The crypto market has grown, but the number of retail investors is decreasing. We analyzed the entry barriers in the nine Asian countries with the largest potential customer base and examined how exchanges are responding. Check it out now.

1. The market grew, but the population decreased.

There are five main reasons why Crypto Curious is not entering the market.

Regulatory uncertainty: It is unknown whether legal protection is available.

Social perception: People around us view cryptocurrency trading as “gambling.”

2. Crypto Curious Analysis of Major Asian Countries: Entry Barriers Vary by Country

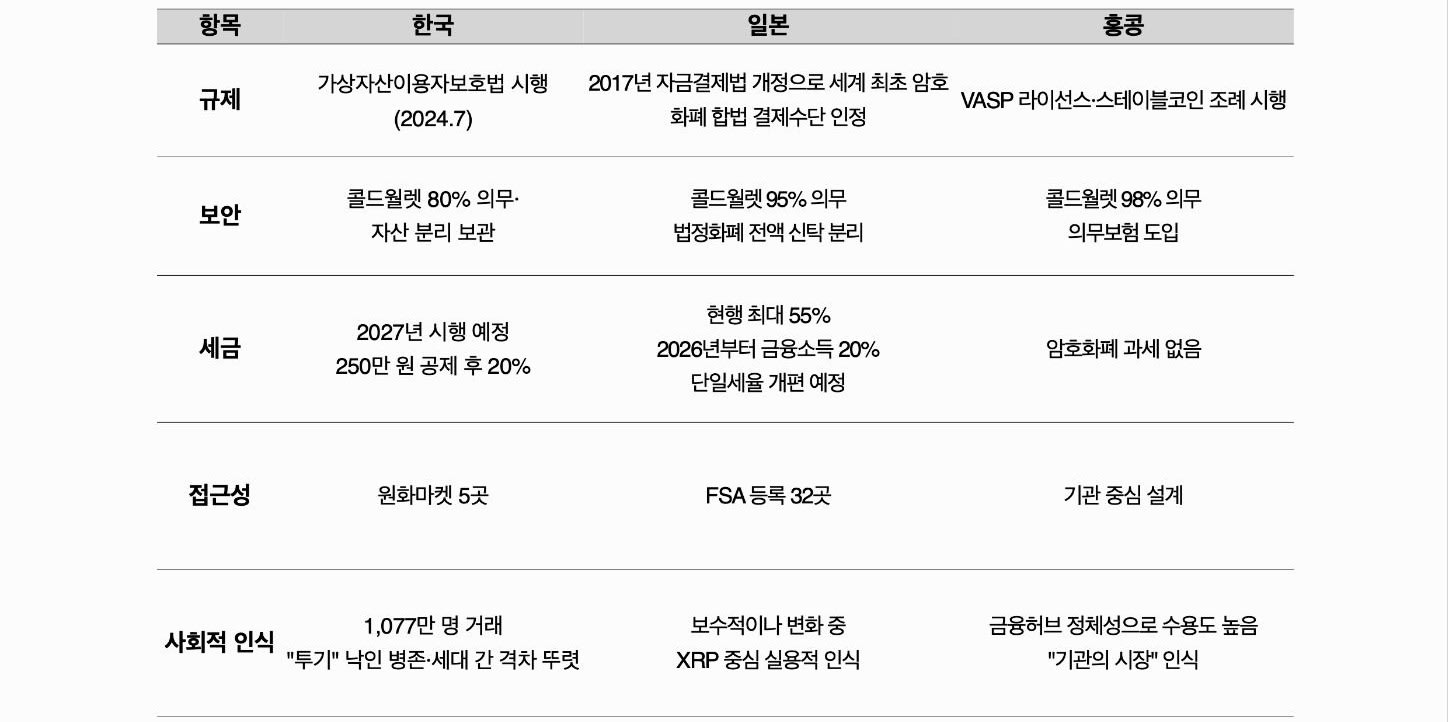

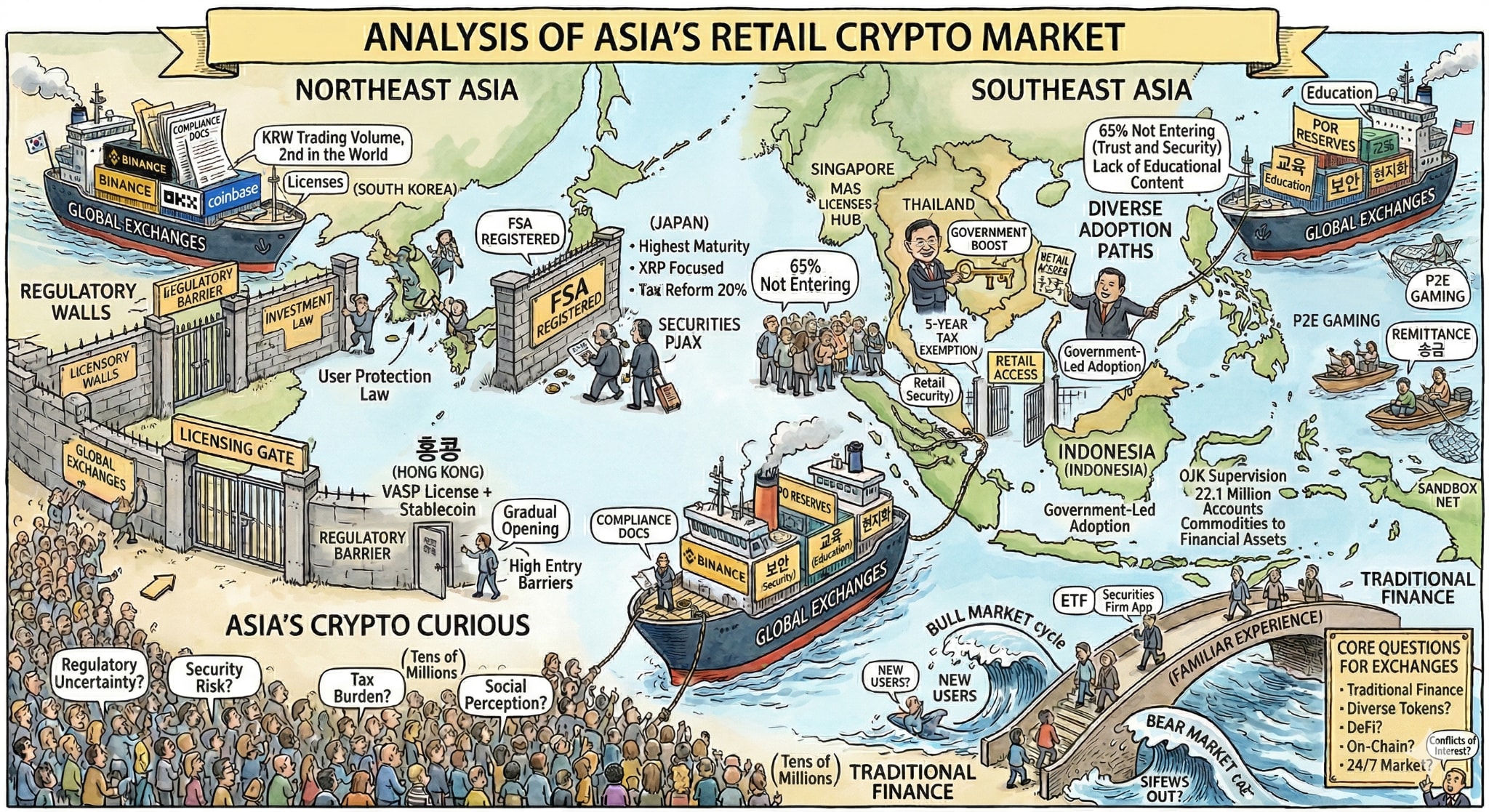

2.1. Northeast Asia: Korea, Japan, Hong Kong

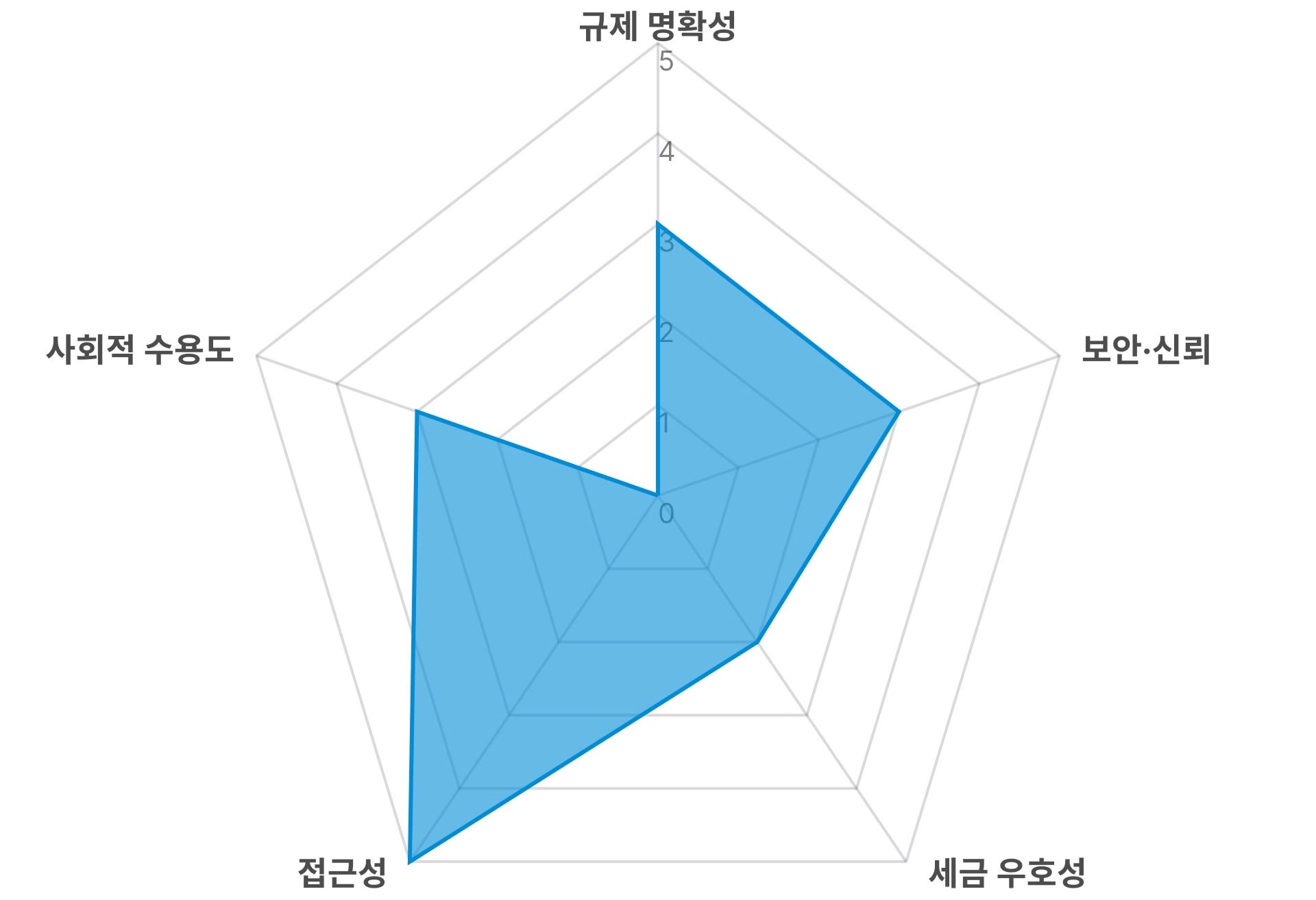

2.1.1. Korea: Second-largest trading volume in the world, but users are declining

Korea is the country with the fiat currency in Asia where cryptocurrency is traded most actively.

In the second half of 2025, the trading volume in Korean Won reached $663 billion, approaching the global USD trading volume and ranking second in the world. Furthermore, with 11.13 million tradable users—approximately 21.53% of the total population— cryptocurrency trading occurs at a high rate relative to the country's population.

As such, Korean users showed a strong willingness to trade cryptocurrencies. However, unlike before, while the number of users has increased by 11% compared to the previous period , the average daily trading volume and won deposits are decreasing . This is because the stock market, which offers better returns, is emerging as a better alternative, and interest in cryptocurrencies has declined.

