On-chain data shows that supply buildup and capitulation by long-term holders continue, with supply pressure of $80,000 to $126,000 being the biggest obstacle to price increases.

Written by: Glassnode

Compiled by: AididiaoJP, Foresight News

Bitcoin remains within the $60,000 to $70,000 range. The spot market shows early signs of accumulation, while the derivatives market has completed its rebalancing. Volatility has cooled somewhat, and the positioning structure is becoming more balanced. However, the market lacks the confidence needed for a sustained breakout due to the absence of a clear catalyst.

summary

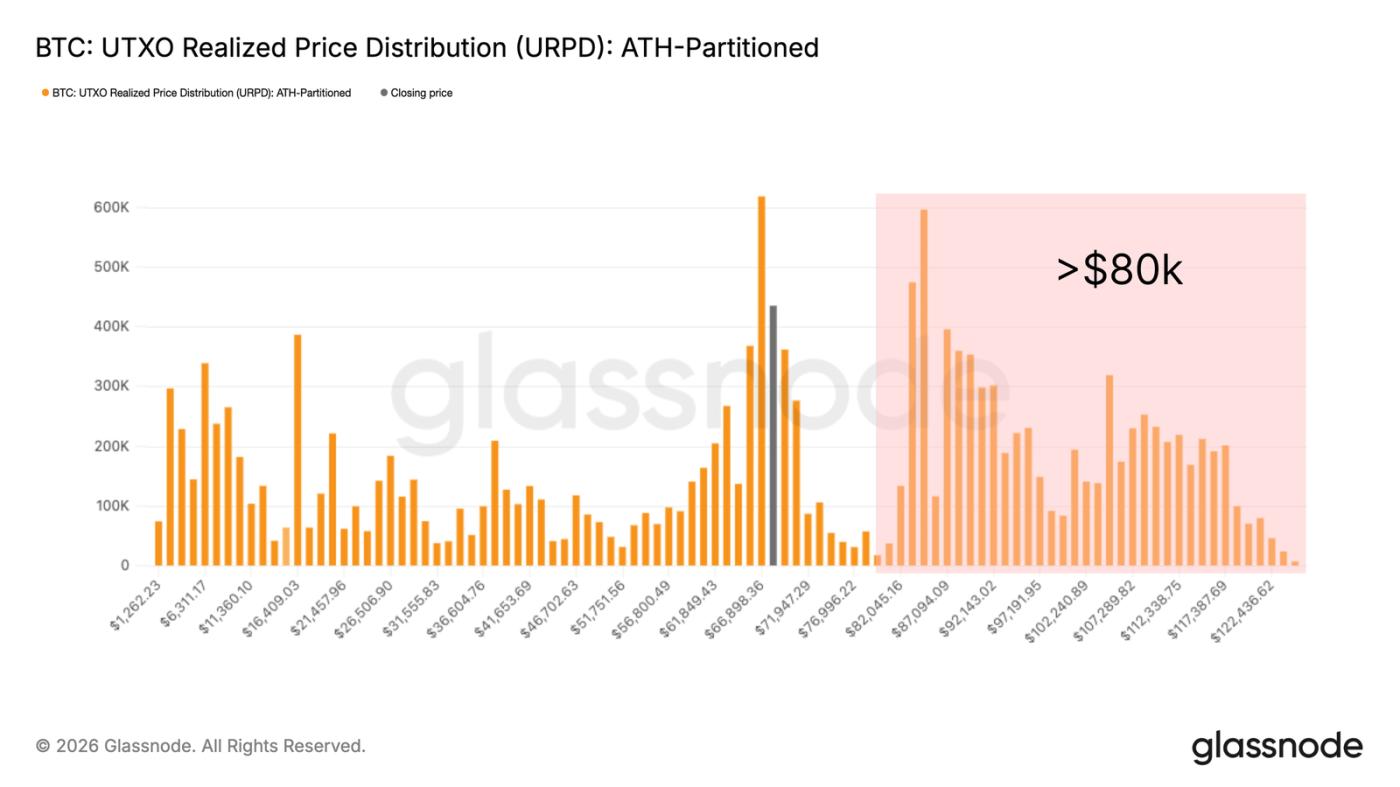

- Bitcoin remains within a wide range of $60,000 to $70,000. URPD data shows a dense supply buildup in the $80,000 to $126,000 range. Absorbing this supply buildup may require a larger price discount or a longer redistribution process.

