Written by: Noah Levine, Guy Wuollet, Robert Hackett

Compiled by: Luffy, Foresight News

The global financial system is being restructured on new infrastructure, and this process is progressing at a pace far beyond what most people outside the crypto industry realize.

Stablecoins are the core catalyst for this transformation. They have long since evolved from niche trading tools into the foundational infrastructure of the financial system and are becoming the cornerstone for building a new generation of global financial products. This article outlines our views on this transformation. The landscape of companies within the sector may shift, and the boundaries of sub-sectors will continue to merge and evolve, but the more fundamental change lies in structural upgrading: how is the new architecture of global finance being constructed, in what aspects is it maturing, and what gaps still exist?

The core argument of this article is that stablecoins are giving rise to a completely new form of Bank as a Service (BaaS) model. In the previous wave of BaaS, fintech companies primarily relied on leasing banking licenses and integrating with traditional core systems to conduct business. This current transformation is fundamentally different: companies are building their businesses on on-chain infrastructure, using self-custodied wallets to reduce transaction friction and dependence on intermediaries; and simultaneously integrating basic financial functions such as accounts, payments, foreign exchange, and credit into end-to-end financial products.

Ten years ago, building such end-to-end financial services required applying for licenses in multiple regions and connecting with local banks in various places; now, as long as you have this new underlying technical architecture, any team can quickly implement related services.

Stripe's acquisition of Bridge and Privy, and Mastercard's acquisition of BVNK, demonstrate that these established companies are employing similar strategies to address the ever-changing market landscape. Major players are engaging in consolidation and mergers, striving to firmly grasp key underlying links before the new infrastructure landscape takes shape.

All signs indicate that on-chain finance transformation has become an irreversible trend. The choice before us is either to embrace and adapt to it, or to be left behind by the times.

