Crypto ETF rules have changed quickly since mid-2025, when U.S. regulators introduced generic listing standards that sped up approvals. The 85/15 framework builds on that system and adds another layer that is easy to misinterpret.

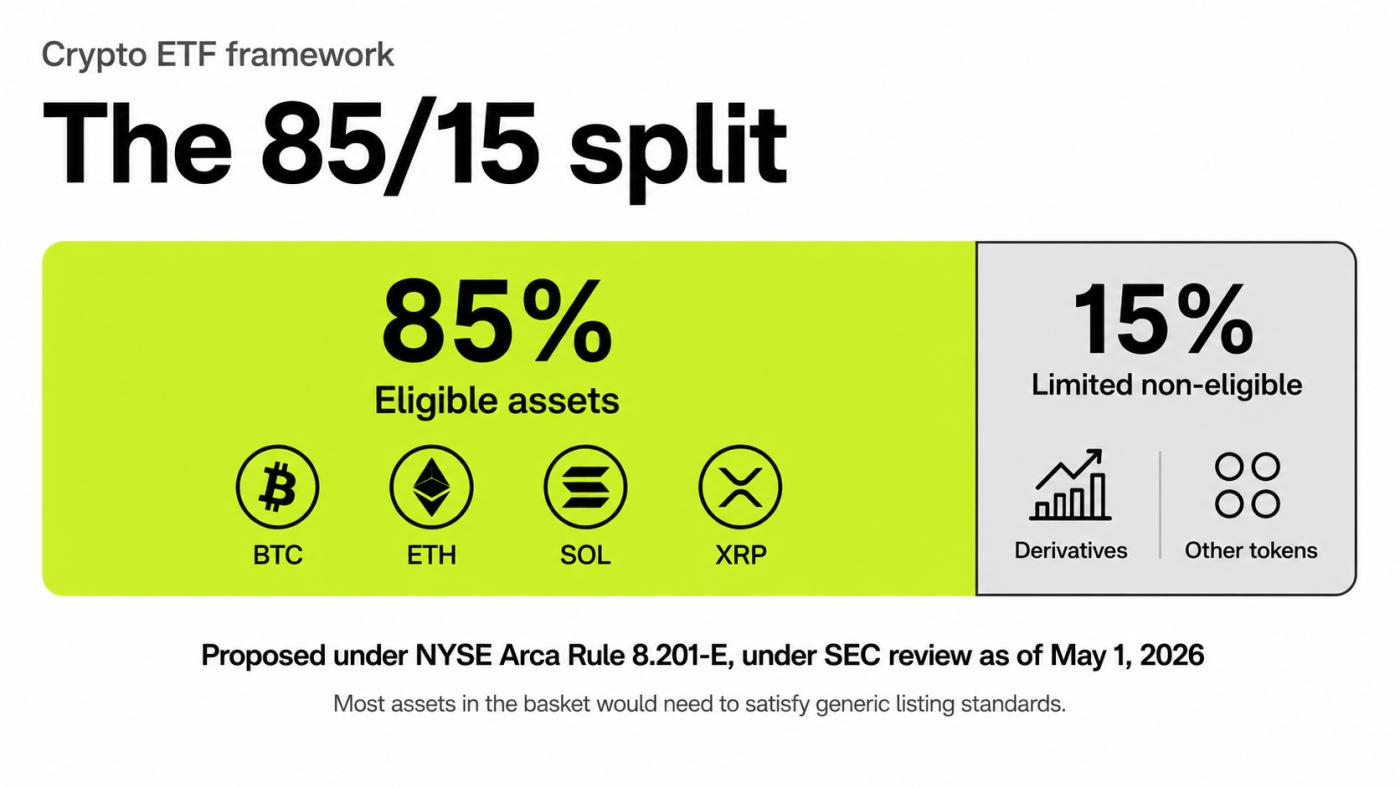

One of the latest developments comes from NYSE Arca, which has proposed a rule change that would let certain crypto trust products qualify if at least 85% of their assets meet existing standards. Bitcoin, Ethereum, Solana, and XRP appear in the filing’s examples, but the proposal does not approve any specific product. Also, this framework applies to U.S.-listed products and does not directly change ETF rules in other regions.

