Introduction:

As economic and trade ties between China and Malaysia continue to deepen, cross-border trade, supply chain collaboration, and personnel exchanges are constantly heating up, leading to a rapid increase in demand for efficiency in areas such as payment collection, currency exchange, settlement, and fund transfer. Particularly between Penang, Malaysia, and Fuzhou, China, Fujianese business communities, cross-border e-commerce sellers, and small and medium-sized foreign trade enterprises are becoming the most active users in upgrading cross-border payments.

KAI believes that, given that the traditional wire transfer system is still constrained by arrival time, fees, and transit losses, digital cross-border remittance services centered on USAD are becoming a new infrastructure more suited to the future trade network.

With the continued growth of trade between China and Malaysia, the demand for cross-border capital flows has also increased.

Trade and business ties between China and Malaysia are entering a phase of increased frequency. Data from the Malaysian Department of Statistics shows that Malaysia's total foreign trade reached RM2.9 trillion in 2024, a year-on-year increase of 9.2% ; China has been Malaysia's largest trading partner for the 16th consecutive year. This expansion in trade volume means that the demand for cross-border payments, settlements, and currency exchange is also growing simultaneously for both businesses and individuals.

Under this trend, cross-border financial services are no longer just financial support, but an integral part of the fundamental capabilities of cross-border commerce. For merchants engaged in foreign trade, distribution, cross-border e-commerce, and supply chain procurement, whoever can complete the collection and transfer of payments faster will have a greater advantage in terms of turnover efficiency and cost control.

Penang and Fuzhou are forging closer cross-border business ties.

As a major manufacturing and export hub in Malaysia, Penang holds a special position in the China-Malaysia trade network. Research data shows that manufacturing accounts for 46.5% of Penang's GDP, with electronic, electrical, and optical products accounting for 74% of manufacturing output. From January to October 2024, Penang's total trade volume reached RM659.4 billion , a year-on-year increase of 10.8% , contributing 31.2% of Malaysia's exports.

On the other hand, Fuzhou is accelerating its development into a hub for cross-border e-commerce and bonded logistics. The 5th China Cross-border E-commerce Fair, held in March 2025, attracted more than 1,800 supply chain and service companies , further strengthening Fuzhou's regional role in cross-border e-commerce, warehousing and logistics, and international supply chain collaboration.

From Penang to Fuzhou, this route connects not only the flow of goods, but also increasingly frequent flows of funds. For Fujianese Chinese businesses and SMEs, the limitations of traditional cross-border remittance methods are becoming more and more apparent.

Traditional cross-border remittance models are facing the real challenges of being slow, expensive, and fragmented.

Currently, most cross-border enterprises still rely primarily on bank wire transfers, SWIFT channels, or traditional payment gateways to complete international settlements. However, in real business environments, these methods generally have several problems: long settlement cycles, complex processes, opaque fee structures, and additional losses due to exchange rate fluctuations.

The problems are particularly pronounced for small and medium-sized businesses. A single cross-border payment often involves multiple steps, including payment channels, clearing institutions, banks, and intermediary banks; a single outward payment may also face issues such as wire transfer fees, intermediary bank charges, and unpredictable arrival times. Research and regulatory data both indicate that a more efficient digital cross-border payment system is becoming an important direction for lowering the barriers to international transactions for SMEs.

KAI is exploring more efficient cross-border remittance service pathways, with USAD at its core.

