Introduction: From "Regulatory Hell" to "Innovation Paradise" — A Belated Paradigm Shift

In March 2026, Michael Selig, the 16th Chairman of the U.S. Commodity Futures Trading Commission (CFTC), gave an exclusive interview to the cryptocurrency podcast Bankless. This was not a typical regulatory official interview, but a historically significant policy declaration.

Over the past few years, the US crypto industry has experienced a dark period known within the industry as "regulatory hell." Former SEC Chairman Gary Gensler, with "enforcement is regulation" as his core strategy, issued Wells Notices to dozens of crypto companies and filed lawsuits, forcing a large number of innovators and capital to move offshore. At the same time, the CFTC, during the Biden administration, also attempted to stifle the prediction market in its infancy by enacting rules to ban contracts for political events and sporting events.

However, everything began to change after the 2024 election. The Trump administration brought a drastically different regulatory philosophy. Selig had previously served as a clerk under former CFTC Chairman Christopher Giancarlo, known as the "Crypto Dad," and then spent a decade representing crypto companies at a private law firm, witnessing firsthand the entire process of regulatory crackdowns. In March 2025, he joined the SEC's Crypto Task Force as Chief Legal Counsel, driving a series of reforms including staking compliance and ending enforcement oversight. In December of the same year, he was confirmed as the 16th Chairman of the CFTC, officially ushering in a new era of crypto regulation in the United States.

This interview covered seven core topics: the legal definition of commodities and the regulatory boundaries of the CFTC, the "de-banning" of prediction markets and federal jurisdiction, the definition of insider trading in information markets, the clarification of the security/commodity attributes of crypto assets, the safe harbor for DeFi developers, the "return to the US" strategy for perpetual contracts, and the grand vision of the US becoming the "crypto capital" in five years.

Selig stated his core mission at the outset of the interview: "I want us to be the cryptocurrency capital not only today, but also to ensure that we remain so for many years to come. I want to ensure that even if the next Gary Gensler emerges, the rules and regulations will be clear enough to keep these innovations in the United States for the long term."

This statement is both a promise and a warning—the results of reform need to be institutionalized, and cannot rely solely on the political will of a particular government.

Chapter 1: Redefining “Commodity” — The Constitutional Power Boundaries of the CFTC

1.1 Legal definition of "commodity": encompassing almost everything

To understand the CFTC's role in crypto regulation, one must first understand the legal implications of the core concept of "commodity".

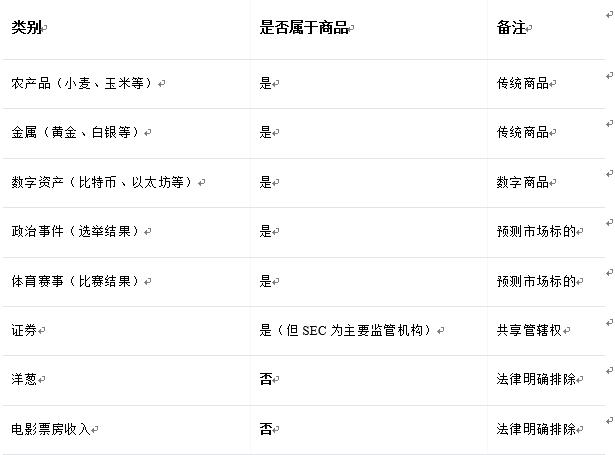

In the interview, Selig gave a startling answer: According to the 1974 amendment to the Commodity Exchange Act, the definition of a commodity is extremely broad, encompassing almost everything that can be the underlying asset of a derivative contract—agricultural products, metals, digital assets, intangible assets, services, rights, interests, political events, sporting events…

Ryan pressed further: "Then what isn't a commodity?"

Selig's answer was concise and humorous: "Onions and movie box office revenue are the only things that are not commodities."

Onions were excluded because of severe price manipulation in the Chicago onion market in the 1950s, leading to Congress passing legislation specifically to exclude them. Movie box office revenue was excluded because the Motion Picture Association of America (MPAA) successfully lobbied to prevent the establishment of a box office futures market. Aside from these, almost anything with a market can theoretically become the underlying asset for CFTC-regulated derivatives contracts.

The breadth of this definition provides a solid legal foundation for the CFTC's regulatory authority in the areas of crypto assets and prediction markets.