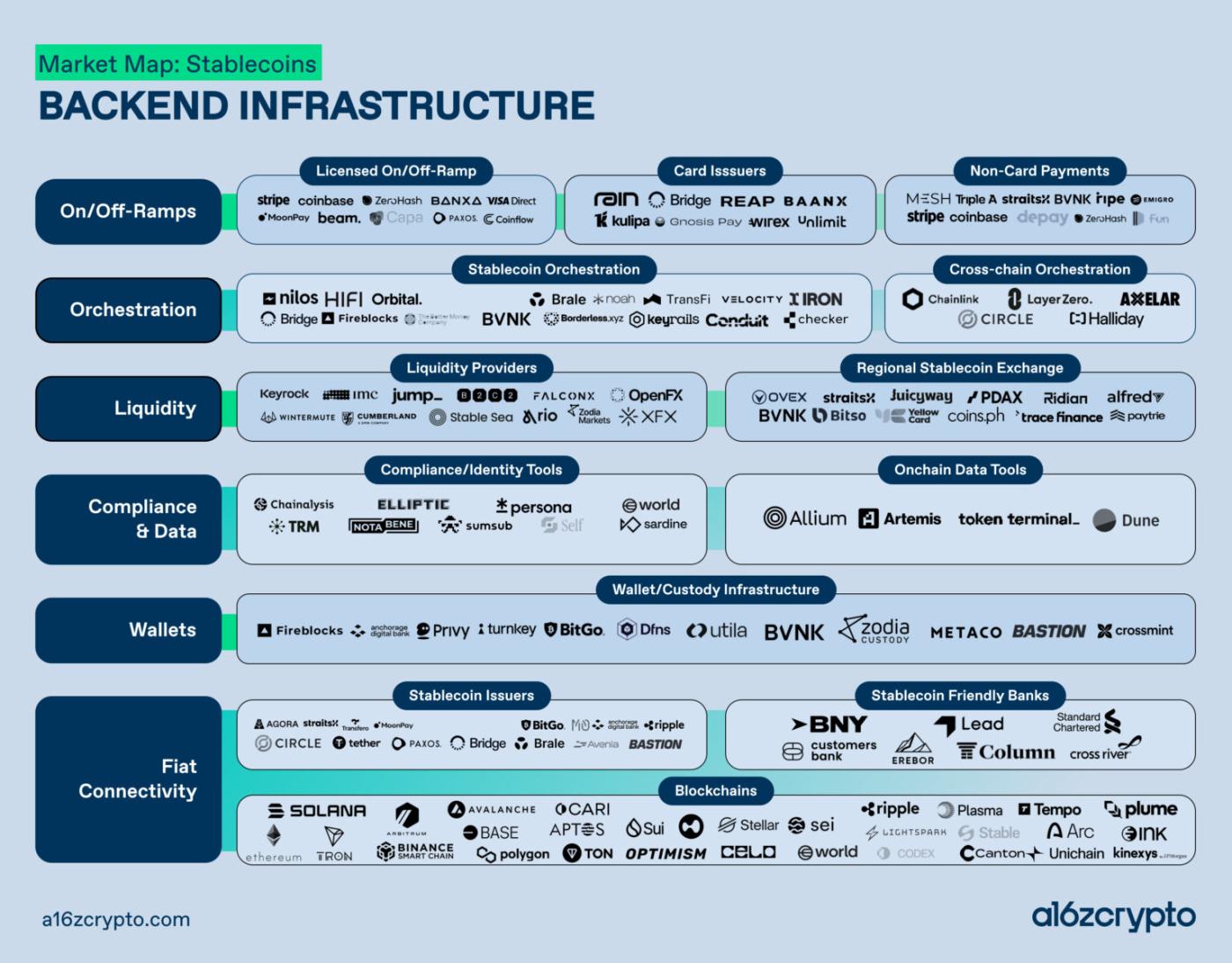

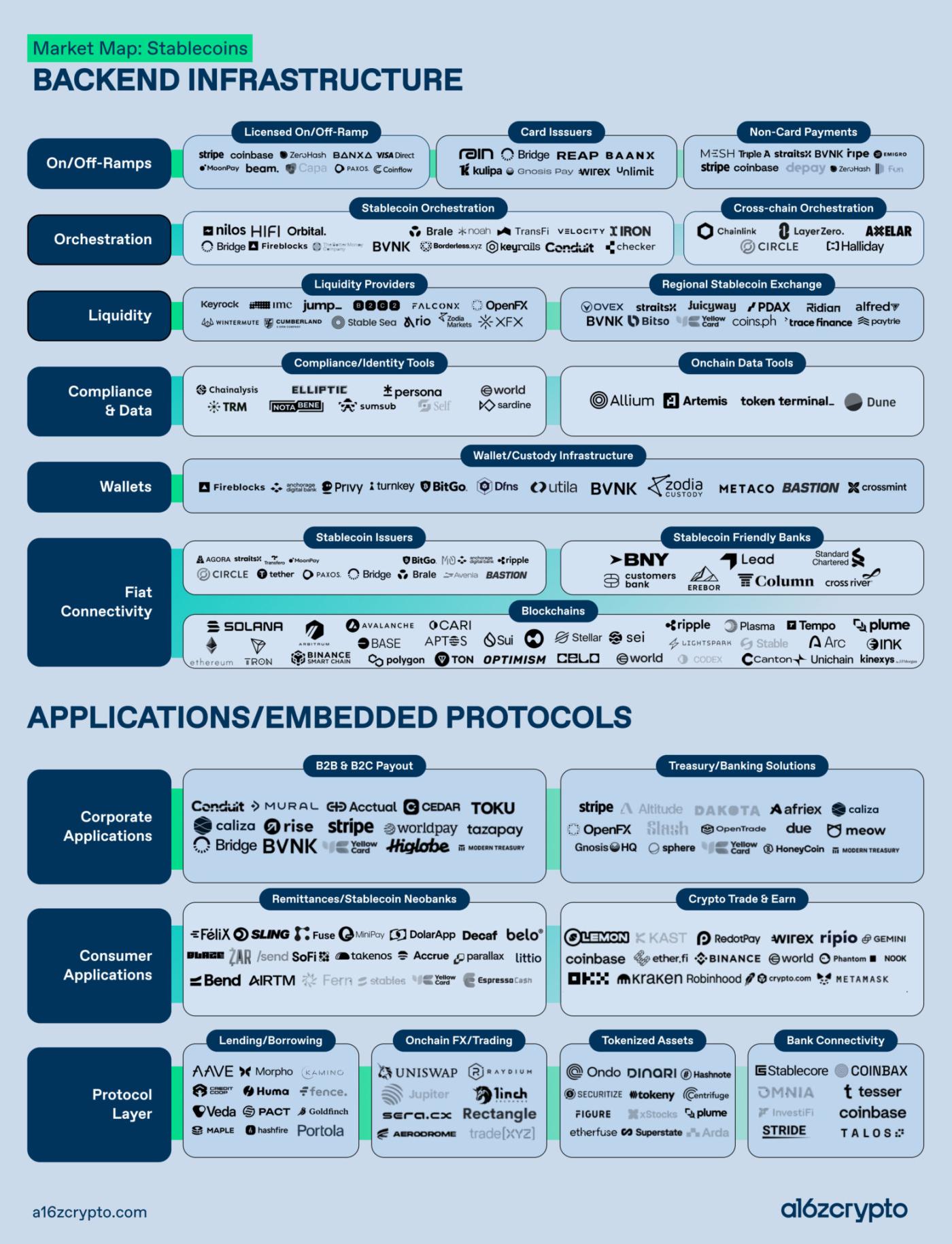

Stablecoin Market Landscape

Three types of blockchain

The previous perception that all blockchains were vying for similar application scenarios is crumbling. Currently, the industry has differentiated into three types of blockchain networks with distinct positioning, each designed based on different needs and prioritizing different performance trade-offs. Understanding these differences is crucial to comprehending the true landscape of global fintech implementation.

General-purpose public blockchains (represented by Solana, Ethereum, and their mainstream L2 networks) remain the core battleground of the crypto capital market, covering core scenarios such as trading, lending, and decentralized finance. This sector boasts a large market size and stable development, but it cannot fully encompass all industry trends.

Payment-specific blockchains represent another emerging category, specifically designed for financial services applications. Networks like Stripe's Tempo and Circle's Arc are competing in functionalities never before optimized for general-purpose blockchain layers: stablecoin-native gas fees, privacy guarantees, and, crucially, predictable transaction costs. Cost modeling capabilities are critical for a fintech company processing millions of payment transactions. Companies in this space are betting that payment-oriented blocks will become the settlement layer of choice for next-generation financial infrastructure.

