This article is from: Viktor

Compiled by Odaily Odaily( @OdailyChina ); Translated by Azuma ( @azuma_eth )

Over the past two weeks, we've seen a significant increase in STRC trading volume, along with growing interest in the product on social media platforms like X, so I felt it was a good time to write an article about Strategy and its new structure. This is my fourth article on Strategy and the Bitcoin Treasury model:

- The first article is an introduction to the Strategy gameplay, in which I clarify some common misconceptions about the mode.

- The second article explains the "full-stack treasury company" model and the mechanism that supports its positive NAV premium.

- The third article introduces the concept of preferred stock, a brand-new model that Strategy will launch in 2025 and is currently the company's main strategy.

In this article, we will focus on STRC. It has now become MSTR's primary preferred stock product and is currently the core focus of Michael Saylor (founder of Strategy) and his management team.

TL;DR

- STRC is a yield-generating instrument backed by Strategy's Bitcoin treasury, with a dynamically adjusted dividend yield to keep the price close to par value ($100). Currently, you can earn an annualized return of 11.5% (paid monthly) on a relatively stable and risk-transparent instrument.

- STRC is essentially a way for Strategy to translate yield demand into structural buying pressure on BTC. As long as Strategy operates an ATM issuance mechanism for both STRC and MSTR (and mNAV > 1), this structure can scale up massively without increasing MSTR leverage. This means Strategy can absorb billions of dollars (or more) of new demand for STRC while still maintaining a leverage ratio of approximately 33% and keeping credit risk unchanged.

- By maintaining leverage through a common stock ATM mechanism, approximately $3 of BTC is added to the treasury for every $1 of STRC issued. A rough estimate suggests that when the daily trading volume of STRC near its face value ($100) reaches $100 million, it could generate $100 million to $150 million in BTC purchases.

- Strategy effectively splits BTC's risk exposure into two distinct risk tranches: STRC holders receive relatively stable, low-volatility returns, while MSTR shareholders bear the remaining upside potential and volatility of BTC. As Lavoisier said, "Nothing is created, nothing is destroyed, everything is simply transformed."

- The entire structure is designed to increase the number of Bitcoins per share over time. This will ultimately benefit MSTR common stockholders, as it means that MSTR will theoretically outperform BTC.

- A 5%–10% pullback in the STRC is possible in the short term, but as long as the market remains confident in this structure, it will usually pull the price back to near par value through arbitrage trading.

- The real risk isn't a sudden collapse, but rather a prolonged bear market for BTC , which could gradually put pressure on the entire structure over time. Even in the (extremely unlikely) worst-case scenario, the process would be very slow due to the dollar reserves and Strategy's flexibility in adjusting dividend yields.

- If Strategy eventually collapses, it is unlikely to happen in a drastic and dramatic way like Luna/UST, but rather as a slow and long-term deterioration.

- Logically, it's difficult to be bullish on BTC but bearish on MSTR and STRC. Given Strategy's current risk level (which may change in the future), it's highly unlikely that Strategy will fail first unless BTC "dies."

What is STRC and how does it work?

First, let me briefly review the concept of preferred shares: Simply put, they are financial instruments similar to debt, but legally still belong to the company as equity. This means that these preferred shares never need to be "repaid," and Strategy cannot default on them.

In the capital structure, preferred stock has a higher priority for repayment than common stock (MSTR), which means that in the event of company bankruptcy, preferred shareholders will be paid before common shareholders.

To date, Strategy has issued five types of preferred stock (STRF, STRC, STRK, STRE, and SRD), which I introduced one by one in the previous article. The following are the main characteristics of STRC (also known as Stretch):

- It falls under the category of "short-duration high-yield credit".

- Strategy's goal is to keep the price of STRC as close as possible to $100 (i.e., "face value"), with an ideal range of 1% fluctuation between $99 and $100.

- STRC pays a monthly variable dividend; the current dividend yield is 11.5%.

- If the price of STRC is significantly below par value, the Strategy can increase the monthly dividend yield to make the product more attractive and increase demand until the price returns to near par value.

- If the price of STRC is above $100, Saylor can issue and sell new STRC shares at $100 through an ATM (at-the-market) issuance program. This effectively creates a price ceiling around $100.

- If Saylor does not wish to issue shares through ATMs, the company has another option—to redeem STRC at $101, meaning that market participants have little incentive to buy STRC above that price.

- Like other preferred stocks in Strategy, STRC is a perpetual preferred stock, meaning it has no maturity date and no repayment period.

