Article by: Prathik Desai

Article compiled by: Block unicorn

“The further you look back, the further you are likely to look forward.” — Winston Churchill

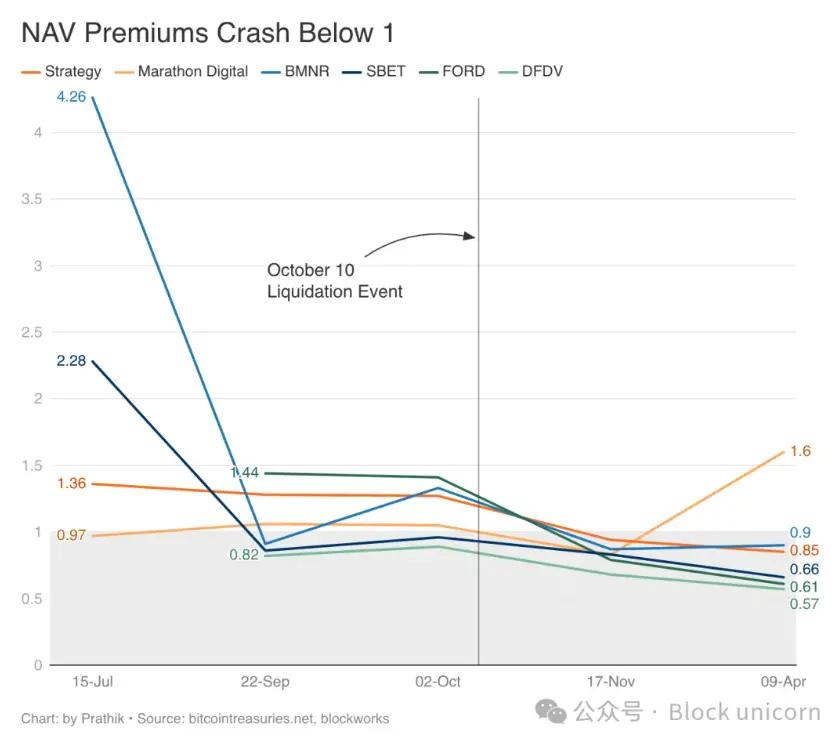

The current state of digital asset vaults (DATs) bears a striking resemblance to closed-end funds in the United States during the 1920s. People bought shares of closed-end funds, which then purchased stocks on the open market. Investors indirectly received the beta returns from these stocks, paying a premium for it. These funds once commanded speculative premiums as high as 30% of their net asset value (NAV) until the stock market bubble of 1929 turned those premiums into discounts. Investors eventually realized, with painful lessons, that this investment approach was not profitable.

When I read this, it felt familiar, just like everything we've seen in the DAT ecosystem over the past few months. It's hard not to see the similarities.

Bitcoin-based DATs (such as Strategy) offer leveraged returns pegged to the price of BTC. Investors pay a premium for this. This flywheel effect works when cryptocurrency prices rise; however, it collapses when the market crashes. The key to a DAT's continued success in market cycles lies in which underlying assets its appreciation is linked to. Most cryptocurrency vaults surrounding BTC and ETH are leveraged bets on the price increases of their underlying cryptocurrencies.

But what if the token price is closely correlated with the revenue generated by its ecosystem? What if it has little to no correlation with uncertainty? Even more ideally, what if it is negatively correlated with the performance of other asset classes during periods of macroeconomic uncertainty?

In today's in-depth analysis, I will use a HYPE-based digital asset strategy (DAT) company as an example to explore why DAT's asset selection determines the sustainability of its digital asset strategy.

Hyperliquid Strategies' (ticker symbol: PURR) DAT journey began with the formation and acquisition of Rorschach LLC, a special purpose acquisition company (SPAC). The company then reverse-merged this SPAC with Sonnet BioTherapeutics, a Nasdaq-listed biotechnology company that was struggling at the time, its flagship cancer drug having been seeking a commercial partner for years.

