Overall, the combination of the leadership transition in monetary policy in May and macroeconomic data will determine whether the crypto market can maintain its strong momentum from April and break through to above $80,000.

Article author and source: BitMart

TL, DR

- The FOMC held rates steady in April, but the change of chairman introduced policy uncertainty. Inflation rose due to the oil price shock, while a recovery in employment supported the economy, and US stocks rebounded overall as risk appetite improved. In May, the market will focus on the policy signals from the new chairman, inflation, and oil price trends. Meanwhile, the momentum in the cryptocurrency market and legislative progress will also be key variables.

- The cryptocurrency market in April exhibited a "low opening - increased volume - high-level consolidation" structure, with multiple volume surges driven by the ceasefire news and maintaining healthy volume throughout the price increase. Total market capitalization rose from approximately $2.43 trillion to $2.70 trillion, reversing its initial decline at the beginning of the month and trending upwards under the catalyst of the ceasefire. Compared to the pressure and consolidation in March, April saw a structural improvement with "market capitalization breakthrough and subsequent volume increase," indicating a significant upward shift in the market's center of gravity.

- In April, both BTC and ETH spot ETFs saw significant net inflows, driving prices up in tandem. The BTC ETF's size surpassed $100 billion for the first time, marking a new phase in institutional allocation. Overall, the market exhibited a "price-led, fund-following" characteristic, with institutional funds still clearly favoring BTC over ETH. Meanwhile, stablecoin supply saw moderate growth, but structural divergence intensified, with USDT dominating expansion while USDe contracted sharply, reflecting a rebalancing of funds between returns and risks.

- BTC recorded its strongest monthly performance this year in April, rebounding strongly driven by easing geopolitical tensions but still constrained by the key resistance level of $80,000. ETH's movement was largely in sync with BTC, rebounding supported by institutional demand and upgrade expectations, but still facing resistance at $2,400 in the short term. SOL, while following the market recovery, performed weakly, dragged down by ecosystem security incidents; its future success hinges on restoring confidence and breaking through the $90 resistance level.

- The US-Iran ceasefire eased geopolitical risks and fueled a strong Bitcoin rebound, with a gain of approximately 13% in April, leading to a significant inflow of funds into the overall crypto market capitalization and ETFs. Meanwhile, attacks on Drift and KelpDAO resulted in over $600 million in losses for DeFi and triggered a large-scale capital outflow, exposing the systemic risks of oracles and cross-chain architectures. On the policy front, the CLARITY Act made key progress and significantly increased its likelihood of passage this year, marking an accelerated formation of a regulatory framework for the crypto market.

- The core market focus in May was on Warsh's first time chairing the FOMC and changes in policy signals, coupled with inflation and oil price trends, which will directly impact whether risk assets and BTC can maintain their strength. Meanwhile, the CLARITY Act entered the Senate vote stage; if passed, it will significantly boost institutional investment and reshape the crypto regulatory landscape. The advancement of Asia-Pacific regulation, along with the acceleration of corporate BTC reserves and RWA tokenization, constitute important drivers of medium- to long-term capital inflows and industry development.

1. Macro perspective

Policy direction

The FOMC held its third policy meeting of the year on April 28-29, and the market expected the federal funds target rate to remain unchanged at 3.50%–3.75%. This meeting did not include an update to the dot plot, so every word was highly interpreted by the market. This was also the last FOMC meeting chaired by Federal Reserve Chairman Jerome Powell—his term officially expires on May 15. His nominee, Kevin Warsh, completed his Senate Banking Committee hearings on April 21, and on April 26, the last key obstacle, Senator Tillis, withdrew his opposition, confirming the vote to proceed to the final stage. The market was widely focused on whether Powell would provide forward guidance on the future policy path at his final press conference, and whether there would be a shift in monetary policy signals after Warsh took over. Overall, the April FOMC meeting did not bring any policy surprises based on the "maintain unchanged" fundamentals, but the uncertainty premium introduced by the personnel transition will extend into May.

US stock market trend

US stocks generally showed a recovery trend, initially declining before rebounding, driven primarily by easing geopolitical tensions. In late March, the S&P 500 remained under pressure due to high oil prices and inflation concerns from the previous month. On April 8th, the US-Iran ceasefire agreement was finalized, and shipping in the Strait of Hormuz partially resumed, leading to a rapid recovery in market risk appetite. The technology sector and consumer discretionary led the gains, and the S&P 500 rebounded sharply in the days following the ceasefire. On April 10th, the March CPI jumped sharply to 3.3%, triggering a brief correction, but the market quickly digested this, characterizing it as a supply-side shock rather than demand-side inflation. The Q1 earnings season became the core driver in mid-to-late April, with the S&P 500 recording positive returns for four consecutive weeks and reaching a new high on April 24th. Earnings from major technology companies generally exceeded expectations, and continued expansion of AI capital expenditure further boosted sentiment. Overall, the S&P 500 recorded a positive monthly return in April, and the VIX fear index fell from a high of 31.65 at the beginning of the month to around 18.5 at the end, indicating a significant improvement in market sentiment.

Inflation data

The U.S. Bureau of Labor Statistics released March 2026 CPI data on April 10: The CPI rose 3.3% year-on-year, a significant increase of 0.9 percentage points from February's 2.4%, and 0.9% month-on-month, the largest monthly increase since 2022; core CPI (excluding food and energy) rose 0.2% month-on-month and approximately 2.6% year-on-year, relatively moderate. The main driver of the sharp jump in inflation was the surge in energy prices caused by the Iran war—gasoline prices rose 21.2% in March alone, the largest monthly increase since 1967, pushing up the overall energy component significantly; the transmission effect of tariffs is also beginning to appear in imported goods categories. The mainstream market interpretation of this data is a supply-side shock rather than demand-side inflation. The relatively controllable core CPI suggests the Federal Reserve is unlikely to change its policy path, but if the Iran conflict continues and oil prices remain high, the risk of a secondary transmission of inflationary pressure to the core component cannot be ignored.