Furthermore, there is the issue of users migrating to overseas exchanges. Unlike in the past, users are heading to foreign exchanges to trade securities not listed on domestic exchanges and leveraged products. In addition, cryptocurrency taxation is scheduled to be implemented next year. Although there is still a possibility of abolition, if it is introduced as planned, the demand for cryptocurrency trading will gradually decrease.

However, the Korean cryptocurrency market’s trading volume, ranking second in the world, and its active investment willingness create an environment that other Asian markets cannot easily replicate. Therefore, if the issue of cryptocurrency tax equity is resolved and various strategies by exchanges are established, it is also a market where the transition to crypto-curious can occur most rapidly on top of the already established infrastructure.

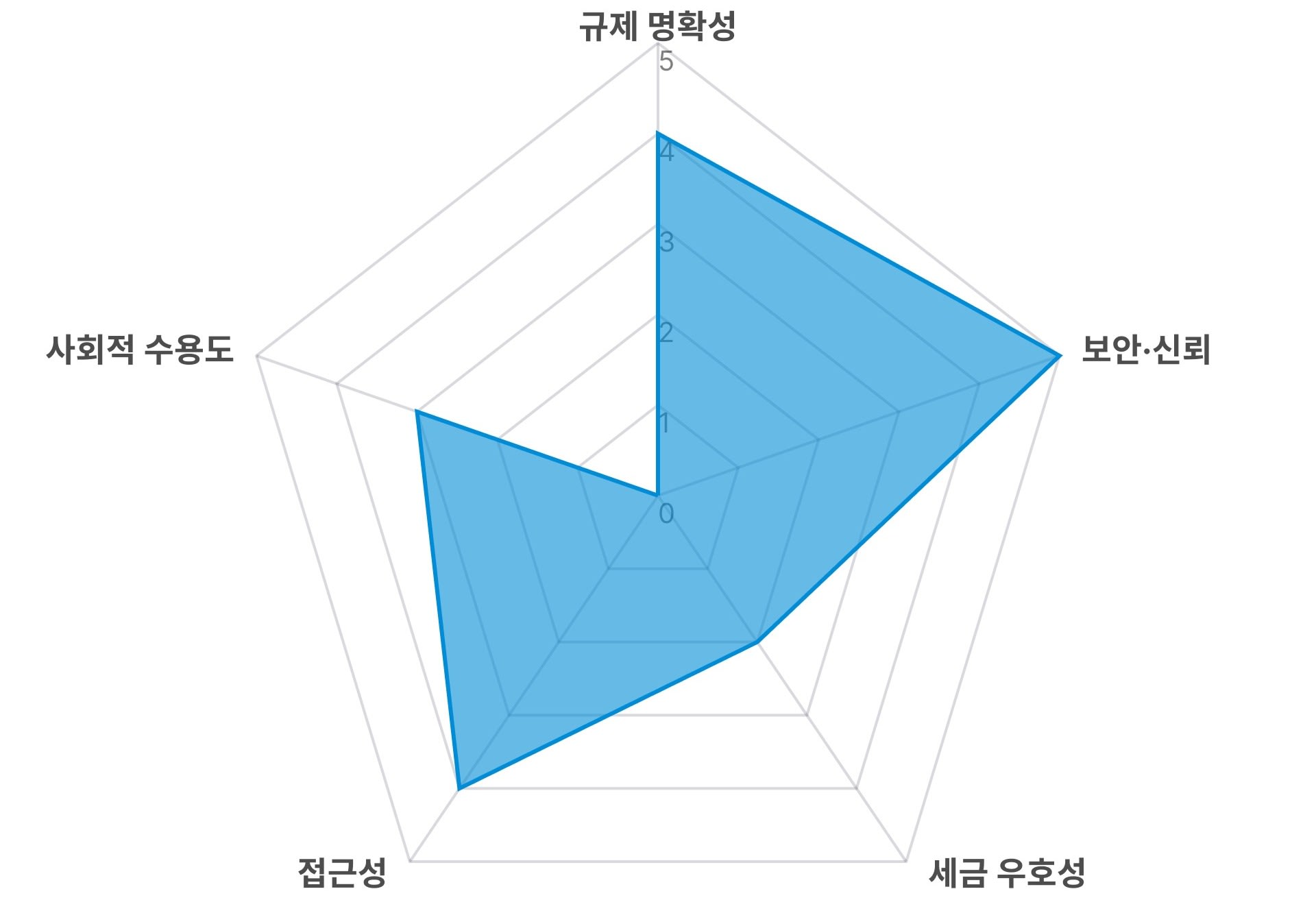

2.1.2. Japan: The safest and most expensive market

Following the loss of approximately 850,000 BTC due to the 2014 Mt. Gox hack, Japan became the first country in the world to establish exchange licenses. The lessons learned from that led to the current structure. Exchanges must store more than 95% of customer assets in cold wallets, and all customer fiat currency must be kept in separate trust accounts. There are 32 FSA-registered exchanges, 12 million cumulative accounts, and 5 trillion yen in customer deposits . This makes it the market with the strongest signal in Asia that it is "safe to enter."