Institutional networks, a third type of network, such as Canton, are designed for regulated entities that require programmability and privacy protection while adhering to statutory compliance frameworks. As banks and asset management companies accelerate their entry into the market, the core role of these compliant networks will become increasingly prominent.

Bottlenecks in banking operations are loosening.

Over the past decade, bank partnerships have been the biggest bottleneck to the development of native crypto financial services. High barriers to entry and fragile relationships with banks pose the most significant survival risk to crypto companies.

While this situation hasn't completely disappeared, it has improved significantly. A group of compliant banks embracing the crypto space are working to establish interconnectivity between on-chain infrastructure and the traditional fiat currency system.

Deposit and withdrawal channels used to be a core challenge for all practitioners in the industry, but now the feasibility has been greatly improved. The establishment of fiat currency channels is the operational foundation of stablecoin-native fintech companies, which is not only significant for the payment process, but also crucial for the entire technology stack.

Stablecoin issuers: A far-reaching licensing race

The competition in the stablecoin issuance sector is currently more intense than ever before, with the core of the competition now shifting entirely to compliance and regulatory arrangements. Since the implementation of the U.S. GENIUS Act, major issuers have been vying to apply for trust licenses from the Office of the Comptroller of the Currency (OCC).

In the short term, a license can give a company compliance credibility, obtain official recognition at the federal level, and win the trust of regulatory agencies and institutional partners.