Employment data

The U.S. Department of Labor released its March 2026 nonfarm payrolls report on April 3: nonfarm payrolls increased by 178,000, significantly better than the market expectation of 59,000, and a significant recovery from the revised -133,000 in February (initial value -92,000); the unemployment rate slightly decreased from 4.4% to 4.3%, and the labor force participation rate slightly declined to 61.9%. The main contributors to the employment recovery were the healthcare industry (+76,000, mainly due to healthcare workers returning to work after the strike), construction, and transportation and warehousing. Average hourly wages increased by 3.5% year-on-year and 0.2% month-on-month, with moderate wage inflation pressure. Overall, the March employment data alleviated previous market concerns about a rapid deterioration in the labor market, providing new support for the "soft landing" narrative and easing some of the pressure on the FOMC to cut interest rates quickly; however, the decline in the labor force participation rate indicates that the employment improvement is partly due to labor leaving the market, and the deeper resilience of the labor market remains to be seen.

Political factors

The political factors influencing cryptocurrency and macroeconomic market sentiment are primarily centered on the US-Iran geopolitical situation. On April 8, the US and Iran announced a temporary ceasefire agreement mediated by Pakistan, and shipping in the Strait of Hormuz gradually resumed some operations. Brent crude oil prices fell sharply from their peak of nearly $120/barrel since the outbreak of the war, with WTI crude oil experiencing a single-day drop of over 16% on the day of the ceasefire. However, this was short-lived, as ceasefire negotiations progressed slowly. In late April, the Iranian Foreign Minister reiterated Iran's stance of control, and Brent crude oil prices rebounded to the $107-108/barrel range on April 26-27. The continued fragility of the ceasefire poses a tail risk, and the market is concerned that if the Strait of Hormuz remains blocked until the end of June, Brent crude oil could potentially hit $150. In the cryptocurrency sector, the Senate Banking Committee marked the "CLARITY Act" before the April 25 deadline, and substantial disagreements were resolved through the Tillis-Alsobrooks stablecoin yield compromise, significantly increasing expectations for the legislation's implementation by the end of the month. The uncertainty surrounding Powell's impending departure and Warsh's succession to the presidency became a significant new variable of market attention at the end of April. Overall, the ceasefire was the most important positive catalyst, but the rebound in oil prices and the uncertainty surrounding the policy transition were the main negative variables.

Outlook for next month

Looking ahead to May, Kevin Warsh will chair the FOMC meeting for the first time as Federal Reserve Chairman on May 6-7 (Politico Powell officially steps down on May 15). The market will be extremely sensitive to the wording of the statement and the policy signals from Warsh's press conference—any significant deviation from Powell's wording could trigger significant volatility in risk assets. April CPI and PCE data will be released in May, and whether the March oil price shock triggered a second wave of core inflation is a key observation point; if the core component remains moderate (month-on-month ≤0.2%), expectations for interest rate cuts will stabilize. After being marked by the Banking Committee in April, the CLARITY Act will enter the Senate vote preparation phase in May, with Senator Moreno setting a late May deadline for passage, making the legislative timeline highly competitive. Regarding crypto assets, whether BTC can effectively break through the key $80,000 level and whether ETF inflows can remain positive are important indicators for judging whether the bullish momentum of April can continue into May; the direction of US-Iran negotiations and whether oil prices can fall below $100 will be the core macroeconomic variables determining whether market risk appetite can further expand.