However, taxes await you once you enter. Currently, cryptocurrency profits are classified as miscellaneous income and are subject to a maximum tax rate of 55%. If you earn 100 million won, the tax is 55 million won. If the same profit had been made through stocks, the tax would be approximately 20%, or 20 million won. That is a 2.7-fold difference. The safest market in Asia is imposing the highest taxes in Asia.

This contradiction is the core barrier to Japan's Crypto Curious. There is ample assurance that it is safe. However, it is as expensive as it is safe. You can enter and be protected, but there may be nothing left.

The market structure is also unique. From July 2024 to June 2025 , XRP accounted for approximately $21.7 billion of the total amount purchased on exchanges with JPY, which was 4.6 times that of BTC ($4.7 billion) . Japan is the only market globally where a single altcoin dominates Bitcoin.

This is a phenomenon created by the strategic partnership between SBI Holdings and Ripple. In Japan, XRP is accepted not as a "speculative asset" but as a "crypto asset with real-world use value." The way crypto has established itself in a society that prefers saving and is wary of speculation is fundamentally different from that in Korea.

Public social acceptance is still slow. The percentage of individual investors with investment experience who hold crypto assets is only 7.3% .

On the other hand, corporations are actively embracing cryptocurrencies. Metaplanet, a DAT company, is accumulating Bitcoin as a strategic asset under the name "Asia's Strategy," while SBI Holdings plans to list a Bitcoin+XRP dual-asset crypto ETF on the Tokyo Stock Exchange.

Amidst this situation, there is one decisive variable in Japan: two reforms scheduled to be implemented in April 2026. One is the reclassification of crypto assets as subject to the Financial Instruments and Exchange Act (FIEA). The other is changing the tax rate to a flat 20% for financial income. With the same tax rate and classification as stocks, if these two measures are implemented simultaneously, the biggest barrier to crypto-curious in Japan will disappear.

Since these changes are anticipated, there is currently no reason for Crypto Curious to enter now and accept a tax rate of up to 55%.