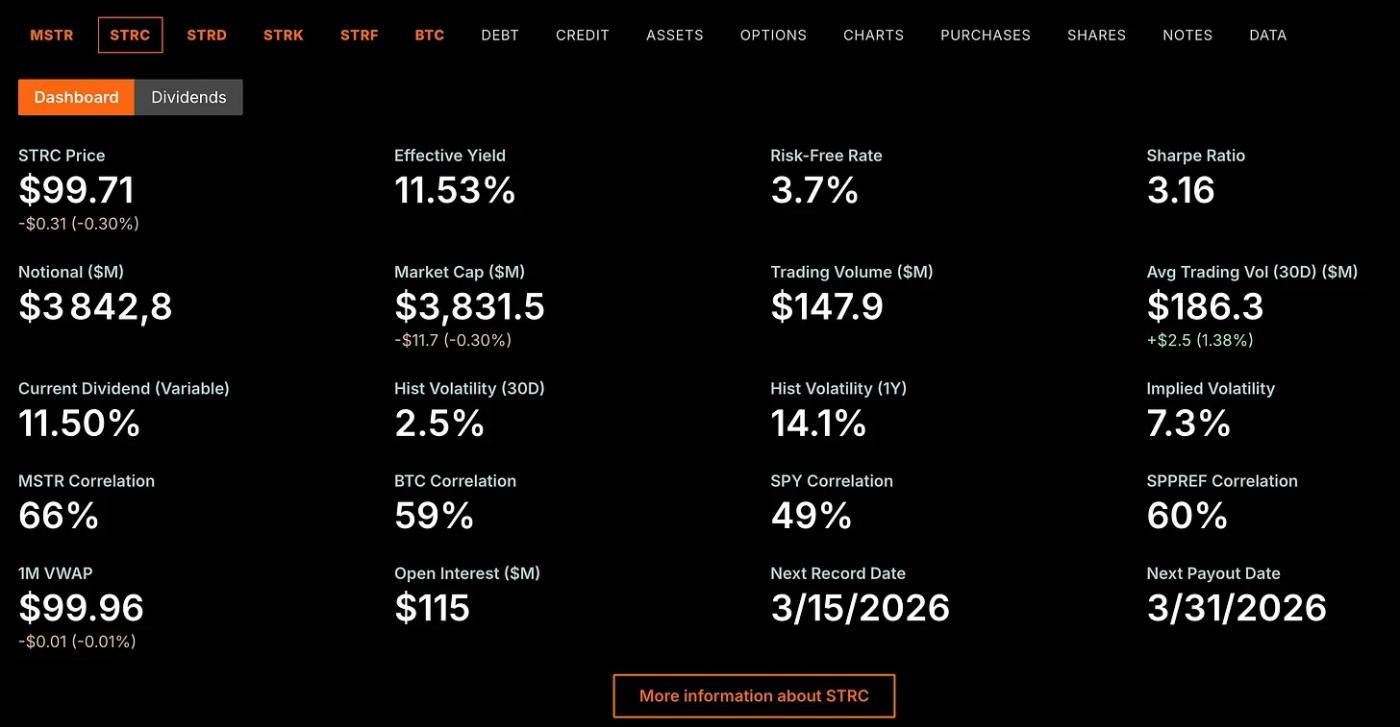

Odaily Note: All data for STRC can be found on Strategy.com. The screenshot below is from March 13, 2026, which is the ex-dividend date, so the price of STRC will be lower than its face value.

How can Strategy use ATMs to control leverage?

Although Strategy's preferred stock is not legally considered debt, it can be viewed as a way to introduce leverage into the balance sheet. Strategy distinguishes between the leverage ratio and the amplification ratio – the leverage ratio only calculates the ratio of "convertible bonds/BTC reserves"; the amplification ratio calculates the ratio of "convertible bonds + preferred stock/BTC reserves".

In fact, the leverage ratio is the true indicator of Strategy's leverage level . This means that every time Saylor issues and sells new STRC, Strategy's leverage level increases. If Saylor wants to reduce the company's leverage level, the tool he can use is the common stock ATM issuance mechanism—by issuing new MSTR shares and using the proceeds to buy BTC, he can reduce the leverage ratio while expanding the company's scale.

This logic is easy to understand: Suppose a company holds $10 billion worth of BTC and has $3 billion in debt, with a market value of $12 billion. Its leverage ratio would be: $3 billion in debt / $10 billion in BTC = 30%.