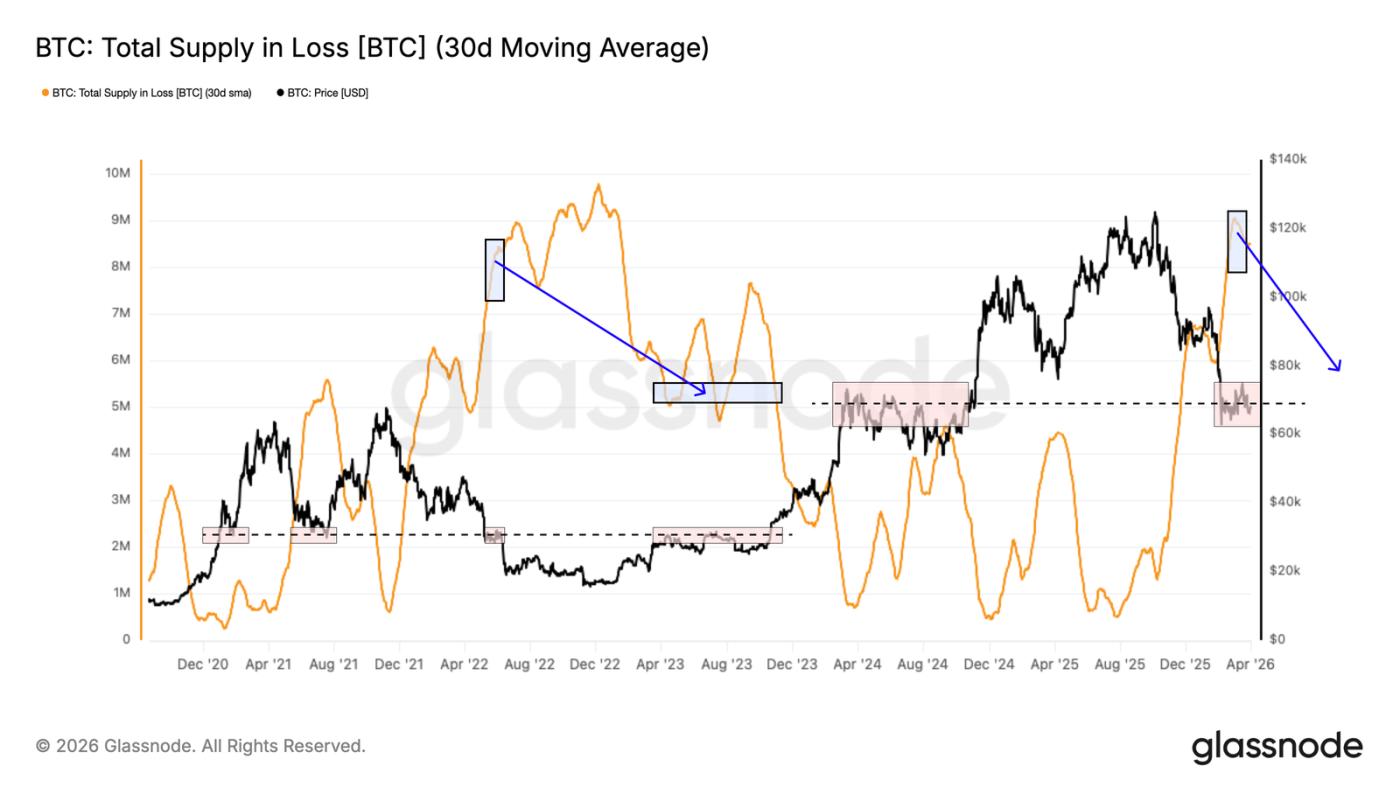

- The total supply currently in a loss-making state is close to 8.4 million BTC, which is similar to the market structure in the second quarter of 2022. At that time, the market needed to redistribute approximately 3 million BTC to return to the cycle midpoint.

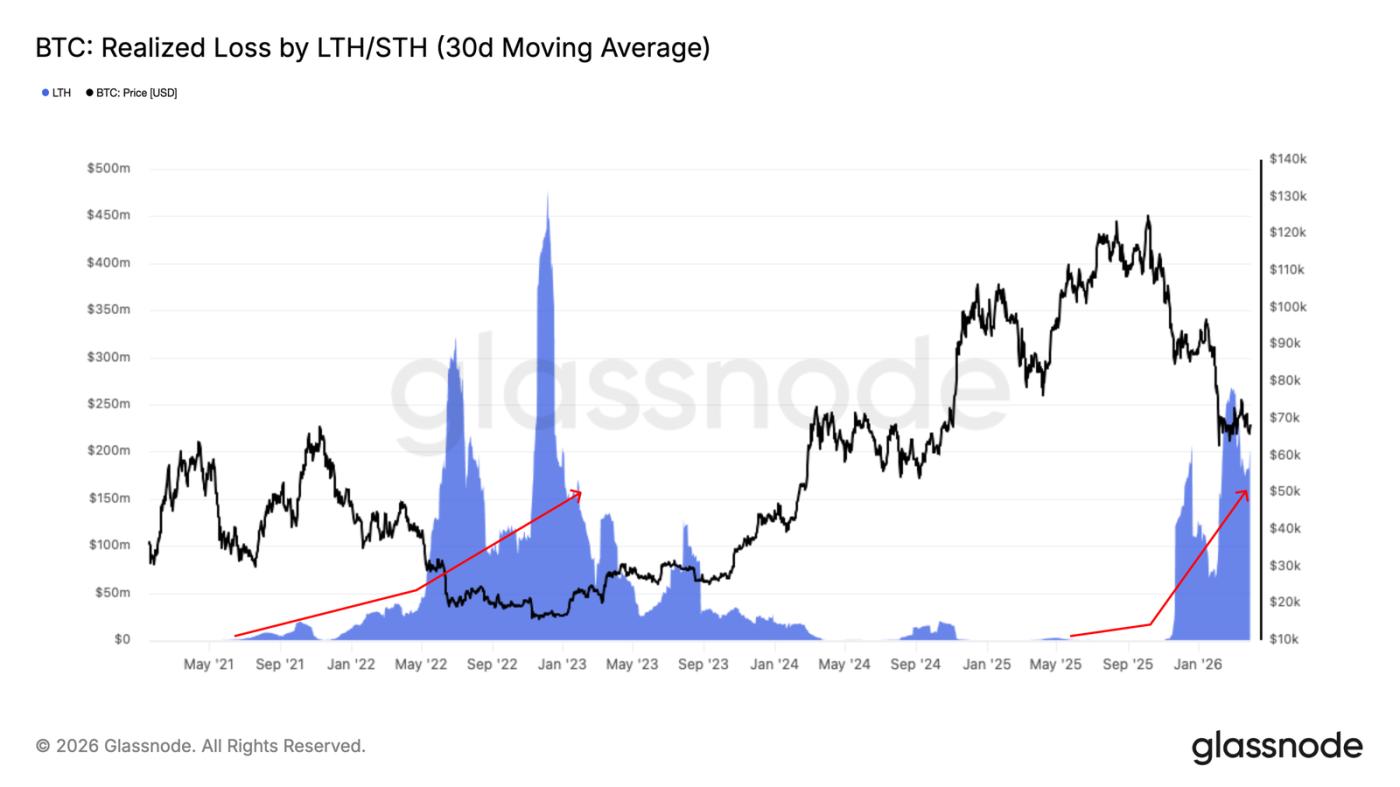

- Realized losses among long-term holders have been steadily climbing since November 2025, currently reaching approximately $200 million per day, confirming the emergence of capitulation behavior. A drop in this metric to below $25 million per day would be a key threshold for market bottoming.