2. Overview of the Crypto Market

Currency data analysis

Trading volume & daily growth rate

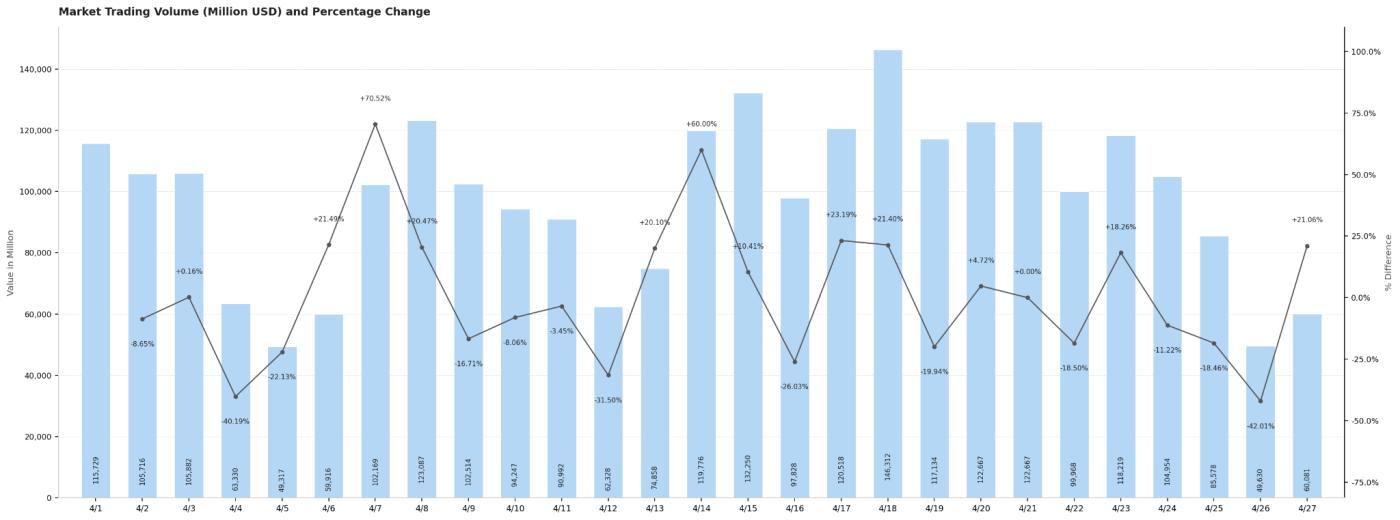

The overall daily trading volume in the cryptocurrency market in April was approximately $98 billion, exhibiting a volatile structure of "low opening – increased volume – high-level fluctuations" throughout the month. Trading volume was approximately $115.7 billion on April 1st, subsequently declining due to the weekend effect, reaching monthly lows on April 4th and 5th ($63.3 billion and $49.3 billion respectively), marking the lowest level for the month. Trading volume recovered rapidly after the start of the work week, surging 70.52% on April 7th to approximately $102.2 billion. The news of the US-Iran ceasefire on April 8th further boosted trading volume to approximately $123.1 billion, indicating a significant improvement in market sentiment. From April 14th to 15th, as the market continued to rise, trading volume remained high for two consecutive days ($119.8 billion and $132.3 billion respectively). April 18th reached the monthly peak of approximately $146.3 billion, the most active trading day of the month, coinciding with a new high in the cryptocurrency market capitalization, demonstrating a significant resonance between volume and price. At the end of the month, on April 25-26, trading volume fell again to low levels due to the weekend (approximately $85.6 billion and $49.6 billion respectively), before slightly rebounding to $60.1 billion on April 27 to close the month. Overall, weekday trading volume generally remained in the range of $90 billion to $130 billion, while weekend volume predictably shrank to $50 billion to $65 billion. Market activity showed a phased upward trend as prices rose, and the volume structure was healthy.

Total market capitalization & daily growth

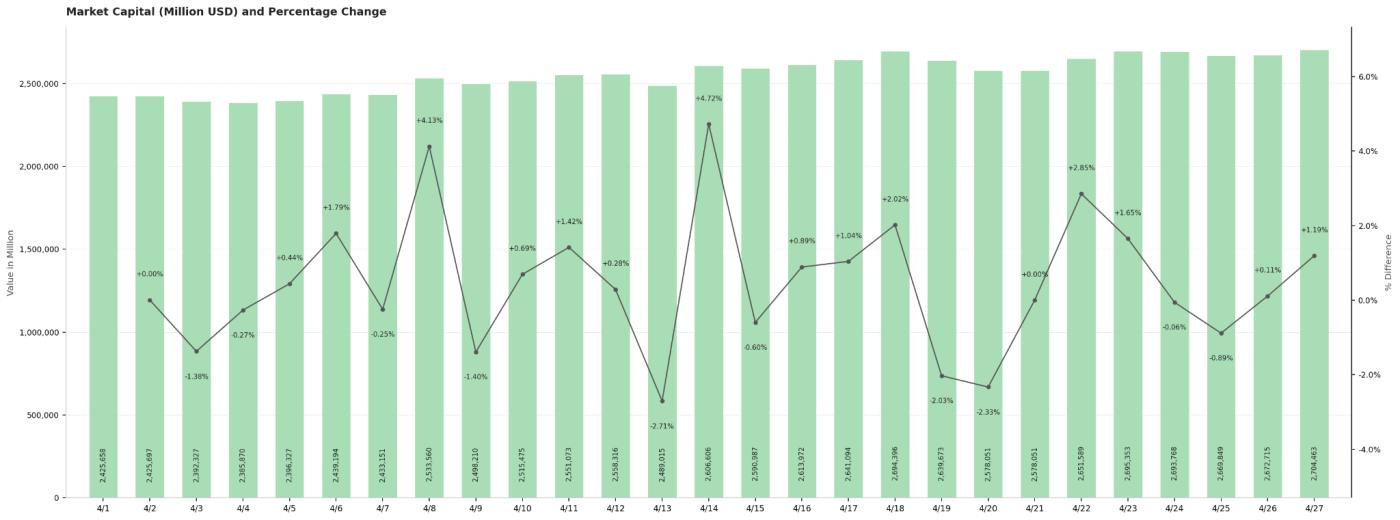

The total market capitalization of the cryptocurrency market steadily climbed from approximately $2.43 trillion at the beginning of April to approximately $2.70 trillion at the end of the month, a monthly increase of about 11.5%. The month's trend exhibited a clear three-stage structure: an initial drop to a bottom, a ceasefire reversal, and a volatile upward trend. From the beginning of the month to April 5th, dragged down by high oil prices and inflationary pressures, the market capitalization slightly declined to approximately $2.39 trillion (the low point of the month). The signing of the US-Iran ceasefire agreement on April 8th became the most important turning point of the month, with a single-day surge of 4.12% in market capitalization, breaking through the $2.53 trillion mark and signifying a substantial recovery in market risk appetite. Subsequently, the market capitalization entered a volatile upward channel. On April 14th, driven by continuous capital inflows, it rose another 4.73% in a single day, reaching a high of approximately $2.69 trillion on April 18th. At the end of the month, from April 22nd to 23rd, the market capitalization further strengthened to around $2.70 trillion, closing at $2.70 trillion on the last trading day of April, the highest closing price for the month. It is worth noting that the largest single-day pullback of the month (-2.72%) occurred on April 13, corresponding to the short-term panic triggered by the KelpDAO security incident. However, the market quickly digested the shock and continued to rise, demonstrating the resilience and dominance of the bulls in this round of market activity.

Comparison with March data

Compared to March, the cryptocurrency market showed significant improvement in both market capitalization and trading volume in April. In terms of market capitalization, March was suppressed by both hawkish signals from the FOMC and high oil prices, with the total market capitalization fluctuating widely between $2.3 trillion and $2.6 trillion without forming a significant breakthrough. In April, however, the market completed a structural rise catalyzed by the US-Iran ceasefire, steadily climbing from $2.43 trillion at the beginning of the month to $2.70 trillion, an increase of about 11.5% within the month. The upper limit of the range expanded by about $100 billion compared to March, and the market center of gravity shifted northward overall. In terms of trading volume, the average daily trading volume in March was approximately $80 billion to $100 billion, indicating low volume and a strong wait-and-see attitude among investors. In April, the average daily trading volume remained at approximately $98 billion, roughly the same as the March average. However, there were several periods of high activity during the month with single-day volume exceeding $120 billion (April 8th, April 14-15th, and April 18th), especially the peak of approximately $146.3 billion on April 18th, far exceeding any single-day level in March, demonstrating a price-volume resonance structure that amplified in tandem with rising prices. Overall, March was a consolidation pattern of "market capitalization under pressure and shrinking volume," while April achieved a structural shift of "market capitalization breakthrough and subsequent volume increase," creating a stark contrast between the two.