This guide explains what the framework does and does not do, and why multi-asset crypto funds may feel the biggest impact.

KEY TAKEAWAYS➤ As of May 2026, the 85/15 framework is a proposed exchange rule change, not a final SEC rule.➤ Under the proposed 85/15 framework, crypto trust products would need at least 85% eligible assets.➤ Bitcoin, Ether, Solana, and XRP appear in examples, but no product gets automatic approval.➤ Derivatives, NFTs, and smaller tokens face strict limits under the proposed generic route.

What is the 85/15 crypto ETF framework?

The 85/15 crypto ETF framework is a proposed rule structure for certain Commodity-Based Trust Shares. It would require at least 85% of a product’s net asset value (NAV) to consist of eligible assets, while up to 15% could include assets that do not independently meet generic list standards.

The proposal is inside an amendment to NYSE Arca Rule 8.201-E, the listing rule that governs Commodity-Based Trust Shares on the exchange. The U.S. Securities and Exchange Commission (SEC) has published the proposal for public comment. It has not been approved yet.

That’s an important distinction because the 85/15 split is a threshold inside a draft listing standard, and it does not approve any specific Bitcoin, Ethereum, Solana, or XRP ETF on its own.

| Field | Detail |

| Proposing exchange | NYSE Arca |

| Affected rule | Rule 8.201-E |

| Product type | Commodity-Based Trust Shares |

| Eligible side floor | 85% of NAV |

| Non-eligible side cap | 15% of NAV |

| Filing status as of May 1, 2026 | Under SEC review |

| Approves a specific token ETF | No |

Why did crypto ETF rules change before the 85/15 proposal?

Before generic standards existed, exchanges typically had to use case-by-case SEC rule filings to list each new spot crypto product. Each filing went through a separate Section 19(b) review, and each one could draw months of public comment, staff feedback, and amendments.

That model worked for a small number of one-off filings. It did not scale once issuers started lining up products for a wider set of digital assets and structures.

In September 2025, the SEC approved generic list standards for Commodity-Based Trust Shares that hold spot commodities, including digital assets. The agency’s press release describes a path where qualifying products can be listed without a separate Section 19(b) proposed rule change.

| Era | Listing path | What it meant for issuers |

| Before September 2025 | Case-by-case Section 19(b) filing for each product | Long, asset-by-asset SEC reviews |

| After September 2025 | Generic list standards for qualifying products | Faster path for products that fit the standards |

| April 2026 proposal | Adds 85/15 split for multi-asset trusts | Defines how multi-asset products can use the generic path |

Generic standards do not remove SEC oversight. They reduce one specific filing step for products that already meet the rules set, while actively managed, leveraged, or novel-feature products can still need the traditional case-by-case route.

Note that the April 2026 proposal does not replace the September 2025 framework. It extends it for products that hold a mix of qualifying and non-qualifying assets, which is where the 85/15 math comes in.

Evolution of crypto ETF rules: BeInCrypto

Evolution of crypto ETF rules: BeInCryptoHow does the 85/15 framework work in practice?

