View full report 🔍

Stablecoin issuance is one of the most profitable businesses in the crypto industry. However, in an oligopoly structure where USDT and USDC account for more than 85% of the market, it is realistically difficult for latecomers to compete using the same reserve interest model. This report analyzes four stablecoin issuers that have secured positions in different ways within this structure.

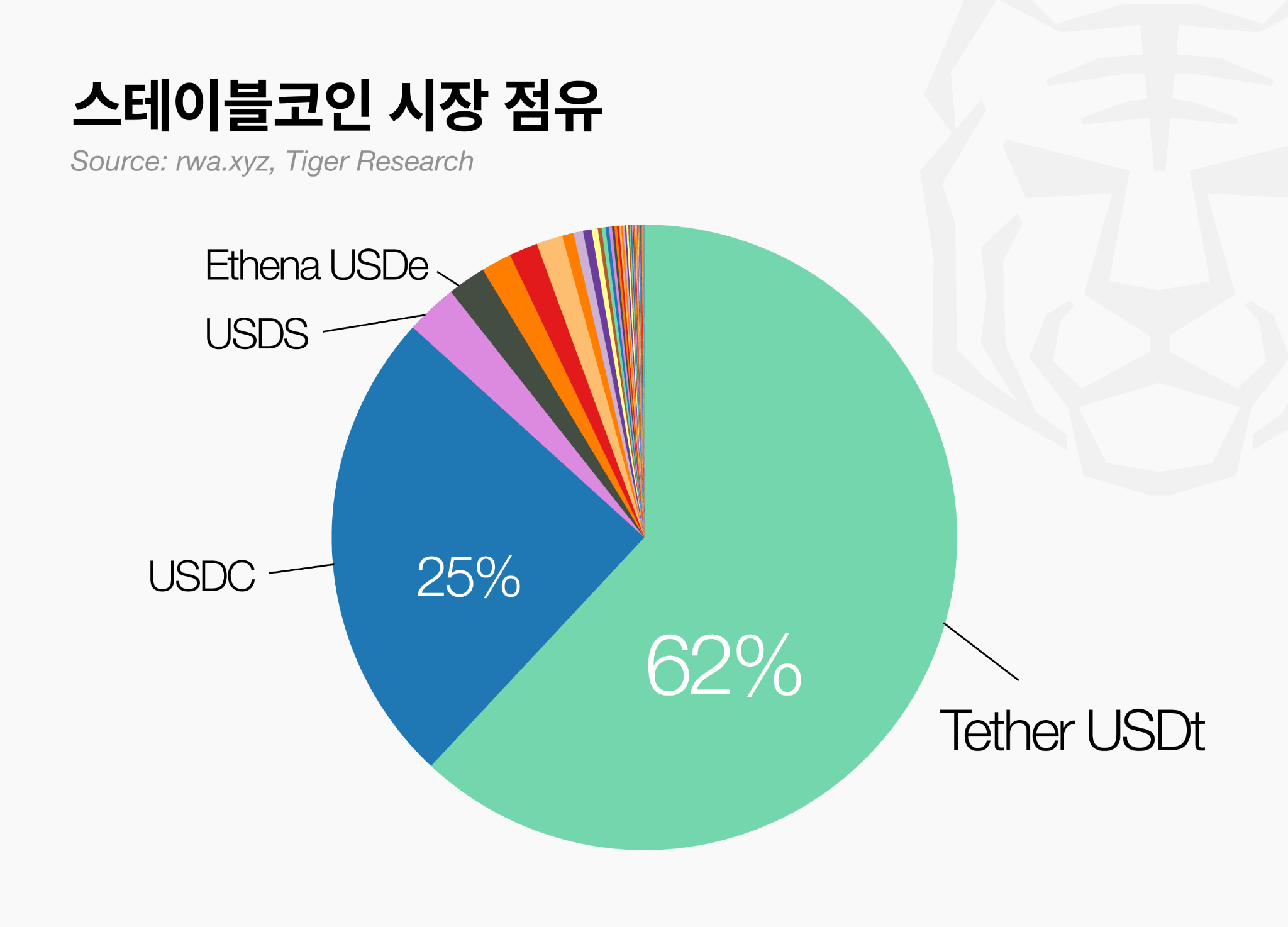

Tether, a market leader with a market share of approximately 62%, is redesigning its trust base and revenue sources simultaneously by introducing full audits by the four major accounting firms and investing in new businesses on top of its core revenue model of reserve management.

StraightX has adopted payment fees as its core revenue source instead of reserve interest. It integrates with physical payment networks such as Alipay+, GrabPay, and Visa Card, and its monthly transaction volume, amounting to 2.5 times its market capitalization, demonstrates the validity of this model. It is also noteworthy that it proactively secured a Major Payment Authority (MAS) license, turning regulation into a competitive moat.

M0 does not issue stablecoins directly, but provides a shared infrastructure that allows other companies to launch stablecoins. Companies such as MetaMask and Exodus are already operating their own stablecoins on this platform, and the structure is such that the network effect is strengthened as the number of issuers and builders increases.

In the absence of domestic regulations, KRWQ adopted a strategy of first absorbing offshore demand in the KRW NDF market, which was already operating outside of regulation. Once regulations are established, the plan is to enter the domestic market using the overseas liquidity it has secured as a weapon, and to expand the same model to major Asian NDF currencies.