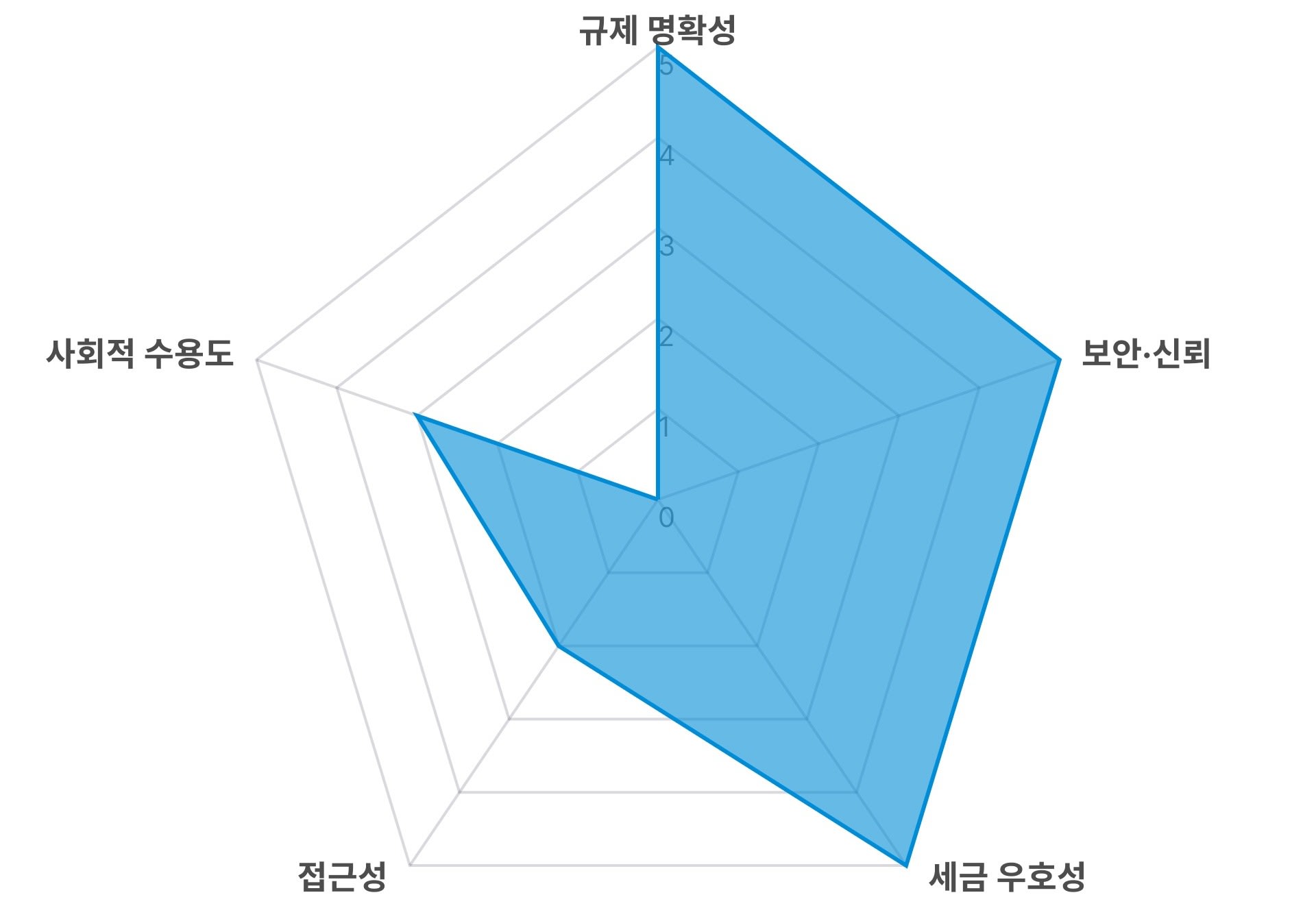

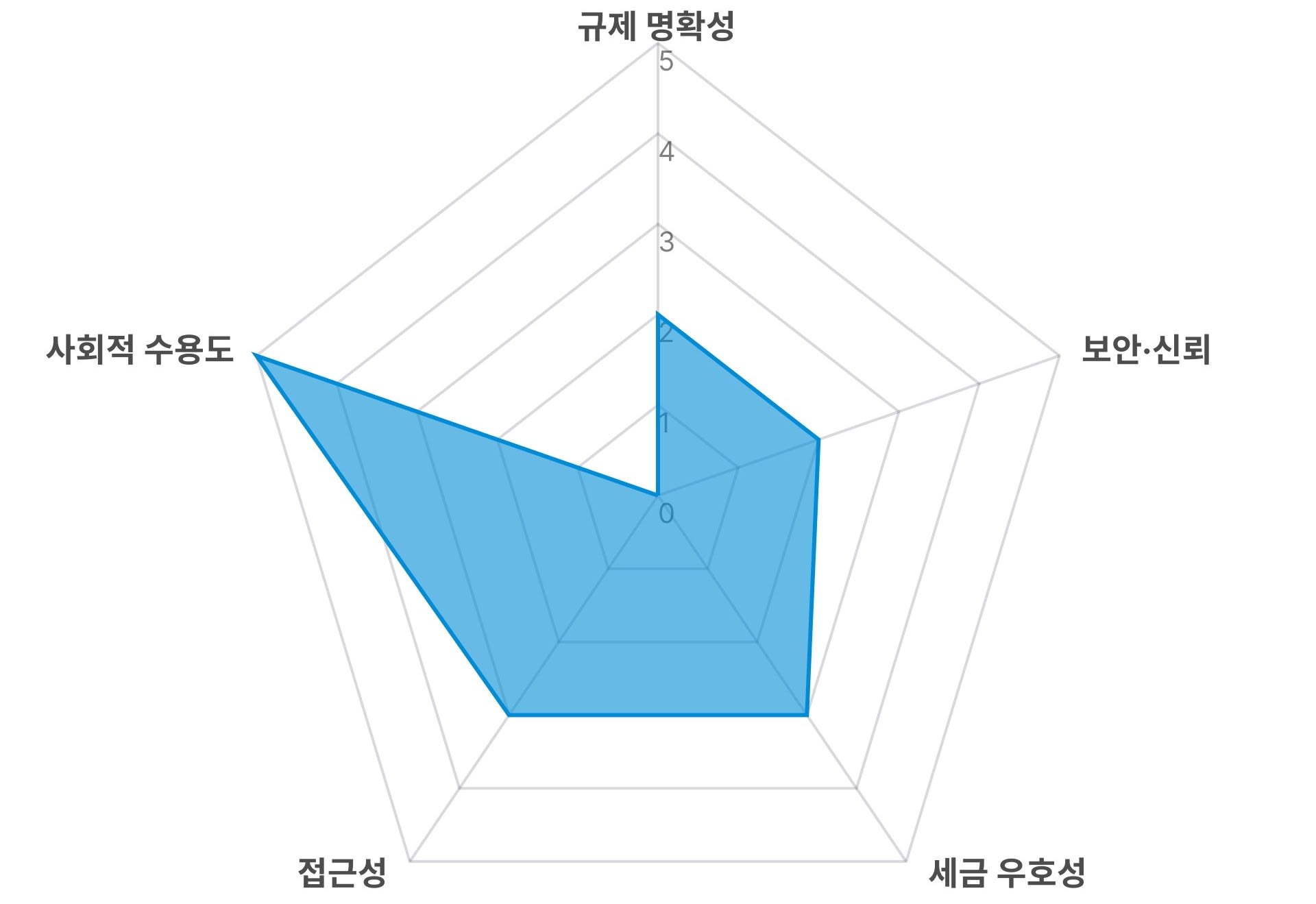

2.1.3. Hong Kong: Three barriers resolved, but accessibility remains a barrier

The SFC has been operating the VATP licensing system since 2023 and disclosed its future regulatory direction through the ASPIRe roadmap in February 2025. In August of the same year, it announced the introduction of stablecoins into the institutional framework and plans to issue the first licenses in early 2026.

Exchanges must store more than 98% of customer assets in cold wallets, and mandatory insurance and annual cybersecurity audits are required. There is also no taxation on cryptocurrency. In 2024, it even approved the first Bitcoin/Ethereum spot ETF in Asia.

Hong Kong has nearly resolved the three issues of regulation, security, and taxation. However, the remaining one is the problem: accessibility.

As of February 2026, there are 12 platforms with SFC licenses , but their services primarily target professional investors with assets exceeding 8 million HKD (approximately 1.3 billion KRW). Unlike in Korea, the structure does not allow users to purchase immediately after installing an app. While the quality of regulation is top-tier in Asia, the door to entering that regulatory framework is narrow.

Social perception also occupies a unique position. Thanks to the city's identity as a global financial hub, the view that crypto is "gambling" is weaker than in Korea or Japan. However, at the same time, there is a strong perception that it is "the domain of experts." While there is no social stigma, there is also a lack of social familiarity. It is a market with a psychological distance that makes it difficult for crypto curious individuals to feel inclined to say, "Maybe I should give it a try."

The path for change is open. The SFC has introduced a shared liquidity framework that allows licensed platforms to utilize overseas order books and has conditionally permitted staking services. Legislative notice for dealer and custody licensing schemes is planned for 2026.

To summarize Hong Kong's situation in a single sentence: while three of Crypto Curious's five barriers have been overcome, the remaining one—accessibility—is rendering the first three ineffective. No matter how safe or tax-free a place is, it is meaningless if one cannot enter. Hong Kong's challenge is to widen the doors so that more people can experience the trust that has already been built.