This is exactly the same strategy that Twenty One Capital used previously on the BTC project, when BTC was backed by Tether, Cantor Fitzgerald, and SoftBank.

At its inception, PURR held 12.6 million HYPE tokens, valued at $583 million, along with $305 million in cash. Earlier this year, the company spent $129.5 million to purchase an additional 5 million HYPE tokens.

But why should Hyperliquid Strategy achieve better results than the previous DAT?

Different jars

In the first wave of DAT, its packaging format itself was innovative. Companies could exchange BTC for ETH and ETH for SOL, and this model worked well. This was because its flywheel effect was built around a premium to the company's net asset value (NAV). The underlying asset didn't matter. As long as DAT shares traded at a premium, investors would buy, hoping to profit from the token's price increase.

However, this bet reversed when the market struggled to recover from the cryptocurrency industry’s biggest single-day liquidation.

Although the reckoning came suddenly and followed US President Donald Trump’s new trade tariff threats against China, DAT’s fate was not unexpected.

Months before the liquidation event, we wrote an article pointing out the risks of Strategy's DAT model, a leading Bitcoin vault strategy:

"This strategy worked well during Bitcoin bull markets because capital appreciation was favorable, allowing for the purchase of more Bitcoin, while rising market capitalization also drove up earnings. However, the sustainability of this model depends on continued market access and rising Bitcoin prices. Any significant downturn in the cryptocurrency market would quickly reverse the second-quarter results, while fixed expenses such as debt interest and preferred stock dividends would continue."

Fast forward to mid-November, and we see the concerns about DAT that have been building for months come to life: declining mNAV, slowing Treasury purchases, and falling DAT company stock prices.

The problem with this strategy is that the three major treasury assets—Bitcoin (BTC), Ethereum (ETH), and SOL—share a common, thorny flaw: they do not generate cash flow themselves. Their price increases depend entirely on how people trade these cryptocurrencies. And this trading is driven by a variety of factors: ETF fund flows, institutional investor interest, discussions in online forums and communities, and investors' perception of BTC's role as "digital gold" in the macroeconomic landscape.

Admittedly, ETH and SOL do compensate for their slow token appreciation through staking rewards. However, staking rewards are paid out in the form of newly minted tokens. Each time ETH and SOL staking rewards are paid out, the equity of existing token holders is diluted in exchange for validators.

Funds holding these assets (whether BTC, ETH, or SOL) operate similarly to closed-end funds holding a single, non-dividend-paying position. Their only profit comes from either a rise in token price or an increase in net asset value premium. The former is affected by market volatility, while the latter is driven by market narratives.

While both Ethereum and Solana generate transaction fees, only a relatively small portion of the revenue is returned to token holders. In 2025, Ethereum's on-chain transaction fee revenue was approximately $515 million, while Solana's was $645 million. The majority of this did not reach token holders; it was either pocketed by validators or offset by newly issued tokens.