The stablecoin issuance market is diversifying into a structure where completely different revenue strategies coexist, rather than a single business model, depending on the scale and positioning of the issuers.

View full report 🔍

Issuing stablecoins is one of the most profitable businesses in the crypto industry. As such, many institutions are targeting this market.

Tether was the first to lead the stablecoin issuance industry. Tether secured a dominant position in the early trading market by playing the role of a key liquidity provider, centered on the USDT market. Subsequently, Circle expanded the market by emphasizing regulatory compliance and significantly expanded its engagement with traditional finance through its listing on the NYSE in June 2025.

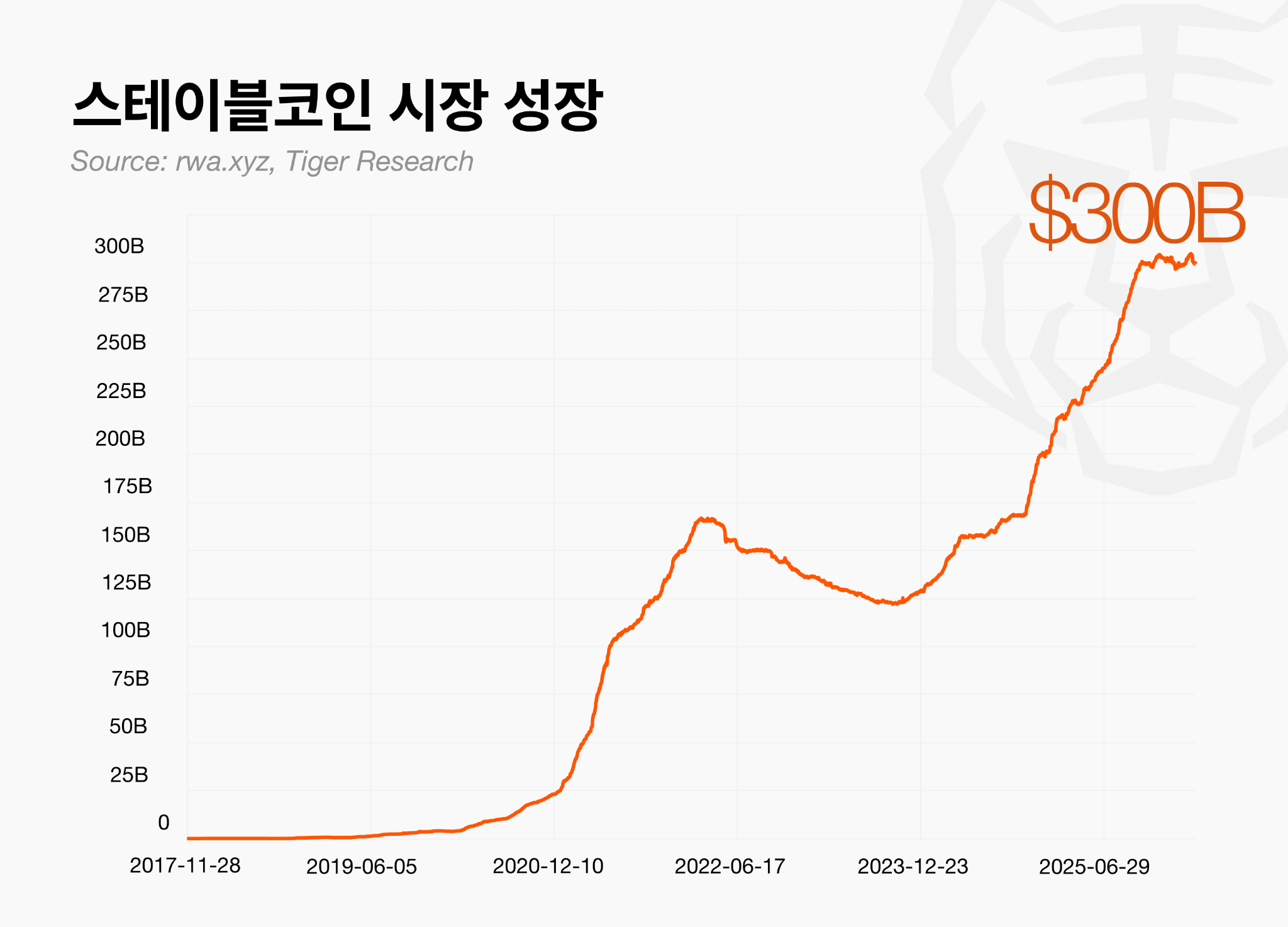

This trend of integration into the institutional framework has driven the total market capitalization of stablecoins up to $300 billion, and major countries have begun scrambling to establish relevant regulatory frameworks. The United States established its first federal regulatory system for payment stablecoins by signing the GENIUS Act in July 2025, while global regulatory competition is intensifying as Europe implements the MICA and Hong Kong enacts its Stablecoin Ordinance.