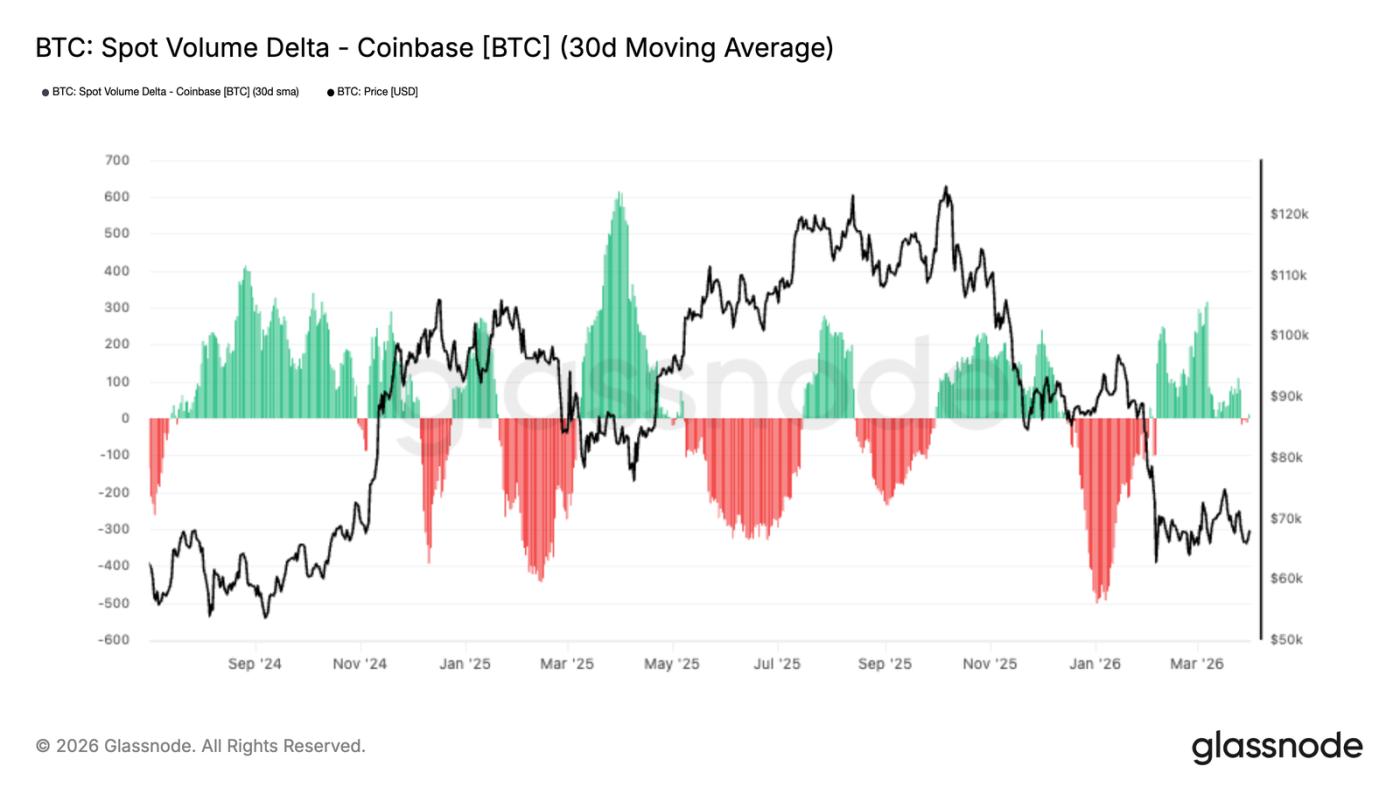

- Coinbase's cumulative spot trading volume differential has turned slightly positive, indicating that spot buyers are beginning to absorb selling pressure. However, current demand levels remain well below what is typically seen when the market forms a sustained low.