Popular tokens in April

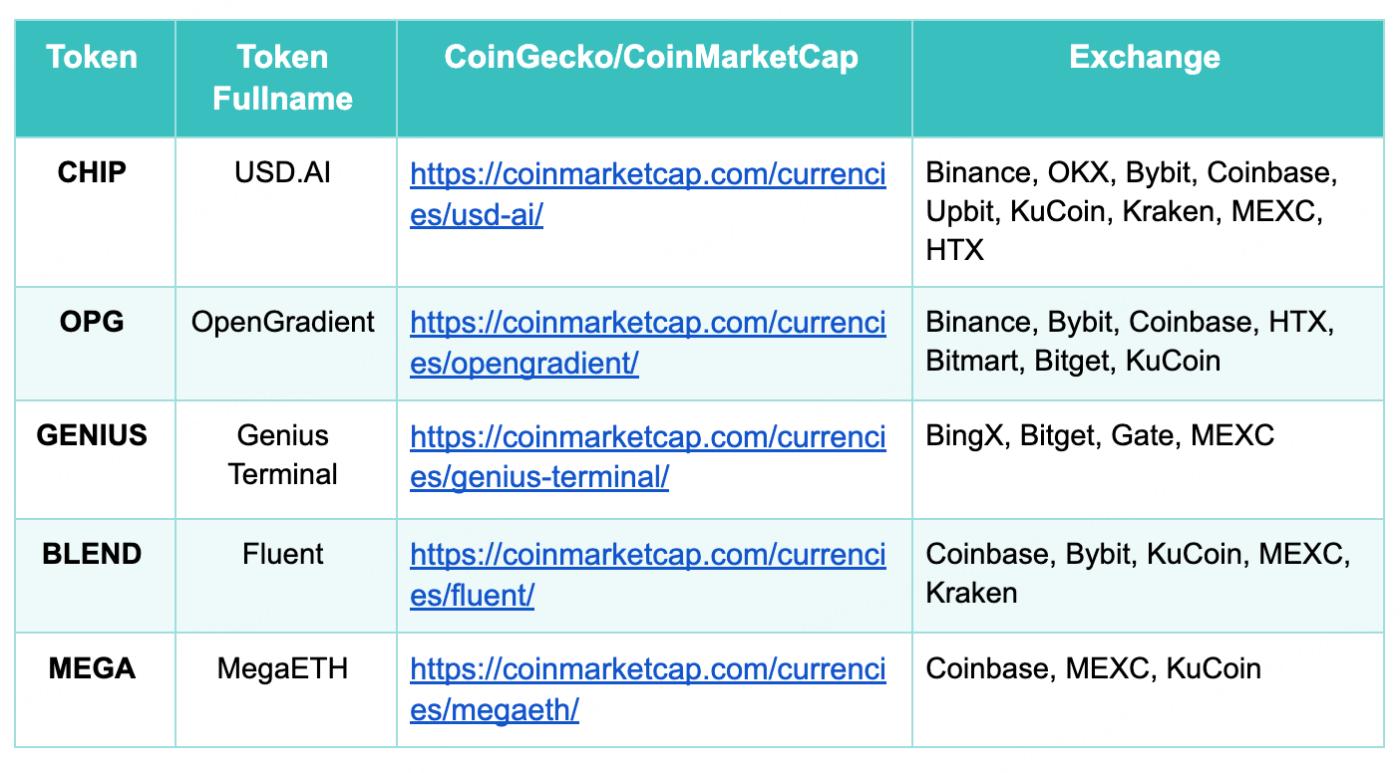

In April 2026, the cryptocurrency market saw several highly anticipated coin launches, exhibiting strong overall performance. In terms of launch volume, CHIP (USD.AI) and OPG (OpenGradient) achieved first-day trading volumes exceeding $1.4 billion and $1 billion respectively, setting new liquidity records for April and indicating a simultaneous influx of institutional and retail funds. GENIUS (Genius Terminal) launched first on April 13th, and thanks to the backing of YZi Labs' multi-billion dollar investment and the market effect of CZ serving as an advisor, its price surged over 65 times on its first day, with a 24-hour trading volume reaching $1.1 billion, rivaling the popularity of the former two.

From a sector perspective, the three leading projects cover AI lending infrastructure (CHIP), decentralized AI inference networks (OPG), and on-chain transaction terminals (GENIUS), respectively, all highly aligned with the AI narrative, confirming the market's continued enthusiasm for the AI+Web3 direction. BLEND (Fluent Network) and MEGA (MegaETH), as new Ethereum Layer 2 projects, completed their TGEs on April 24th and April 30th respectively, with relatively moderate trading volumes, but Coinbase's endorsement provided strong compliance credibility. Overall, the focus of new coin launches in April was concentrated on two main themes: AI infrastructure and Ethereum scaling. Leading projects enjoyed ample liquidity on their first day and widespread exchange coverage, reflecting the market's continued strong capacity to absorb high-quality new projects.

3. On-chain data analysis

Analysis of BTC and ETH ETF inflows and outflows

In April, both BTC and ETH spot ETFs continued to see net inflows, indicating a significant rebound in institutional allocation intentions. The total net inflow into BTC spot ETFs reached $8.44 billion, pushing total net assets up significantly from $89.9 billion at the end of March to $101.2 billion, a month-on-month increase of 12.8%, breaking the $100 billion mark for the first time and setting a new historical high. BTC's opening price rose from $67,842 to $78,661 during the same period, a monthly increase of 15.9%, marking its strongest monthly performance in the past year. ETH spot ETFs also recorded a monthly net inflow of $1.75 billion, with total net assets rising from $12.2 billion to $13.5 billion (+10.7%). The price of ETH rose from $2,052 to $2,369 (+15.4%), with the increase largely in sync with BTC.

