Morgan Stanley's entry did not change the rules of the Bitcoin spot ETF market, but it completely changed the scale of the players.

Article author and source: 0x9999in1, ME News

Introduction and core viewpoints

Morgan Stanley's official launch of its Bitcoin spot trading platform exchange-traded fund (ETF), code MSBT, marks a historic step in the fusion of traditional finance (TradFi) and crypto assets (Crypto). According to trading data disclosed by CoinDesk, MSBT demonstrated impressive activity on its first day of trading, with volume exceeding 1.6 million shares and a net inflow of approximately $34 million. Even more noteworthy is its groundbreaking management fee of 0.14%, setting a new low for similar mainstream products.

As the world's first Bitcoin spot ETF directly issued by a large systemically important bank (G-SIB), the launch of MSBT marks the transition of crypto assets from the "asset management company-led" 2.0 stage to the "Wall Street universal banks entering" 3.0 stage.

Based on long-term tracking and data analysis by ME News Think Tank, this report presents the following three core judgments:

First, the fee war has entered a more complex phase, but it's not the decisive factor. Morgan Stanley's ultra-low fee of 0.14% is a strategic weapon to open up the market, but the core of competition in Bitcoin spot ETFs has shifted from "price competition" to "liquidity and scale effects." A simple fee advantage is insufficient to overturn the existing duopoly (BlackRock IBIT and Fidelity FBTC).

Secondly, its true competitive advantage lies in its vast internal wealth management network. Morgan Stanley possesses trillions of dollars in client assets and tens of thousands of financial advisors. MSBT's long-term viability depends on its ability to transform its massive traditional high-net-worth client funds into a portfolio of crypto assets through a "whitelist" mechanism and solicited trades.

Third, the market structure will evolve into a stratified hierarchy of "one dominant player and many strong players." MSBT is expected to gain a foothold in the second tier by virtue of its channel advantages, but due to the liquidity discount caused by the lack of first-mover advantage, it still faces great uncertainty in the competition for institutional funds (such as pension funds and sovereign wealth funds).

A Breakthrough Tool: Strategic Considerations and First-Day Performance Analysis of the 0.14% Fee Rate

In the face of fierce competition among similar financial products, fees are the most direct and sharpest weapon. Morgan Stanley's decision to set MSBT's fee rate at 0.14% was not arbitrary, but a meticulously calculated market maneuver.

Quantitative analysis of rate advantages

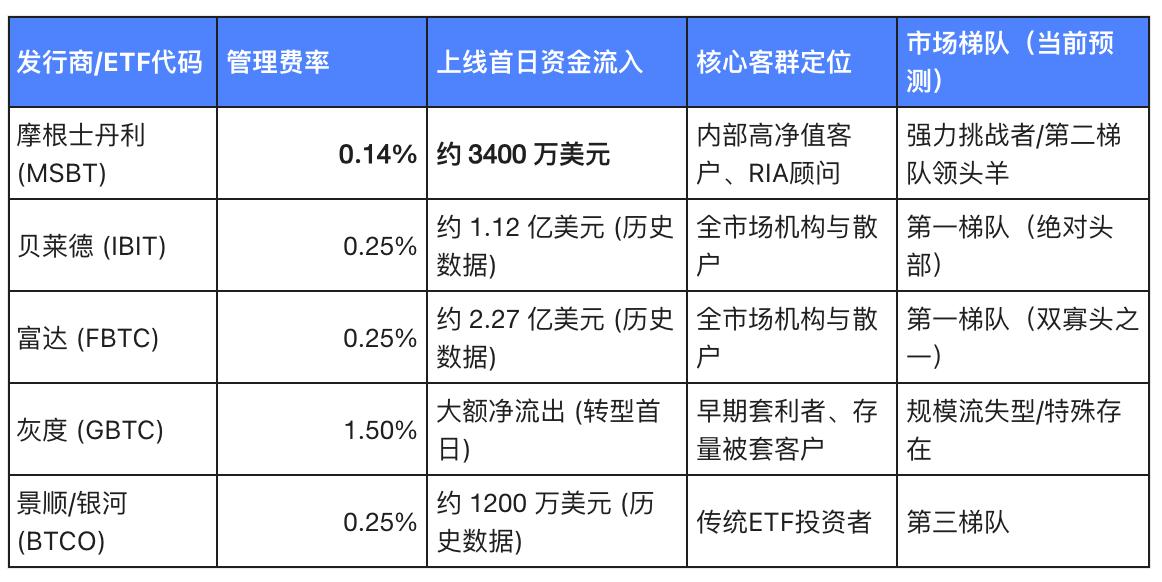

Prior to this, the fees for Bitcoin spot ETFs in the US market were generally concentrated in the range of 0.20% to 0.25% (except for Grayscale GBTC, which was as high as 1.50%). BlackRock's IBIT and Fidelity's FBTC both have long-term fees anchored at 0.25%.

