Compiled & translated by: TechFlow TechFlow

Guest: Sean Farrell, Head of Crypto Research at Fundstrat

Host: Zack Guzman

Podcast source: Coinage

Original title: Why The Analyst Who Called Crypto's Crash Is Still Cautious

Broadcast date: March 18, 2026

Key points summary

While many investors believe that Bitcoin and other cryptocurrencies have bottomed out, market volatility and the ongoing uncertainty surrounding the war with Iran have led some analysts to remain skeptical of this optimism.

Sean Farrell, an analyst at Fundstrat who accurately predicted the market crash in February, shared his views on Bitcoin and the risks in the crypto market in an interview with Coinage. He delved into Bitcoin's potential future trajectory, factors that could impact risk assets, and why his cautious stance on the crypto market remains unchanged. Furthermore, he analyzed Hyperliquid's cross-asset growth potential, considering it one of the most noteworthy protocols in the crypto space today.

Summary of key viewpoints

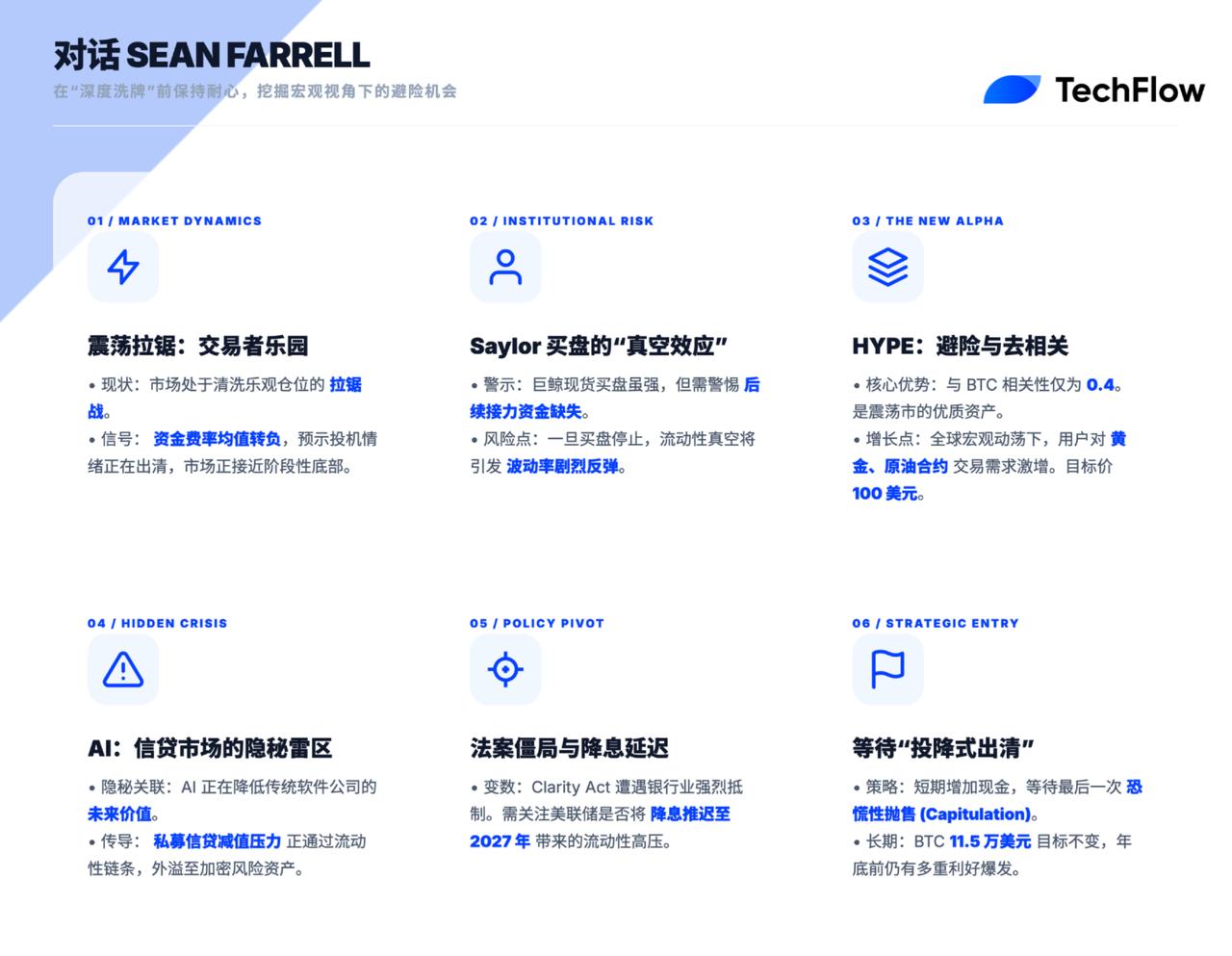

Market timing and position sizing: Now is the time for traders' "tug-of-war".

- At the beginning of the year, the market exhibited extreme position allocation, with low volatility but unusually active trading in risky assets. Coupled with miners selling off regardless of cost, I judged that there would not be much risk-reward potential in the first half of the year.

- The current market is not in a clear trend; it remains a typical trader's market. During a market uptrend, it's wiser to reserve cash.

- The 30-day moving average of funding rates has turned negative, which typically indicates that the market is approaching a more stable bottom. However, I expect a difficult adjustment period before the year-end turning point.

Institutional Game: The Vacuum of "Auxiliary Buying" Behind Saylor's Purchase

- While large institutional buying has injected liquidity, the problem is that once these spot purchases cease, the market may lack sufficient "auxiliary buying" to take over, which could increase short-term volatility risk.

- Many alternative asset management firms' stock prices have already been hit, and if credit spreads start to surge across the board, the impact on risky assets like the crypto market will be delayed but fatal.

Paradigm Shift of Top Alpha Target: Hyperliquid (HYPE)

- Hyperliquid is the most attractive asset in our portfolio. Its HIP-3 market trading volume reached $28 billion in the first 15 days of March, driven by user demand for gold and crude oil contracts amid global macroeconomic turmoil.

- HYPE has a 90-day correlation of only around 0.4 with Bitcoin (crypto assets are typically closer to 1). This low correlation makes it an important addition to building a crypto portfolio.