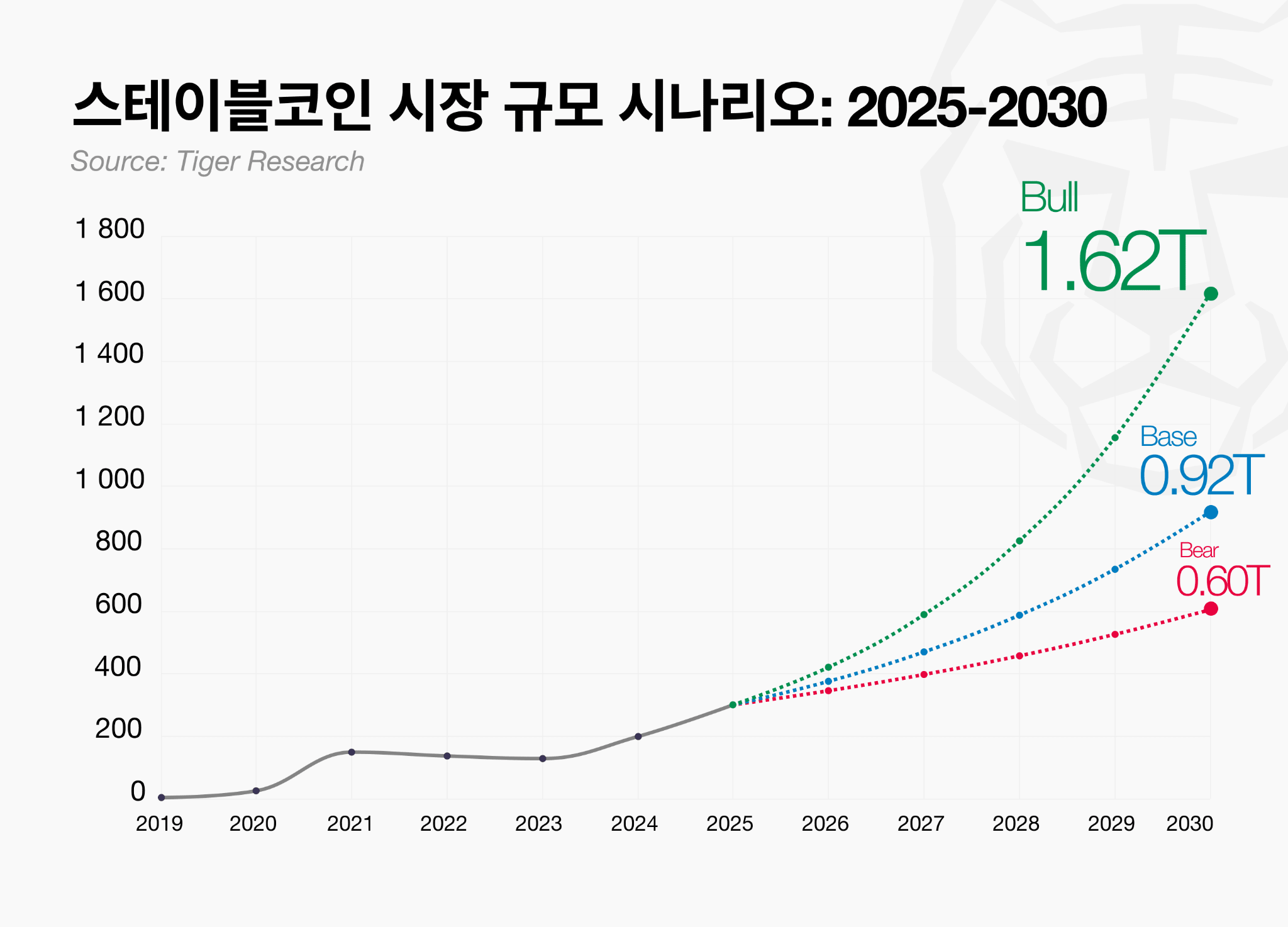

This growth trend is expected to accelerate further. According to Tiger Research's own analysis, the annual net increase in the stablecoin market nearly doubled from $55 billion in 2024 to $101 billion in 2025. If relevant legislation in major countries takes concrete form and demand from institutional investors begins to flow in in earnest, the market size is projected to exceed $600 billion by 2030, even under a conservative growth scenario (15% annual growth).

As the market expands, the issuer's profits naturally grow along with it. While it is easy to view the issuance of stablecoins as merely the act of printing tokens, the actual source of profit lies not in the issuance itself, but in the management of reserves. When a user deposits $1, the issuer issues 1 USDT or 1 USDC and deposits the received dollars into low-risk assets such as U.S. Treasury bonds or money market funds. As the market grows, the size of the reserves expands, and the interest income generated from this becomes the issuer's core revenue.

However, this revenue model is essentially a game of scale. To generate meaningful returns solely from reserve interest, it requires a circulating supply of over tens of billions of dollars. Currently, the stablecoin market is a strong oligopoly structure where USDT (approx. 62%) and USDC (approx. 25%) account for more than 85% of the total. With the remaining 15% divided among dozens of issuers, it is realistically difficult for latecomers to compete solely on the same reserve interest model.

Consequently, players are emerging in the market who are designing revenue sources beyond reserve interest or shifting their business starting points entirely. While some issuers establish points of contact with the real economy by making payment fees their core revenue, platform-type models have also appeared that collect network fees by providing issuance infrastructure rather than directly issuing stablecoins. There are also cases where a contrarian strategy has been adopted in currency zones where regulations are not yet fully established, involving absorbing offshore demand first before entering the domestic market.

Ultimately, the stablecoin issuance market is diversifying into a structure where entirely different revenue strategies coexist, rather than a single business model, depending on the scale and positioning of the issuers. Below, through interviews with key players, we examine how these distinct revenue structures and business models operate.

Tether is the company that first issued USDT, a stablecoin pegged to the US dollar, in 2014. It currently holds approximately 62% of the stablecoin market and plays a pioneering role in the industry.