1.2 CFTC's Regulatory Boundaries: Derivatives, Not Spot Commodities

Having understood the broad definition of "commodities," it is also necessary to clarify the CFTC's actual regulatory scope. Selig clearly pointed out that the CFTC's core function is to regulate the derivatives market, not the spot market for all commodities.

Specifically, the CFTC's regulatory authority covers the following categories:

• Futures Contracts: Standardized contracts traded on regulated exchanges.

• Swaps: Over-the-counter derivatives included in the regulatory framework under the Dodd-Frank Act.

• Event Contracts: A regulatory form of prediction markets

• Leveraged spot trading: Spot commodity trading financed with margin.

It is worth noting that the CFTC does not have comprehensive regulatory authority over spot markets (such as the direct buying and selling of Bitcoin), but it does have anti-fraud and anti-manipulation powers—the CFTC has the right to intervene if someone manipulates prices in the Bitcoin spot market, thereby affecting futures prices.

If the Clarity Act is passed, it will further expand the CFTC's regulatory authority over the digital asset spot market, which is also one of the legislative goals that Selig is actively promoting.

1.3 Three Major Technological Revolutions: New Frontiers for CFTC Regulation

Selig likens the current transformation of commodity markets to the electronic revolution of the 1980s—when futures trading shifted from manual outcry halls to electronic matching systems, revolutionizing the entire industry. Today, three major technologies are simultaneously reshaping the face of commodity markets:

First, blockchain and crypto assets: decentralized value transfer networks are creating entirely new financial infrastructure.

Second, prediction markets: Through the mechanism of "collective intelligence," they aggregate scattered information into price signals, becoming a powerful supplement to traditional polls and media reports. In the 2024 election, the prediction accuracy of prediction markets significantly outperformed traditional polls, fully demonstrating their informational value.

Third, artificial intelligence is reshaping the underlying logic of information consumption, transaction decisions, and work methods.

Selig argues that the previous administration's suppression of these three technologies was essentially an "anti-future" ideological bias, rather than based on objective risk assessment. The new CFTC's mission is to provide a clear regulatory framework for the development of these three technologies in the United States.

Chapter Two: The “Unbanning” of Prediction Markets — From Political Suppression to Federal Protection

2.1 The repeal of the 2024 rule proposal: the end of a political maneuver.

One of the most noteworthy policy actions during the interview was Selig's announcement of withdrawing the previous government's "2024 Event Contracts Rule Proposal".

This proposal, put forward by the former chairman of the CFTC under the Biden administration, aims to ban political event contracts and sports event contracts from being listed on regulated exchanges. Selig's assessment of this is quite blunt:

"This is a highly biased rule proposal aimed at blocking political event contracts on the eve of the 2024 election... It is a deliberate effort to ensure that channels capable of spreading fake news and polls remain unimpeded, while preventing the truth revealed by prediction markets from seeing the light of day in the United States."

As it turns out, prediction markets far surpassed traditional polls in their accuracy during the 2024 election, with platforms like Polymarket predicting Trump's victory well in advance. This result not only validates the informational value of prediction markets but also makes the previous administration's repressive actions appear particularly suspicious.

Selig withdrew the proposal and made it clear that the CFTC would establish a clear regulatory framework for political event contracts and sports event contracts, rather than banning them outright.

2.2 Defending Federal Jurisdiction: Responding to Lawsuits in 50+ States

The legalization of prediction markets has not been smooth sailing. Currently, more than 50 states across the US have filed lawsuits against prediction market platforms such as Kalshi, Polymarket, and Crypto.com. The core issue is whether prediction markets are derivatives regulated by the CFTC federally or gambling activities governed by state laws.

Selig took aggressive legal action, submitting an amicus curiae opinion to the court, explicitly arguing that the CFTC has exclusive federal jurisdiction over prediction markets. Their core argument is:

• The Commodity Exchange Act explicitly grants the CFTC regulatory authority over derivatives contracts.

• When a derivatives contract is listed on an exchange registered with the CFTC, federal law prevails over state law.

• The CFTC never enforces laws in casinos or Indian reservations, but when derivative contracts are based on sports or political events, this falls under the CFTC's federal regulatory purview.

Regarding the vague concept of "gambling," Selig stated that it will clarify it through rule-making and await the final court ruling.