In the long run, the stakes are even higher. If regulators grant Federal Reserve clearing access to institutions holding national banking licenses in the future, stablecoin issuers who secure compliant licenses first will be deeply integrated into the core global financial system and become key participants in the digital transformation of finance.

This competition is less a battle of brands and more a struggle for dominance within the payment system. More importantly, it's about who can lay the foundation for the prosperity of credit and capital markets.

Liquidity service providers: the last mile problem

Stablecoins have achieved a major breakthrough in the intermediate links of cross-border payments, greatly simplifying the intermediate steps of cross-border fund transfers: faster settlement speeds, reduced reliance on pre-deposited agent accounts, and lower friction costs in cross-border transfers.

The remaining issue is liquidity between stablecoins and local fiat currencies, particularly in emerging markets. Insufficient liquidity in most cross-border channels leads to problems such as slippage, settlement delays, and price instability. If these issues remain unresolved, they could severely hinder the potential of stablecoins in business-to-business (B2B) applications.

This gap is beginning to narrow through the following three channels:

- Forex service providers that support stablecoins (such as OpenFX and XFX).

- Regional exchanges that have a deep understanding of local fiat currency resources (Bitso in Latin America, Yellowcard in Africa, Coins.ph in Southeast Asia);

- In the future, we will directly support partner banks for stablecoin foreign exchange settlement.

All three types of entities are indispensable. Foreign exchange service providers offer technical integration capabilities, regional exchanges solidify the liquidity depth of the local market, and banks provide balance sheet support and a global correspondent banking network. No single channel can independently complete the closed loop.

Bank connections: an indispensable key link

The entire infrastructure of stablecoins is built almost entirely by fintech companies, non-bank payment institutions, and native crypto enterprises, operating independently of the traditional banking system. This model brings the advantages of efficient and open development, but it also creates structural risks: the underlying architecture of stablecoins is inherently incompatible with the traditional core systems used by most banks, requiring a dedicated switching layer to achieve connectivity.

"Bank integration services" form this crucial transition layer. Related companies build dedicated infrastructure to help banks quickly launch stablecoin-related businesses without completely replacing their existing legacy systems.

A number of forward-thinking service providers have gradually expanded their business scope, extending from the crypto capital market and payment scenarios to areas such as on-chain lending, and are making early preparations for the future stablecoin business needs of banks.