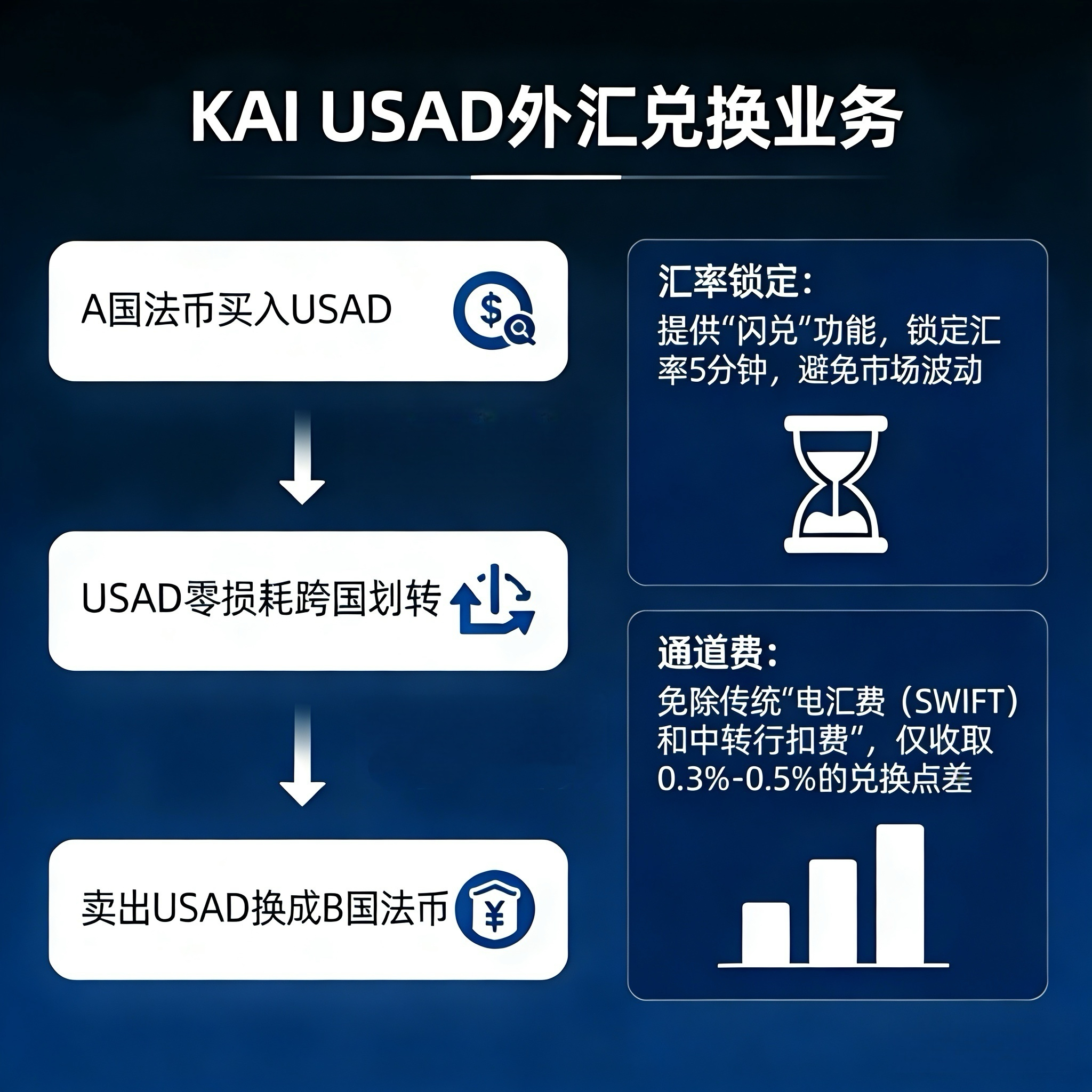

To address these pain points, KAI is leveraging USAD to build cross-border remittance services that are closer to real-world business scenarios. In KAI's business logic, USAD is not just a stable value carrier, but also an intermediary tool connecting cross-border payments, fund transfers, foreign exchange bridging, and fiat currency withdrawals.

In cross-border acquiring scenarios, overseas buyers can pay with fiat currency or cryptocurrency, and the system settles the payment in USD at the real-time exchange rate, helping merchants complete the collection of payments and funds more quickly. In cross-border currency exchange and supplier payment scenarios, enterprises can also shorten the traditional cross-border transfer chain and reduce intermediate losses by using the model of "buying USD with fiat currency in country A - transferring USD across borders - selling USD to exchange for fiat currency in country B".

KAI believes that the value of this model lies not only in technological innovation, but also in its suitability for the current global trade structure characterized by high frequency, small amounts, and multiple markets. It allows cross-border capital flows to gradually shift from the traditional model that relies on multiple intermediaries to a more real-time, transparent, and controllable digital model.

In the Web4 era, cross-border payment competitiveness will become an integral part of the global business ecosystem.

From a broader perspective, the facilitation of personnel and business connections between China and Malaysia is also continuously amplifying the demand for upgraded cross-border payments. On July 17, 2025, the visa-free agreement between China and Malaysia officially came into effect; official data shows that in 2024, the number of Chinese tourists visiting Malaysia exceeded 3.8 million . More frequent personnel movements typically lead to more active demand for tourism payments, family remittances, business payments, and cross-border consumption.

Meanwhile, Malaysia's local cross-border digital payment network is also developing rapidly. Data from Bank Negara Malaysia shows that in 2024, the country saw 4.1 million cross-border QR code payment transactions, totaling RM348.3 million . This demonstrates that the market is proving through actual transactions that faster, lighter, and less frictional payment methods are becoming a crucial support for regional economic synergy.

In conclusion, from regional trade routes to digital financial infrastructure, KAI sees a larger long-term opportunity.

From Penang to Fuzhou, the demand for cross-border remittance services is not an isolated financial issue, but rather the result of the combined evolution of China-Malaysia trade, Chinese business networks, cross-border e-commerce, and digital payments. For Fujianese Chinese merchants, independent online sellers, and small and medium-sized trading enterprises active along this route today, future competitiveness lies not only in selling products to more countries, but also in the ability to complete global fund transfers at lower costs and higher efficiency.

KAI hopes to participate in this upgrade of cross-border financial efficiency through USAD and a more open Web4 payment infrastructure. Because in the new global business ecosystem, what really matters is not just "whether the funds can arrive," but "whether the funds can arrive faster, more stably, and more intelligently."