- We have set a target price of around $100 for HYPE, which still represents significant upside potential compared to the current price of around $40.

Macroeconomic Risks in Deep Waters: The Negative Link Between Private Lending and AI

- My biggest concern is the pressure in the private credit market. Many funds are being forced to redeem and lower their valuations. Credit spreads are widening, and it will be too late to act if we wait until spreads surge across the board.

- Many private lending targets software companies, and the rapid development of AI may reduce the terminal value of these companies, thereby affecting their credit quality. This pressure will spill over into the crypto market.

Regulation and the Federal Reserve: Catalysts of Uncertainty

- Strong opposition from banking lobbying groups and controversy surrounding stablecoin yields have clouded the bill's prospects for passage. The battle is protracted more than anticipated.

- Investors should pay close attention to whether the Federal Reserve will postpone its rate cut expectations until 2027. If this happens, it will amplify the current war risk premium and negatively impact asset prices.

- I'm waiting for a "surrender-style clearing." If the price can break through the key moving average again and CME open interest increases, I'll be more confident in increasing my investment.

Long-term vision: Target price remains unchanged.

- Despite short-term caution, I have no plans to adjust my year-end target price of $115,000, as favorable factors may emerge in the second half of this year.

Sean Farrell discusses "predicting the crypto market crash".

Zack Guzman : Welcome to the latest episode of Coinage. Today we are delighted to have our guest again – Sean Farrell, Head of Digital Asset Strategy at Fundstrat.

You appeared on our show earlier this year and successfully predicted the market downturn. Now, after a apparent rebound, the market remains volatile. I noticed you recently released a report warning of caution, particularly regarding certain sectors of the crypto space. Could you share your thoughts on the current market volatility and how this volatility is impacting the cryptocurrency market?

Sean Farrell :

I'd like to first review the situation at the beginning of the year, when I held a very cautious view of the market. The market at that time exhibited extreme positioning, with low volatility but unusually active trading in risky assets, coupled with unclear liquidity. Many investment products were trading near or even below their net asset value (NAV). Bitcoin miners, pressured by the market environment, were selling their Bitcoin holdings indiscriminately, undoubtedly exacerbating the downward trend. Based on these signals, I judged that the crypto market in the first half of the year did not offer good risk-reward potential, and that the market might face greater volatility. This judgment proved correct.