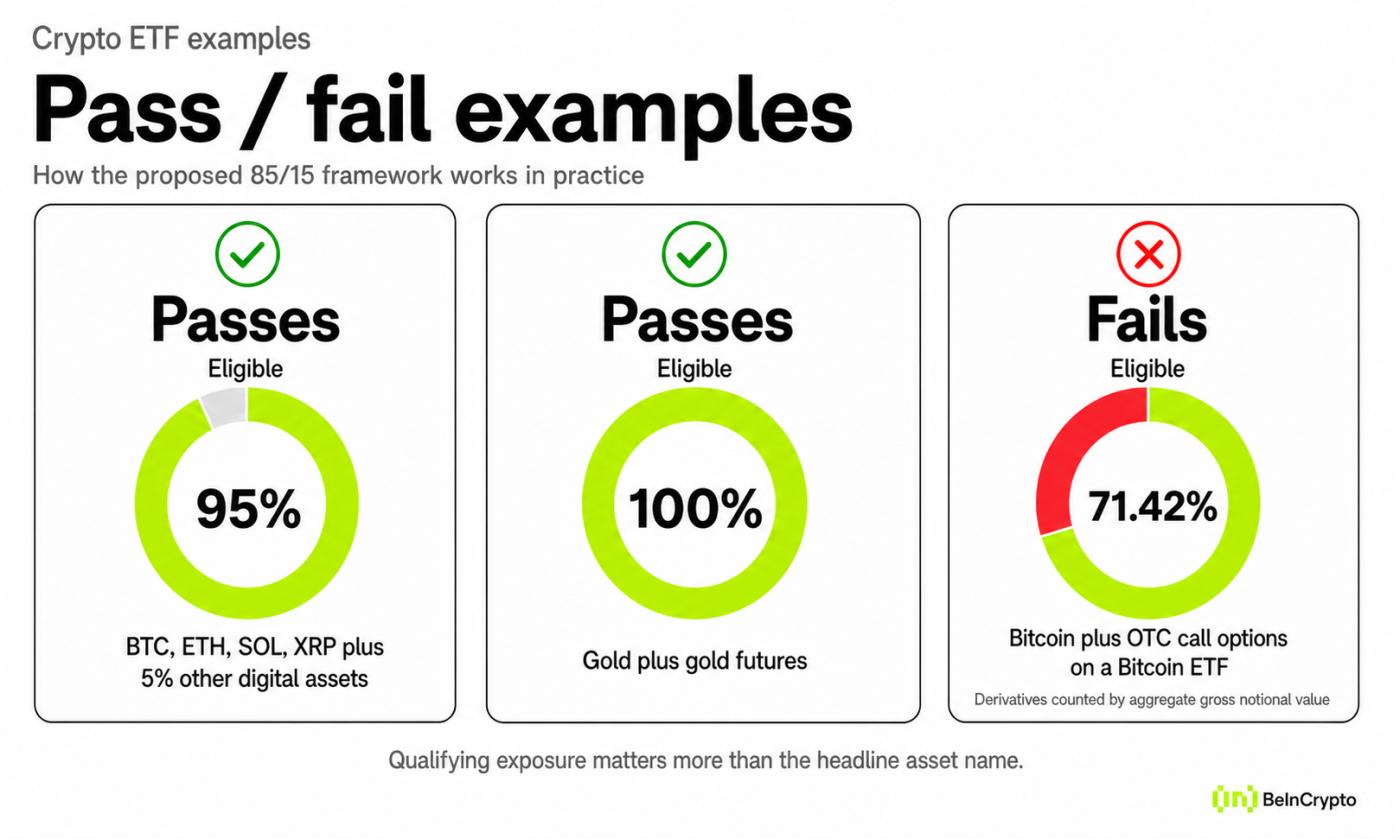

The 85/15 split looks simple, but the math depends on how each holding gets counted. The Federal Register notice for NYSE Arca’s filing includes example portfolios that show when a product would pass and when it would fail.

| Example portfolio | Eligible side | Other side | Result |

| BTC, ETH, SOL, XRP plus smaller digital assets | 95% | 5% | Passes proposed threshold |

| Gold plus gold futures | 100% | 0% | Passes proposed threshold |

| Bitcoin plus OTC call options on a Bitcoin ETF | About 71% | About 29% | Fails proposed threshold |

The Federal Register examples show that a trust holding $95 million in Bitcoin, Ether, Solana, and XRP, plus $5 million in other digital asset commodities, would exceed the 85% threshold. A Bitcoin trust that adds over-the-counter (OTC) call options on a Bitcoin ETF would fail because only about 71.42% meets the criteria.

This second example highlights the key constraint. A fund can appear heavily tied to Bitcoin and still fall short if derivative exposure increases the non-eligible side under gross notional rules.