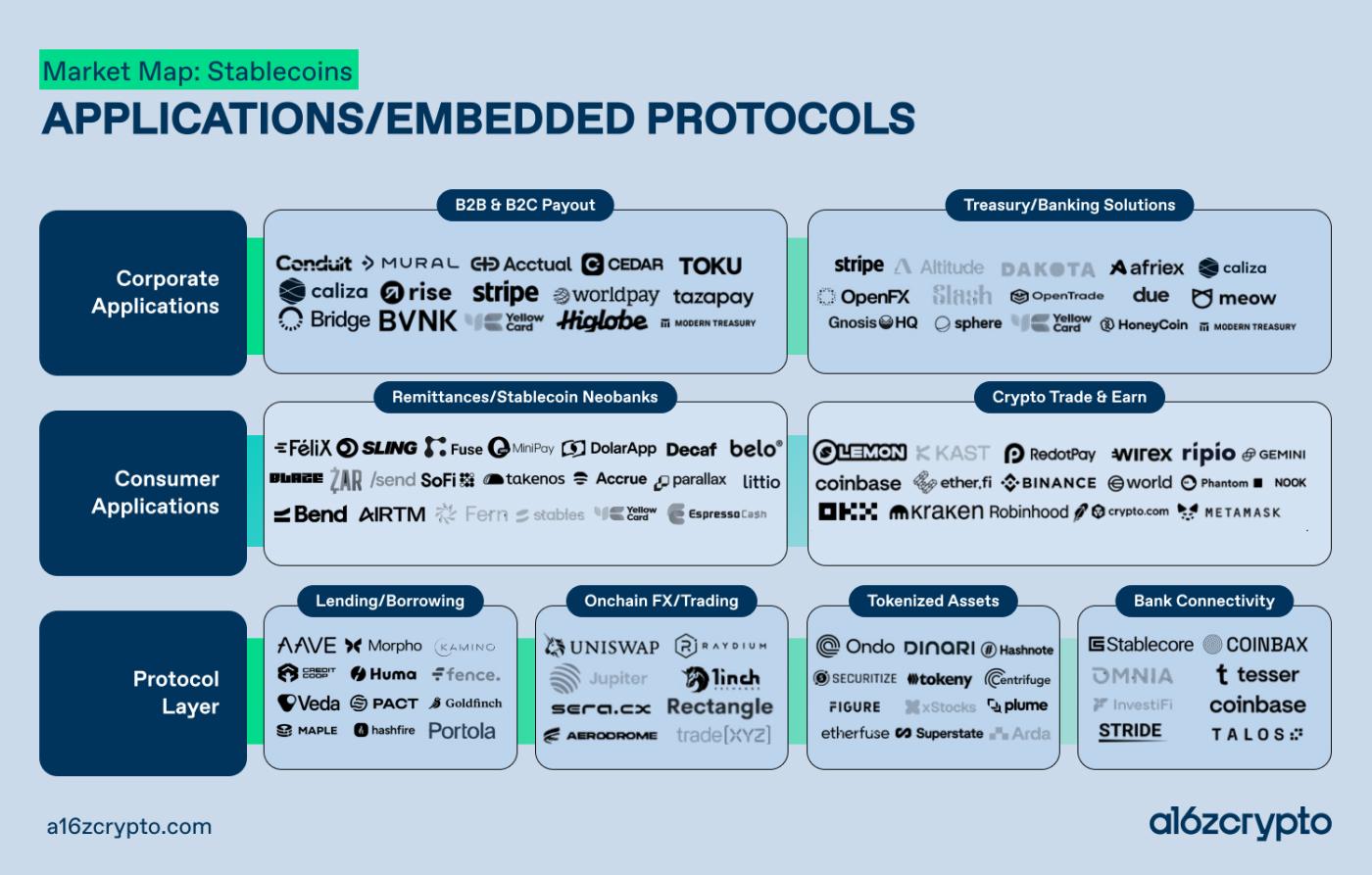

Application Layer: New Financial Functions Deployed

Two major trends are reshaping the terminal application ecosystem.

The first trend is the convergence of fintech new banks and crypto wallets.

Exchanges are adding features such as virtual accounts, payment cards, and reward programs; internet banks are accelerating the integration of crypto assets with traditional wealth management products. The boundaries between the two types of products are rapidly blurring, ultimately forming a unified comprehensive financial platform that serves both native crypto users and general users through a single interface.

The ultimate winners of this competition will not necessarily be the companies with the best products, but rather those that can combine distribution channels and customer trust with products and services that meet customer needs.

The second trend is the application of stablecoins in corporate banking. In markets where dollar banking infrastructure is limited, unreliable, or too costly (such as most of Latin America, sub-Saharan Africa, and Southeast Asia), stablecoins provide businesses with unprecedented dollar settlement channels, covering essential scenarios such as supplier payments, global collections, and cash pooling management.

The core of this demand is not related to the concept of the crypto space, but rather to the efficient accessibility of dollar assets. Given the weak local financial system and volatile currency, businesses are proactively embracing stablecoins due to practical operational needs.

The more critical long-term changes at the application layer stem from the value-added ecosystem built upon basic account services.

The introduction of dollar assets is just the beginning. Whether you are a micro-business owner in Lagos, a freelancer in Buenos Aires, or a savings user in Jakarta, as long as you hold stable, stablecoin-denominated assets, you can access a full range of financial services that were previously difficult to access: credit, investment, wealth management, insurance, and more.

Internet banks and super apps that take the lead in securing user account access will leverage their customer base to cross-sell a full range of financial products, covering the vast, underserved markets long neglected by the traditional financial system. Payment is merely the entry point for opening an account; credit and investment are the core carriers of commercial value.

Credit Markets: Profound Subprime Changes

If payment is the first step, then credit is likely the second step, and perhaps even the more important one.

