the future.

The fourth hurdle: Do the issuance documents and information disclosures meet the standards of "auditability and accountability"? Filing requirements mandate the submission of a complete set of overseas issuance materials, ensuring their authenticity, accuracy, and completeness, and prohibiting false statements, misleading representations, or material omissions. This means that the practice of "lightening documents, uploading to the blockchain first and then supplementing materials" has no place in the system.

The fifth hurdle: Is continuous compliant operation feasible? The obligation to report major events after registration (completion of issuance, major risks, other major events) requires projects to have a continuous monitoring and reporting mechanism. In other words, if the project team is only good at "making a quick buck and running away" and lacks the ability to operate sustainably, compliance risks are likely to erupt after issuance.

Finally, it's important to emphasize that compliance addresses the question of "whether a project can exist," but from a market perspective, the more crucial first step remains determining whether an RWA project possesses genuine and sustainable market value. Compliance determines "whether it can be done," while value determines "whether it's worth doing." Before designing an RWA structure, we should return to the essence of business: Does the underlying asset face difficulties in financing, insufficient liquidity, or excessively high transaction costs? Is there information transparency? Can "on-chaining" truly expand market boundaries, rather than merely representing a technological upgrade? Specifically, through the RWA structure, can the project reach new investor groups? Can it reduce cross-border financing costs or improve asset pricing efficiency? Can it achieve higher capital turnover efficiency while keeping risks under control? If these questions lack clear answers, then even the most sophisticated cross-border structure design and the most complex registration process may simply be an accumulation of costs.

Especially under the current stringent regulatory environment, RWA projects often face high compliance costs and cross-border regulatory uncertainties. If the underlying assets themselves have limited returns, coupled with structural and compliance costs, the situation may ultimately arise where "compliance costs outweigh commercial value," fundamentally challenging the project's sustainability.

Similarly, for financing needs that could have been addressed through traditional ABS, trusts, or private equity funds, if RWA does not bring significant efficiency improvements or market growth, and the choice of tokenization is solely based on technological trends, its structural complexity and compliance costs may actually exceed those of traditional financial instruments. In this case, RWA ceases to be an innovative tool and merely a more costly alternative. Therefore, when discussing RWA under a strong regulatory framework, it's more important to answer "is it worthwhile" than to first ask "how to comply." Only when a project possesses a clear value logic does a compliance path have practical significance.

What the lawyer has to say

Interpreting the "February 6th Notice" as merely a "tightening of regulations" is inaccurate. A more accurate description is that virtual asset governance has moved from the past "special rectification and case-by-case crackdown" to a stage of "institutionalized governance, full-chain disposal, and cross-border penetrating supervision." Simultaneously, RWA has been explicitly incorporated into the financial regulatory framework: prohibited in principle domestically and strictly regulated overseas.

For market players, the era of relying on "concept packaging" and "regulatory ambiguity" has basically come to an end. In the future, what will be truly scarce will not be "people who can tell a story," but people who can create a closed system that integrates underlying assets, rights structures, cash flow, issuance documents, continuous disclosure, and cross-border regulatory requirements! The value of legal professionals will also return to "structural design and risk isolation": only by clearly defining boundaries, drawing red lines, and ensuring that every compliance judgment can be audited, explained, and reviewed can we truly achieve "steady and sustainable development."

Original link: https://mp.weixin.qq.com/s/D4JrfyYjGespAnqVx-_2og

Disclaimer: This article is a reprint. Readers can obtain more information through the original link. If the author has any objection to the reprint format, please contact us and we will modify it according to the author's request. This reprint is for information sharing only and does not constitute any investment advice, nor does it represent Wu Blockchain views or positions.

In a previous article, Attorney Liu interpreted the financial characterization of RWAs in the "February 6th Notice" and the domestic regulatory landscape. However, RWAs often possess global liquidity. This time, we will delve into how the "February 6th Notice" uses the "boundary regulation logic of subject and rights boundary" to identify "five compliance checkpoints" for market participants in the era of strong regulation.