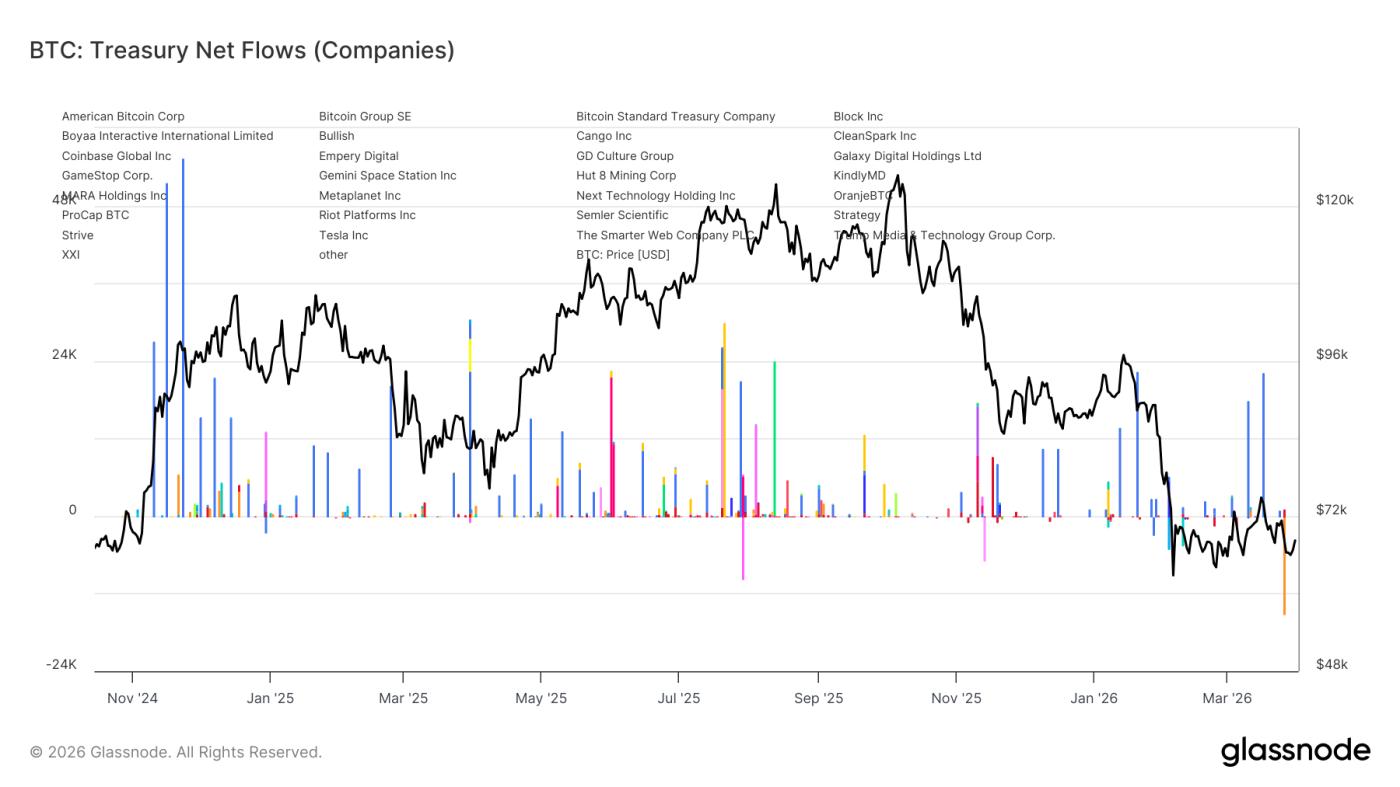

- Treasury fund flows have become more concentrated: Marathon has distributed approximately 15,000 BTC, while Strategy remains the only institution consistently making large-scale purchases.

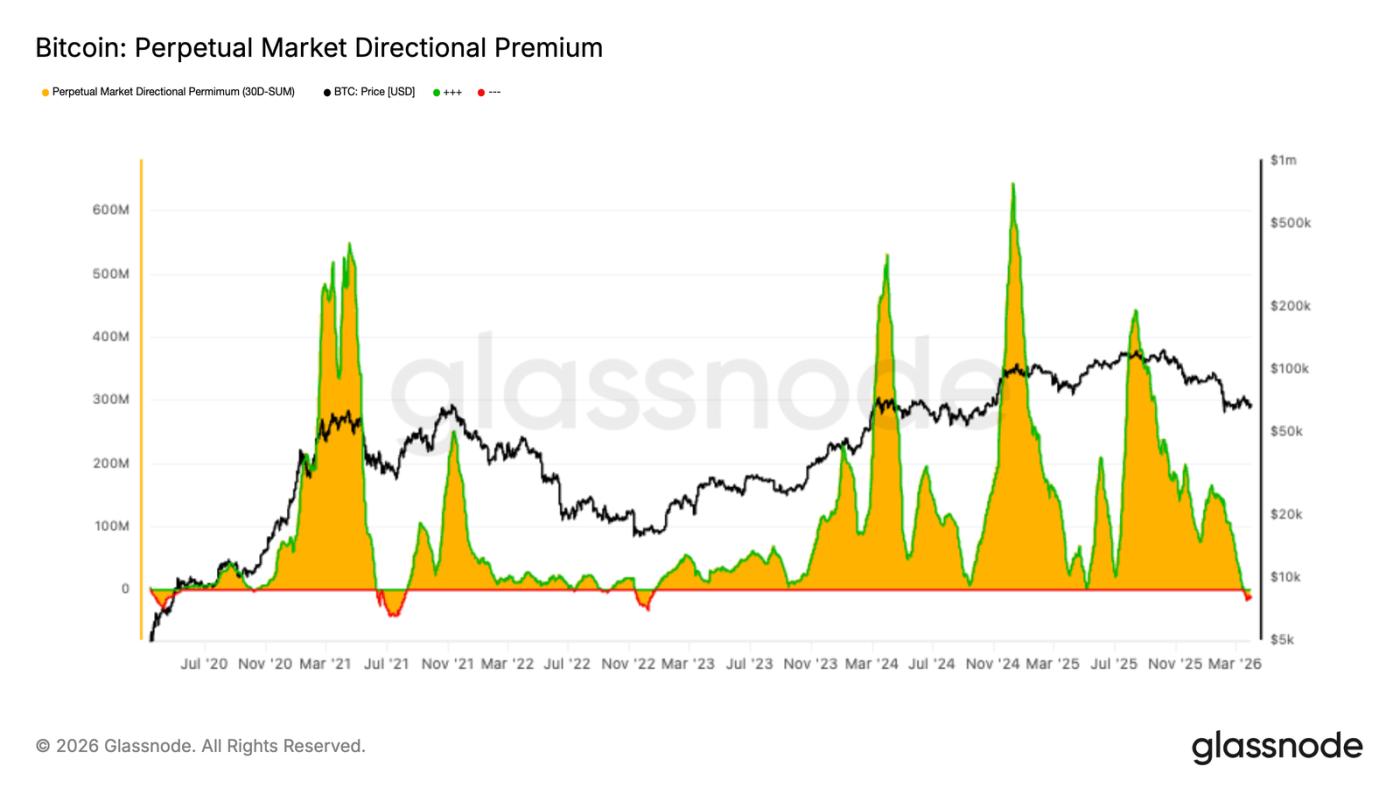

- The directional premium in the perpetual contract market has compressed to near neutral levels and slightly below zero, reflecting the rebalancing of long leverage and a cooling of speculative enthusiasm.