We did see a market pullback on February 5th. However, I believe that drop was more of a short-term trading opportunity, suitable for "short-term holding" rather than "long-term buying." While the market did experience some rebound afterward, the spillover effects and volatility of the crypto market as a whole remain key issues to watch.

Recent market performance has also shown some positive signs. For example, market fears have eased, and volatility in both the stock and bond markets has increased, indicating that investors are beginning to reassess market risks. In the crypto market, we've also noticed some signs of sentiment clearing, such as the 30-day moving average of funding rates turning negative. Typically, this phenomenon suggests the market may be approaching a more stable bottom. Furthermore, Strategy's recent large-scale Bitcoin purchases have injected some liquidity into the market.

Nevertheless, I remain cautious about my overall market positioning. The current market environment remains highly uncertain, especially given that cash allocations were at historic lows during January and February. Looking at major stock indices and the broader market, current market pricing still appears overly optimistic, suggesting that the market may not have truly undergone a full-blown clearing yet.

Despite the current market uncertainty, I remain optimistic about Bitcoin's long-term prospects. I believe the market may see a significant upward turn before the end of the year, but prior to that, the crypto market may need to undergo a relatively difficult period of adjustment.

For investors, closely monitoring the global macroeconomic environment is crucial, especially the Federal Reserve's monetary policy, geopolitical risks, and potential pressures on the private credit market. These factors not only impact traditional financial markets but also profoundly affect the cryptocurrency market through spillover effects. Nevertheless, I remain confident that Bitcoin's fundamentals are solid, and its value is poised to continue growing in the long term.

Will these risks definitely materialize? Not necessarily, but I believe they remain, especially considering the many potential uncertainties in the market. For example, geopolitical risks remain a key concern. Meanwhile, international oil prices remain high, nearing $100 per barrel, and the credit market is beginning to show signs of deterioration. Although these problems are not entirely due to geopolitical risks, they are indeed challenges that the market cannot ignore.

Furthermore, the Federal Reserve will hold a meeting tomorrow. Based on current market expectations for interest rate cuts, this year's rate cuts are almost entirely "excluded" from the yield curve. While I believe the Fed's policy adjustments may have some positive impact on the market in the second half of the year, given the current internal divisions and policy uncertainty within the Fed, I find it difficult to foresee them adopting a significantly accommodative stance to support the market in the short term.

Strategy's continued buying, Bitcoin fund flows, and market risks

Zack Guzman: At the beginning of the year, you mentioned that the market might experience significant volatility, and your prediction proved correct. Bitcoin did indeed drop rapidly to around $60,000 in a short period and hovered at that low for some time. What's even more interesting is that you issued this warning before the outbreak of the conflict with Iran. This makes me wonder if similar geopolitical events should also be included in market risk assessments?

Furthermore, we have inflow data from CoinShares showing that digital asset investment products have seen inflows for three consecutive weeks. You mentioned the large-scale buying by Michael Saylor and Strategy. If the market had moved in a different direction, perhaps Saylor's buying wouldn't have attracted as much attention. But when we combine these factors, we can indeed see some noteworthy trends. Could this be creating a kind of "crowding-out effect," thus suppressing the enthusiasm of other market participants?

TechFlow TechFlow Note: The crowding-out effect is a term in economics and finance, generally used to describe the phenomenon where excessive concentration of funds or resources leads to the crowding out of resources in other sectors or markets. In the crypto market, this concept is often used to describe how large investors like "whale," by buying large amounts of a crypto asset (such as Bitcoin), may drive up the price and attract market attention, thereby forcing other investors to withdraw their funds and enthusiasm or reduce their investment in other assets.

Sean Farrell:

I'm not sure if it's entirely appropriate to call it a "crowding-out effect," but I do think it's part of the market risk. We've seen similar situations many times in the past: crypto assets significantly outperforming the stock market for short periods, and these rallies are often driven by large institutional investors or "whale" like Strategy.

The problem is that once these spot purchases cease, the market's overall support may prove insufficient. If demand for Strategy's or other whale' common stock weakens within a week, the market may lack enough "secondary buying" to absorb the losses after these large-scale purchases withdraw. This situation could lead to further market volatility and increase short-term investment risk.