I. Cross-border approach: From "prohibition of providing services to domestic residents" to "entity penetration and rights penetration"

(a) The "personal jurisdiction" rule for overseas currency issuance

The "2.6 Notice" explicitly states that without consent, domestic entities and their controlled overseas entities are prohibited from issuing virtual currencies overseas. The practical power of this provision lies in the fact that "overseas issuance locations" no longer constitute a natural safety net. When projects adopt structures such as foundations, DAOs, or offshore SPVs, the key to compliance assessment becomes: who initiates the project, who controls governance, who decides on the token economy, who controls funds and critical infrastructure, and who enjoys the primary benefits. In other words, the more substantial the control relationship, the more likely it is to be identified by regulatory authorities as "a domestic entity issuing virtual currencies overseas through a control chain."

(II) Categorized supervision of offshore RWAs: Foreign debt type, ABS/equity type, and other forms are respectively included in different regulatory categories.

We believe that the "February 6th Notice" and its accompanying "Answering Questions from Reporters on the Notice on Further Preventing and Handling Risks Related to Virtual Currencies" by relevant officials of the People's Bank of China and the China Securities Regulatory Commission have clearly outlined the regulatory structure for domestic entities conducting RWA-related business overseas: Following the principle of "same business, same risk, same rules," domestic entities conducting RWA in the form of foreign debt, or RWA based on domestic equity and involving asset securitization or equity-related activities, will be strictly regulated by the National Development and Reform Commission, the China Securities Regulatory Commission, and the State Administration of Foreign Exchange in accordance with laws and regulations; other forms will be regulated by the China Securities Regulatory Commission in conjunction with relevant departments; no entity or individual may conduct such activities without consent or filing. The key here is not the "classification terms," but the regulatory anchor. As long as "domestic entities/domestic equity" enter the structure, domestic regulation is triggered, and "consent/filing" becomes a prerequisite for overseas business operations.

(III) Comparison with Hong Kong's "Licensed Closed-Loop" System: Two Regulatory Models Reflecting Two Market Forms

To fully understand mainland China's regulations, a comparative analysis with a control group is often necessary. Hong Kong's regulatory approach to RWA, particularly in licensing tokenized securities and virtual asset trading platforms, provides a clear mirror for the mainland: Hong Kong tends to embed tokenization activities into its existing securities regulatory system through licensing and intermediary responsibilities, and imposes specific requirements on intermediaries' risk management in tokenized securities activities. Simultaneously, Hong Kong has established a dedicated licensing system for virtual asset trading platforms, with anti-money laundering regulations serving as a crucial legal foundation.

Therefore, mainland registration and Hong Kong licensing are more like two forms of compliant products under two different institutional objectives. The mainland system focuses on preemptively addressing the risks of tokenizing domestic assets for cross-border transactions, ensuring compliance of the entities involved, verifiable assets, verifiable cash flow, and auditable issuance documents, emphasizing information disclosure and accountability. The Hong Kong system, on the other hand, embeds the issuance, distribution, custody, and trading processes into the responsibility chain of licensed institutions and market infrastructure, emphasizing closed-loop governance and continuous supervision. There is no simple comparison of superiority or inferiority between the two; rather, they serve different constraints related to "controllable cross-border risks" and "sustainable market ecosystem."

In practice, the most crucial point is that if the project's goal is to create sustainable secondary market liquidity and inter-institutional trading order, Hong Kong's "licensed closed loop" is naturally more suitable; while if the project's goal is to enable domestic assets to complete overseas financing in a controllable manner, the path of "filing in the mainland, clarifying the negative list, and continuous reporting" is the institutional foundation that remains sound even after penetration.

II. Practical Implementation: Under the framework of the "February 6th Notice," what else can the market do?

If we read the "2.6 Notice" together with the accompanying "Guidelines", we can arrive at a more actionable conclusion: an "open RWA market" will not emerge in China; the space for discussion is mainly in the narrow path of "domestic assets, overseas issuance, prior filing, and post-reporting", as well as a very small number of domestic pilot programs "relying on specific financial infrastructure and approved by the competent authorities".