- Current open interest in perpetual contracts is far from being momentum-driven; long positions are being closed out, and short interest is re-emerging. This makes the futures market more balanced overall, but also more cautious.

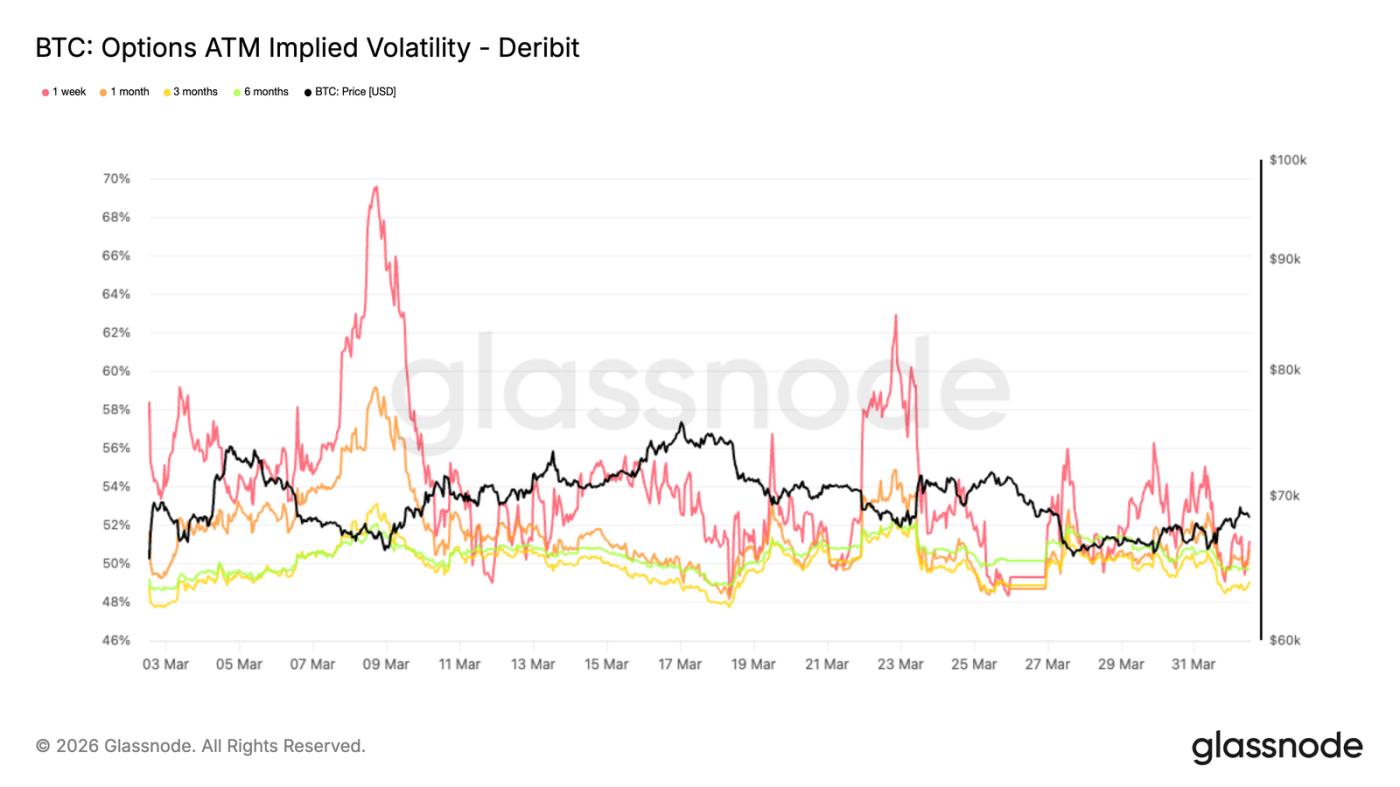

- Implied volatility continued to soften across the term structure, indicating that the options market is pricing in a calmer environment in the near term and a decrease in demand for volatility exposure.

- The skewness indicator has begun to tilt downwards again, indicating a return to protective positioning, but its level is still far below the level that is usually associated with strong hedging demand.

- Gamma positions have shifted back to a supportive position in the market, reducing the convexity effect during price declines and indicating that market makers' short-term position positioning has stabilized after the recent negative gamma phase.

On-chain insights

The volume of unrealized loss-making supply

With prices consolidating in the $60,000 to $70,000 range, this report will move beyond short-term price dynamics to assess the structural forces shaping the current market environment. As discussed in recent reports, one of the most persistent resistances to downward momentum comes from the large supply purchased above $80,000, which is currently operating at an unrealized loss.

This group has endured more than six months of bear market conditions and faces a binary behavioral choice: either sell during any rally to reduce further losses, or psychologically surrender as the price pullback deepens.

The URPD chart clearly illustrates this, showing a dense cluster of supply firmly hanging above the market price in the $80,000 to $126,000 range. Addressing this supply buildup will likely require either attracting new buyers with a significant price discount or a prolonged period of time for these coins to transfer from loss-making holders to more committed new holders.