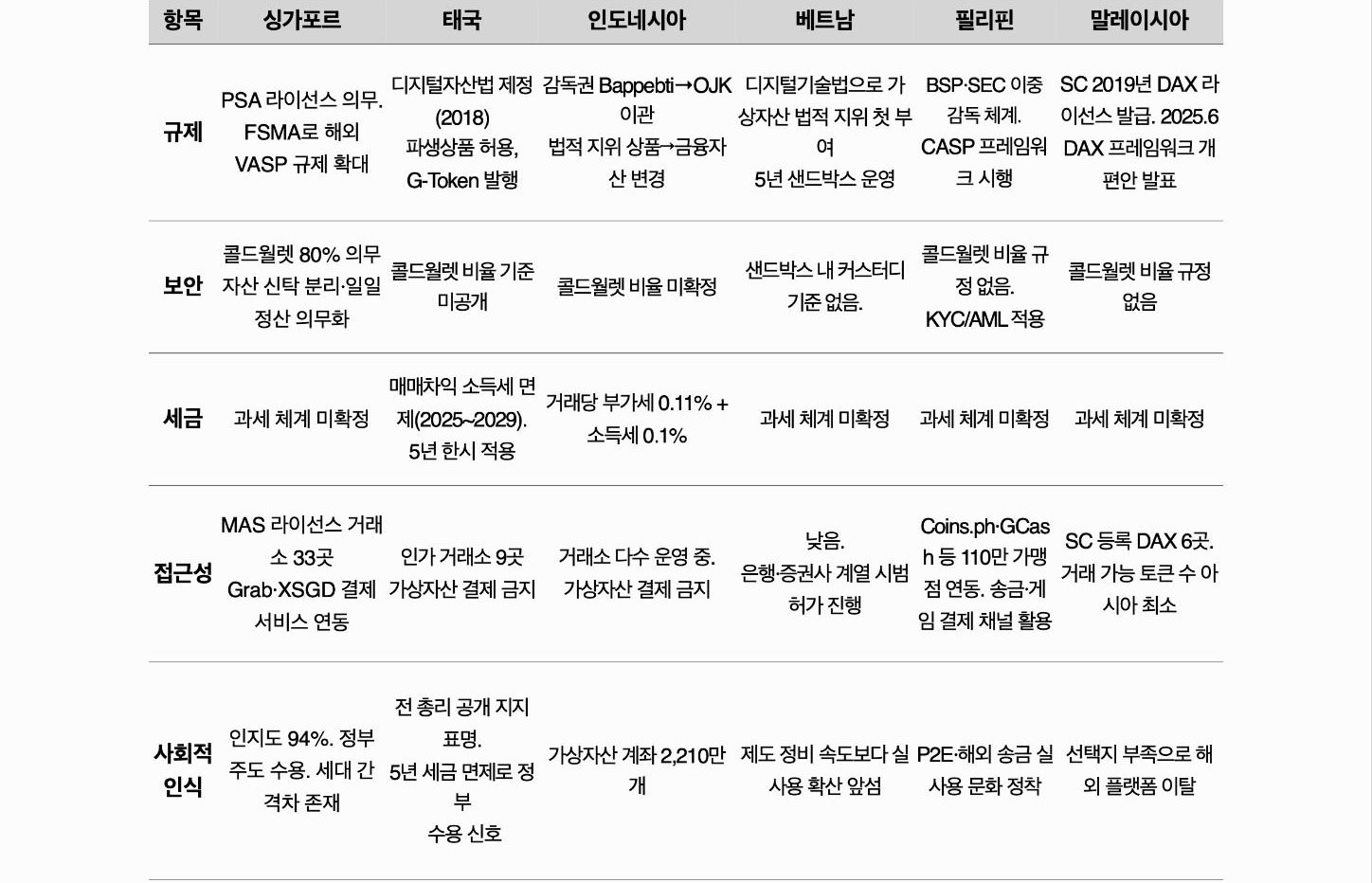

2.2. Southeast Asia: Singapore, Thailand, Indonesia, Vietnam, Philippines, Malaysia

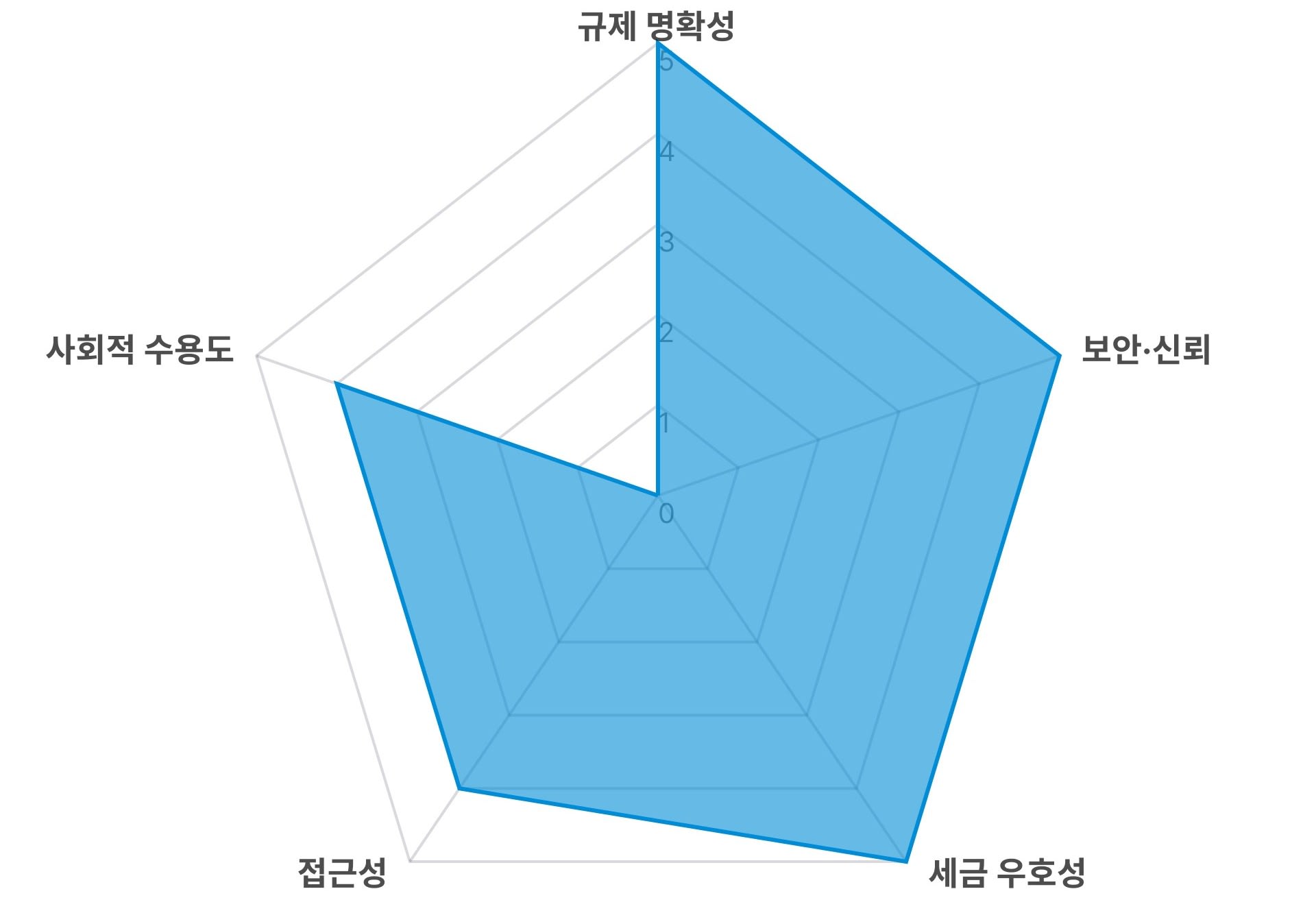

2.2.1. Singapore: All conditions met, but 65% is not coming in

The MAS operates the most consistent licensing system in Asia, and in June 2025, it mandated licensing for businesses targeting only overseas customers. Exchanges must hold customer assets in trusts, have completed FATF mutual evaluations, and there is no taxation on cryptocurrencies.

Furthermore, real-world usage is expanding. Payment integration between Grab and the stablecoin XSGD, the MAS tokenized government bond pilot project, and the three major banks' CBDC interbank lending tests. A structure is being created for crypto to expand into everyday finance within a regulatory framework.

Looking at it this way, there is no reason for Crypto Curious not to join. However, the reality told by the numbers is different. Crypto awareness is at an all-time high of 94%, but the actual ownership rate is 29% . The remaining 65% is Crypto Curious from Singapore.

These 65% are not people who are unaware. They are people who know about it, have access to it, and face no social stigma, yet choose not to do it. The biggest barrier they cited was market volatility (68%) , and the number one criterion for choosing an exchange was “ trust and security” (65%) . This is higher than fees.

Singapore serves as an interesting counterexample for Crypto Curious. Even after resolving almost all institutional barriers, 65% are not entering the market. The fact that Crypto Curious's transition is not completed by the removal of barriers alone is a point that other Asian markets should take note of.

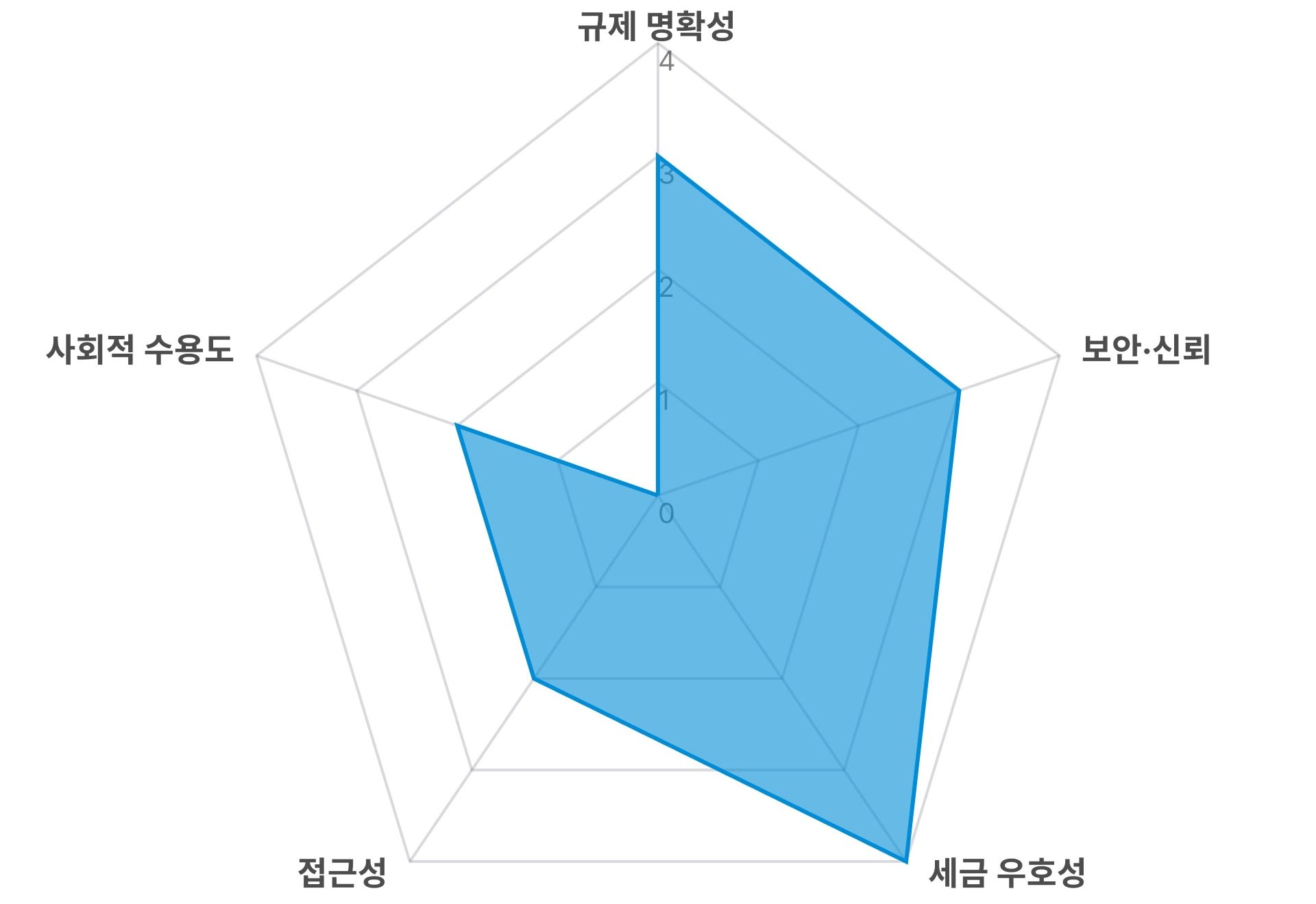

2.2.2. Thailand: Government-operated markets

Thailand has approximately 13 million crypto users, representing about 18% of the population. It established a legal framework early in Asia through the 2018 Emergency Decree on Digital Asset Business, and the SEC is currently issuing licenses to nine exchanges. The trading volume of THB-based stablecoins stands at $9.4 billion, making it the second largest in the APAC region after the KRW . It is a market that has entered a stage of active nurturing, rather than merely allowing it.

Regulatory enforcement is also operating on two fronts. In April 2025, offshore regulations on overseas platforms were implemented, blocking five sites including Bybit and OKX; simultaneously, in July, investment token services by securities firms were permitted, and public hearings on the introduction of crypto derivatives began. It is a structure that blocks illegal activities while expanding legal avenues.