What does a 0.14% fee rate mean? For the average retail investor, the fee difference of $11 on an annual investment of $10,000 is barely noticeable. However, for the high-net-worth individuals and family offices served by Morgan Stanley, the situation is quite different. For asset allocations in the tens of millions of dollars, the hidden cost savings of $11,000 per year, combined with the effect of compound interest, will generate significant returns over a ten-year asset allocation cycle.

To clearly and intuitively illustrate the competitive landscape, we compared the key metrics of major Bitcoin spot ETFs in the market.

Table 1: Comparison of Key Indicators of Mainstream Bitcoin Spot ETFs (Note: Historical data is based on the performance of the first batch of ETFs listed in early 2024 as a benchmark)

Implicit information from the first day's data

MSBT saw over 1.6 million shares traded on its first day, with approximately $34 million in capital inflow. Objectively speaking, this was a "steady but not explosive" start.

On the one hand, compared to the hundreds of millions of dollars flowing into the first batch of spot ETFs in early 2024, $34 million seems relatively modest. This is mainly because the market's "revenge allocation demand" has already been largely absorbed by IBIT and FBTC in the past few years. Moving existing funds (especially considering capital gains tax) incurs frictional costs.

On the other hand, in the current market dominated by a few large players and where Bitcoin prices are fluctuating at high levels, the fact that a non-initial offering could raise $34 million on its first day precisely demonstrates Morgan Stanley's internal mobilization capabilities. ME News Think Tank tends to believe that a very high proportion of this $34 million came from targeted allocations to Morgan Stanley's own wealth management clients, rather than random purchases by retail investors in the public market. This reflects MSBT's unique development path—autogenous growth through self-production and self-sales.

Core Moat: The Conversion Potential of Morgan Stanley Wealth Management Network

If the 0.14% fee is the entry point, then Morgan Stanley's much-vaunted global wealth management network is MSBT's true moat. This is an underlying infrastructure that no pure asset management company (such as BlackRock or ARK Invest) possesses.

The driving force of large AUM and financial advisors

Morgan Stanley manages trillions of dollars in client assets (AUM), and its wealth management division is the core engine of the company's profits. Even more crucial is its large team of Registered Investment Advisors (RIAs) and financial representatives.

In the traditional US wealth management model, ETF sales rely heavily on asset allocation advice from financial advisors. Previously, while Morgan Stanley allowed its clients to purchase Bitcoin spot ETFs, there were strict restrictions: they typically only accepted "unsolicited trades," meaning clients had to request to buy IBIT or FBTC themselves, and financial advisors were not allowed to actively promote them.

With the issuance of MSBT, this rule faces substantial change. Compliance departments typically give higher internal ratings and sales incentives to products they issue and that have undergone rigorous internal due diligence. Once Morgan Stanley opens up "solicited trades" for MSBT by its financial advisors and incorporates it into its standard 60/40 equity/bond asset allocation model (even if it only accounts for 1%-3%), the amount of capital released will be staggering.

The "long-term money" effect brought about by channel closure

The funds of high-net-worth clients are often referred to as "long-term capital." Unlike retail investors who frequently engage in short-term trading on cryptocurrency exchanges such as Coinbase or Binance, funds entering MSBT through wealth management channels have longer holding periods and lower turnover rates.

These investors view Bitcoin as a hedge against inflation or a diversification tool, similar to digital gold. Morgan Stanley's endorsement provides them with an extremely important psychological safety net. Therefore, although MSBT's early momentum may not be as fierce as the first batch of ETFs, its asset size growth curve is expected to exhibit strong resilience and a long tail effect.

Table 2: Analysis of Channel Empowerment Models for Bitcoin Spot ETFs by Different Types of Institutions

Breaking Through the Dilemma: Liquidity Barriers and the Suppression of First-Mover Advantage

Despite its low fees and strong internal channels, we must maintain an objective and impartial attitude when examining the serious challenges facing MSBT. In the ETF market, the winner-takes-all principle is a brutal iron law.

Liquidity black hole and slippage cost

For large institutional investors (such as hedge funds and large pension funds) who truly determine the market landscape, fees are only one factor to consider; liquidity is the key to survival .

BlackRock's IBIT and Fidelity's FBTC have accumulated hundreds of billions of dollars in AUM due to their first-mover advantage, resulting in excellent order book depth. This means that when large institutions need to buy or sell tens of millions of dollars worth of shares at once, the bid-ask spread on IBIT can remain within an extremely small range (usually less than 1 cent), with almost no slippage.

In contrast, MSBT, as a latecomer, initially lagged far behind the leading players in terms of AUM and average daily trading volume. Insufficient market depth leads to significant slippage costs for institutional investors. These slippage costs can easily outweigh the meager savings from a 0.14% fee. This creates a classic vicious cycle: a lack of liquidity discourages institutional participation; conversely, this reluctance to participate hinders the improvement of liquidity.