Structurally, the net asset value (NAV) increase of the BTC ETF (+12.8%) was slightly lower than the price increase (+15.9%), indicating that price increases contributed the majority to the expansion of AUM, while the contribution of net capital inflows was relatively moderate—consistent with the overall market rhythm of "price leading the rise, followed by capital inflows" in April. Regarding ETH, the NAV increase (+10.7%) was also slightly lower than the price increase (+15.4%), but the size of the ETH ETF is still only about 13% of that of the BTC ETF, indicating a significant divergence in institutional fund allocation between the two asset classes. Overall, the BTC ETF's total NAV exceeding $100 billion is the most significant milestone of this period, marking a new stage in Bitcoin's mainstream adoption as an institutional asset.

Stablecoin Inflow and Outflow Analysis

In April, the total circulating supply of the six major stablecoins expanded slightly from $283.6 billion in March to $288.4 billion, a month-on-month increase of 1.7%, continuing the overall moderate growth trend, but the internal structural differentiation intensified significantly.

In terms of incremental growth, USDT was the primary driver of expansion this period, with its circulating supply increasing from $184.1 billion to $190 billion (+3.2%), a net increase of approximately $5.9 billion, accounting for over 90% of the total increase. This further solidifies its dominant position in on-chain settlement and trading scenarios. DAI saw a slight increase of 2.3% to $4.7 billion during the same period, reflecting a moderate recovery in demand for decentralized stablecoins amid a market rebound.

In terms of trading volume, USDe saw the largest decline among stablecoins this period, with its circulating supply plummeting from $57.5 billion to $35.8 billion, a reduction of approximately $21.7 billion within the month, representing a drop of 37.7%. The significant decrease in USDe's value was primarily due to the impact of ETH futures basis compression on the Ethena protocol's yield, which significantly reduced its attractiveness, leading to substantial redemptions and exits. PYUSD also declined by 15.6% during the same period, with its circulating supply shrinking to $3.4 billion, indicating that PayPal's stablecoin still faces considerable pressure in expanding its on-chain application scenarios. USDC and USD1 saw slight decreases of 1.1% and 0.7% respectively, remaining relatively stable overall. Notably, USYC entered the market in April as a new member, with a circulating supply of approximately $2.6 billion, adding a significant player to the stablecoin market for yield-generating government bonds.

4. Price Analysis of Major Currencies

Bitcoin (BTC) Price Analysis

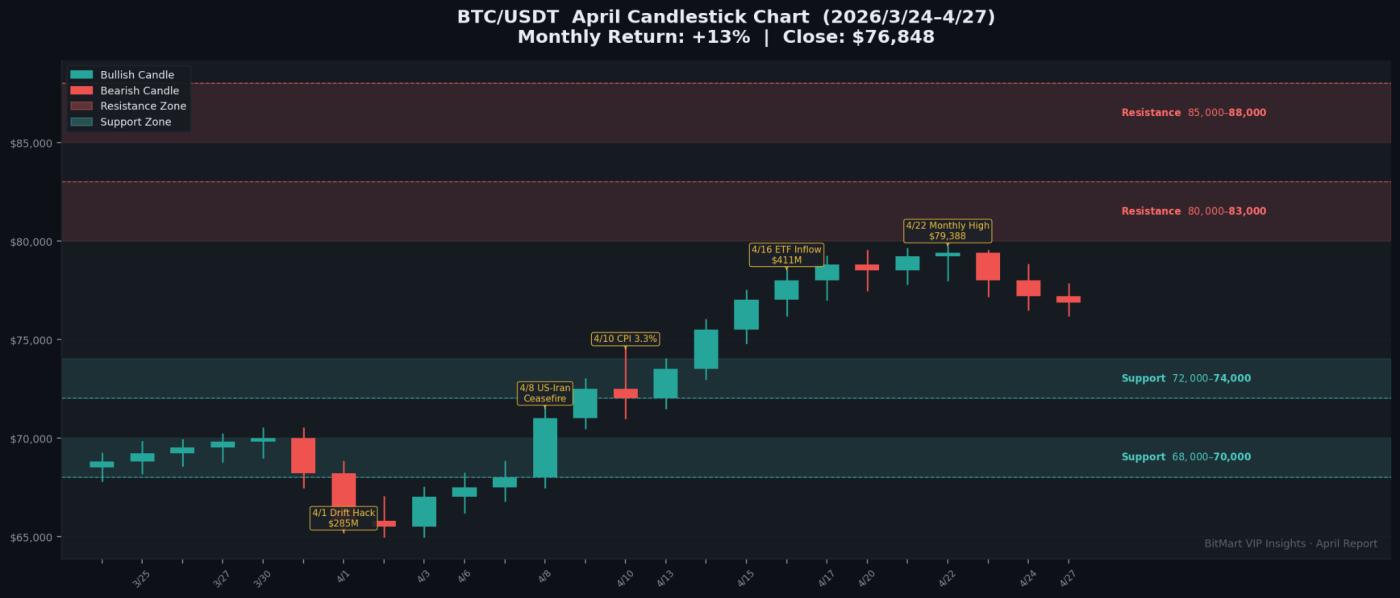

In April, Bitcoin recorded its strongest monthly performance in the past year, with a monthly increase of approximately 13%. Starting from around $68,000–$69,000 at the end of March, BTC briefly fell to a monthly low of around $65,000 at the beginning of the month due to the sharp jump in March's CPI (3.3%) and high oil prices. After the US-Iran ceasefire was announced on April 8th, risk appetite quickly recovered, and BTC rebounded strongly within days, breaking through $70,000 and continuing to climb to the $75,000–$79,000 range. On April 22-23, BTC briefly touched around $79,388, approaching the key $80,000 level but failed to break through effectively, subsequently falling slightly to around $76,848 (as of April 27th). From a technical perspective, $80,000–$83,000 is the key resistance zone in the near term; a break above this level would open up further upside potential towards $85,000–$88,000. On the downside, the first support level to watch is $72,000–$74,000; a break below this level could lead to a test of the mid-term support level of $68,000–$70,000. Overall, BTC completed a structural shift from range-bound trading to a strong rebound in April, but a break above $80,000 is still pending. Future price movements will depend on FOMC policy signals and the evolution of macroeconomic risk appetite.