Suppose the company issues an additional $2 billion in new shares and uses the funds to purchase $2 billion worth of BTC. Assuming the price of BTC remains unchanged, the company's market capitalization now becomes $14 billion, and the value of its BTC treasury becomes $12 billion. However, the nominal amount of debt remains the same. Therefore, the new leverage ratio is: $3 billion in debt / $12 billion in BTC = 25%.

This example clearly shows that by issuing ATMs of common stock, a company can both expand its size (market capitalization from 12 billion to 14 billion) and reduce its leverage (30% to 25%).

Is Strategy using STRC to buy up cryptocurrency in large quantities?

How STRC demand translates into BTC buying?

As I said before, Saylor will only sell STRC at $100, and not below $100.

This means that when the price is below $100, all trading volume consists of STRC shares being traded among past, present, and new holders. When the price reaches $100, some trading volume still corresponds to ordinary STRC share trading (because there are also people willing to sell at $100), but the remaining trading volume corresponds to Saylor issuing new shares and selling them to "excess demand" at $100.

Last week, the ratio between STRC's weekly transaction volume and the size of ATMs that week was approximately 40%. I will use this figure in the examples below, but this is obviously not a fixed rule; in some cases, this ratio could be 25% or 60%.

When STRC is trading near par value and has a daily trading volume of $100 million, the situation is roughly as follows: Saylor can issue 40% of the amount through STRC's ATM issuance program, which means issuing and selling $40 million worth of new STRC shares. He will then immediately use this $40 million to buy BTC.

Odaily Note: The ATM will start operating when the STRC price reaches $100.

However, selling STRC would increase the company's leverage level (which is also a debt-like instrument), and Saylor certainly wants to keep the leverage level stable. Currently, Strategy's leverage level is around 33%, and I believe he wants to maintain it around that figure. This means that for every $1 of new debt, there must be a corresponding increase of $3 in BTC reserves . In the previous example, if Saylor increased his "debt" by $40 million through STRC and purchased $40 million worth of BTC, he would still need to add another $80 million worth of BTC to the company's reserves. How can he do this?

The answer was explained in the previous section—using the ATM issuance mechanism of MSTR common stock. Therefore, Saylor would issue and sell $80 million worth of new MSTR stock and immediately use the proceeds to purchase $80 million worth of BTC.

Therefore, the conclusion is that, based on this rough calculation, a daily trading volume of $100 million in STRC would correspond to approximately $40 million in new STRC issuance and the purchase of about $120 million in BTC. Through STRC, Strategy has found a way to translate the demand for stable returns into buying power for BTC.

What would happen if demand for STRCs exploded? Would Saylor be forced to leverage its resources to the limit?

I also want you to notice another point: according to the model I just described, Strategy could easily triple STRC’s market capitalization (in other words, add about $8 billion more in STRC debt on top of the current $4 billion market capitalization) without increasing the company’s leverage ratio (i.e., credit risk).

Saylor has all the necessary tools to scale up STRC to any extent that meets market demand, while still keeping leverage levels stable at 33%.

This will obviously increase the company's nominal debt and the amount of dividends that need to be paid, but these metrics will grow in tandem with the size of the BTC treasury, meaning that Strategy will not take on any additional risks related to the price of BTC.

What are the real limitations of this strategy?

The mode I described above, which simultaneously runs both the STRC and MSTR ATM mechanisms, requires two conditions to be met.

The first condition is obvious: STRC must trade at $100 . When this happens, it essentially means that demand for STRC exceeds its current market capitalization, so Saylor will issue new shares to meet the excess demand.

The second condition, which I haven't mentioned before, is that mNAV must be higher than 1 to use the common stock ATM mechanism . I explained this in detail in another article . Strategy's core goal has always been to increase the number of bitcoins per share (bps) in the long run. When they sell MSTR stock and buy BTC when mNAV is higher than 1, this is accretive from a bps perspective; the higher the mNAV, the more significant the accretive effect of this operation; when mNAV is exactly equal to 1, this operation is neutral; but when mNAV is lower than 1, using the money from selling MSTR to buy BTC would dilute from a bps perspective, so they would avoid doing so.

As you may have noticed, in the previous section I mentioned that using the MSTR ATM mechanism can both expand company size and reduce leverage. However, if mNAV is higher than 1x, then using the common stock ATM has an additional benefit—increasing the bps ratio.

Incidentally, the mNAV metric is actually displayed directly on the Strategy.com homepage. They are using the most diluted mNAV as a reference, which is correct. Currently, the value is about 1.2 times, while I believe the lowest it will be since 2026 will be only around 1 times.