Listed and over-the-counter (OTC) derivatives are measured using aggregate gross notional value under the 85/15 test. This means a product can fall below the required threshold even when its visible exposure looks small, as derivative positions can expand the non-eligible portion of the portfolio.

The key point is simple: the 85% test depends on how exposure is calculated under the rules, not just on the headline assets in the portfolio.

What counts toward the 85% side

The eligible side of the split is built around assets and securities that already meet existing exchange standards. The proposed rule lays out several routes that an asset can take to qualify.

| Eligibility route | Plain-language meaning |

| ISG market trading | Asset trades on a market that participates in the Intermarket Surveillance Group |

| CFTC futures, six months | Asset underlies futures on a designated contract market for at least six consecutive months |

| 40% NAV ETF route | Asset is covered by an existing ETF that gives at least 40% NAV exposure to that commodity |

| Eligible securities | Securities that already meet existing listing standards |

| Cash and cash equivalents | Cash, treasury bills, and money market instruments |

SEC Commissioner Hester Peirce’s public statement on the generic standards summarizes the same eligibility routes. Eligible holdings may include commodities that trade on an ISG member market, commodities that underlie CFTC-regulated futures for at least six months, or commodities covered by an ETF with at least 40% NAV exposure.

These conditions are designed to help exchanges monitor for fraud and manipulation, which is the core legal standard behind any new listing rule. The routes also affect product design, since each one determines whether a holding can count toward the eligible side of the portfolio.

With those routes in mind, the next question is what can fit on the smaller side of the test.

What can fall into the 15% side?

The 15% side is a limited sleeve, not an unrestricted bucket. It allows some non-qualifying exposure, but only when the rest of the product still meets the full ruleset.

| What fits in the 15% side | How it is counted |

| Non-qualifying digital asset commodities | Market value, subject to the 15% cap |

| Listed derivatives | Aggregate gross notional value |

| OTC derivatives | Aggregate gross notional value |

| Other non-eligible holdings | Subject to the 15% cap and the rest of the rule set |

Listed and OTC derivatives count by aggregate gross notional value, not market value. That choice is what causes the Bitcoin plus OTC option example to fail. A product with too much derivative exposure can fail the test even when its market-value mix looks balanced.

The 15% side is not a loophole for any asset. It is a limited sleeve that allows some non-qualifying exposure, as long as the product still meets the full rule set.

That makes the 15% sleeve a real constraint on product design, especially for trusts that try to layer options or other complex instruments on top of a core spot holding.

What does this mean for Bitcoin and Ethereum?

Bitcoin (BTC) and Ethereum already have more mature ETF access than most other crypto assets. The 85/15 proposal matters less for direct BTC or ether exposure and more for multi-asset products that use them as core eligible holdings.

| Question | Bitcoin | Ethereum |

| Already has spot ETF access in the U.S. | Yes | Yes |

| Role under 85/15 proposal | Qualifying anchor in multi-asset trusts | Qualifying anchor in multi-asset trusts |

| New approval implied by this proposal | No | No |

| Underlying market risk changes | No | No |

In the filing, Bitcoin and Ether function as qualifying anchors. A trust that combines them with smaller digital assets can keep the eligible side dominant, which makes the 85% threshold easier to meet. That structural role explains why they appear in the example portfolios.

However, this does not change the underlying market risk of either asset. It also does not represent a new approval event, since both already trade through existing spot products in the United States.

For readers who already follow Bitcoin and Ethereum ETFs, the key change is structural rather than asset-specific. The framework clarifies the listing path for funds that combine these anchors with other digital assets, which is separate from whether a single-asset BTC or ETH product receives approval.

What does this mean for Solana and XRP?

Impact of the 85/15 framework: BeInCrypto

Impact of the 85/15 framework: BeInCryptoSolana (SOL) and XRP appear in the filing’s example portfolios alongside Bitcoin and ether. That placement is what fuels much of the headline coverage, but the filing carefully avoids approving any specific product around them.

