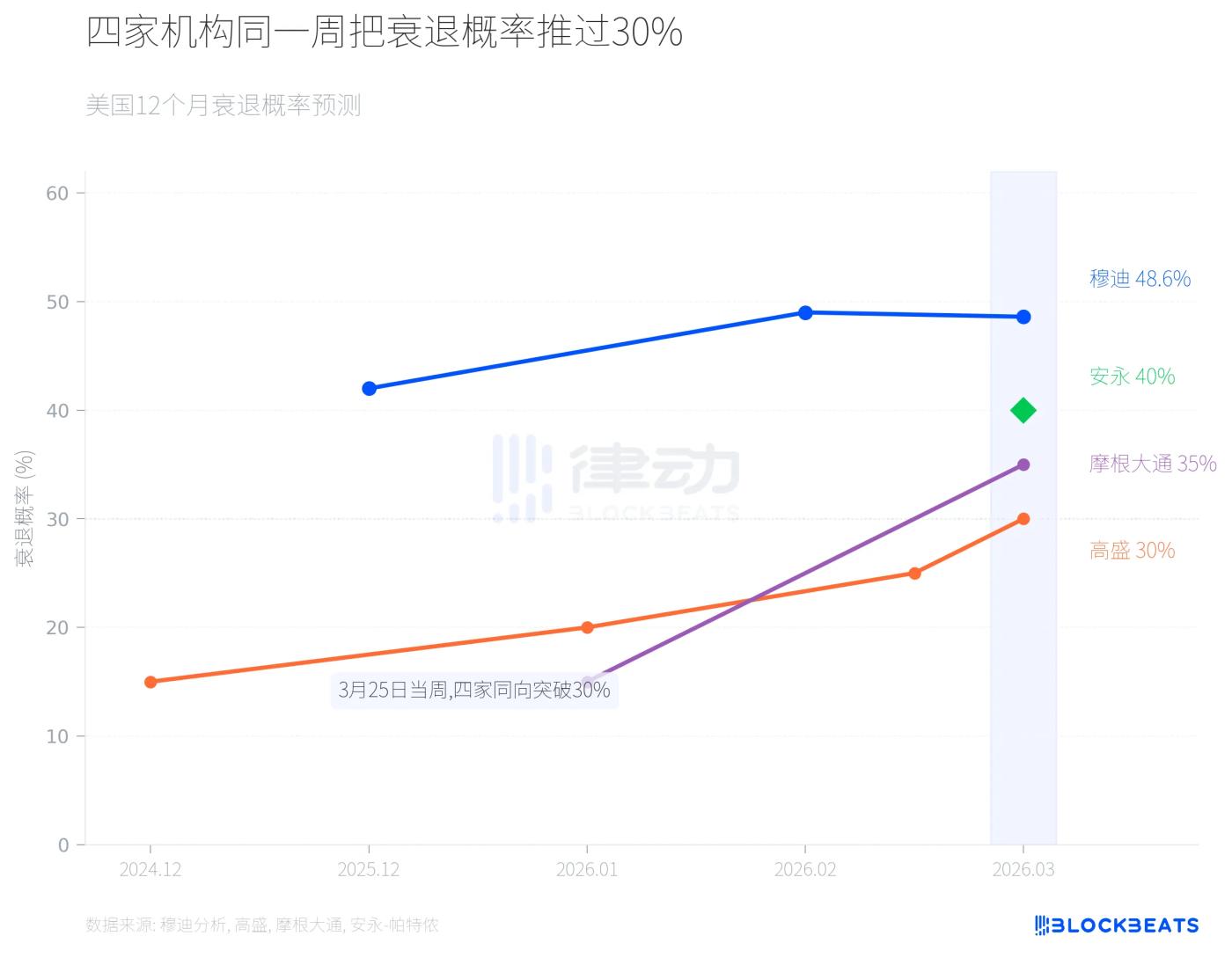

In the week of March 25th, four institutions using different methodologies—Moody's Analytics, Goldman Sachs, JPMorgan Chase, and EY-Parthenon—unanimously raised their probability of a recession in the U.S. over the next 12 months to over 30%. Moody's gave 48.6%, EY-Parthenon 40%, JPMorgan Chase 35%, and Goldman Sachs 30%.

This matter itself is more important than any specific number.