So what if a situation arises where Saylor is forced to issue new STRC shares due to excessive demand for STRC, but his mNAV is below 1x? Does this mean he can't use MSTR's ATM to maintain a stable leverage level, thus being forced to increase his leverage?

First, I think this scenario is unlikely because the fact that STRC can trade stably at $100 itself implies that investors have confidence in the overall structure, so MSTR's mNAV should theoretically be at least 1x. Second, this assumption ignores the fact that they have another tool to control the demand for STRC—reducing dividends.

The question remains: can the 11.5% dividend yield be sustained?

First, let me remind you that STRC's dividend yield was 9% when it was launched. Dividend yield is a tool that can be adjusted to simultaneously match the demand for STRC and ensure its price remains near par value.

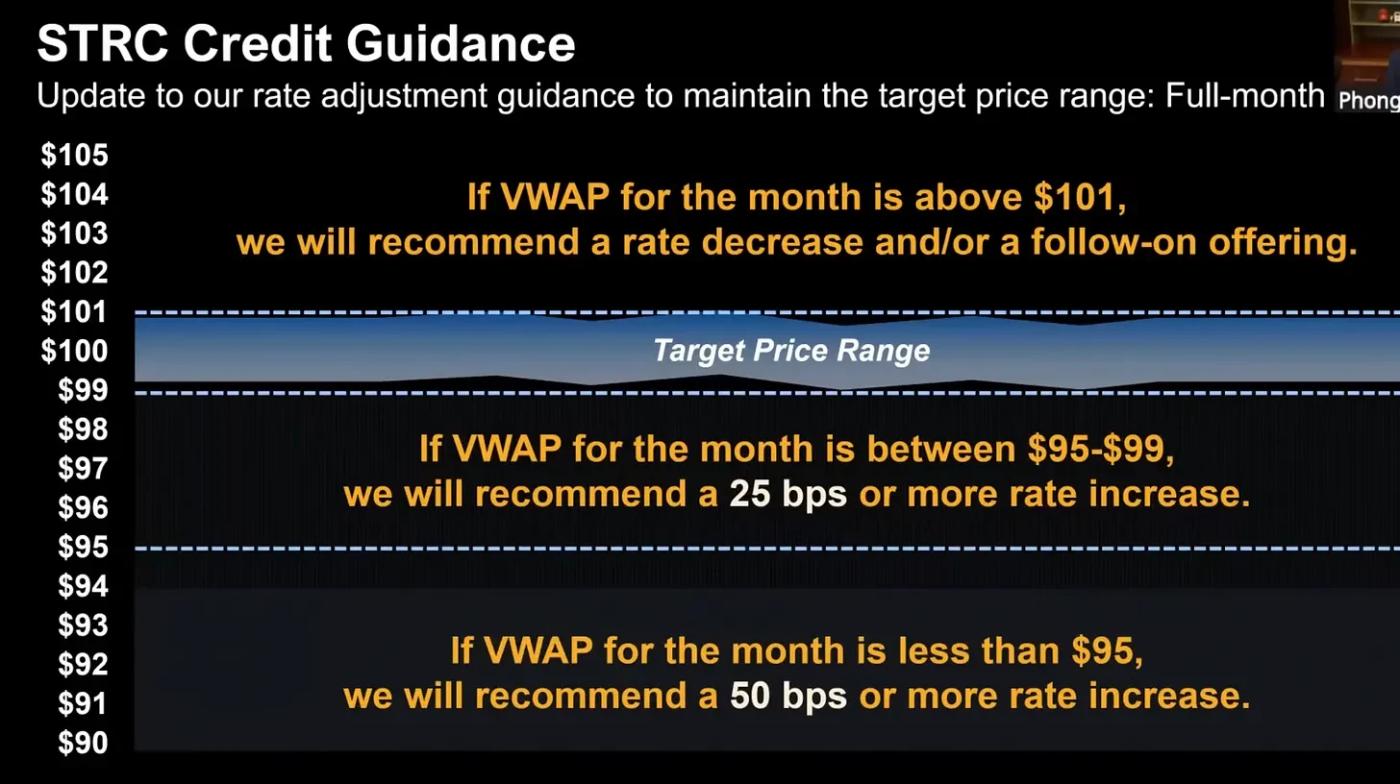

Strategy's current guidance is as follows: if the monthly VWAP (volume-weighted average price) of STRC is between $95 and $99, they will increase the dividend yield by 25 basis points (bps); if the monthly VWAP is below $95, they will increase it by 50 basis points; and if the monthly VWAP is above $101, they will decrease the dividend yield.