Ethereum (ETH) Price Analysis

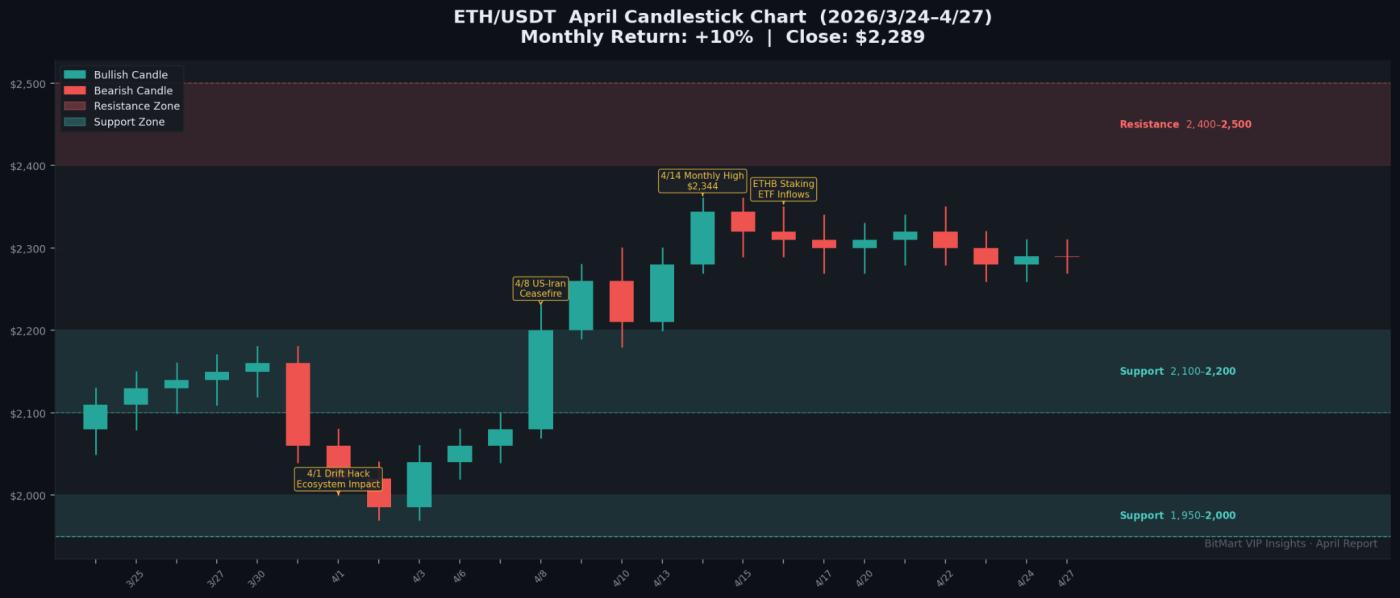

In April (March 24 to April 27), Ethereum's price recorded a significant increase along with the overall market recovery, performing largely in sync with BTC. Starting from around $2,050-$2,100 at the end of March, ETH was initially dragged down by inflation data and high oil prices, seeking support in the $1,950-$2,050 range. After the US-Iran ceasefire, it rebounded sharply in tandem with BTC, reaching a monthly high of around $2,344 in mid-April. As of April 27, it was trading at approximately $2,289, representing a monthly increase of about 10%. Technically, $2,400-$2,500 is a key resistance zone in the near term, requiring a significant increase in trading volume to break through. Below, $2,100-$2,200 is a key support level; a break below this level could lead to a retest of the $1,950-$2,000 medium-term support. The continued expansion of ETHB (BlackRock ETH Staking ETF) has provided additional institutional demand support for ETH. Coupled with the expectation of Glamsterdam upgrade, ETH's medium-term fundamentals have improved compared to March. However, whether it can break through the $2,400 resistance zone in the short term remains a key test.