2.3 New Frontiers of Insider Trading: From Mr. Beast to Political Candidates

The rapid development of prediction markets has also brought new challenges to the regulation of insider trading. Selig cited two typical cases in the interview:

Case 1: An employee of Mr. Beast (a well-known YouTube blogger) took advantage of his prior knowledge of video release information to engage in insider trading in the relevant prediction market. He was sued by Kalshi and fined.

Case 2: A political candidate who used insider election information to trade in the market that predicted his election results was also sued by Kalshi.

Selig points out that the determination of insider trading in prediction markets is governed by a "misappropriation theory" similar to that in securities markets: if someone obtains information based on a duty of confidentiality to their employer or another person and then trades in violation of that duty, it constitutes insider trading. This standard is relatively clear and supported by ample judicial precedent.

He also emphasized that the CFTC welcomes participants who trade based on a genuine information advantage—this is the core mechanism by which prediction markets discover prices and aggregate information. The regulatory goal is to combat improper misappropriation, not to suppress legitimate information trading.

Chapter 3: The "Identity Card" of Crypto Assets — Securities or Commodities?

3.1 Limitations of the Howey Test and the Digital Goods Clarity Act

The debate over the regulatory status of crypto assets has been the biggest source of legal uncertainty in the US crypto industry for the past few years. The SEC's insistence on using the Howey test, established in 1946, to determine whether crypto assets constitute securities has led to a large number of projects falling into a legal gray area.

Selig is keenly aware of this. He points out that the Howey test itself is not unsuitable for crypto assets, but the problem lies in the fact that regulators use it for enforcement rather than rulemaking, preventing the industry from obtaining clear compliance guidance in advance.

He and SEC Chairman Paul Atkins jointly promoted "Project Crypto," which has already provided a preliminary classification framework through regulatory interpretation without relying on legislation.

• Digital Commodities: Network tokens, such as Ethereum (ETH), Solana (SOL), etc. — not securities.

• Digital Collectibles: Non-fungible assets such as NFTs — not securities (and possibly not commodities).

• Digital Tools: Functional receipt tokens, etc., on the blockchain — not securities

However, Selig also acknowledged that regulatory interpretation cannot completely replace legislation. The value of the Clarity Act lies in enshrining these classifications in law, ensuring they won't be overturned by the next administration. Polymarket data shows the bill has approximately a 70% chance of passing in 2026.

3.2 The Vision of “Super Apps”: The Historic Reconciliation Between the SEC and the CFTC

One of the most exciting moments of the interview was when Ryan asked directly: "Is the turf war between the CFTC and the SEC over?"

Selig's reply was only three words: "Yes, rest in peace."

Behind this brief response lies a historically rare deep collaboration between the two regulatory bodies. Selig and Atkins are jointly advancing "Project Crypto," aiming to establish a unified, cross-agency coordinated regulatory framework for crypto assets, with core visions including:

• Tokenization: Allows for the on-chain tokenization of securities and derivatives collateral, unifying technical standards.

• On-chain financial applications: Providing a compliance path for DeFi protocols and bringing offshore activities back to the United States.

• Single regulatory body: Allows a company to offer securities and commodity services under a single regulatory body (“super app” model)

• Interoperability: Ensure interoperability between the SEC-regulated securities chain and the CFTC-regulated derivatives chain.

If this vision is realized, it will completely change the landscape of US financial regulation and create a truly unified and compliant market for the crypto industry.

Chapter 4: A Safe Haven for DeFi Developers — From “Potential Criminals” to “Protected Innovators”

4.1 The spectrum of intermediary institutions: from fully centralized to fully decentralized

Over the past few years, the biggest misconception that US regulators have had about DeFi has been that all on-chain software developers are "intermediaries," and therefore they are required to register as exchanges or brokers. This misconception has forced many DeFi projects to move offshore or operate in the shadow of the law.

Selig explicitly proposed an analytical framework for the intermediary spectrum:

• Left end of the spectrum (highly centralized): Traditional exchanges, which hold user assets, facilitate transactions, and assume full regulatory responsibility.

• Middle of the spectrum: L2 networks and other highly automated infrastructure with partial control.

• Right end of the lineage (highly decentralized): Pure code pushers and non-custodial wallet providers should not be considered intermediaries.

He explicitly stated that "software developers who merely push code to the blockchain, or developers who provide non-custodial digital wallet programs, are fundamentally different from exchanges that host user assets," and should not be subject to the same regulatory requirements.