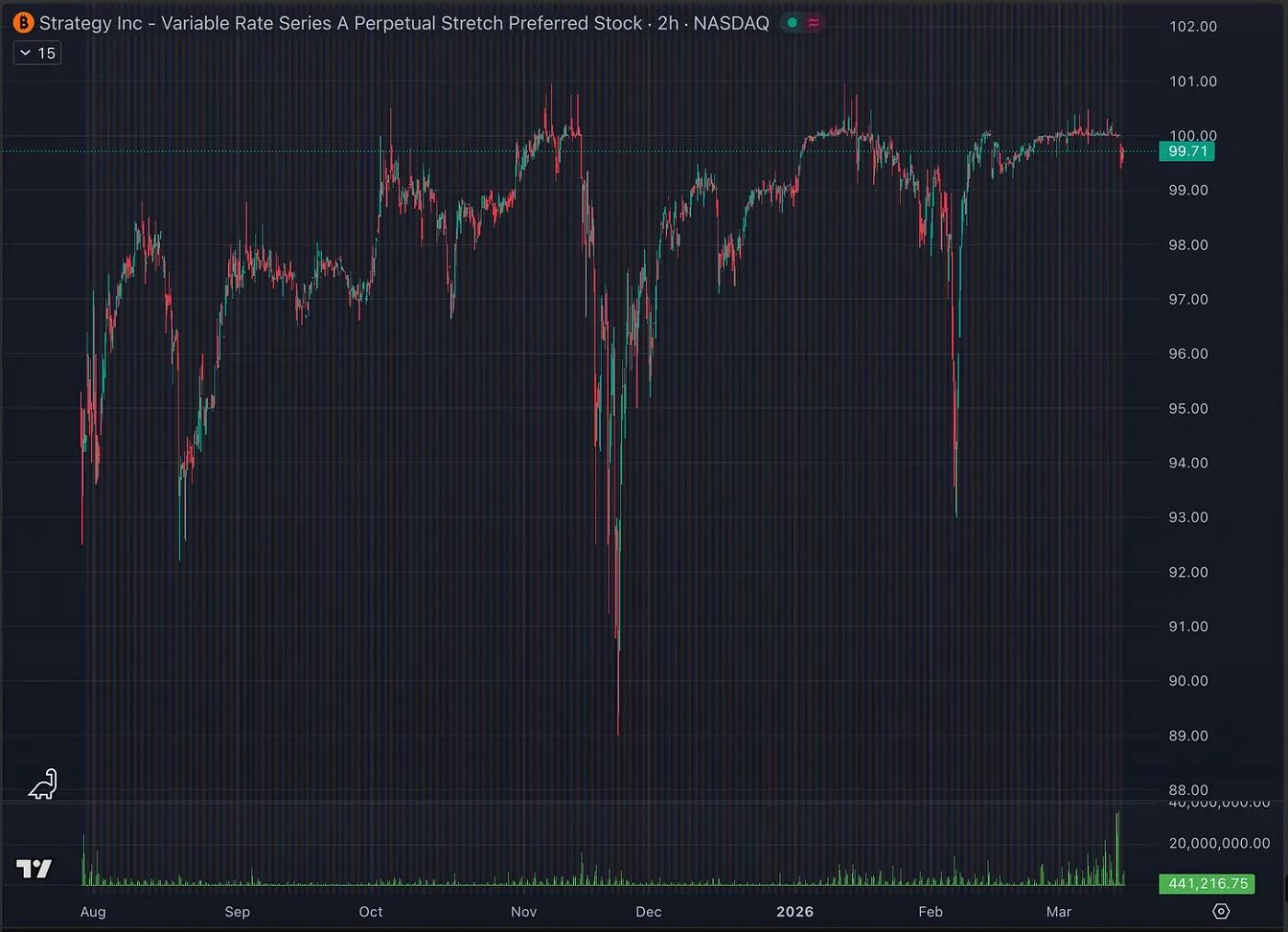

Therefore, what they've done so far has essentially been to gradually increase STRC's dividend yield from 9% to 11.5% to achieve a balance where STRC fluctuates around $100 in daily trading. This week has been STRC's most successful week to date, as it has not only continued to trade near par value but has also seen extremely high trading volumes (approximately $300-400 million per day, compared to an average of just over $100 million previously).

Odaily Note: STRC's trend chart since its launch.

The requirements of the STRC fundamentally depend on several variables:

- Credit risk: What is Strategy's current leverage ratio? In other words, how much BTC is currently "supporting" STRC? This depends directly on the price of BTC—if BTC falls, all else being equal, the leverage ratio will increase, credit risk will increase, and demand for STRC will decrease (i.e., the price of STRC will fall).