The reason Tether has been able to maintain its position as the market leader for over a decade is not simply because it started first. What made Tether what it is today was a series of structural transformations. It completely restructured its reserves from being centered on commercial paper to being centered on U.S. Treasury bonds and established a quarterly external audit system. On top of this, it transitioned to a diversified business model that reinvests stablecoin profits into AI, energy, education, and telecommunications.

Business model

Tether's revenue structure is divided into several branches, but the core is reserve management.

Whenever Tether issues USDT, it receives the corresponding dollars and invests them in safe-haven assets such as U.S. Treasury bonds, reverse repos, and money market funds. As the issuance volume increases, the size of assets under management grows, and interest income accumulates proportionally. Since a portion of the reserves is also held in gold and Bitcoin, additional mark-to-market gains are generated when the prices of these assets rise. Based on publicly available information, it appears that returns from managing reserves account for the majority of total profits.

Incidental revenue sources include protocol integration fees and transaction fees. Separately, Tether operates a strategic investment portfolio separated from USDT reserves, investing in the AI, energy, and telecommunications sectors.

Regulatory Response

Since the first quarter of 2025, Tether has obtained a license to issue stablecoins in accordance with El Salvador's Digital Assets Act and is operating under the supervision of the National Digital Assets Commission (CNAD). However, this structure has been criticized for having limitations in terms of transparency. In fact, S&P has assigned USDT a low transparency score based on this.

In response, Tether is targeting the U.S. market separately. While launching USAT , a product exclusive to the U.S. market in accordance with the GENIUS Act regulatory framework, it maintained USDT as its existing global general-purpose stablecoin. This is a strategy of structurally separating the two markets and pursuing them simultaneously.

Responses to the transparency controversy have also begun in earnest. Until now, Tether has maintained a basic framework of quarterly reserve verification reports verified by BDO. In addition, it entered into a formal contract with one of the four major accounting firms in March 2026 and commenced a full audit of USDT reserves.