Why the crypto market remains a paradise for traders

Zack Guzman: You mentioned at the beginning of the year that many fund managers had very little cash reserves. In your view, does the current market risk-reward ratio mean that there is limited buying power available in the market, and that Bitcoin and other crypto assets might be the first to be affected should investors need to sell? I'd like to know, what are your biggest concerns right now?

Sean Farrell:

I agree with you; I do tend to view the market from a more tactical perspective than some of my colleagues. Based on our current assessment, I believe the market is not far from the bottom, but still some distance from the top. However, my task is to help investors better manage risk and outperform Bitcoin throughout the market cycle. Frankly, the market is not currently in a clear trend; we are still in a typical trader's market.

For investors looking to gain an edge in the market, developing a clear yet flexible tactical perspective in the short term is crucial. Looking back to early February, the market experienced a downturn, but has since rebounded significantly: Bitcoin's price has risen by approximately 20% to 25%, while Altcoin have seen even larger gains.

From the current risk-balanced perspective, I believe that during a market uptrend, it might be a wiser choice to appropriately increase "dry powder" (i.e., reserve cash or ammunition).

Sean Farrell remains bullish on Hyperliquid.

Zack Guzman: Arthur Hayes once set a price target of over $100 for HYPE. When we analyze the actual data driving HYPE's performance, we see many interesting phenomena. For example, there are a large number of users trading gold, silver, and crude oil contracts on the Hyperliquid platform. Considering these factors, do you share Arthur Hayes's bullish view on HYPE? If so, what is your target price for HYPE? Also, I know you've discussed DATs (Digital Asset Treasurys). What are your thoughts on HYPE's future development?

Sean Farrell:

Last year we set a target price for HYPE at around $100 per token. Compared to the current price, HYPE still has considerable upside potential (HYPE was priced at $40.55 at the time of the show).

From a fundamental perspective, Hyperliquid is one of the most attractive assets in our portfolio. This includes not only the Hyperliquid token HYPE, but also the related digital asset treasury company Hyperliquid Strategies, which has also performed exceptionally well.