- Yield: What is the current dividend yield paid by STRC? The higher the dividend yield, the greater the demand for STRC.

- Awareness: How many people know that STRC exists? This is a very important factor in the first few months or years after the product launch, because it is essentially a variable that only increases, and all else being equal, it will significantly affect the demand for STRC.

- Confidence: How many people are willing to invest in STRC after seeing it trade for months and continue paying dividends? This is a special factor because confidence can fluctuate greatly—if STRC trades in a narrow range close to $100 for a long time, more and more people will consider it safe; but if we suddenly see it drop 10% in a single day, that confidence can also disappear quickly.

Since the launch of STRC, we have seen the following: credit risk has increased (due to the 45% drop in BTC from its all-time high), yields have increased, awareness has increased, and confidence has increased . One factor has negatively impacted demand, while the other three have had a positive effect. We are now finally in an "ideal" state: STRC is stabilizing around $100.

With BTC priced around $68,000, an 11.5% yield is the dividend level needed to pull the STRC price back to par value. For a product that has been listed for less than eight months, this seems like a fairly positive sign to me. Saylor projects BTC to have a compound annual growth rate (CAGR) of 20–30% over the next 20 years. As I explained in detail in another article , under this assumption, issuing debt at an 11.5% interest rate to purchase an asset with a 25% annual growth rate is perfectly reasonable. Theoretically, you could even pay higher interest rates and profit from the arbitrage between the interest cost and the expected annual return of BTC.

In my view, the most likely development path is that demand for STRC will continue to grow, while Strategy will gradually reduce its dividend yield back to 10% (or even below that level for a long period) in order to reduce the company's interest costs while controlling demand.

What happens to STRC if everyone wants to sell?

In this scenario, the price of STRC would plummet! In fact, we've already seen similar situations with this product several times: In August 2025, STRC fell from $98 to $92 (a 6% drop); during the market sell-off in November 2025, STRC fell from $100 to $89 (an 11% drop); and in February of this year, it fell again from $100 to $93 (a 7% drop).

It's important to note that Saylor's explicit goal is to keep STRC within a narrow range close to $100, and STRC has become a core focus for Strategy. Therefore, if the average price of STRC falls below $99 over a month, Strategy will increase the dividend yield to bring demand back to a level that supports a $100 price. As long as market participants have confidence in Strategy's ability to maintain this mechanism, there will always be bargain hunters below $100, hoping to profit through "reversion to par arbitrage" trades.

In the short term, the price could indeed drop by 10% due to panic among holders. But if you have confidence in the structure that Strategy has built, the price will typically return to near par value within days or weeks—as we have seen in the past.

Why can't the dividend yield rise indefinitely?

Let’s assume that STRC fails to revert to par value, which means that Strategy must keep increasing the dividend yield… and since the dividend yield has no upper limit in form, does this look like a “death spiral” scenario? Actually, it’s not quite like that.

First, you need to understand that the so-called dividend "guidance" does not legally bind Saylor to any action. Ultimately, companies have complete autonomy over their dividend yield, and they can stop increasing it even when the average monthly price is below $99.

If Strategy anticipates BTC to grow by 20-30% annually, they likely have an acceptable "maximum dividend yield" in mind, perhaps around 15%. Once that level is reached, they will disregard the trading price of STRC and stop further increasing the dividend yield.

It's important to remember that dividend yields can be adjusted monthly . If you anticipate a recovery in BTC after the bear market, a higher dividend yield doesn't need to be maintained indefinitely. As BTC prices rise again, the credit risk of STRC will improve, mechanically increasing demand for STRC and pushing its price back near par value. At that point, Strategy can resume lowering the dividend yield. In the long term, even if the dividend yield briefly rises to 13% during a period of stress, STRC's dividend yield will likely eventually fall back to a level similar to 8%.

In the next section, I will outline a worst-case scenario: what would happen if BTC entered a prolonged bear market and Saylor was forced to continuously increase the dividend yield.

Understanding Risk

After reading the entire article, it seems like everything will go smoothly, but there's no such thing as a free lunch. So, as a STRC holder, what risks do I actually bear?

Let me first clarify my position: I believe the market is currently mispricing the risk of STRC. Given a reasonably bullish assumption about BTC price, its risk-reward ratio is quite attractive. Note that I am not saying you can obtain high returns with zero risk; risk does exist and is always related to BTC's performance.