Loss supply

To quantify the supply accumulation overhead, we can use the metric of "total supply in a loss-making state." This metric tracks the number of circulating Bitcoins whose last moving price was higher than the current spot price. After being smoothed by a 30-day simple moving average to remove short-term noise, this metric currently shows approximately 8.4 million BTC, meaning that roughly 8 to 9 million coins have been in a loss-making state over the past month.

The sheer size of this supply accumulation, coupled with spot prices trading near the midpoint of the current cycle, suggests a market structure similar to that observed in the second quarter of 2022. Historically, resolving such a large supply buildup requires a significant redistribution of coins from losing holders to new buyers entering at lower prices. The precedent of the 2022 bear market is relevant. Typically, the market only decisively regained its position above the cycle midpoint after the total supply in a losing position was compressed from over 8 million BTC to approximately 5 million BTC. This implies that approximately 3 million coins changed hands before market conditions normalized.

Tracking ongoing reallocation

After determining the scale of the loss-making supply that needs to be reallocated, the next step is to monitor the speed of this process. The "Long-Term Holders Realized Losses" metric measures the total losses realized by investors who have held their positions for more than six months and are now selling at a price below their initial cost basis. This metric directly captures the proactive reallocation process of the aforementioned overhead supply.

The 30-day moving average of this indicator has been steadily rising since November 2025 and is currently at a high of approximately $200 million per day. This confirms that long-term holders are increasingly surrendering to the current market. While this wave of losses is a necessary and constructive step in the bear market clearing process, it is not sufficient on its own to constitute a sufficient condition for a market reversal. If this indicator can significantly cool down to below $25 million per day, it will represent a more convincing signal of the exhaustion of selling pressure and is a prerequisite for market bottoming historically before the start of a sustainable bull market.

Off-chain insights

Coinbase spot demand returns

The spot market is showing initial signs of stabilization. The 30-day moving average of Coinbase's spot volume difference has turned slightly positive in the latest data. Previously, it experienced a prolonged period of negative values in January and early February, when persistent selling pressure reflected continued distribution behavior.

Recent shifts suggest that buyers are beginning to absorb available supply and provide support as prices stabilize. However, the size of the positive balance remains modest, indicating that current demand is still exploratory rather than driven by strong conviction.

Historically, stronger market recovery requires sustained positive cash flows in the spot market, while short-term buying often fails to generate subsequent gains. Currently, the recent rebound appears constructive, but a more sustainable recovery may require continued increasing buying pressure.

The flow of treasury funds is becoming more complex.

In recent months, the broad base of treasury fund flows has weakened significantly. Recent data reveals a more uneven and selective pattern of activity. Early in the cycle, corporate hoarding was supported by a wider range of allocators. However, recent fund flows suggest that buying support is becoming increasingly concentrated.

Most notably, Marathon has sold approximately 15,000 BTC, one of the clearest examples of recent corporate cash reserves being reduced rather than increased. In contrast, Strategy appears to remain the only consistent structural buyer; even as participation from other companies becomes more sporadic, the firm continues to buy regularly.

This shift points to a significant change in market structure. Corporate demand is no longer a broad trend of corporate hoarding; it now appears narrower and more reliant on a single dominant player. The end result is that while corporate buying still exists, its base is less broad, and therefore less reliable as a source of structural support compared to earlier stages of the cycle.

Perpetual Premium Reset

Directional premiums in the perpetual contract market continue to compress, with the 30-day total currently near neutral and slightly below zero. This indicates a significant cooling of the bullish conditions that previously supported the rally.

This shift indicates that bullish speculative positions are being liquidated, while short-selling interest is re-emerging. The current structure does not reflect strong market conviction, but rather points to a more cautious and balanced perpetual contract market landscape.

Historically, the resetting of directional premiums has often been accompanied by consolidation or trend exhaustion. This is because leverage is repriced after a prolonged period of price movement. In this sense, the recent decline in premiums indicates that speculative appetite has subsided, allowing the perpetual market to complete a full reset with reduced leverage.

Volatility expectations are decreasing

After the options market positions were reset, implied volatility was the first area to show changes. Bitcoin's volatility term structure shifted downwards overall compared to last week, with front-end maturities leading the decline. The 1-week at-the-money implied volatility is currently 51%, and the 3-month term is 49%. Implied volatility for other maturities is closely aligned in between, with the 6-month term at 49.8%, pointing to a significantly compressed term structure.

This reflects a market that is lowering its expectations for significant near-term volatility, despite lingering macroeconomic uncertainty. Longer-term volatility is relatively more supported, indicating that uncertainty has not disappeared but rather shifted to a more distant time horizon. In the short term, pricing is moving towards a more convergent volatility regime as the market lacks immediate catalysts and the demand for option flexibility has diminished.