The government plays a significant role in terms of social perception as well. Former Prime Minister Thaksin Shinawatra publicly emphasized the need for crypto regulation and positively evaluated the Phuket crypto payment pilot project. A perception is forming that "since the government is even exempting taxes, isn't it acceptable to proceed?" The opening of brokerage channels, allowing existing stock investors to access crypto through familiar routes, is also facilitating this transition.

However, one thing is missing: payment. Since 2022, using crypto as a payment method has been prohibited. Piloting crypto-to-Baht exchanges for foreign tourists is being conducted through the TouristDigiPay sandbox, and BOT is also running a separate sandbox for Baht-based stablecoins. However, Thais have not yet experienced making payments with crypto in their daily lives.

A key characteristic of Thailand is that the government is removing barriers to Crypto Curious from the top down. From tax exemptions and the issuance of G-Tokens to opening up institutional funding and introducing derivatives, such active government signals are rare in Asia. The remaining challenge is the transition from an "asset to be bought and sold" to a "usable asset." The lifting of the payment ban could mark the next turning point for Crypto Curious in Thailand.

2.2.3. Indonesia: From Commodities to Financial Assets

However, Indonesia's potential lies in its large population. Among its 280 million population projected for 2025 , the percentage of crypto account holders was still in the single digits . The remainder represents the potential crypto-curious population of this market. The transfer to the OJK is the strongest institutional signal to them that cryptocurrencies have been "recognized as financial products." For this signal to lead to actual conversion, the transition period must conclude smoothly.

The next chapter of the 280 million market depends on whether the OJK system is established.

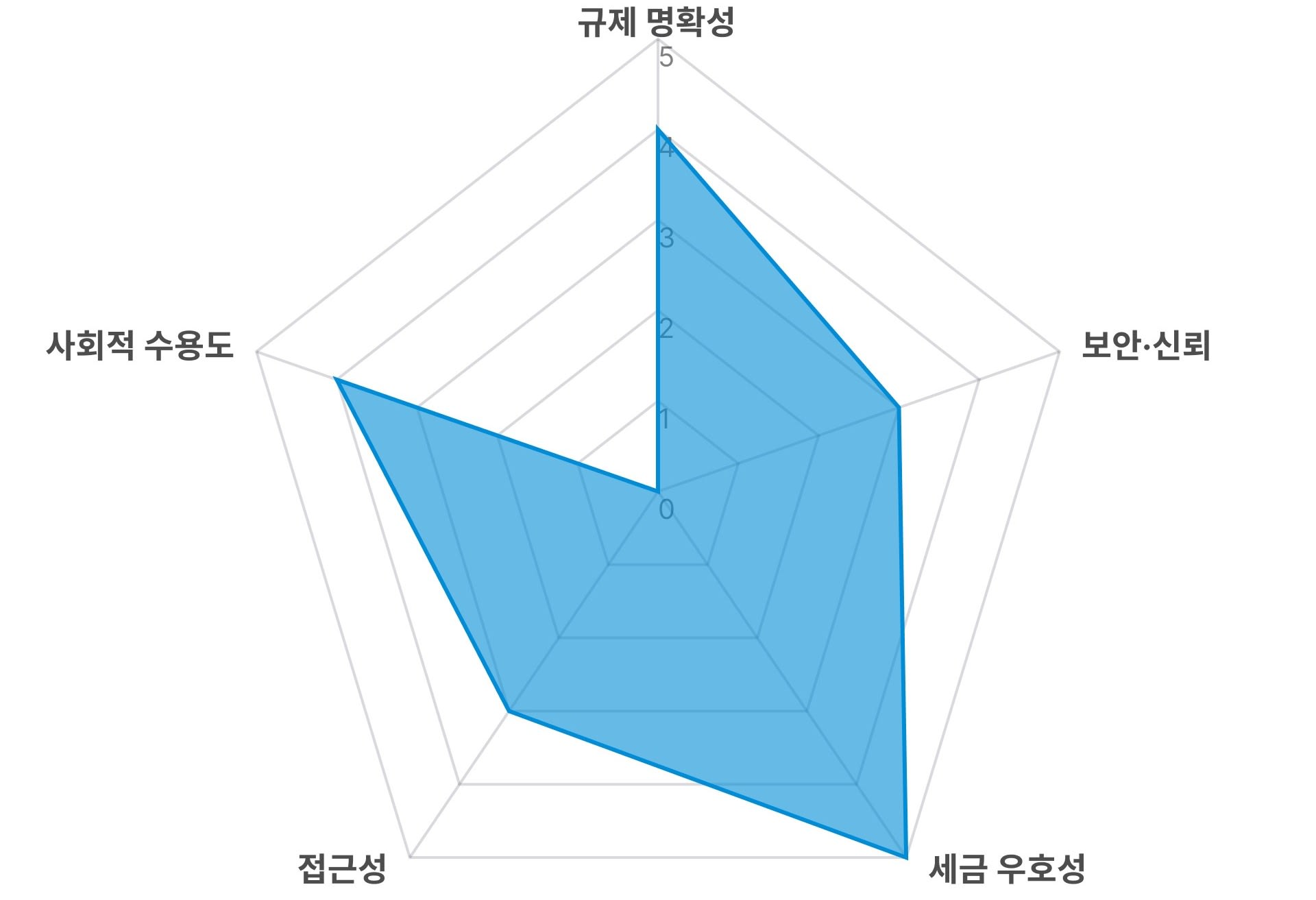

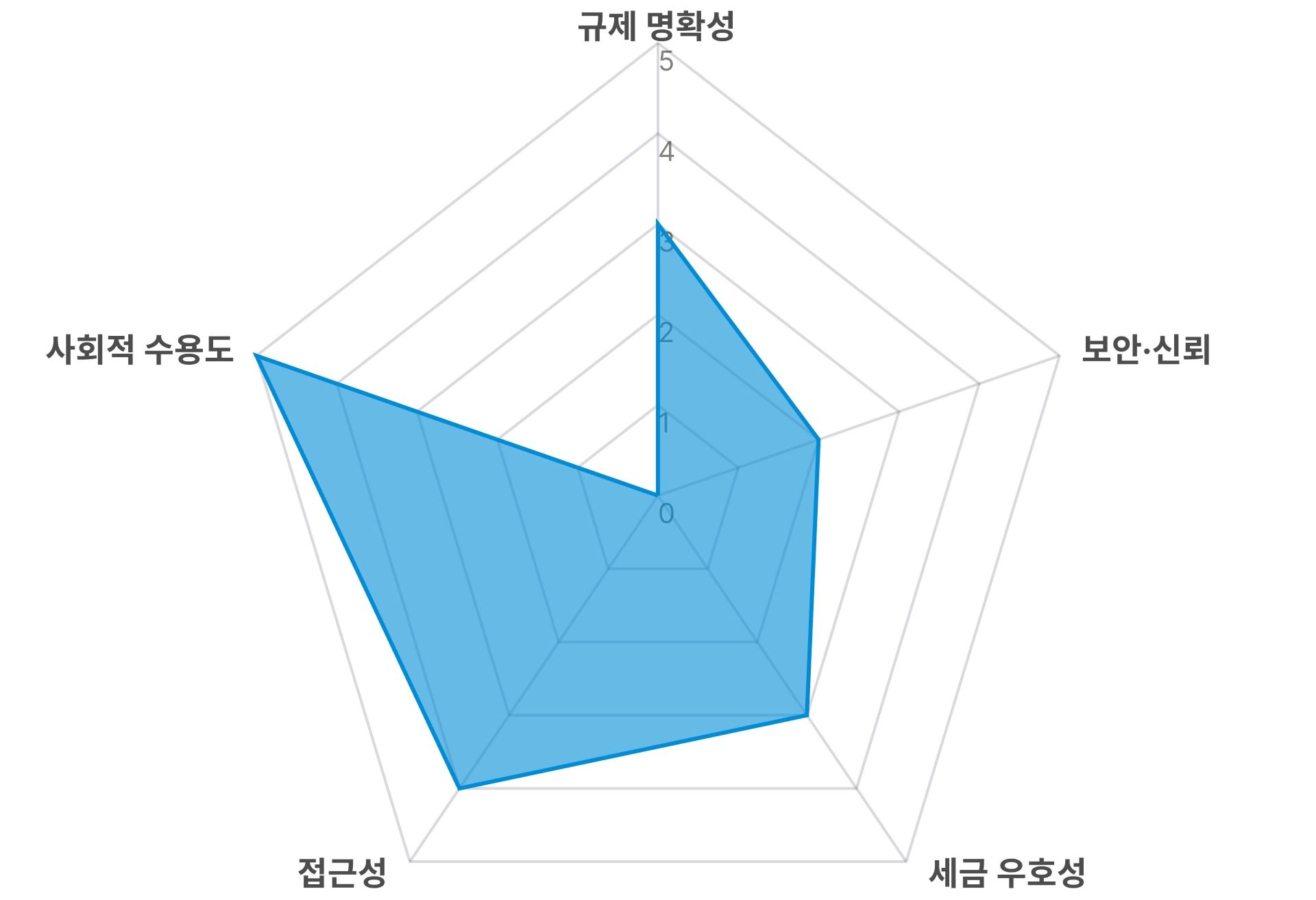

2.2.4. Vietnam: A market where people enter first, and systems follow.

Therefore, the government enabled ownership, transfer, inheritance, and legal protection of digital assets by having the National Assembly pass the Digital Technology Industry Act in June, officially recognizing them as property under civil law. Furthermore, in September 2025, it additionally introduced a five-year (2025–2030) pilot program for the crypto asset market. It is attempting to transition to a comprehensive framework all at once after a long hiatus.