I believe there's a mismatch between people's expectations for BTC's future price movement and their perception of the risks associated with STRC. Simply put, if you look at the expectations of crypto-native investors for BTC over the next few years, 95% of them anticipate scenarios that won't have a substantial impact on STRC. In other words, within their own BTC expectation framework, they believe they can achieve a return of over 10% with "low risk." But let's discuss these risks in more detail.

Risk 1: Asymmetry between downside risk and upside potential.

The structure of STRC means that if you buy at $100, its upside is limited to the annual dividend yield (currently 11.5%), while its downside could be 0–10% within a few days—based on historical price performance.

This means that if the STRC drops 6% in a week, you effectively lose the equivalent of half a year's dividend income temporarily. This could be a problem if you need to exit your position quickly.

If your goal is to hold STRC long-term, then this isn't so important. As long as you believe it will eventually return to $100, you can still exit your position without a discount. As a reminder, STRC dividends are return-of-capital, meaning holders don't pay taxes on dividends, so they don't have a strong incentive to trade in the short term.

Risk 2: STRC and BTC fall simultaneously

STRC's credit risk is directly related to the price of BTC, so you may have noticed that STRC pullbacks typically occur when BTC experiences a significant sell-off. This means that your "stable, yield-generating asset allocation" will incur losses precisely when you, as a crypto bull, are most vulnerable.

Odaily Note: The biggest drops in IBIT (BlackRock Bitcoin ETF) have often been accompanied by drops in STRC.

Risk 3: STRC traded at a discount for an extended period.

People's confidence that STRC can return to par value stems from two factors: its actual credit risk and the risk perception formed by historical price movements. However, the second factor could also have a reverse effect: what happens if everyone believes a 5% drawdown will be quickly reversed, but then one day that doesn't happen?

If that happens, those who bought at the 5% pullback might choose to exit their positions, causing prices to fall further and potentially triggering a new wave of emotional selling, ultimately resulting in a larger drop. We can imagine a scenario where the STRC falls 15% and fails to rebound within days; previously accumulated confidence could gradually erode, leading to even greater selling pressure.

In this situation, what can break this vicious cycle? The answer remains the price of BTC. Saylor's entire strategy is ultimately built on the expectation that BTC will generate returns of over 20% annually for the next decade or more.

Risk 4 (Worst-case scenario): The fundamental risk always lies in the performance of BTC.

The worst-case scenario for STRC is what I just described, but at the same time, BTC fails to recover its strength in a prolonged bear market. Because so many variables are involved, it's difficult to predict precisely what will happen in this situation, but it's roughly like this: STRC will continue to trade below par value, so Saylor will increase the dividend yield each month in an attempt to pull its price back to $100.

At some point, the dividend yield will become unreasonably high, so he will stop increasing it and simply maintain it at a certain level. This means he will no longer follow the previous "guideline"—that is, increasing the dividend yield when monthly VWAP is below $99. Remember, this is just a guideline; there is nothing that forces him to adhere to it.

Failure to follow this guideline would further erode market confidence in STRC, which could continue to trade at a significant discount, such as a 40% discount and a 15% dividend yield, implying an actual yield of up to 25%.

MSTR will also trade below 1x mNAV, meaning the company cannot help pay dividends by selling MSTR shares. Strategy will rely entirely on its dollar reserves to pay dividends, and currently their reserves are sufficient to cover 28 months (approximately 2 years and 4 months) of dividend payments. As these 28 months draw to a close, all related assets may face greater pressure, and BTC, MSTR, and STRC will all have more reasons to continue falling.

Once its dollar reserves run out, Strategy will have to gradually sell off its BTC. Currently, its annual dividend payout is approximately $1 billion. If this figure rises to $2 billion, Strategy would have to sell about $200 million worth of BTC each month to maintain dividend payments. Alternatively, they could choose to stop paying dividends altogether. In this case, the value of preferred stock, STRC, and MSTR would further decline, and the company would have little to do until the price of BTC recovers.

This is roughly the outline of the worst-case scenario. As you can see, Strategy's dollar reserves provide a huge buffer against a prolonged bear market because, in theory, Strategy could do nothing but pay dividends from its reserves for more than two years without being forced to take action.

We are currently in the middle of a BTC bear market, with prices around $70,000 (a drop of about 45% from the peak), but STRC is still trading near par value (dividend yield of 11.5%) and mNAV is 1.2x. Considering that I don't expect BTC to experience a two-year bear market (the 2022 bear market lasted about a year from peak to trough), and that Strategy hasn't even started using its dollar reserves yet, I believe that at the current leverage level, Strategy's overall structure is quite safe and resilient.