4.2 Safe Harbor and Innovation Exemption: Thomas Edison did not need to apply for a license.

Selig proposed two specific policy tools to protect DeFi developers and early innovators:

First, Safe Harbor: This defines a clear regulatory exemption zone for fully decentralized on-chain activities, ensuring that "permissionless innovation" can legally take place in the United States. He cited a powerful historical analogy: "Thomas Edison could innovate without a license. We must preserve this framework for those who simply want to push boundaries and test new technologies."

Second, the Innovation Exemption: This provides a time- or scale-limited regulatory exemption window for early-stage projects, allowing them to quickly enter the market to test their products without fully registering as exchanges or brokers. The design logic of this exemption is that projects should not be bound by full registration requirements while seeking product-market fit; once scaled up, they can be gradually incorporated into the full regulatory framework.

Selig stated that these two policy tools are being actively pursued and are expected to be implemented in the "very near future."

4.3 The Regulatory Dilemma of L2 Networks: Having Control But Not Wanting Control

During the interview, David raised a rather thorny regulatory issue: Ethereum L2 networks (such as Arbitrum, Optimism, etc.) have a certain degree of control over transaction ordering in terms of technology, but these networks themselves do not want to exercise this control, nor do they want to assume regulatory responsibilities at the exchange level.

Selig's response reflects the new CFTC's "principles-based" regulatory philosophy: "We need to develop purpose-appropriate rules for all these technologies, rather than fitting everything into the old 'intermediary' framework." He explicitly stated that the CFTC's regulatory framework is flexible enough to develop differentiated compliance standards for different technology architectures, rather than requiring all software with a certain control vector to register as an exchange.

Chapter 5: The "Return to the US" of Perpetual Contracts — The Largest Crypto Liquidity Hotspot

5.1 The Offshore Dilemma of Perpetual Contracts: The Largest Source of Liquidity Forced to Leave

Perpetual futures (Perps) are the most traded product type in the crypto derivatives market and one of the most important sources of liquidity in the entire crypto market. However, due to the uncertainty of US regulation, this market has long been able to operate only on offshore exchanges such as Binance, OKX, and Bybit, preventing US users and institutions from legally participating.

Selig bluntly stated: "Perpetual contracts have been flowing offshore for years, and in my opinion, they are the biggest source of liquidity in our crypto market."

Currently, the "quasi-perpetual contracts" available in the US market are actually 50-year long-term futures contracts—a product of regulatory arbitrage, using extremely long expiration dates to simulate the economic effects of perpetual contracts. Selig argues that this workaround is not fundamentally different from genuine perpetual contracts in terms of risk management, but it creates unnecessary legal uncertainty.

5.2 Technical Barriers: Futures or Swaps?

The main technical hurdle for the return of perpetual contracts to the United States lies in the uncertainty of their regulatory affiliation: are they futures contracts or swaps?

This distinction is crucial because, under the Dodd-Frank Act, swap contracts are subject to far more stringent regulatory requirements than futures contracts. Selig criticizes the Dodd-Frank Act's "hammer-like" regulatory approach, arguing that it treats high-risk products like credit default swaps (CDS) the same as low-risk products like agricultural swaps and Bitcoin swaps, constituting over-regulation.

His solution was:

1. Clarify the regulatory jurisdiction of perpetual contracts: Through rule-making, clarify which perpetual contracts can be classified as futures contracts (rather than swap contracts).

2. Provide no action letter or exemption: For perpetual products that are indeed swap contracts, reduce unnecessary regulatory burdens.

3. Swift Action: In the interview, Selig promised to complete the regulatory framework for perpetual contracts "within the next month or so."

The fulfillment of this commitment will mark a historic turning point for the U.S. crypto derivatives market.

5.3 Market Impact of Perpetual Contract Repatriation

The return of perpetual contracts to the United States will have a profound impact on the entire crypto market:

• Liquidity Concentration: A significant amount of offshore liquidity will flow back to the regulated US market, improving market depth and price discovery efficiency.

• Institutional participation: US institutional investors will be able to legally participate in the perpetual contract market, bringing in larger-scale capital inflows.

• Regulatory arbitrage disappears: The competitive advantage of offshore exchanges will be weakened, and US exchanges will regain their competitiveness.

• Tax compliance: Perpetual contract transactions for US users will be included in a tax compliance reporting framework, eliminating legal risks.