All four lines rose simultaneously

Moody's Analytics' machine learning model has given the highest reading yet. According to a Fortune report on March 25, Moody's chief economist Mark Zandi stated that this figure was only 15% in December 2024, rising to 42% by the end of 2025, jumping to 49% in February of this year, and the latest calculation shows 48.6%. Zandi predicts that the next round of data will likely push this figure above 50%. The baseline recession probability is typically between 15% and 20%, meaning the current reading is nearly three times the normal level.

Goldman Sachs' path has been equally steep. According to Fortune, Goldman Sachs' December 2024 forecast was 15%, slightly revised to 20% in January, raised to 25% on March 12, and reached 30% by March 25. This pace of revising its forecast every two weeks is rare in Goldman Sachs' historical forecasts. Goldman Sachs also raised its PCE inflation forecast by 0.2 percentage points to 3.1%, lowered its full-year GDP growth forecast to 2.1%, and postponed its first rate cut expectation from June to September.

JPMorgan Global Research gave a 35% target. According to a CNBC report on March 19, JPMorgan economists simultaneously lowered their year-end target price for the S&P 500 from 7500 points to 7200 points, with an extreme scenario potentially seeing it fall to 6000 points.

Ernst & Young Parthenon was the last of the four to speak out, but its 40% probability prediction came with an interesting qualifier. According to a March 24 report by World Oil, Ernst & Young Parthenon's chief economist, Gregory Daco, defined the current situation as a "multi-dimensional disturbance," arguing that the impact extends beyond crude oil supply to include refining systems, LNG infrastructure, and the fertilizer supply chain. This implies that even if oil prices fall, inflationary pressures will not subside accordingly.