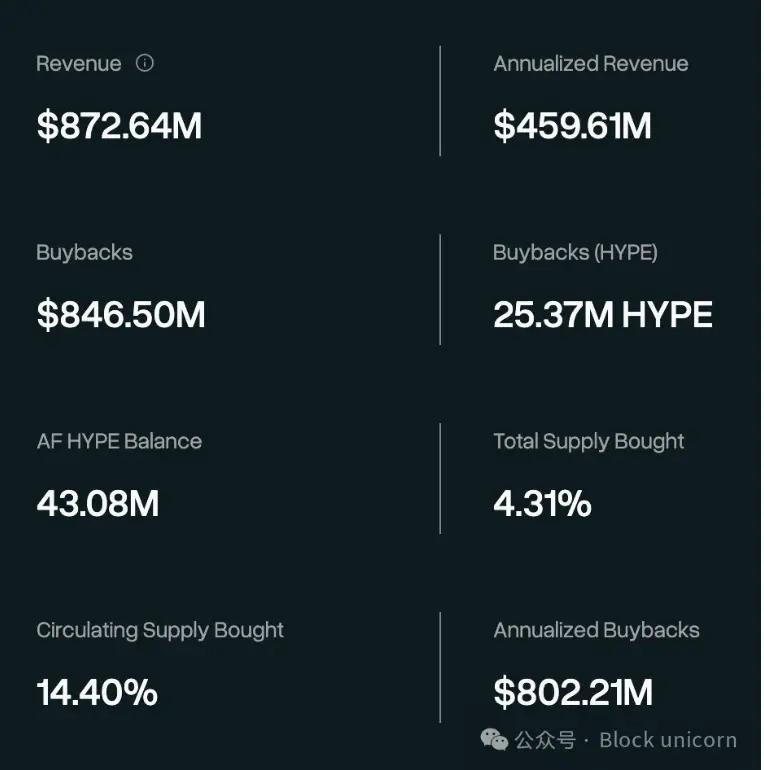

In comparison, the Hyperliquid protocol incurred nearly $1 billion in fees last year. Even more compellingly, 97% of those fees were returned to HYPE holders through buybacks via an aid fund.

Hyperliquid currently has a daily trading volume of $5 billion to $7 billion and a monthly trading volume of approximately $200 billion, generating about $730 million in fees annually from trading activity. Therefore, every dollar traded on Hyperliquid helps strengthen the fundamentals of HYPE's pricing.

Hyperliquid currently has a daily trading volume of $5 billion to $7 billion and a monthly trading volume of approximately $200 billion, generating about $730 million in fees annually from trading activity. Therefore, every dollar traded on Hyperliquid helps strengthen the fundamentals of HYPE's pricing.

This makes HYPE Vault feel less like storing BTC or ETH in a vault waiting for market valuation, and more like holding receipts for derivatives exchange fees.

Any listed package holding HYPE, including the HYPE recently held by PURR, is essentially still a bet on the price of HYPE. Their organizational structure is identical to that of the treasury companies of BTC, ETH, or SOL. This allows us to view them from the same perspective. However, considering the fundamental factors driving the token's price movement, I am more optimistic about the HYPE treasury company.

PURR's share price reflects its indirect claim to the present value of all cash flows generated by the Hyperliquid protocol from its derivatives business.

You don't have to believe me completely. Hyperliquid has proven this multiple times recently.

A proven case

During the Iraq War last month, both risk assets and traditional markets experienced volatility. HYPE rose 40%, while the S&P 500 and Bitcoin weakened. The former fell 3% to 5%, and the latter rose 5%.

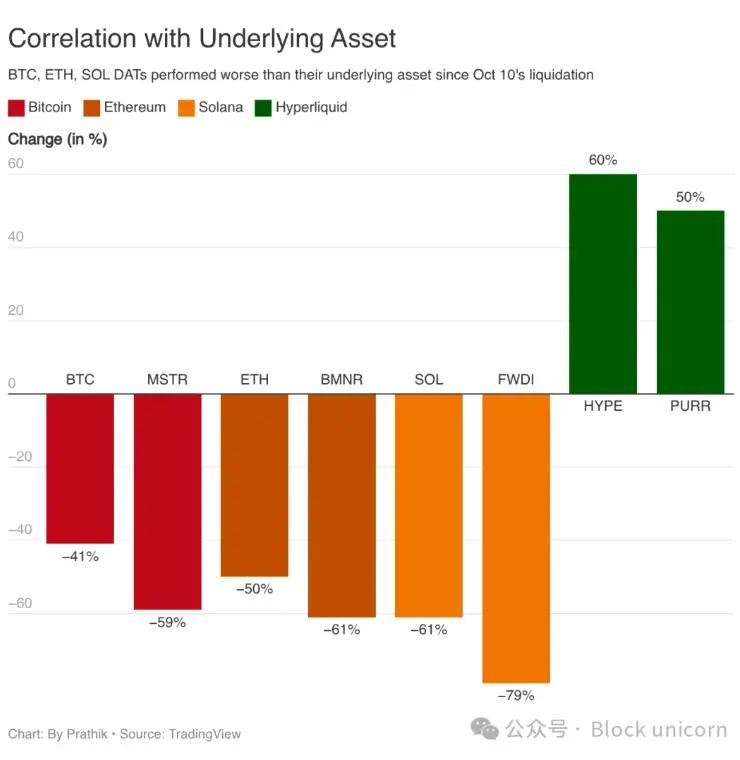

Since the largest cryptocurrency liquidation event on October 10, the price of HYPE has risen by about 60%, while the price of BTC has fallen by 40%.