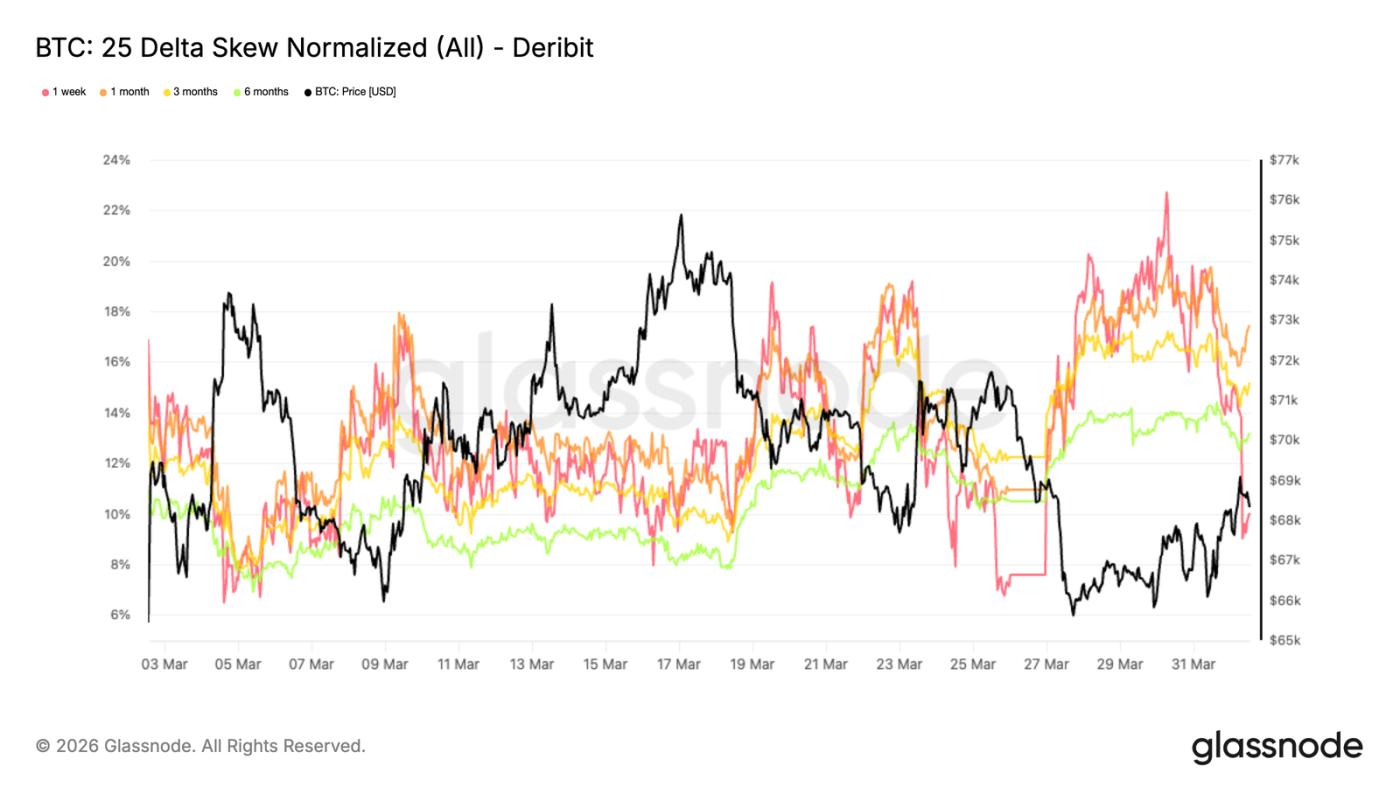

Downlink protection begins reconstruction

As volatility expectations soften, skewness metrics reveal a shift in positioning towards a more cautious approach. A higher 25-delta skewness (calculated by subtracting call options from put options) indicates a greater market pricing bias towards downside protection. Last week, the 1-month skewness hit a monthly high of 22.7% before a pullback, reflecting its sensitivity to immediate price movements. In contrast, longer-term skewness continued to rise and remained high: 17.4% for 1-month and 13.2% for 6-month.

This divergence across different maturities is quite telling. While recent price stabilization has slightly eased short-term hedging demand, strong buying interest remains in medium- to long-term protective options. The market has not aggressively priced in significant volatility, but the overall term structure consistently assigns more weight to downside risk. This points to a persistent defensive bias, rather than merely a temporary reaction to short-term market fluctuations.