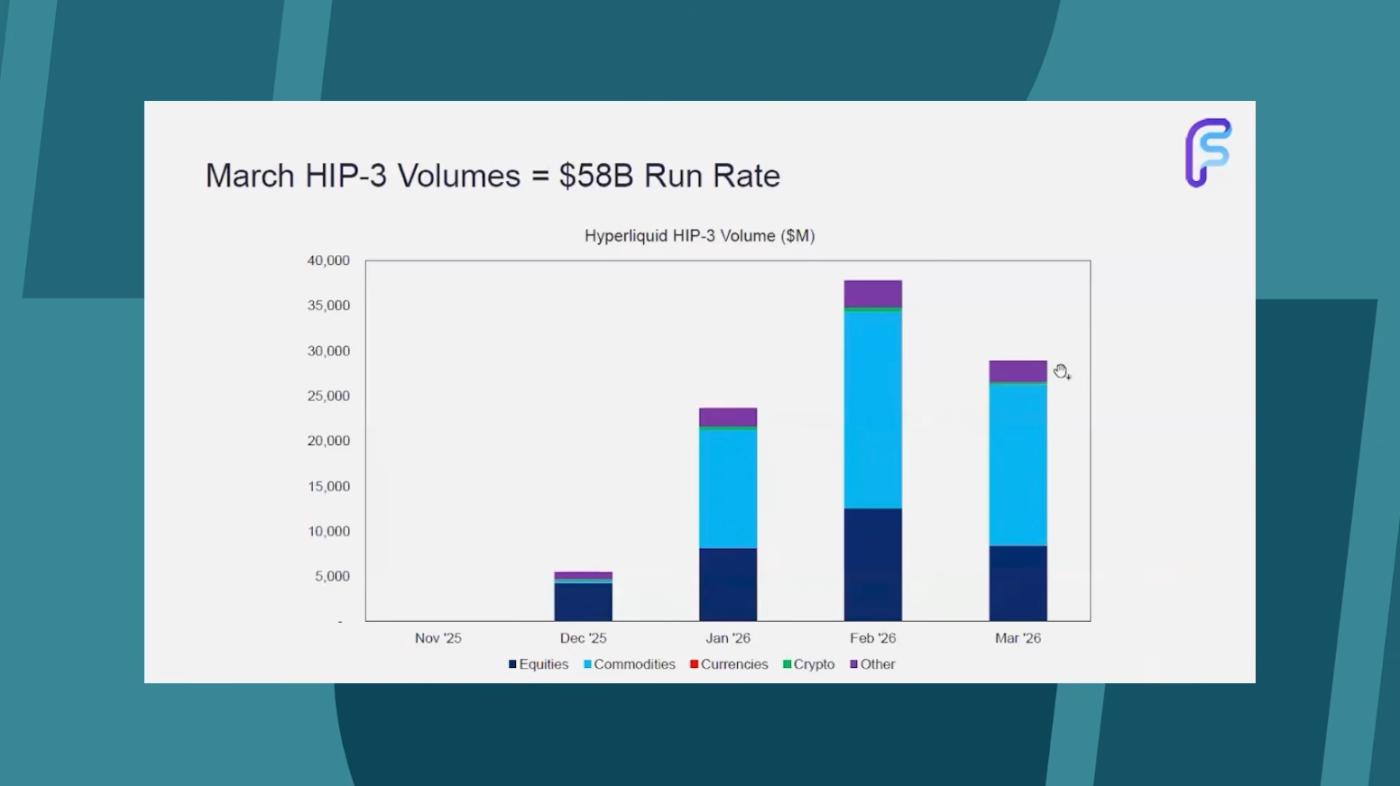

Hyperliquid recently launched their HIP-3 market, a permissionless market where anyone can create their own. These markets primarily consist of tradable assets, such as perpetual futures contracts tracking commodities and stocks.

I also shared a chart: in the first 15 days of March, trading volume in the HIP-3 market reached $28 billion, mainly due to recent cross-asset price volatility and global macroeconomic turmoil. We noticed that many investors traded crude oil contracts over the weekend, while precious metals were also a hot trading area before that.

These trading activities not only increased Hyperliquid's revenue, but more importantly, these revenues came from external assets outside the cryptocurrency ecosystem. This is why we observed a significant decrease in the correlation between HYPE and Bitcoin. Traditionally, the correlation between crypto assets is very high, usually close to 1. However, since the beginning of this year (up to last week), the 90-day correlation between HYPE and Bitcoin is only around 0.4. This low correlation makes HYPE an important addition to building a crypto asset portfolio.

The price of HYPE has risen considerably in the past few weeks, and some adjustment may be needed in the short term to digest the gains. However, I remain confident in the long-term prospects of the Hyperliquid protocol.

Cryptocurrency regulation, the Clarity Act, and market structure

Zack Guzman: If we want to clear the current fear in the market, what factors besides the smooth passage of the Clarity Act are you focusing on? Or, what final catalyst do you think is needed for you, like Tom and other crypto bulls, to regain confidence that the crypto market can return to its former glory?

Sean Farrell:

I'd like to start by addressing the issue of regulation. At the beginning of the year, I was relatively optimistic about the prospects of the Clarity Act, believing it was likely to pass. This optimism was based primarily on two reasons: first, it was a midterm election year, and the Republican Party's position in Congress was not secure; second, organizations like Fairshake had just raised nearly $200 million in "war chests" to support related legislative work, so I believed the risk-benefit analysis at the time favored the Clarity Act's passage.

However, as time went on, the situation became more complicated. From what I understand within the industry, lobbying groups in the banking sector are strongly opposing the bill, and the controversy surrounding stablecoin yields has lasted far longer than expected; this "battle" is protracted more than many anticipated. Meanwhile, Congress faces many other higher-priority issues, further clouding the future of the Clarity Act.

Nevertheless, I believe the market is underestimating the fact that the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) will continue to push forward with rulemaking regardless. Therefore, I anticipate some positive changes in market structure in the second half of this year, which will have a beneficial effect. Of course, I still hope the Clarity Act will ultimately be passed, which would be a significant milestone.

Regarding the conditions you mentioned for "realigning" or changing my perspective, I believe that if there is some kind of "capitulation" in the broader risk market, it would give me more confidence in buying at low prices.