Does the 85/15 framework approve Solana ETFs? No. Solana appears in the filing’s examples, but the proposal does not guarantee approval for a standalone Solana ETF.

Does the 85/15 framework approve XRP ETFs? No. The framework does not approve any specific XRP ETF. XRP appears in the filing’s examples as an eligible asset, but each product must still meet all rule and disclosure requirements.

The example treats SOL and XRP as eligible holdings inside a multi-asset trust. That can help products that include several digital assets, since their inclusion supports the 85% side rather than weighing it down. It does not, however, guarantee a standalone Solana ETF or XRP ETF approval.

A separate product focused on a single one of these tokens would still need to satisfy all rules and disclosure requirements, plus any further SEC review specific to that filing. Headlines that imply otherwise stretch beyond what the proposal actually says.

For Solana and XRP searchers, the practical takeaway is clear: the 85/15 proposal could improve the path for certain U.S.-listed multi-asset trusts that include these tokens. It does not endorse SOL or XRP, set a launch date, or guarantee approval for any specific product.

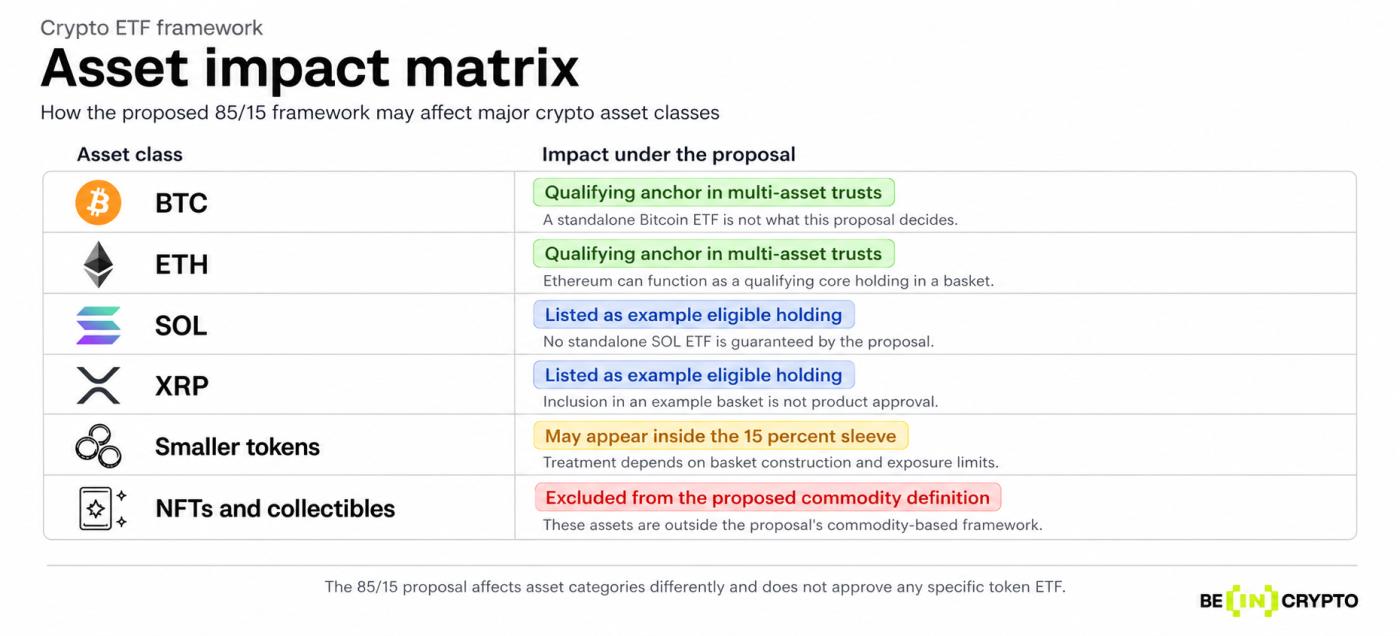

Asset impact matrix

| Asset | Main rule impact under the proposal | Key caveat |

| Bitcoin (BTC) | Qualifying anchor in multi-asset trusts | No new BTC approval implied |

| Ether (ETH) | Qualifying anchor in multi-asset trusts | No new ETH approval implied |

| Solana (SOL) | Listed as an example eligible holding | No standalone SOL ETF guaranteed |

| XRP | Listed as an example eligible holding | No standalone XRP ETF guaranteed |

| Smaller tokens | May appear inside the 15% sleeve | Cap and full rule set still apply |

| NFTs and collectibles | Excluded from the proposed commodity definition | Separate filing route remains possible |