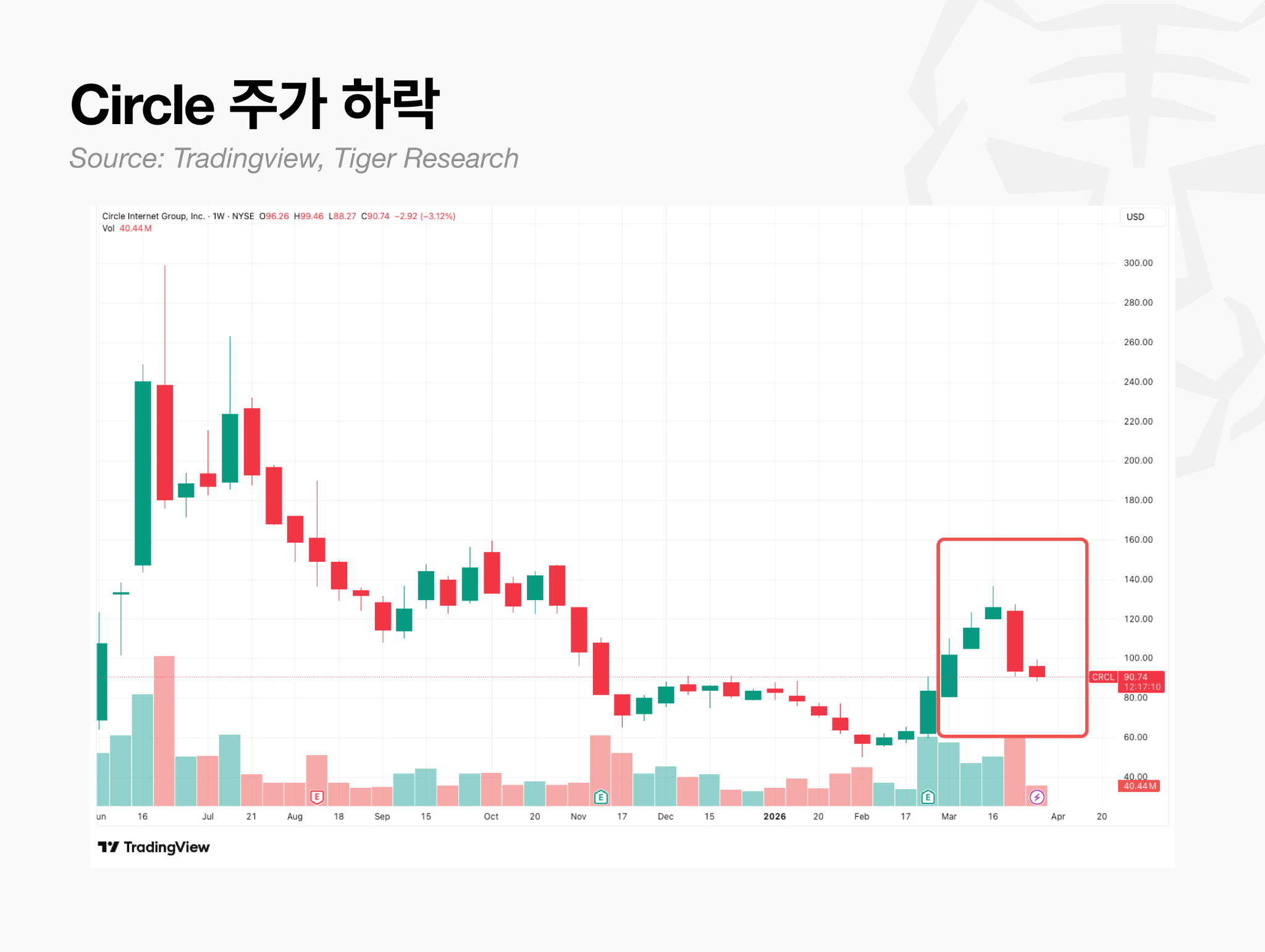

While attestation is limited to verifying the composition of reserves at a specific point in time, a full audit verifies assets, liabilities, and internal control systems to a much higher level. The market took note of this. As Tether's regulatory standing strengthened, Circle's stock price fell by about 20%, which is interpreted as a signal that the competitive landscape of the market itself is being reshaped as the transparency issue—Tether's biggest competitive weakness—is resolved.

Tether's growth strategy is unfolding around the expansion of physical assets (RWA), technological innovation, and new business development.

A representative RWA product is Tether Gold (XAUT). As a token pegged 1:1 to physical gold stored in Swiss vaults, it accounts for more than half of the total market capitalization of gold-backed stablecoins. The size of the underlying assets is also steadily expanding.

The expansion of new businesses is also proceeding at the same pace. Tether maintains its own investment portfolio diversified across sectors such as AI, energy, media, and telecommunications. This portfolio operates completely separate from USDT reserves and serves as a surplus capital growth engine that reinvests profits generated from stablecoin issuance into long-term growth drivers.

Key Implications

The case of Tether contains structural lessons that every company considering entering the stablecoin business must take into account.

1. The issuance of stablecoins is a business of scale. Every time $1 USDT is issued, that $1 is invested in U.S. Treasury bonds. As the issuance volume increases, the holdings of Treasury bonds grow, and interest income increases accordingly. Understanding this structure, where expanding the issuance volume directly leads to an expansion of assets under management (AUM), is the starting point for analyzing the business model.

2. Regulatory compliance is a prerequisite, not an option. Even Tether is eventually coming under regulatory scrutiny. Even in areas where regulations are not yet clearly defined, business structures must be designed from the outset with regulatory integration in mind. Stablecoins are inherently an industry that operates within regulations.

StraitsX: Issuer of ASEAN real-economy-based stablecoin

StraightX is a Singapore-based stablecoin issuer. Its main products are the Singapore Dollar-pegged XSGD and the US Dollar-pegged XUSD, and it is pursuing expansion into major ASEAN currencies such as the Indonesian Rupiah-pegged XIDR.

StraightX is drawing attention because it is building a payment infrastructure directly connected to the ASEAN real economy, going beyond the simple issuance of digital assets. Based on the on-chain data platform rwa.xyz, XSGD's monthly transaction volume (approx. $39.9 million) amounts to about 2.5 times its market capitalization (approx. $15.8 million).

Compared to global stablecoins like USDT or USDC, its absolute asset size and trading volume are small. However, its usage is fundamentally different. While major stablecoins are primarily used for investment and trading on crypto exchanges, StraightX tokens are used for everyday real-world commerce. This means that the issued coins are not locked up in investors' wallets but circulate continuously in the market.

Ultimately, the reason StraightX is recognized as an ASEAN-specific payment infrastructure lies not only in its on-chain metrics but also in the robust B2B payment network integration that underpins it.

Business model

StraightX's revenue model is designed around settlement fees. While reserve interest income is influenced by external variables such as circulating supply and interest rates, settlement fees are linked to trading volume and therefore expand with business growth.

Reserve Interest Income: Reserves corresponding to the circulating supply of XSGD and XUSD are held in trust accounts at DBS, Standard Chartered, and CIMB. In accordance with Monetary Authority of Singapore (MAS) regulations, interest income accrues to the issuers, not the token holders. Based on a combined circulating supply of approximately $65 million, the estimated annual interest income is between $2.6 million and $3.25 million.

Payment processing fees: These are incurred whenever the stablecoin is used for payment or settlement. Major channels include on/off ramps (DVA), QR payment networks (Alipay+, GrabPay integration), and card issuance (Visa BIN sponsorship). The structure is pegged to transaction volume rather than interest rates.

OTC and Exchange Spreads: These are exchange margins generated from stablecoin swaps, buy-sell transactions, and large-scale over-the-counter (OTC) trading.

In particular, payment fees are generated through StraightX's integration with external networks. Major mobile payment platforms such as Alipay+ and GrabPay, as well as global exchanges like Binance and Bybit, have adopted StraightX's system for fund settlement. Notably, according to StraightX's internal data, the volume of Visa-linked stablecoin payments increased 40-fold over the past year, while the number of card issuances rose 83-fold during the same period.

In the crypto industry, it is common to view strict regulations as a constraint on business expansion. StraitsX, however, took the opposite approach. Its strategy is to utilize the regulatory framework of the Monetary Authority of Singapore (MAS) as a shield against competition.

The foundation of this strategy is the Major Payment Institution (MPI) license obtained from the MAS. Through this license, StraitsX has secured the authority to operate six of the seven major payment services regulated by the MAS. This means that beyond simple coin issuance, the entity can legally perform cross-border remittances, foreign exchange, merchant payments, and account issuance within a single entity. XSGD and XUSD are recognized as stablecoins that effectively comply with the MAS Single Currency Stablecoin (SCS) regulatory framework.