Another possible scenario is that geopolitical risk premiums begin to decline, market expectations for interest rates gradually stabilize, and the credit market returns to normal. Meanwhile, if the market enters what I call a trending market, exhibiting a clearer direction, I would be more willing to take action.

Specifically, if market prices can break through key moving averages again, institutional funds begin to flow back in, CME open interest increases, and basis widens, I will be more confident in increasing my investment.

Private credit stress and broader market risks

Zack Guzman: How much of your market assessment is based on macroeconomic risks? If we look at the current market risks from a broader perspective, especially the pressures in the credit markets, it's worth noting that my professional experience tells me that what truly drives a market downturn is often not the widely discussed risks. So, could these credit market pressures also exert additional pressure on the crypto market?

Sean Farrell:

I believe there will definitely be some impact; sometimes people can quickly forget important things. For example, everyone is currently focused on geopolitical events, such as the Iran-Iraq War and its impact on commodity prices, which is certainly important. But in reality , even before these events occurred, we had already seen many significant problems in the broader markets, and one of the main driving factors was the deterioration of the private credit market.

Recently, we've seen many private credit funds forced to redeem their holdings and also downgrade the valuations of their assets. Of course, I don't fully understand the overall credit quality of these private credit assets, as there can be significant differences between them, but when you see these negative news stories repeatedly, you have to be wary of this trend.

From a market perspective, the share prices of many alternative asset management companies have suffered significant losses . Simultaneously, we've observed a gradual widening of credit spreads (a key indicator of corporate financing costs), consistent with the downward trend in alternative asset management company share prices. While the absolute level of spreads remains low, the speed of this widening is more concerning and is not optimistic. Waiting until credit spreads surge across the board before taking action will be too late.

This situation may indeed have some impact on the market, but I don't believe it will evolve into a systemic risk. Some of the problems may be related to technology companies affected by AI . For example, many private equity investments target software companies, which may face market share losses due to the rapid development of AI. Furthermore, AI may reduce the terminal value of these companies, further impacting their valuations.

So this is indeed an issue I'm closely monitoring. I'm still trying to figure out how it might erupt and at what specific time, but in any case, it's definitely a direction worth paying attention to.

Why he didn't change his target price for Bitcoin

Zack Guzman: Every time you come on the show, we talk about your long-term price predictions. For example, I remember you gave a Bitcoin price target of $115,000 at the beginning of the year. When you look back at those predictions from January, do you feel the need to adjust them? Or, as we get closer to the end of 2026, will you reassess those targets?

Sean Farrell:

It's only mid-March now, and I don't think it's wise to adjust these long-term forecasts at this time. I still believe we will benefit from some of the favorable factors we've previously highlighted, which are likely to materialize in the second half of the year, so I currently have no plans to adjust my year-end target price.

Currently, my focus remains on managing short-term market volatility and increasing investment when a clearer trend reversal emerges in the market.

Federal Reserve Meeting: What should crypto investors pay attention to?

Zack Guzman: What will you be particularly focused on at the upcoming Federal Reserve meeting this Wednesday? How will you interpret the Fed's statement? What do you think crypto investors should pay close attention to?

I recall you mentioning in your recent report that the market seemed to have already priced in some dovish expectations, anticipating that Fed Chair Powell might signal some easing at the meeting. But as you noted, the situation is more like a tug-of-war: on the one hand, the weakness in the job market has raised many concerns, especially regarding potential job displacement due to AI; on the other hand, inflation risks appear to be resurfacing.

Sean Farrell:

I agree with you. Most people expect Powell to take a relatively "neutral" stance at this meeting, as he currently has no sufficient reason to be overly hawkish on policy.

Investors should pay close attention to the Federal Reserve's dot plot and summary of economic projections . These tools will reveal the Fed's latest forecasts for future inflation, economic growth, and unemployment, and may also indicate their views on the future path of interest rate cuts.

If the dot plot indicates that the Federal Reserve is postponing its rate cut expectations until 2027, this could negatively impact asset prices. Such an adjustment could shift market attention to other risk factors and even further amplify the existing war risk premium in the market. Of course, the final market reaction will depend on the specific content released by the Federal Reserve.