Based on this assessment, we recommend using the following "five compliance checkpoints" to screen project feasibility in practice:

The first hurdle: Are the relevant ownership relationships clear and can they be enforced against third parties? The ownership, source of income rights, transfer and restrictions on the creation of rights of the underlying assets must be able to support the arrangement of "repayment supported by cash flow"; if there are major ownership disputes or if the assets are legally prohibited from being transferred, it will directly trigger the prohibition.

The second hurdle: Is the cash flow verifiable, sustainable, and auditably traceable? The project must answer the questions: "Where does the cash flow come from? Who collects it? How is it segregated? How is it allocated? How are expenses and default scenarios covered?" Any structure that cannot be explained as "ABS-like" will lose its footing on the compliance path.

The third hurdle: Can the entity pass the compliance and negative list screening? Criminal offenses in the past three years, conclusions of major illegal investigations, national security review risks, prohibited circumstances for capital market financing, and negative lists of underlying assets will all become hard thresholds in the future.

The fourth hurdle: Do the issuance documents and information disclosures meet the standards of "auditability and accountability"? Filing requirements mandate the submission of a complete set of overseas issuance materials, ensuring their authenticity, accuracy, and completeness, and prohibiting false statements, misleading representations, or material omissions. This means that the practice of "lightening documents, uploading to the blockchain first and then supplementing materials" has no place in the system.

The fifth hurdle: Is continuous compliant operation feasible? The obligation to report major events after registration (completion of issuance, major risks, other major events) requires projects to have a continuous monitoring and reporting mechanism. In other words, if the project team is only good at "making a quick buck and running away" and lacks the ability to operate sustainably, compliance risks are likely to erupt after issuance.

Finally, it's important to emphasize that compliance addresses the question of "whether a project can exist," but from a market perspective, the more crucial first step remains determining whether an RWA project possesses genuine and sustainable market value. Compliance determines "whether it can be done," while value determines "whether it's worth doing." Before designing an RWA structure, we should return to the essence of business: Does the underlying asset face difficulties in financing, insufficient liquidity, or excessively high transaction costs? Is there information transparency? Can "on-chaining" truly expand market boundaries, rather than merely representing a technological upgrade? Specifically, through the RWA structure, can the project reach new investor groups? Can it reduce cross-border financing costs or improve asset pricing efficiency? Can it achieve higher capital turnover efficiency while keeping risks under control? If these questions lack clear answers, then even the most sophisticated cross-border structure design and the most complex registration process may simply be an accumulation of costs.

Especially under the current stringent regulatory environment, RWA projects often face high compliance costs and cross-border regulatory uncertainties. If the underlying assets themselves have limited returns, coupled with structural and compliance costs, the situation may ultimately arise where "compliance costs outweigh commercial value," fundamentally challenging the project's sustainability.

Similarly, for financing needs that could have been addressed through traditional ABS, trusts, or private equity funds, if RWA does not bring significant efficiency improvements or market growth, and the choice of tokenization is solely based on technological trends, its structural complexity and compliance costs may actually exceed those of traditional financial instruments. In this case, RWA ceases to be an innovative tool and merely a more costly alternative. Therefore, when discussing RWA under a strong regulatory framework, it's more important to answer "is it worthwhile" than to first ask "how to comply." Only when a project possesses a clear value logic does a compliance path have practical significance.

What the lawyer has to say

Interpreting the "February 6th Notice" as merely a "tightening of regulations" is inaccurate. A more accurate description is that virtual asset governance has moved from the past "special rectification and case-by-case crackdown" to a stage of "institutionalized governance, full-chain disposal, and cross-border penetrating supervision." Simultaneously, RWA has been explicitly incorporated into the financial regulatory framework: prohibited in principle domestically and strictly regulated overseas.

For market players, the era of relying on "concept packaging" and "regulatory ambiguity" has basically come to an end. In the future, what will be truly scarce will not be "people who can tell a story," but people who can create a closed system that integrates underlying assets, rights structures, cash flow, issuance documents, continuous disclosure, and cross-border regulatory requirements! The value of legal professionals will also return to "structural design and risk isolation": only by clearly defining boundaries, drawing red lines, and ensuring that every compliance judgment can be audited, explained, and reviewed can we truly achieve "steady and sustainable development."