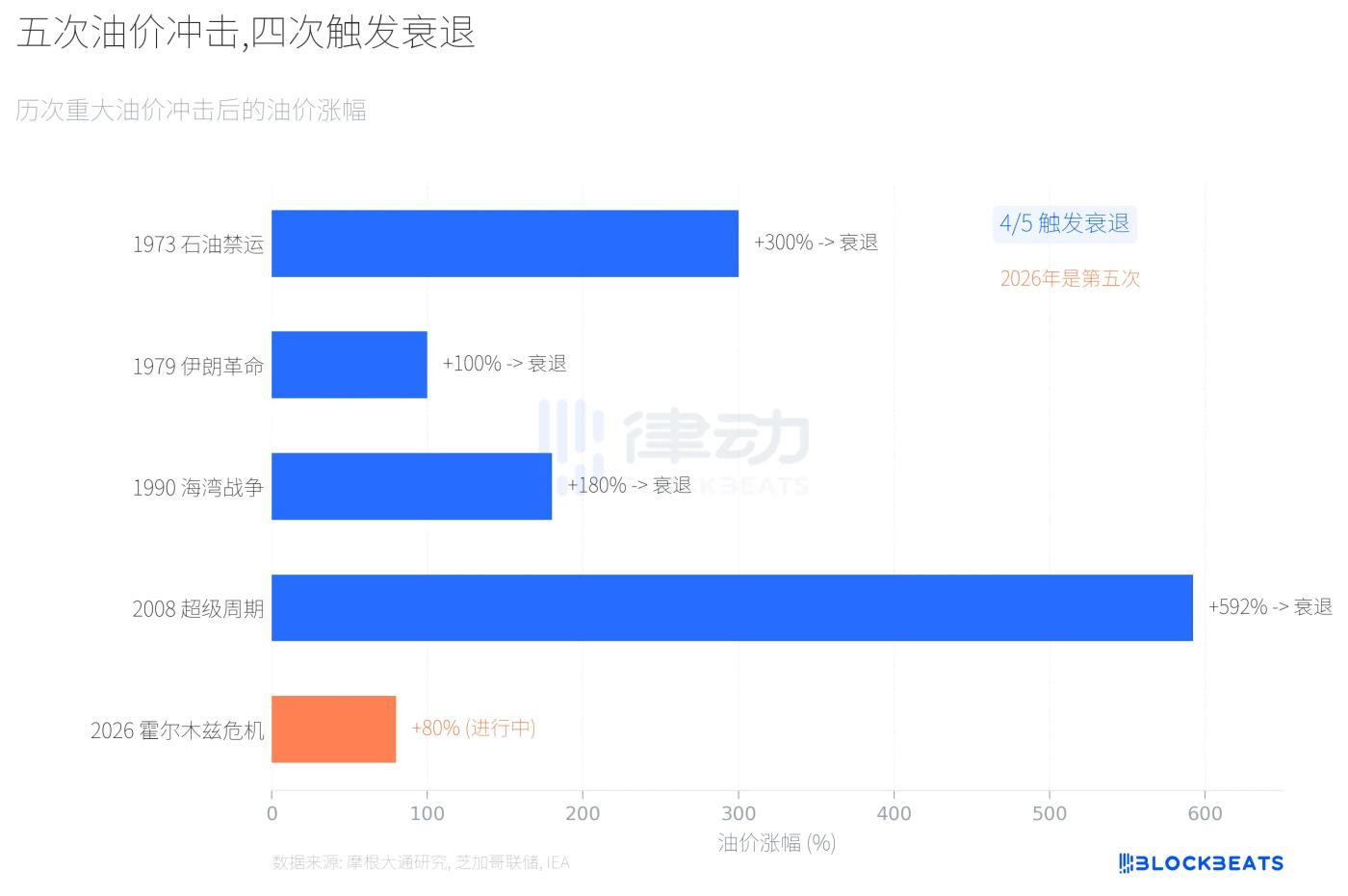

Historical success rate of oil price shocks

The core assumptions of the four institutions share a common variable: oil prices. Since the US-Israel strikes against Iran on February 28, Brent crude oil has climbed from around $70 per barrel, breaking through $100 on March 8 (the first time in four years), and briefly reaching $115 last week. It closed at $102.22 on March 25.

According to an IEA report in March, the Strait of Hormuz previously saw approximately 20 million barrels of crude oil pass through daily, accounting for about 20% of global seaborne oil trade. Following the outbreak of conflict, Gulf countries reduced their crude oil production by at least 10 million barrels per day. Zandi, in an interview with Fortune, estimated that about one-third of the world's fertilizer supply also passes through this waterway.

This level of energy shock has occurred four times in history.

According to JPMorgan Chase research, four out of the five major oil price shocks since the 1970s triggered subsequent recessions. The Yom Kippur War in 1973 caused oil prices to surge by 300%, and the US entered a recession that November. The Iranian Revolution in 1979 doubled oil prices, and a recession began the following January. The Gulf War in 1990 pushed oil prices up by 180%, with a recession starting almost simultaneously. The supercycle from 2002 to 2008 saw oil prices rise by a cumulative 592%, ultimately ending in a global financial crisis.

The 2026 Strait of Hormuz crisis is currently estimated at around 80%, the smallest of the five predicted crises. However, there is a key difference: the scale of this supply disruption will be larger than any previous one. The IEA describes it as "the largest disruption to energy supplies since the energy crisis of the 1970s."

JPMorgan economists have provided a quantitative estimate: every 10% increase in oil prices would drag down U.S. GDP by approximately 15 to 20 basis points.