Chapter Six: Five-Year Vision — Making America the True "Cryptocurrency Capital"

6.1 Completed foundational work

In the interview, Selig outlined the regulatory reforms that have been completed since the new government took office:

• The Genius Act was passed: establishing a federal regulatory framework for stablecoins.

• End enforcement oversight: Stop issuing Wells Notices to innovators and replace litigation with rulemaking.

• The Digital Goods Clarity Act is nearing signing: Under the President's leadership, market structure legislation is close to completion.

6.2 Five-Year Goals: Permissionless Innovation in the United States

Selig paints a picture of the US crypto ecosystem five years from now:

A permissionless innovation environment: Innovators don't need to apply for a license every time they want to do something new. Innovation exemptions are a first step toward this goal, but the ultimate goal is to establish a systematic "default permission" framework.

On-chain markets are becoming mainstream: Traditional exchanges such as the New York Stock Exchange, Nasdaq, and CME will be able to build and operate on blockchains, enjoying the same certainty and clarity as traditional database systems. Selig believes there are no technical or regulatory reasons preventing this shift.

Regulatory super app: Allows a single company to simultaneously provide a full range of financial services, including securities, commodities, and derivatives, under a unified regulatory framework, eliminating the current problem of regulatory fragmentation.

The convergence of AI and encryption: providing a compliance framework for AI agents to participate in financial markets, ensuring that regulatory rules for algorithmic trading and autonomous agents are developed within the United States, rather than flowing to China or other competitors.

6.3 Preventing the “Next Gary Gensler”: The Necessity of Institutional Reform

The most strategically insightful statement in the interview came from Selig's opening remarks: "I want to make sure that even if the next Gary Gensler comes along, the rules and regulations are clear enough to keep these innovations in the United States for the long term."

This statement reveals a profound institutional logic: the achievements of regulatory reform cannot rely solely on the political will of a particular government, but must be solidified through legislation and rule-making. This is also the fundamental reason why Selig is so actively pushing for the Digital Goods Clarity Act—only rules enshrined in law can withstand the backlash from the next government.

Chapter Seven: In-Depth Expansion — The Underlying Logic of Regulatory Philosophy

7.1 "Principles-oriented" vs. "Rules-oriented": The Regulatory Advantages of the CFTC

Selig has repeatedly emphasized that the CFTC employs a principles-based regulatory framework, rather than a rules-based framework like the SEC. This distinction is significant in crypto regulation.

A rules-oriented regulatory framework tends to formulate detailed and specific regulations. Its advantage is that it provides a high degree of certainty, but its disadvantage is that it lacks flexibility when facing new technologies, often leading to over-regulation or regulatory gaps due to a "one-size-fits-all" approach.

A principle-based regulatory framework, by setting high-level principles and objectives, allows regulators to apply them flexibly according to specific circumstances, making it more suitable for rapidly evolving technological environments. Selig stated that this characteristic gives the CFTC a natural regulatory advantage when dealing with new technologies such as blockchain, prediction markets, and AI.

7.2 AI as a Regulatory Tool: A Regulatory Efficiency Revolution in a $500 Trillion Market

Faced with a $500 trillion derivatives market and tens of thousands of emerging prediction market contracts, how can the CFTC achieve effective regulation with limited manpower? Selig's answer is: AI.

He revealed that the CFTC has widely adopted AI and automation tools for market monitoring, and many systems no longer rely on manual review. AI can identify abnormal patterns in massive amounts of trading data and flag potential insider trading and market manipulation, making it far more efficient than traditional manual monitoring systems.

This statement has profound policy implications: regulatory agencies themselves are undergoing an AI-driven efficiency revolution, which means that future regulatory costs will be significantly reduced, regulatory coverage will be greatly expanded, and reliance on human resources will be significantly reduced.

7.3 Conflict of Interest within the Trump Family: A Test of Regulatory Independence

During the interview, David raised a sensitive question: the Trump family has a clear conflict of interest in the prediction market field—Eric Trump is both an advisor to Polymarket and an investor in Kalshi, while Selig is the CFTC chairman appointed by Trump.

Selig's response was concise and formal: he was bound by strict government ethics protocols, would not discriminate against anyone, and believed that the entire government adhered to the same standards.

While politically impeccable, this response also reveals a deep-seated systemic challenge: how to ensure the independence and impartiality of regulation when those who appoint regulators have a direct interest in the regulated market? There is no easy answer to this question, but Selig's statement at least demonstrates his personal professional stance.