However, the system is still in its early stages. Investor protection mechanisms are applied restrictively only within the sandbox, and detailed regulations regarding exchange security standards and asset separation obligations are still being refined. Escaping the FATF Grey List is also a challenge. Being on the Grey List imposes restrictions on international partnerships.

Accessibility is changing rapidly. As of early 2026, a pilot licensing process for approximately five exchanges is underway under the leadership of the Ministry of Finance . Bank-affiliated entities such as Techcombank (TCEX), VP Bank, and LP Bank, as well as securities firm-affiliated entities like VIX Securities (VIXEX), are taking the lead. With a minimum capital requirement set at $400 million, creating high barriers to entry, the financial stability of licensed operators is guaranteed.

While overseas platforms such as Binance have dominated the market so far, it is highly likely to be reorganized around locally licensed exchanges. A pathway for institutional entry is opening for the first time in a market that has already achieved large-scale adoption outside the regulatory sphere.

Vietnam's pentagon represents an extreme imbalance where social acceptance is overwhelmingly high and the rest are low. However, the direction of this imbalance is important. It is not a market where regulations must be created because acceptance is low, but rather a market where regulations must catch up because acceptance is already high. Once the sandbox operates stably and detailed regulations are established, the fastest transition to institutionalization can occur on the already formed foundation.

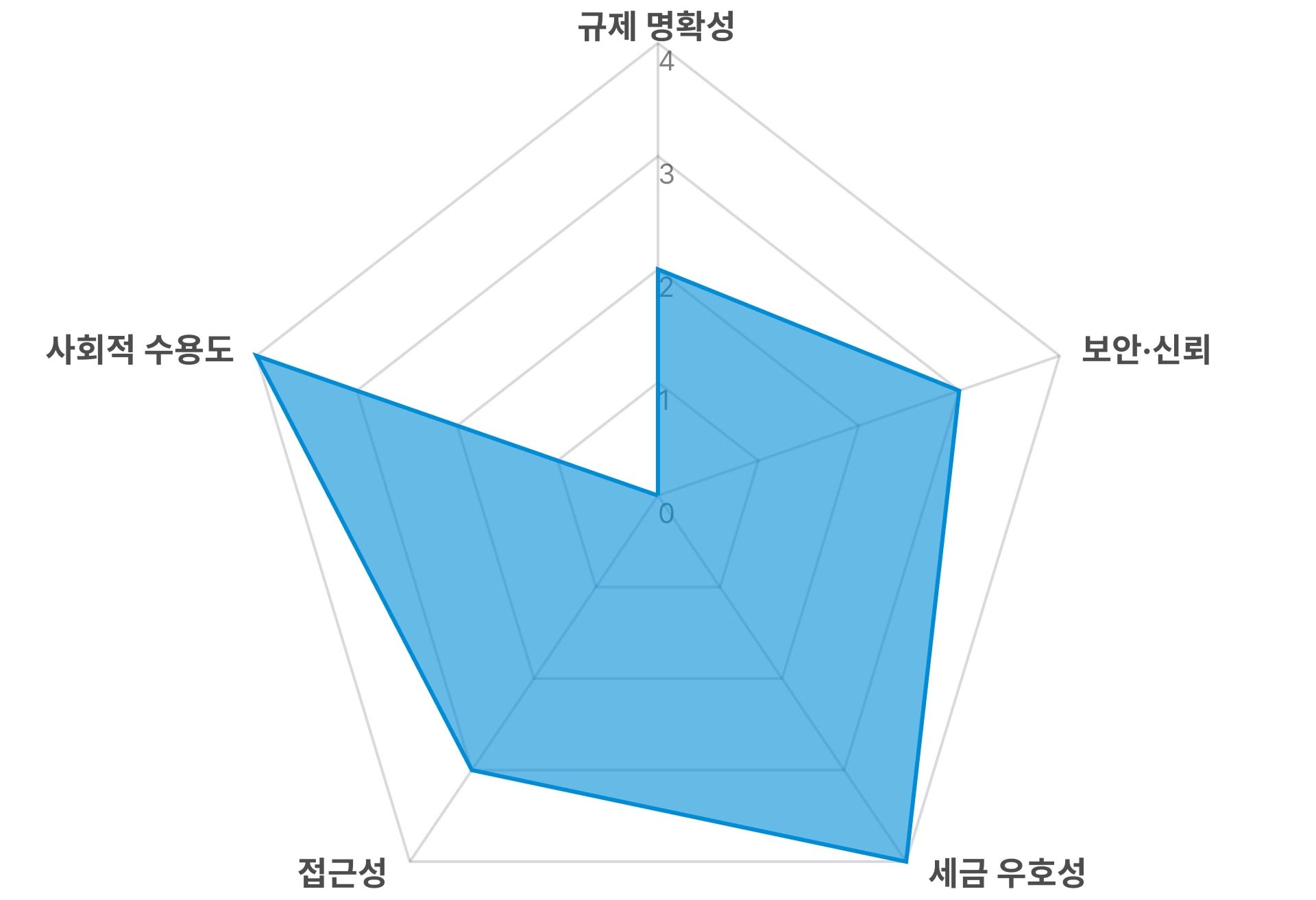

2.2.5. Philippines: A Crypto Market Built on Lifestyle, Not Investment

Social acceptance is already sufficient. The problem lies in the institutional protection above it. BSPs have frozen the issuance of new VASP licenses since September 2022. Although this was extended further in September 2025, there are only nine VASPs . The SEC implemented the CASP framework in July 2025, introducing minimum capital requirements, asset separation, and marketing regulations, but it is still in the early stages.

Security risks are the most pronounced weakness of this market. Although the SEC is taking measures to remove unregistered platforms from app stores, phishing scams via social media continue to recur. In a structure where actual usage replaces trust, that trust can collapse with a single incident if institutional protection does not follow.

Positive changes are also underway. The Philippines has been removed from the FATF Grey List . UnionBank and GoTyme Bank have obtained licenses under moratorium exceptions and are offering crypto trading on their banking apps. A bill for a strategic Bitcoin reserve has even been introduced in the House of Representatives. Political legitimacy is also being secured as President Marcos Jr. publicly supports digital innovation.

The Philippines' pentagon is similar to Vietnam's in that it is characterized by high social acceptance and low regulation and security. However, their natures differ. Vietnam is in the process of establishing new systems where there were previously no regulations, whereas the Philippines has locked the doors to existing systems. Once the VASP moratorium is lifted and the CASP framework takes root, it could become a structure where institutional trust builds upon the already established foundation of real-world use.

2.2.6. Malaysia: Regulations exist, but there are no options

Malaysia is a rare case where the market fails to grow despite having a regulatory framework.

The problem is that there is too little that can be done within that framework. There are only six DAX exchanges registered with the SC, and the number of tradable tokens is the most limited in Asia. DeFi and derivatives have not been incorporated into the institutional framework. Although the total trading value of DAX in 2024 was RM 13.9 billion (approximately $3.1 billion), a 2.6-fold increase from the previous year , the absolute scale is small compared to Thailand or Indonesia.

When options are limited, people move elsewhere. According to the SC, 996 complaints regarding unregistered DAX have been received since 2019. This means that investors seeking a wider variety of tokens and products are migrating to unregistered overseas platforms. While regulations provide protection, they simultaneously narrow market choices, leading to a shift toward unregulated areas.