This is no coincidence. Uncertainty-driven volatility is detrimental to passive stores of value but beneficial to derivatives exchanges. Uncertainty prompts traders to hedge positions. Liquidation events incur costs for both parties. Factors that erode the net value (mNAV) of Bitcoin vault strategies, however, benefit traders by allowing them to generate more funds on exchanges.

This is no coincidence. Uncertainty-driven volatility is detrimental to passive stores of value but beneficial to derivatives exchanges. Uncertainty prompts traders to hedge positions. Liquidation events incur costs for both parties. Factors that erode the net value (mNAV) of Bitcoin vault strategies, however, benefit traders by allowing them to generate more funds on exchanges.

This bear market, which brought Bitcoin and Ethereum vaults to their demise, has instead generated record trading volumes and fees for the Hyperliquid ecosystem. While Bitcoin and Ethereum vaults can only wait for the market crash to pass, Hyperliquid's profits have flourished in this environment.

Hyperliquid's HIP-3 market further reinforces this argument by bringing traditional assets, including metals such as silver and gold, onto the blockchain and enabling investors in financial markets to express their views across asset classes.

I believe this is the biggest reason why HYPE's DAT strategy differs from other strategies.

Nobody is safe

PURR's DAT strategy remains a bet on the price of Hyperliquid. Hyperliquid may lose its existing market share and be replaced by competitors such as Lighter and Aster, or some protocol that has not yet been conceived.

However, despite these challenges, the choice of underlying assets remains a source of confidence. PURR's institutional backers tout their DAT strategy as "the only way for US investors to participate in HYPE." But the entire DAT strategy could become obsolete if fund companies are allowed to issue HYPE spot ETFs. 21Shares and Grayscale have both submitted applications.

Earlier DATs needed to worry about maintaining their net asset value premium. This depended on market sentiment and investor confidence in the model. HYPE-based DATs, however, only needed to answer a simpler question: Can Hyperliquid continue to be profitable? This question depended more on weekly fee data, potential market share, and the protocol roadmap—including the upcoming HIP-4.

All of this is data that analysts can use to make informed decisions. Analysts can still make mistakes, but they have data to support their judgments.

There is a counterargument here.

What if Ethereum and Solana surpass Hyperliquid in transaction fee revenue? It's not impossible. But the situation becomes much more complicated when Hyperliquid returns profits to HYPE holders through buybacks.

While Ethereum returns a portion of its transaction fees to ETH holders, this is entirely offset by new ETH issued to validators. Solana's fees, on the other hand, go entirely to validators, with a negligible amount ultimately reaching Solana holders. Both Ethereum and Solana would need to rewrite their underlying token economics to reach the yield levels of Hyperliquid tokens. Simultaneously, network activity must be several times higher than current levels. These are not things that can be accomplished overnight.

Even if this happens, I believe the same argument still holds true. I don't believe that HYPE will always be the only successful asset in DAT. I believe that DATs built on assets that can generate consistent returns for holders will have a longer lifespan than those built on assets that cannot generate consistent returns.

These two models are quite different. The first generation of DATs (debt financing agreements) expects investors to believe in the story they have built and to underwrite them, while the second generation expects investors to believe in their cash flow.

Those closed-end funds that survived the 1929 bubble economy were those that continued to pay dividends during market downturns. Everything else was just speculation in disguise.

DAT, fueled by hype, may ultimately disappear like other DATs. No one can be sure. But criticism of them will likely revolve around market share, transaction fee stability, and other fundamental business metrics. At least they won't end up like the BTC DAT crash, with the "I told you so" sentiment.