Matthew effect of market dominance

The ETF market exhibits a strong network effect. The most liquid ETFs attract market makers to provide better quotes, which in turn attracts more trading volume, creating a self-reinforcing positive cycle.

Based on current market data, BlackRock and Fidelity practically monopolize nearly 80% of the incremental funds in the Bitcoin spot ETF market. In this oligopolistic market structure, latecomers find it extremely difficult to overtake established players through conventional means. Morgan Stanley's MSBT will most likely have to rely on its massive client base for growth, making it extremely difficult for it to seize market share from IBIT in the public market.

Macroeconomic trends and capital flow analysis: Why focus on this particular time?

Morgan Stanley's decision to launch its own spot ETF at this juncture is not only a supplement to its micro-product line, but also a reflection of its profound foresight into the macroeconomic and regulatory environment.

- Regulatory certainty has been established : Since the US SEC approved the first batch of spot ETFs, Bitcoin's status as a compliant asset is irreversible. The initial concerns of traditional banks regarding Anti-Money Laundering (AML) and Know Your Customer (KYC) have been alleviated by the smooth operation of the first ETFs. Entering the market now avoids early compliance pitfalls.

- The upward shift in the inflation center and the demand for safe-haven assets : Against the backdrop of global debt expansion and frequent geopolitical conflicts, the demand for non-sovereign assets among high-net-worth individuals is genuinely growing. Morgan Stanley does not want to relinquish this lucrative allocation demand to pure asset management companies like BlackRock. Direct involvement is a logical necessity, allowing them to retain funds within their own system while earning management fees.

- The "equalization" of returns in crypto assets : The profits from the past decade's cryptocurrency bull market were largely captured by Silicon Valley venture capitalists and crypto-native institutions. The widespread availability of large bank spot ETFs signifies that Wall Street's "old money" has officially gained control of mainstream pricing and distribution power in the crypto market.

Conclusions and Investment Recommendations

Based on the above logical framework and empirical data, ME News Think Tank has drawn the following qualitative and quantitative strategic assessments of the Morgan Stanley Bitcoin Spot ETF (MSBT):

1. Market Positioning and End-Game Prediction :

MSBT is unlikely to overturn the current market landscape dominated by BlackRock's IBIT. It's not the terminator of the first tier, but rather the strongest gatekeeper of the second tier . Its low fee of 0.14% demonstrates its sincerity towards investors, but its true core competitiveness lies in the targeted support from Morgan Stanley's multi-trillion-dollar wealth management channels. It is projected that within the next 12-18 months, leveraging internal conversion capabilities, MSBT's AUM will steadily climb to the billions to tens of billions of dollars, becoming an undeniable force in the market.

2. Profound impact on the industry ecosystem :

The transformation of major banks from "distributors" to "issuers" marks the deepest integration of crypto assets into the traditional financial system. The emergence of MSBT is highly likely to trigger a domino effect, forcing other Wall Street investment banks such as Goldman Sachs and JPMorgan to reassess their crypto strategies and even launch similar competing products in the future. Bitcoin has completely transformed from a geeky fringe experiment into a standardized profit center on Wall Street.

3. Investment recommendations for different types of investors :

- For high-net-worth clients within the Morgan Stanley system : MSBT is an excellent asset allocation tool. Its extremely low fees and seamless integration with the bank's system lower the operational barriers and transaction costs, making it suitable as a satellite asset in a long-term portfolio (recommended allocation: 1%-5%).

- For institutional/quantitative funds seeking maximum liquidity and intraday trading : In the short term, BlackRock's IBIT and Fidelity's FBTC remain the preferred options, as their deep order books can handle large inflows and outflows without significant slippage. MSBT's liquidity metrics still need time to develop.

- For ordinary retail investors : if their brokerage platform waives transaction commissions and they plan to hold the stock for a long time (more than three years), MSBT has a definite cost advantage in the long run with its ultra-low management fee rate of 0.14%; for short-term swing traders, the experience of major mainstream ETFs is not significantly different.

Morgan Stanley's entry hasn't changed the rules of the Bitcoin spot ETF market, but it has fundamentally altered the scale of the players. In this feast of Wall Street giants, crypto assets are ushering in the most solid and profoundly reshaped chapter in their history.

Source cited:

- CoinDesk. (2026). Morgan Stanley Enters the Fray: Spot Bitcoin ETF Sees 1.6M Shares Traded on Day One. 2. Bloomberg Intelligence. (2025). Bitcoin ETF Market Structure and Liquidity Analysis Report.

- SEC Filings. (2026). Morgan Stanley Bitcoin Spot ETF (MSBT) Prospectus and Fee Schedule.