Risk 5 (Long-term concern): Strategy's model is too effective.

As I said on X yesterday, the biggest risk associated with Strategy as a BTC bull is that it might be running too successfully .

"The biggest bearish argument against Strategy is that the strategy is working too well. If it's successful, they will keep increasing their BTC holdings. But eventually they will become too large, thus polluting the original 'pure' narrative of BTC. In fact, this is already happening."

In fact, Strategy already holds approximately 3.5% of the total BTC supply. This could negatively impact future BTC demand, as it may begin to undermine the narrative of BTC as a purely decentralized asset. Furthermore, the narrative surrounding STRC and its high-yield "digital credit" has also generated some negative reactions within the crypto community, which could indirectly affect BTC demand as well.

As I explained throughout the article, Strategy's BTC holdings will only continue to increase. The only scenario that could prevent this is a painful cycle for BTC lasting at least two years. Even then, it would require an even longer period of market downturn before Strategy's BTC reserves gradually decrease due to dividend payments.

I can understand why some people are uneasy about Strategy's role in the BTC ecosystem. But in my opinion, if this alone is enough to turn you bearish on BTC's long-term prospects, then you probably weren't so bullish on BTC in the first place. From my perspective, it's not a particularly serious matter. It's true that Strategy is a single entity holding 3.5% of the BTC supply, but ultimately, Strategy and its BTC reserves belong to its shareholders.

How different is this from BlackRock holding a similar amount of BTC on behalf of IBIT shareholders? Of course, they are not entirely the same, and IBIT does not face bankruptcy risk. But in my view, they are similar in some ways—they both represent the financialization of BTC, a trend that is itself inevitable.

I don't believe Strategy and STRC pose a systemic risk to BTC, but I do understand the potential negative impact they could have on the BTC narrative. In any case, this article primarily aims to help you understand the structure of STRC and Strategy. After that, you can decide for yourself whether you are more bullish or bearish on them.

Is STRC the new UST?

In recent social media discussions, comparisons between STRC and Luna/UST/Anchor have been mentioned far too frequently, so I think it's worth discussing in detail. In reality, these two are completely different things on many levels.

Odaily Note: LUNA price chart before the crash.

UST is a stablecoin, so maintaining its peg to $1 is crucial; STRC, on the other hand, is a preferred stock that ideally trades within a 1% range of close to $100, but it's entirely possible for it to drop by several percentage points. This has happened before and will happen again, and it's not necessarily a problem in itself.

UST is backed by LUNA, and LUNA's value, in turn, depends to some extent on UST's success. When UST falls below its peg price, users can exchange UST for newly minted LUNA. This increases selling pressure on LUNA, weakening market confidence in the system and further increasing selling pressure on UST. The result is a reflexive death spiral that can drive the value of both UST and LUNA to near zero within days. STRC does not have this reflexive mechanism because a drop in STRC's price does not trigger forced issuance, redemptions, or dilution of other assets within the system, nor does it affect BTC.

Anchor offers UST a yield of 18%–20%, which is not only significantly higher than STRC's current yield of approximately 11.5%, but is also largely subsidy-driven and structurally unsustainable. STRC's yield is relatively straightforward: Strategy projects BTC will have an annualized return of over 20% over the next decade, with STRC holders receiving the initial approximately 11.5% (or the then-current dividend yield) with relatively low volatility, while MSTR shareholders bear the remaining upside and volatility.

We also have a very clear understanding of how Strategy will continue to pay dividends. If mNAV is above 1x, they can issue MSTR shares via ATMs; if mNAV is below 1x, they can rely on their dollar reserves (currently sufficient to cover dividend payments for more than two years). If the reserves run out, they can eventually sell BTC derivatives or directly sell the BTC in their treasury. In the case of UST and Anchor, it's essentially just—"Trust me, I'll definitely keep throwing money at you."

The impact of price declines on these two systems is also completely different. When the UST loses its anchor, confidence collapses rapidly, and the market quickly assumes the system may go to zero; while for the STRC, a lower price means a higher effective return, which may actually attract new buyers. For example, in a completely pessimistic scenario, if the STRC trades at $50 with a dividend yield of 12%, its effective return is approximately 24%.

Finally, their time dynamics are completely different. Luna/UST is an extremely fragile system that could collapse within days after a loss of confidence. For STRC, even in the worst-case scenario described above, the process would be much slower (a very slow decline), potentially taking years, unless you assume BTC suddenly and catastrophically drops by 90% within a few months.