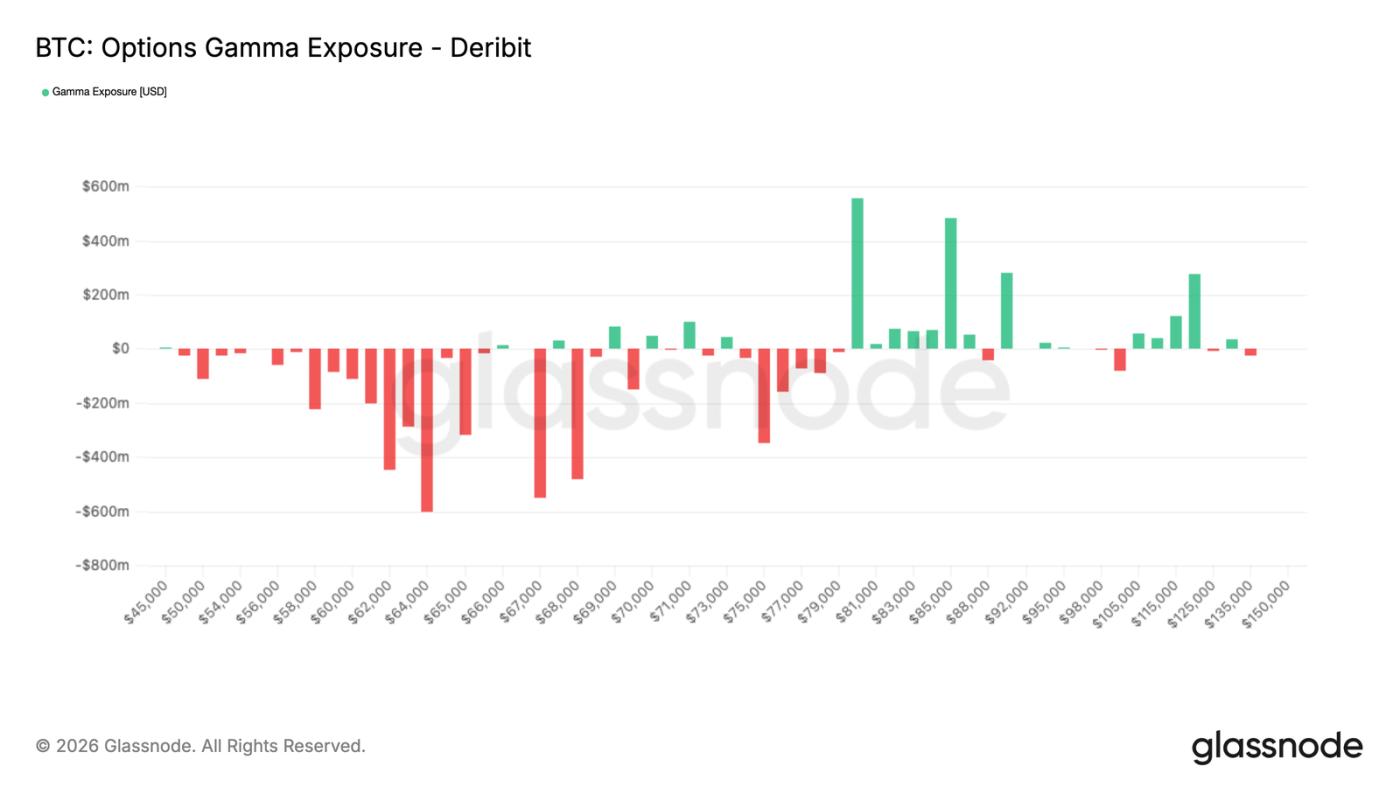

Short-term Gamma is below market level

This more defensive positioning becomes even more relevant when it comes to market makers' gamma exposure. Negative gamma is currently accumulating below current price levels, stretching from $68,000 to over $50,000. This means the market is buying put options below current prices and doesn't expect the recent rally to last long, forcing market makers to be the counterparty in these trades.

Under this mechanism, market makers will be forced to sell when prices weaken, amplifying downside volatility. With market liquidity remaining thin after the March 27 contract expires, the overall market structure appears fragile. Once prices enter this area, the downward momentum could be exacerbated by hedging flows, triggering accelerated selling and transforming what might have been a gradual move into a more dramatic repricing, potentially retesting the $60,000 level—the low point of the February 5 sell-off.

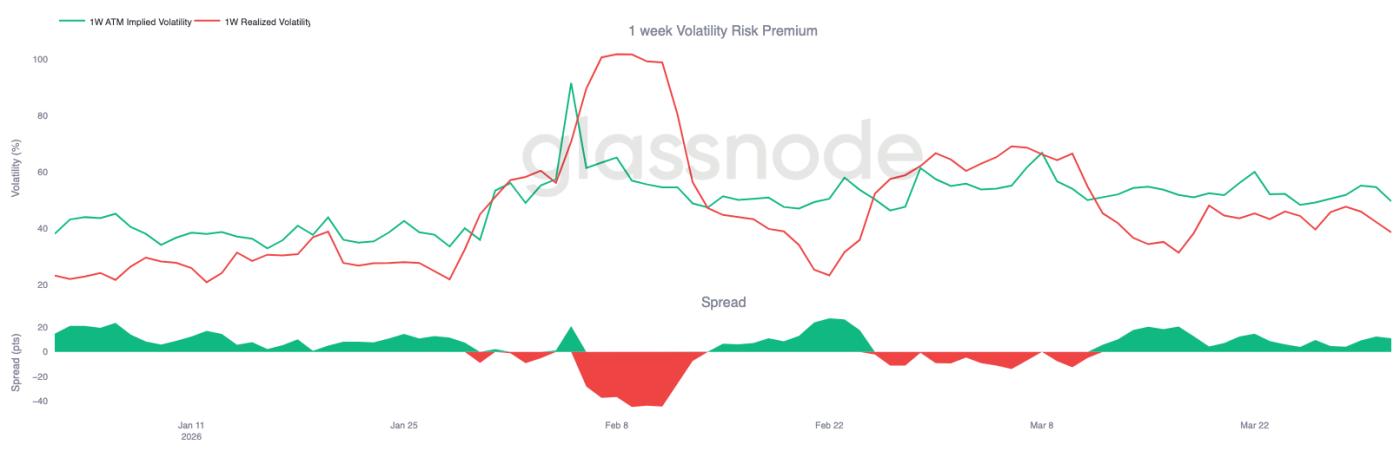

The calm realization of volatility masks the vulnerability.

Adding to the current instability is the persistent higher implied volatility compared to realized volatility. At the front end of the timeframe, 1-week realized volatility is 38%, while 1-week implied volatility is 49%, a difference of 11 percentage points. This gap has persisted for over three weeks, indicating that option pricing is consistently higher than actual market volatility.

At first glance, this reflects a seemingly stable market, as volatility remains within manageable limits. However, the persistent premium suggests that market participants are still pricing in risk despite the lack of actual directional price movement, pointing to an environment of low market confidence.

When volatility pricing is higher than realized volatility and gamma is negative, even relatively small selling pressure can amplify price movements. This is because the market adjusts rapidly from a compressed pricing base, while the holding capacity to absorb capital flows is limited.

in conclusion

Bitcoin remains locked in a wide range of $60,000 to $70,000. The market is showing initial signs of stabilization, but lacks sufficient momentum for a decisive breakout in either direction. On-chain conditions still reflect a market in a recovery phase: loss-making supply remains high, and capitulation by long-term holders has not yet fully subsided. Meanwhile, spot demand is beginning to show signs of improvement, indicating that sellers no longer have complete control of the market.

The off-chain market is similarly in a state of equilibrium. Corporate funding needs have narrowed significantly, perpetual contract leverage has been reset, implied volatility has softened, and market makers' positions have become more stable. These signals collectively point to an environment no longer under significant pressure, but one that still needs to find stronger market conviction.

Currently, Bitcoin appears to be undergoing a redistribution phase rather than emerging with a clear trend. Range-bound trading is expected to remain the primary characteristic of the market until spot demand expands significantly and the overhead supply buildup begins to clear.