The matrix shows that the proposal touches different parts of the market in different ways. The next section follows the long tail.

What does this mean for smaller tokens, NFTs, and collectibles

Smaller digital tokens that do not independently meet the eligibility routes can still enter a product, but only inside the 15% sleeve. That cap limits how much weight any single non-qualifying token can carry inside a trust that wants to use the generic listing standard.

The filing also treats non-fungible tokens (NFTs) and other collectibles separately. Under the proposed commodity definition for this generic route, non-fungible assets and collectibles would not qualify as eligible commodities. That removes them from the 85% side and from the limited 15% sleeve under this specific path.

| Asset class | Inside 85% side | Inside 15% sleeve | Separate filing path |

| Major crypto assets (BTC, ETH, SOL, XRP) | Yes, when they meet a route | Not needed | Yes |

| Smaller digital tokens | Only if they meet a route | Yes, capped | Yes |

| NFTs and collectibles | No | No | Possible |

The exclusion is not a permanent ban. The NYSE Arca notice says the proposal would exclude non-fungible assets and collectibles from the commodity definition for generic standards, but it would not stop the exchange from submitting a separate rule change for products that include such assets, which would go through its own SEC review.

Why crypto ETF and crypto ETP are not always the same thing

Many readers search for “crypto ETF rules” because that is the common shorthand in market coverage. The rule text, however, refers to Commodity-Based Trust Shares, which is a specific category of exchange-traded product (ETP).

| Feature | Commodity-Based Trust Shares (ETP) | Traditional ETF |

| Registration statute | Securities Act of 1933 | Investment Company Act of 1940 |

| Investor protection regime | 1933 Act framework | 1940 Act framework |

| Common label in headlines | “Crypto ETF” | “ETF” |

| Coverage of crypto trust products today | Yes | Limited |

These products typically register their securities under the Securities Act of 1933. That sets them apart from many traditional ETFs that register under the Investment Company Act of 1940 and carry a different set of investor protections. The legal structure can affect disclosure rules, governance, and how investor concerns are handled.

SEC Commissioner Caroline Crenshaw’s dissent on the generic standards highlights this point. The dissent argues that ETP issuers register under the 1933 Act and warns that letting qualifying digital asset products list without case-by-case Commission review is a meaningful change.

This terminology point is small but useful, since it changes how readers should weigh the practical effect of the framework. A faster listing path for Commodity-Based Trust Shares is not the same as a faster listing path for traditional ETFs, even when the headlines treat them as one category.

Is the 85/15 framework final?