For institutional capital to enter the blockchain ecosystem in earnest, bank-level KYC (Know Your Customer) and AML (Anti-Money Laundering) systems must be in place. Most crypto firms operating outside the regulatory framework find it difficult to meet these standards.

StraitsX is jointly developing a next-generation encryption-based identity verification system with regulatory authorities. The strategy is to secure such capital exclusively by preemptively meeting the compliance standards required when institutional funds are injected.

StraitsX, having established its own sustainable revenue model, has a next goal of entering the new settlement market.

The core long-term growth driver is the real-world asset (RWA) settlement sector. As traditional assets such as stocks and bonds are traded on-chain, the demand for tokenized cash as a means of final settlement is also expected to grow. StraitsX plans to preempt institutional settlement demand by providing cross-chain compatibility that spans various blockchain environments.

The core long-term growth driver is the real-world asset (RWA) settlement sector. As traditional assets such as stocks and bonds are traded on-chain, the demand for tokenized cash as a means of final settlement is expected to grow alongside them. StraightX plans to preempt institutional settlement demand by providing cross-chain compatibility that spans various blockchain environments.

1. Turnover is more important than capital size. Non-dollar issuers find it difficult to grow solely by expanding issuance volume. Priority should be given to securing actual use cases and integrating into B2B settlement networks. The key performance indicator is turnover, not market capitalization.

2. Regulatory compliance is a competitive moat. StraightX proactively secured MAS certification, transforming regulatory burdens into structural barriers to entry. Stablecoins are inherently a regulated industry situated at the intersection of traditional finance. How quickly regulatory alignment is achieved and how closely one communicates with the government will be decisive competitive variables.

M0 provides a shared infrastructure that helps companies launch stablecoins and financial institutions issue them.

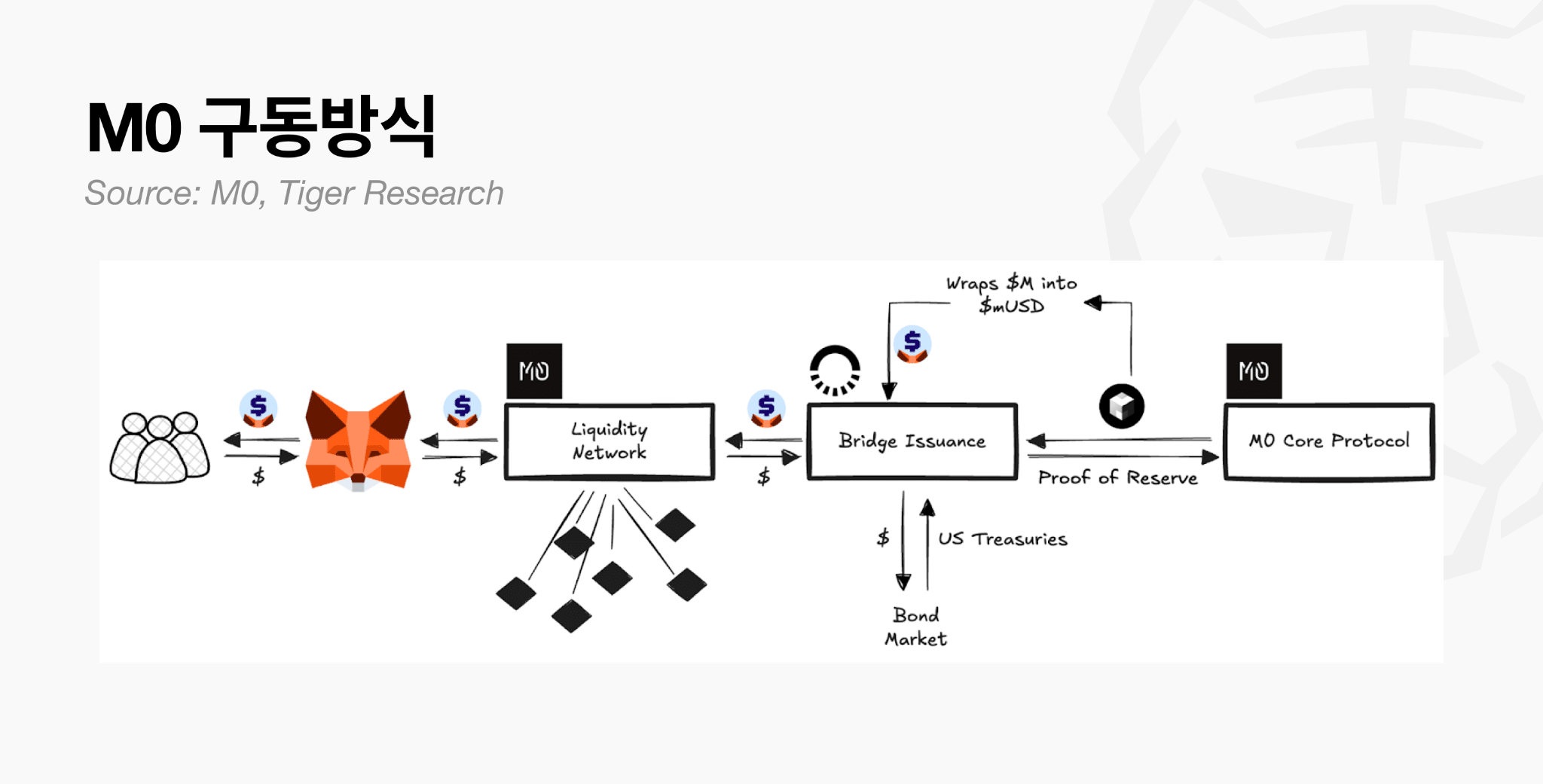

M0 does not issue stablecoins directly. Instead, it provides an infrastructure that allows multiple builders to launch their own stablecoins on a single common technology platform.