Solana (SOL) Price Analysis

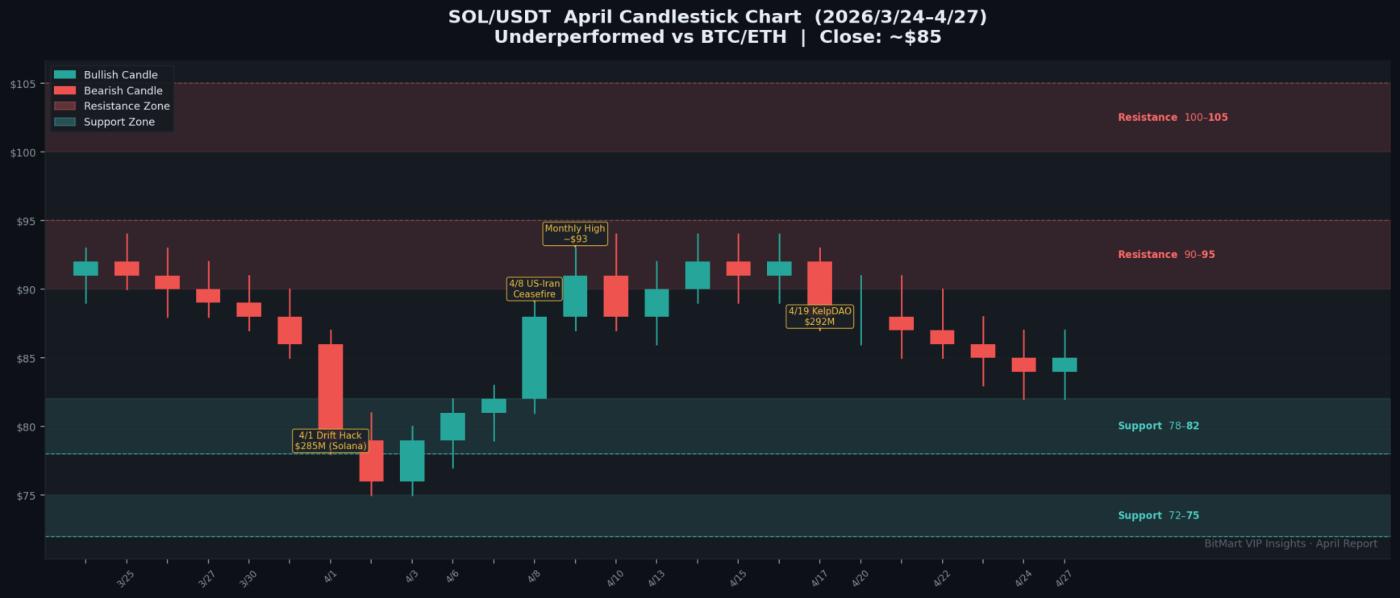

In April (March 24 to April 27), Solana's price rebounded moderately along with the overall market recovery, but its performance was relatively weaker than BTC and ETH. SOL started at around $89-$92 at the end of March, falling to a monthly low of around $75-$78 at the beginning of the month during a period of overall market pressure. After the ceasefire, it rebounded to the $85-$90 range, and as of April 27, it was trading at around $84-$86, with relatively limited monthly gains. The $285M hack of Drift Protocol on April 1 had a temporary negative impact on confidence in the Solana ecosystem, with some DeFi liquidity withdrawing from the Solana chain, temporarily limiting the strength of SOL's rebound. Technically, key resistance is concentrated in the $90-$95 range; a successful break and hold above this level is needed to initiate a recovery towards $100 or higher. On the downside, $78-$82 is a significant support level; a break below this level could test the mid-term support of $72-$75. Overall, SOL exhibited characteristics of "following the market rebound but with relatively weak strength" in April. The recovery of ecosystem confidence following the Drift attack and the breakthrough of the $90 resistance level are key signals for judging the next stage of SOL's trend.

5. Hot Topics This Month

With the US-Iran ceasefire in place, Bitcoin surged 13% in the month, marking its strongest monthly gain in a year.

On April 8th, with Pakistan's mediation, the United States and Iran reached a temporary ceasefire agreement regarding a potential war in 2026. The blockade of the Strait of Hormuz began to ease, and global Brent crude oil prices quickly fell from a peak of over $113/barrel to the $105-$107 range. The ceasefire became the most important single macroeconomic catalyst for the crypto market in April: Bitcoin rebounded strongly from its early April low of around $65,000, accumulating a gain of over $10,000 within a week of the ceasefire, breaking through $75,000 and continuing to approach $79,000. BTC's cumulative gain in April was approximately 13%, its strongest monthly performance since March 2025. The total market capitalization of the global crypto market rebounded from approximately $2.3 trillion to over $2.7 trillion, and BTC spot ETFs recorded large net inflows for several consecutive days after the ceasefire, with a single-day net inflow of approximately $410 million on April 16th.

On April 21, Trump announced an extension of the ceasefire until the negotiations concluded, but progress in the Islamabad talks has been slow, with neither side softening their stance on core issues. The fragility of the ceasefire continues to suppress the market's ability to completely rule out geopolitical risks. Analysts point out that Bitcoin's "risk appetite recovery asset" attribute, exhibited when geopolitical risks ease, reinforces its increasingly mature role in institutional allocation, demonstrating the further enhancement of the status of crypto assets in the global macro trading framework. If the ceasefire breaks down, a second surge in oil prices will quickly suppress the market again; if the negotiations make substantial progress, expectations of declining inflation will provide additional support for risk assets, and BTC is expected to challenge the $80,000 level.

Drift and KelpDAO attacks combined to cause over $600 million in DeFi losses in April.

April became the most challenging month for DeFi security since 2026, with two major attacks causing over $600 million in losses within 18 days. On April 1st, Drift Protocol, the largest decentralized perpetual contract exchange in the Solana ecosystem, suffered an attack costing approximately $285 million: attackers created a fake token, CVT (CarbonVote Token), established a price history on Raydium with approximately $500 in seed liquidity, and manipulated trading to deceive oracles into amplifying the value of the fake collateral, ultimately withdrawing approximately $285 million. On April 19th, the Ethereum liquid staking protocol KelpDAO (rsETH) suffered an even larger attack, losing approximately $292 million, becoming the largest single DeFi attack in 2026—the root cause being a misconfiguration of cross-chain verification based on LayerZero, allowing hackers to commit fraud at the cross-chain messaging layer.

Both attacks, attributed to North Korea's Lazarus Group by security agencies, resulted in losses exceeding $600 million and triggered an outflow of approximately $13 billion from the DeFi ecosystem. Major lending protocols such as Aave quickly activated risk isolation and emergency response mechanisms. In late April, Volo Protocol suffered losses of approximately $3.5 million due to a vulnerability related to KelpDAO, further exacerbating market concerns about systemic risks in cross-chain infrastructure. These two attacks exposed two major structural weaknesses: vulnerabilities in oracle price manipulation protection and systemic risks inherent in modular cross-chain architectures lacking minimum security standards. The CFTC and SEC have announced a joint investigation, and the establishment of a DeFi security regulatory framework has been put on the agenda.

The Senate Banking Committee has marked the completion of the CLARITY Act, marking the final push for legislation this year.

In late April, the Clarity Act completed its marking process with the Senate Banking Committee, taking a crucial step towards a full Senate vote. The most closely watched aspect of the committee's deliberations, the stablecoin yield provisions, reached a basic compromise framework, allowing for market-based yield payments under certain compliance conditions, thus eliminating the biggest point of contention between the banking and crypto industries. Galaxy Digital, an analysis firm, pointed out that if the bill had not completed its marking by the committee by the end of April, its probability of passing this year would have been "extremely low"—this successful marking significantly increased Polymarket's prediction of its probability of passage this year from 72% to over 85%. The bill also clarifies the commodity/securities classification standards and market structure regulatory rules for digital assets, providing legislative confirmation for the SEC/CFTC joint classification interpretation on March 17.