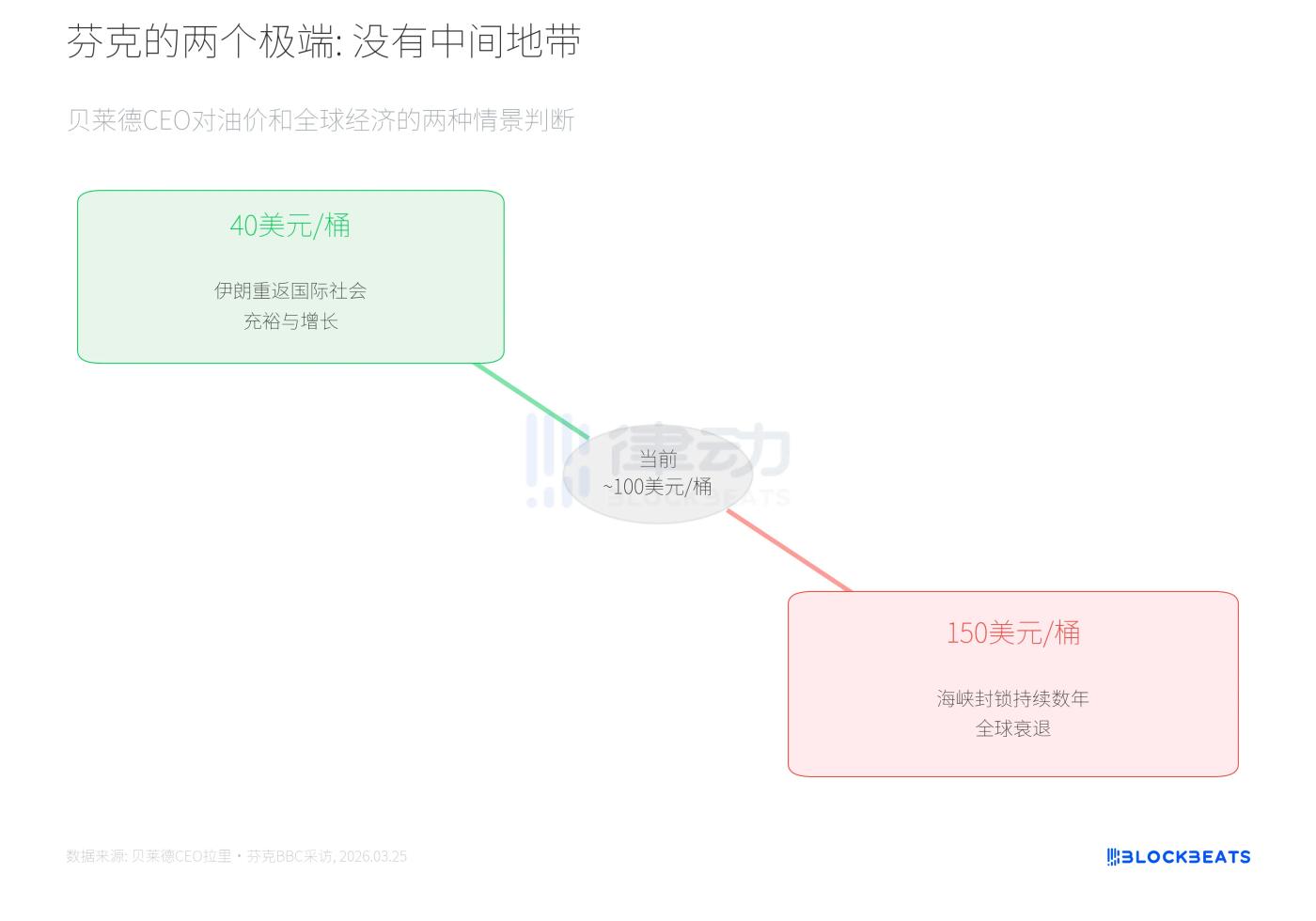

Fink's Dichotomy

On March 25, Larry Fink, CEO of BlackRock, which manages more than $10 trillion in assets, gave a more direct framework than just numbers in an interview with the BBC.

According to Fortune, Fink said, "There will be no middle ground; the outcome will inevitably be one of the two extremes."

In the first scenario, Iran is accepted by the international community and re-engages in global trade, oil supplies are restored, oil prices fall to $40 per barrel, and global growth ensues. In the second scenario, the conflict continues, the Straits of Hormuz blockade persists for several years, oil prices remain above $100 or even approach $150, and the world enters a recession. Fink specifically points out that the ripple effects of high oil prices will extend to agricultural products and fertilizers, as these are byproducts of natural gas.

However, Fink also ruled out one possibility, stating explicitly that a systemic financial crisis like that of 2008 would not occur, as the current capital adequacy ratios of financial institutions are far higher than they were back then.

Consensus itself is a variable.

Returning to the initial question, Moody's used machine learning models, Goldman Sachs used a macroeconomic forecasting framework, JPMorgan Chase tracked five-factor indicators, and EY-Parthenon approached the issue from a supply chain perspective. These four different methodologies converged on the same direction within the same week.

According to a University of Michigan survey in March, the consumer confidence index fell to 55.5, placing it in the second percentile historically. According to BLS data, U.S. nonfarm payrolls fell by 92,000 in February, the opposite of market expectations of a 60,000 increase. Leisure and hospitality jobs decreased by 27,000, healthcare by 28,000, manufacturing by 12,000, and federal government jobs by 10,000. According to BLS statistics, since the peak in October 2024, federal government employment has cumulatively shrunk by 330,000, a decrease of 11%.

In an interview, Zandi said that if oil prices average around $125 per barrel in the second quarter, "that would push us into a recession." At Brent crude's current level of around $102, that's still $23 away from that level.

The predictions from these four institutions may not be accurate. But when four institutions reach similar conclusions in the same week using different methods, the impact is more than just a probability figure. Businesses may postpone investment plans, consumers may tighten their spending, and these actions, in turn, will depress economic data, causing the next round of predicted figures to rise further.