SC also recognized this issue and announced a plan to revamp the DAX framework in June 2025. It is simultaneously pursuing the introduction of a liberalized listing framework that shortens the new token listing process, along with strengthening capital adequacy requirements and asset separation. Furthermore, with the Prime Minister's Office approving the establishment of the Digital Assets and AI Advisory Committee, the initiative has begun to move not only in terms of regulation but also at the level of industrial strategy.

For Malaysia's Crypto Curious, this market is a place where “it is possible, but there is not enough reason to do so.” Regulations protect the market, but at the same time, they are acting as a ceiling on growth. The next question for Malaysia is whether the overhaul of the DAX framework can raise this ceiling.

3. How to strategize for Crypto Curious on exchanges

What we need to look at now is “how global crypto exchanges are trying to enter different markets.”

3.1. Securing a License: Starting with the Qualification to Exist in the Market

Accordingly, the response strategies of global exchanges are broadly divided into two categories.

At the same time, exchanges that fill the void in Asia are the first to ride the region's growth.

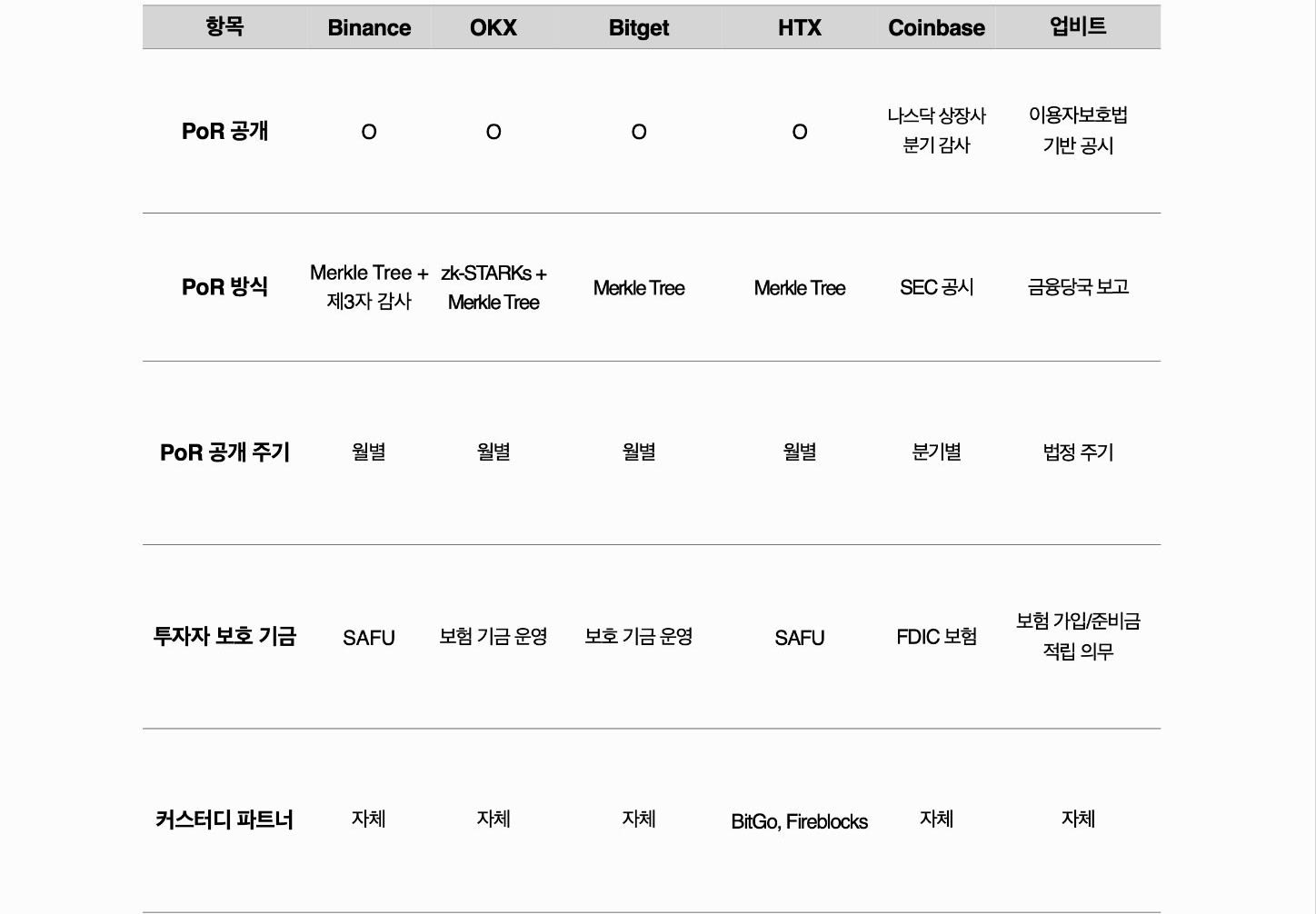

3.2. Transparency and Security: Can I Entrust My Money?

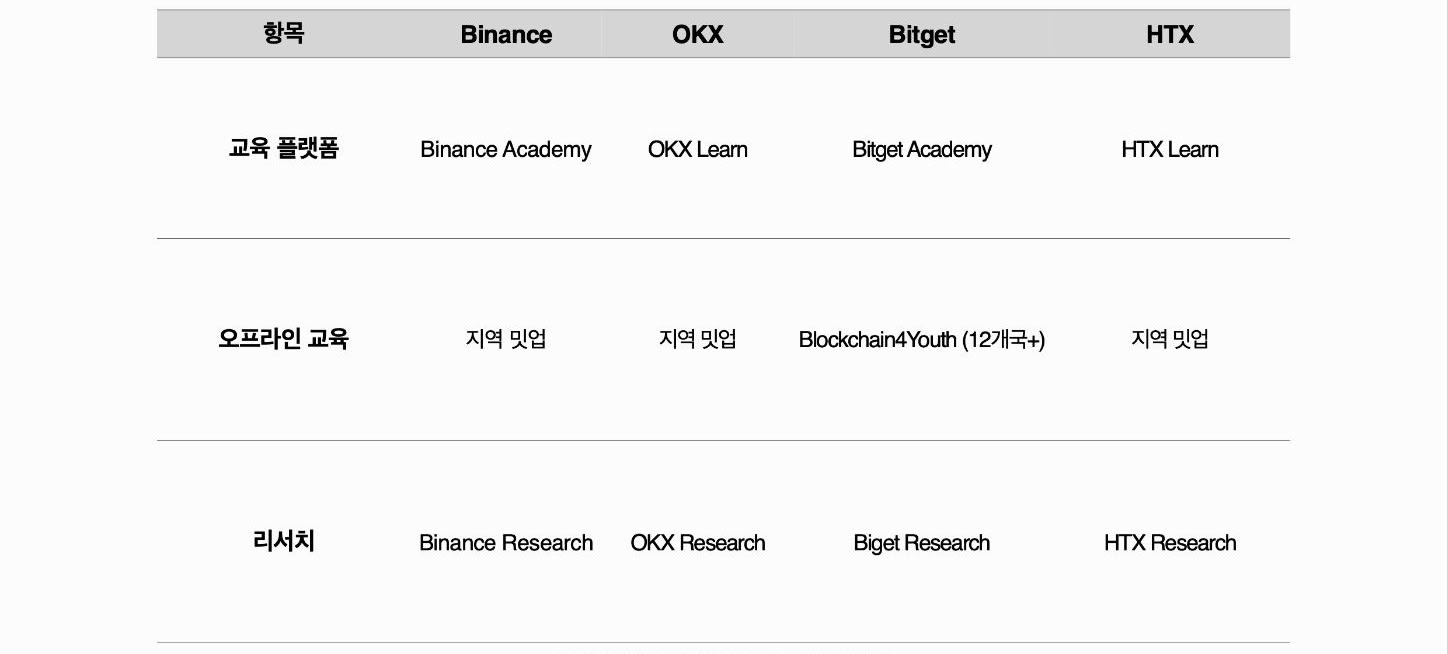

3.3. Education and Localization: Approaching with Local Languages and Currency

4. You must prepare while waiting for a bull market.

Disclaimer

Terms of Usage

Tiger Research supports the fair use of reports. This is a principle that allows for broad use of content cited for public interest purposes, provided that its commercial value is not affected. Under fair use rules, reports may be used without prior permission; however, when citing Tiger Research reports, you must 1) clearly identify 'Tiger Research' as the source and 2) include a logo ( Black/White ) that complies with Tiger Research's brand guidelines. Separate consultation is required if the material is restructured for publication. Use without prior permission may result in legal action.