The legislative progress of the CLARITY Act, in conjunction with the SEC/CFTC's joint digital goods classification on March 17, is building a top-down regulatory framework for the digital asset market. The three pillars—legal determination of commodity attributes (SEC/CFTC), market structure regulatory legislation (CLARITY Act), and stablecoin regulatory legislation (GENIUS Act)—are expected to be finalized by 2026, marking a historic milestone for digital assets as they enter the "era of mainstream financial compliance." If the Senate passes the bill in May, it is expected to unleash significant institutional demand and provide the strongest regulatory backing for compliant crypto financial products, including Bitcoin ETFs and Ethereum staking ETFs.

6. Outlook for next month

Warsh chairs FOMC for the first time; crypto markets are highly sensitive during monetary policy transition.

The most crucial macroeconomic variables in May are Kevin Warsh's appointment as Federal Reserve Chairman and the FOMC policy meeting on May 6-7. Warsh will chair the policy discussion for the first time as Chairman at this meeting, and the market will be extremely sensitive to the wording of the statement and the policy signals he sends during the press conference—any significant deviation from Powell's wording could trigger significant volatility in risk assets. If Warsh signals a continuation of the policy path, BTC is expected to remain above $75,000 and challenge $80,000; if his hawkish stance is reinforced through the press conference, coupled with the lingering effects of the March inflation shock, it could trigger a new round of adjustments in risk assets. April CPI and PCE data will be released in May, and whether the March oil price shock triggered a second wave of core inflation is a key observation point—if core inflation remains moderate (month-on-month ≤ 0.2%), expectations for interest rate cuts will stabilize; if core inflation jumps, interest rate cuts this year may be completely ruled out.

May will also see the release of revised Q1 GDP data and the end of the corporate earnings season. Capital expenditure trends in the AI sector will continue to determine the Nasdaq's trajectory, thus impacting the risk appetite environment in the crypto market. If the US-Iran ceasefire negotiations make substantial progress and oil prices further decline, it will provide strong support for cooling inflation and drive further expansion of risk assets. Conversely, if negotiations break down and oil prices surge again, the new Fed chairman will face severe inflationary pressures. Overall, the combination of the monetary policy leadership transition in May and macroeconomic data will determine whether the crypto market can maintain its strong momentum from April and break through to above $80,000.

The Senate vote on the Clarity Act: The most important regulatory legislation moment of this cycle.

After undergoing the Senate Banking Committee's marking process in April, the Digital Asset Market Clarity Act will officially enter the Senate's full vote preparation stage in May. Polymarket predicts that its probability of passing this year has risen to over 85%. The core significance of this bill lies in ending the years-long jurisdictional dispute between the SEC and CFTC over digital assets at the legislative level: tokens that meet the criteria for commodity status (including mainstream assets such as BTC, ETH, and SOL) will be explicitly regulated by the CFTC, while security tokens will be subject to SEC rules, ending the compliance arbitrage dilemma caused by the regulatory vacuum. The compromise on stablecoin yield terms allows for market-based returns under a specific compliance framework, which substantially enhances the institutional attractiveness of compliant stablecoins such as USDC and USDT—the competitive advantage of traditional money market funds will be partially weakened, and the penetration rate of stablecoins in corporate fund management and cross-border payment scenarios is expected to accelerate. If the bill passes smoothly in May, it is expected to trigger two major chain reactions: first, large traditional asset management institutions (pension funds, sovereign wealth funds) will accelerate the allocation of crypto asset ETFs after the compliance path is opened; second, compliant exchanges such as Coinbase and Kraken will rapidly expand the number of listed products and the scope of institutional services under a clear regulatory framework. If the vote is postponed due to partisan differences, market sentiment will face significant pressure in the short term. However, analysts generally believe that the legislative direction of the bill is irreversible, and the postponement is only a matter of time rather than a fundamental obstacle.

The Implementation of Hong Kong's Virtual Asset Regulation 2.0 and the Flow of Funds in the Asia-Pacific Region

The Hong Kong Securities and Futures Commission (SFC) is expected to complete legislation on the stablecoin issuer licensing framework in Q1 2026 and formally accept the first batch of stablecoin issuance license applications in May or June. Once the issuance mechanisms for Hong Kong dollar-backed stablecoins (HKD-backed) and compliant Hong Kong versions of USDC/USDT are clarified, they will provide institutional backing for Hong Kong to become an Asia-Pacific stablecoin settlement center. Meanwhile, following the initial launch of Hong Kong spot crypto ETFs (BTC+ETH) in 2025, May will see a concentrated release of Q1 size data. If net inflows continue to grow positively, coupled with the Japanese Financial Services Agency's cautious opening attitude towards crypto ETFs and Singapore's MAS further easing restrictions on institutional-grade crypto custody, the "second tier" effect of compliant Asia-Pacific funds entering the market will structurally complement the global crypto funding landscape, becoming an important observation dimension alongside US ETF fund flows.

The wave of corporate BTC reserves continues and RWA tokenization accelerates.

In April, MicroStrategy's holdings surpassed 530,000 BTC (approximately $40.8 billion), making it the world's largest publicly traded Bitcoin holder. In May, the market will continue to track whether MicroStrategy will continue to purchase more Bitcoin through convertible bonds or equity financing, as well as the movements of follower-type publicly traded companies such as MetaPlanet (Japan) and Semler Scientific. If the "corporate BTC treasury" trend expands to more Asian and European publicly traded companies, it will provide continuous structural incremental buying for BTC, further compressing the market's circulating supply. Meanwhile, BlackRock's BUIDL tokenized government bond fund exceeded $2 billion in Q1, and institutions such as Franklin Templeton and Ondo Finance continue to expand their on-chain RWA deployments. If new sovereign or publicly traded RWA products are launched in May, it will be a significant signal of accelerated integration between on-chain finance and traditional assets, potentially driving a significant increase in on-chain settlement demand for related public chains (especially Ethereum).