This structure solves two key problems.

The current stablecoin market is fragmented. Because each issuer operates an independent issuance stack, compatibility between different coins is structurally difficult.

Without M0, stablecoin builders face the 'cold start' problem because they must secure liquidity, partnerships, and network effects entirely on their own from day one of launch.

M0 solves these two problems simultaneously through a shared layer. All stablecoins on the platform are built with common standards and technology, and upon launch, they can share existing liquidity and be redeemed 1:1 with other stablecoins.

Currently, stablecoins built on the M0 infrastructure include MetaMask's mUSD, Exodus' XO Cash, Cast's USDK, Noble's USDN, and Usual's UsualM, with numerous additional projects under development. Issuers utilizing the M0 issuance stack include Bridge (a subsidiary of Stripe), MoonPay, and OneMoney.

Business model

There are two roles in the M0 platform.

Issuer : A regulatory body that holds reserves as collateral and issues stablecoins through the M0 infrastructure. It pays a portion of the interest income generated from the reserves to the platform at a designated rate.

Builder : An entity holding a specific use case that launches and operates its own stablecoin using a pool of stablecoins issued by the issuer. It can directly design the revenue structure and customize the currency's operation to suit its own products.

MetaMask's mUSD clearly demonstrates how these two roles actually work.

MetaMask designed a proprietary stablecoin called mUSD using M0 technology and layered desired features and products on top of it. The bridge holds a regulatory license, manages U.S. Treasury bonds as collateral, and fulfills platform obligations to issue and burn mUSD according to demand.

The two roles are completely separate. The bridge does not own the end use case or product, and MetaMask does not touch the collateral assets. Nevertheless, the stablecoins delivered to end users can be instantly converted 1:1 with any stablecoin on the M0 network, and liquidity is shared from the start.

The revenue stream begins with interest on government bonds held as collateral by the issuer. While receiving this interest, the issuer separately pays the platform a minter rate (3.33% as of March 2026) on the outstanding balance.

The current circulating supply of M0 is approximately $276 million. This figure is expected to grow further as the number of issuers and builders utilizing M0 increases.

M0 positions itself as a technology platform and structurally separates regulatory compliance obligations by issuer.

M0’s Stablecoin Core has compliance features necessary for issuers, such as allowlist management, suspension, and freezing, embedded in the technology layer. However, each issuer bears direct responsibility for the actual operation of these features, license acquisition, and regulatory obligations such as AML and KYC. M0 provides only technical tools and does not assume regulatory responsibility.

For this separation of roles to actually work, it must be predicated on the issuer complying with the regulations of each market it enters.

M0 views the United States as the market where stablecoin regulation is advancing most rapidly. With the implementation of the GENIUS Act in July 2025, a federal regulatory framework for stablecoins was established, and since then, demand for corporate adoption has accelerated significantly. As major countries establish clear regulatory frameworks, the demand for stablecoins expands, and the opportunity for M0 to establish its infrastructure as the market standard increases accordingly.

M0's top priority is to increase the total circulating supply of stablecoins issued on the platform. This is because, due to the nature of its spread-based revenue model, revenue grows as the circulating supply increases. CEO Luca Prosperi has also stated in a public interview that network expansion is the most important goal for the next two to five years.

The builder base is currently expanding into various areas such as wallets, gaming, fintech, and payments. MetaMask, Exodus, Noble, Usual, and Kast are already participating. In particular, with the demand for stablecoins among enterprises rapidly increasing following the GENIUS Act, now is the opportune time to expand the issuer network. The number of issuers and builders attracted to the platform during this period will determine M0's long-term market position.

The case of M0 demonstrates that the competitive landscape of the stablecoin market is changing. While the key factor in the past was "which stablecoin is the most widely circulated," the focus is now shifting to "who can first dominate the issuer/builder network and infrastructure standards."

Rapid integration creates network effects. Developing on M0's stablecoin infrastructure ensures automatic compatibility with all stablecoin extensions within the platform. There is no need to repeatedly perform integration work separately for each individual stablecoin.

The advantages of infrastructure providers grow with the market. Not all companies possess the capacity to issue stablecoins independently. The value of shared infrastructure, which handles tasks such as securing licenses, building technology, and managing liquidity on behalf of others, increases as the number of issuers grows. This is why M0's structural strengths are reinforced alongside market growth.

As long as the stablecoin market does not become concentrated in the hands of a few dominant players, the value of a common infrastructure that unites multiple issuers and builders is bound to continue rising. Whether M0’s shared standard can establish itself as the industry’s fundamental infrastructure layer is the key question to watch going forward.

KRWQ is a KRW-pegged stablecoin launched by IQ in collaboration with Frax in October 2025. Currently, there is no domestic regulatory framework in Korea for KRW-based stablecoins.

The primary target market for KRWQ is overseas, not domestic. Although the Korean won is legally a currency that can only be traded within Korea, there is significant demand for hedging and speculation regarding fluctuations in the won exchange rate overseas.

