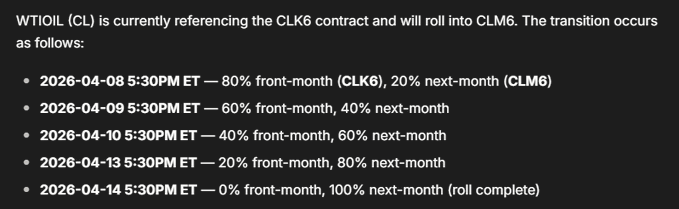

Shout out to @papipnl for flagging one major issue with this that really puts a wrench in the whole thing. @tradexyz transitions the oracle price from the current CME to the subsequent CME price over a 7-day period, starting the 8th of this month. Currently, the June future for WTI is a full 10% LOWER than the current May future. That means that during the 5 transition days (no move on weekends) the oracle price will drop suddenly by about 2%. Now, this does open up other opportunities. If you assume rational actors on Boros, shorting the rate here may make sense, as someone would not rationally long WTI on HL without being compensated those 2% each transition day, which would average about -260% required funding for full 10% compensation over 14 days. However, there are many other possible plays here (short funding, short on HL, long June CME, e.g.). But I'm more interested to know if anyone else has thought up a good play for this.

Stephen | DeFi Dojo

@phtevenstrong

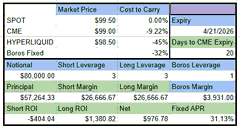

Another incredible strategy available for decent size:

TL;DR: 30% FIXED RATE APR using just @HyperliquidX, CME Futures, and @boros_fi until CME expiry (20 days).

The Set Up

1. Short WTI CME May

This has an implied negative APR of about 9% because it expires at parity with the

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share