The market's general interpretation of stablecoin growth is often limited to a large-scale, narrow banking model: dollar tokenization, wallet storage, instant settlement, and on-demand redemption. However, this perspective overlooks the core changes that will occur after stablecoins become widely adopted: when trillions of dollars worth of stablecoins circulate in the market, the investment demand for idle capital will explode. Companies holding stablecoins will need to activate their idle funds, various protocols will need liquidity replenishment, and end users will eventually generate borrowing needs.

A completely new on-chain lending market will inevitably emerge. This is not the lending product with strong speculative attributes based on crypto assets as seen in the early decentralized finance cycle, but rather a real-world lending system that returns to the essence of banking: facilitating capital formation, providing lending based on real assets and accounts receivable, and offering operational funding support to enterprises in regions lacking local banking infrastructure.

The early era of the rapid, unregulated growth of decentralized finance has come to an end, and the industry is entering a more stable and mature era of on-chain finance.

This evolutionary logic is highly similar to the development of the private lending industry over the past decade. Under regulatory pressure, traditional banks gradually scaled back some of their lending businesses, while private lending funds rapidly filled the market gap, growing from a niche alternative asset to a core sector with a scale of trillions of dollars, directly comparable to syndicated loans. The underlying logic of on-chain lending is the same: accumulating capital outside the traditional banking system and serving borrowers neglected by traditional finance with a completely new architecture. The core difference lies in the fact that on-chain financial infrastructure possesses inherent attributes of openness, programmability, and globalization—advantages that private lending cannot match.

Traditional lending institutions have begun to closely monitor changes in the industry, and those that have made early arrangements and completed mergers and acquisitions will dominate the future development of the on-chain capital market.

Dollar Hegemony and Geopolitics

Behind this market map lies a story bigger than fintech, and this story has two directions.

For individuals and businesses, the new financial system brings tangible economic empowerment: effectively mitigating the risk of local currency devaluation, accessing globally accepted payment channels, and conducting business using the most liquid currency in the world, the US dollar. Farmers in sub-Saharan Africa, manufacturers in Southeast Asia, and small importers in Latin America can independently hold, trade, and save US dollars without opening US bank accounts or relying on the traditional correspondent banking system, completely breaking down the privileged barriers of past dollar services.

For the United States, stablecoins further strengthen its existing financial hegemony. For the past century, the dollar's dominance has been maintained through the International Monetary Fund, the World Bank, the global correspondent banking system, and a network of bilateral agreements, allowing the US Treasury and the Federal Reserve to wield global financial power. Stablecoins, however, open up a more direct and entirely new channel: every wallet holding a dollar-denominated stablecoin is a new node in the dollar financial network, enabling low-cost, near-instantaneous value settlement between any two points globally. The higher the adoption rate of stablecoins, the stronger the network effect, and the deeper the dollar's penetration will continue to deepen in financially vulnerable regions.

This is the most profound strategic value of stablecoins: the implementation of regulations represented by the GENIUS Act is not simply about controlling a new type of financial product, but rather a strategic layout by the United States to consolidate the core position of the US dollar in the long term, relying on stablecoin infrastructure, against the backdrop of the continuous challenges to the dollar's hegemony since the Bretton Woods system.

Beyond Payments: Reconstructing the Underlying Global Financial System

The new underlying architecture of global finance is still under construction, and its strategic value extends far beyond the payment sector.

This transformation is essentially a comprehensive upgrade of the global financial system. The new on-chain underlying network is open, programmable, and inherently interconnected, capable of covering regions, populations, and scenarios where traditional systems have never been adapted. Its core value includes:

- To provide stable US dollar services to regions with underdeveloped financial infrastructure;

- Create a stable channel for the appreciation of massive amounts of idle capital;

- To provide inclusive credit services to groups neglected by traditional finance;

- It will help billions of ordinary people participate in the global capital market without barriers for the first time.

Today, companies that are deeply involved in all aspects of this new financial industry chain will define the global financial landscape of the next era and dominate the future form of the global dollar economy.