7.4 "Open Doors" vs. "Enforcement Traps": A Fundamental Shift in Regulatory Culture

In the interview, Selig described an impressive cultural shift: under the previous administration, crypto companies invited to "come in for a chat" often ended up receiving Wells notices or facing lawsuits. This "enforcement trap" culture fostered a deep distrust of regulators across the industry, leading many companies to choose to operate offshore or in the shadow of the law.

The new CFTC has a completely different culture: "We no longer issue Wells notices for entering buildings. We welcome businesses to come and talk to us, and we work with them to find registration, licensing, or other compliance paths, rather than treating them like criminals."

This cultural shift is one of the most important soft factors attracting innovators back to the United States.

Conclusion: The Historical Significance and Future Challenges of the Regulatory Revolution

Michael Selig's interview is not only a policy declaration but also a profound manifesto of his regulatory philosophy. From the reinterpretation of the definition of "commodity" to federal protection of prediction markets, from the establishment of DeFi safe harbors to the return of perpetual contracts to the United States, and the grand vision of a "crypto capital" five years from now—Selig paints a complete picture of the United States re-embracing financial innovation.

However, the challenges facing this regulatory revolution are equally undeniable:

First, there is uncertainty surrounding the legislation: While the Digital Goods Clarity Act has a high probability of passing, the political maneuvering in Congress is fraught with uncertainty. Regulatory reforms without legislative support always face the risk of being overturned by the next administration.

Second, the pressure of global competition: The EU's MiCA regulations have established a relatively clear framework for the European crypto market, while jurisdictions such as Singapore and Dubai are actively vying for the status of crypto innovation hubs. US regulatory reforms need to be swift enough to gain a competitive edge globally.

Third, the potential for conflicts of interest: The Trump family's direct interests in the forecasting market, and the potential impact of the political appointment system on regulatory independence, are systemic risks to this reform.

Fourth, the speed of technological evolution: The evolution of technologies such as AI, quantum computing, and on-chain finance may once again outpace the adaptability of regulatory frameworks. Establishing a truly forward-looking regulatory system is a long-term challenge for Selig.

Nevertheless, Selig's clear thinking, pragmatic approach, and sense of historical mission demonstrated in the interview inspire optimism for the future of encryption regulation in the United States. As he stated, "This country has always been great because builders and innovators have developed new things, and the country has benefited from them. We've seen railroads, telegraph lines, and the internet. These opened up countless new possibilities for our country and our people. We can't just push these offshore and say, 'We're happy with the status quo and we can't allow new things to emerge.'"

This statement is perhaps the best summary of the entire interview — and also the best footnote to the new era of encryption regulation in the United States.

WeChat: battle000000

References

1. Bankless Podcast, “Making America the Crypto Capital of the World | New CFTC Chairman,” March 9, 2026. https://www.bankless.com/podcast/making-america-the-crypto-capital-of-the-world

2. CFTC, “Michael S. Selig, Chairman: 9th Annual DC Blockchain Summit,” March 18, 2026. https://www.cftc.gov/PressRoom/SpeechesTestimony/opaselig3

3. Bankless, “CFTC Issues New Guidance for Regulated Prediction Market Operators,” March 12, 2026. https://www.bankless.com/read/news/cftc-issues-new-guidance-for-regulated-prediction-market-operators

4. Bankless, “Perpetual Futures Poised for US Debut, Pending Final Regulator Approval,” March 3, 2026. https://www.bankless.com/read/news/perpetual-futures-poised-for-us-debut-pending-final-regulator-approval

5. Bankless, “CFTC Chief Defends Agency’s Exclusive Control over Prediction Markets,” February 17, 2026. https://www.bankless.com/read/news/cftc-chair-selig-defends-exclusive-federal-jurisdiction-over-prediction-markets

6. CFTC & SEC Joint Press Release, “CFTC Joins SEC to Clarify the Application of Federal Securities Laws to Crypto Assets,” March 18, 2026. https://www.cftc.gov/PressRoom/PressReleases/9198-26

7. TradingView/CoinPedia, “SEC, CFTC Crypto Commodity List 2026: All 16 Digital Assets Named and What It Means,” March 2026. https://www.tradingview.com/news/coinpedia:8f05e3db8094b:0-sec-cftc-crypto-commodity-list-2026-all-16-digital-assets-named-and-what-it-means/