For example, foreign investors holding Samsung Electronics shares are directly exposed to fluctuations in the Korean Won exchange rate. They incur losses when the dollar strengthens and gain profits when it weakens. Even if they wish to eliminate this exchange rate risk, there are few suitable means to directly hedge their Won exposure outside of Korea. It is the NDF (Non-Deliverable Forward) that has filled this gap. NDFs are structured to settle the difference between the contracted rate and the actual rate in dollars, without the direct exchange of Won. Having grown on this structure, the Won NDF market currently ranks among the top in the global NDF market in terms of trading volume.

KRWQ's strategy is to secure overseas demand first, and then enter the domestic market once regulations in Korea are established. Overseas first, domestic later. It is essentially just the order reversed.

Business model

The existing NDF market is an over-the-counter (OTC) market centered on bilateral negotiations between banks. It suffers from low price transparency and high transaction costs. Liquidity is also insufficient due to a narrow pool of participants resulting from the Korean government's restrictions on offshore Won trading. Furthermore, counterparty risk is inherent as settlement must be waited for until the contract matures.

KRWQ attempts to resolve these limitations through perpetual futures. NDFs and perpetual futures are structurally the same product.

Won is not exchanged directly.

Settle the price difference in dollars.

It is used for hedging against Korean Won exchange rate risk or for directional betting.

The only difference is expiration. While NDFs have a fixed expiration date, perpetual futures operate 24 hours a day on-chain without expiration and offer the same functionality at a lower cost. Recently, KRWQ launched an NDF market through EDXM International.

KRWQ adopts a dual-track strategy. It establishes overseas markets first and then enters the domestic market once domestic regulations are in place.

KRWQ was designed by preemptively referencing the stablecoin bill currently under discussion in the National Assembly. Its goal is to become the first compliant KRW stablecoin. However, the domestic legislative environment remains complex. While regulatory uncertainty acts as a barrier to market entry in the short term, it also provides KRWQ with time to build up overseas liquidity ahead of competitors.

In the final stage, KRWQ plans to partner with domestic licensed banks to establish an issuance and redemption system through KRW deposits and withdrawals.

KRWQ's growth strategy consists of three stages.

Preemption of Overseas Markets (Current Phase) : Establish a KRWQ-based perpetual futures trading infrastructure targeting overseas institutions and DeFi protocols.

Domestic Transition : Once the domestic bill is passed, enter the Korean market based on the liquidity and infrastructure already secured overseas.

Asian Currency Expansion : The same model is replicated for major Asian NDF currencies, such as the Indian Rupee (INR), Taiwanese Dollar (TWD), and Indonesian Rupiah (IDR), in addition to the Korean Won. These currencies share structural characteristics with the Won, namely the existence of active overseas NDF markets despite the presence of capital controls.

The absence of regulation can be turned into an opportunity rather than a wait. In the Asian stablecoin market, regulation is generally considered a prerequisite for entry, and most players wait indefinitely until laws are established. KRWQ noted that a market structure already exists overseas that operates independently of domestic regulations.

Offshore liquidity serves as a weapon for entering the domestic market. The KRW NDF market was operating outside the jurisdiction of domestic regulations, and KRWQ moved to absorb that demand first. Once regulations are established, it enters the domestic market using its already built overseas liquidity and infrastructure. It did not wait; rather, it started where revenue was already being generated.

The stablecoin market has a strong oligopoly structure, with USDT and USDC accounting for over 85% of the total. Realistically, it is difficult to overcome this barrier with the same revenue model based on reserve interest. However, the cases examined in this report demonstrate that there is not a single path for latecomers to enter the market.

For latecomers, the key is to avoid playing the same game as Tether or Circle. While they may not be able to win the competition in terms of reserve size, they can secure unique positions on distinct axes such as payment networks, issuance infrastructure, and offshore markets. As the stablecoin market grows, the forms of competition also diversify. The current state of this industry is that it is evolving into a market where different strategies coexist, rather than a repetition of identical models.

However, the players discussed in this report have now become leaders in their respective fields rather than challengers. While we can learn from this structure, simply following it exactly is not enough. For the next generation of entrants, the challenge remains to define and solve their own problems beyond the positions already secured by these players.

Ultimately, the players that survive in the stablecoin issuance market will not be those with differentiated entry strategies, but rather those that solve the next stage of problems in the process of executing and expanding those strategies. The market has already passed the stage of “who finds a new model” and is entering a phase of “who actually makes that model work.”

View full report 🔍

This report is based on reliable sources. However, we do not expressly or implicitly warrant the accuracy, completeness, or suitability of the information. We assume no liability for any losses arising from the use of this report or its contents. The conclusions, recommendations, forecasts, estimates, projections, objectives, opinions, and views in this report are based on information available at the time of writing and are subject to change without notice. They may also not align with or contradict the views of other persons or organizations. This report is for informational purposes only and should not be construed as legal, business, investment, or tax advice. Furthermore, references to securities or digital assets are for illustrative purposes only and do not constitute investment advice or an offer of investment advisory services. This material is not intended for investors or potential investors.

Tiger Research supports the fair use of reports. This is a principle that allows for broad use of content cited for public interest purposes, provided that its commercial value is not affected. Under fair use rules, reports may be used without prior permission; however, when citing Tiger Research reports, you must 1) clearly identify 'Tiger Research' as the source and 2) include a logo ( Black/White ) that complies with Tiger Research's brand guidelines. Separate consultation is required if the material is restructured for publication. Use without prior permission may result in legal action.