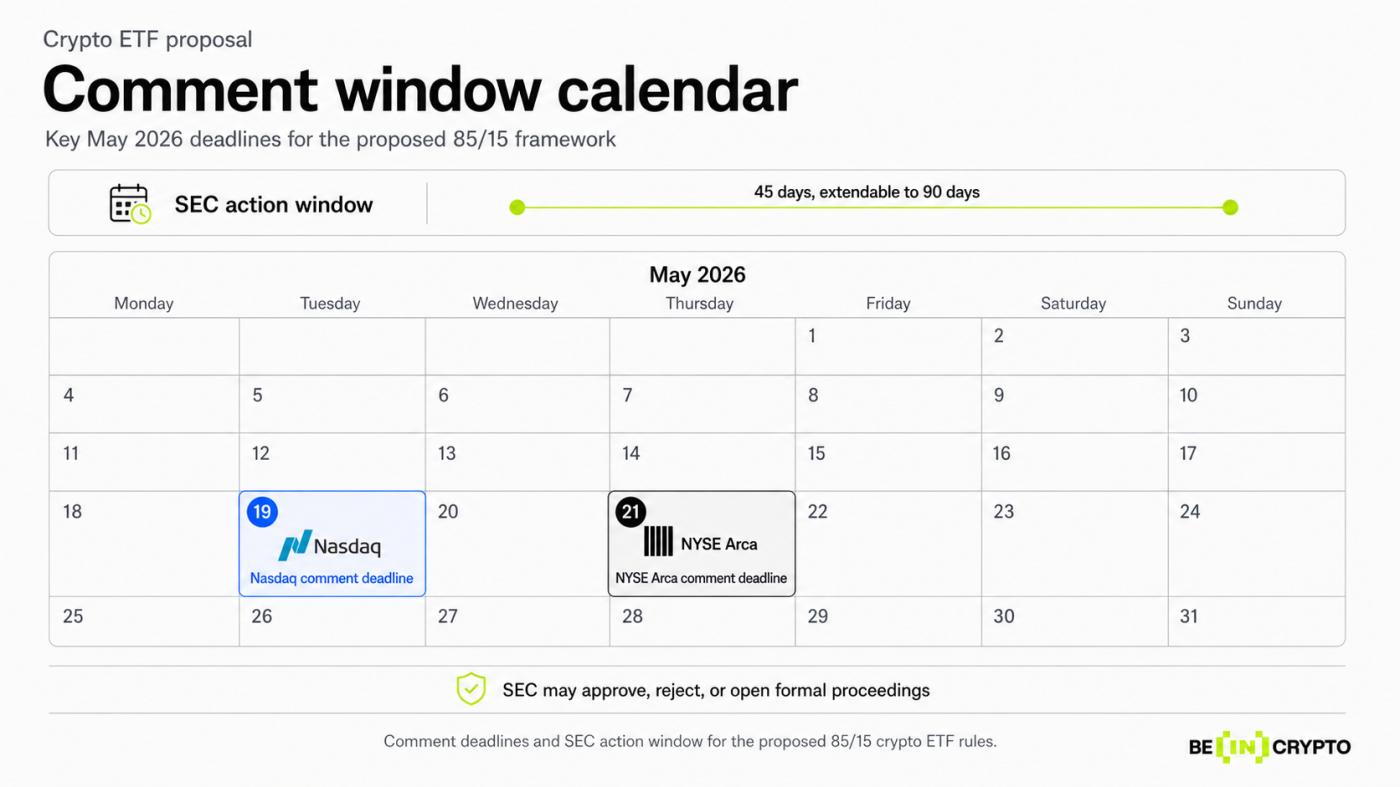

No. As of May 1, 2026, the 85/15 framework is a proposal. Comments on the NYSE Arca proposal are due by May 21, 2026, and the SEC can approve, reject, or start proceedings within the review window.

A parallel Nasdaq filing sits next to the NYSE Arca proposal. The Nasdaq notice uses the same 85% threshold, the same 15% limit, the same gross notional treatment for derivatives, and the same Bitcoin, ether, Solana, and XRP example. Its public comment deadline is May 19, 2026.

| Item | NYSE Arca filing | Nasdaq filing |

| Threshold | 85% eligible / 15% other | 85% eligible / 15% other |

| Derivative treatment | Aggregate gross notional value | Aggregate gross notional value |

| Public comment deadline | May 21, 2026 | May 19, 2026 |

| SEC action window | 45 days, extendable to 90 days | 45 days, extendable to 90 days |

| Assets in example | BTC, ETH, SOL, XRP | BTC, ETH, SOL, XRP |

The two filings together signal a broader exchange-level move around generic standards. The actual outcome still depends on the SEC’s review and on any changes that emerge from public comments.

Public comments often shape the final rule. Issuers, legal commentators, and investor advocates can push for changes in how derivatives are treated, how the 15 percent sleeve is calculated, or how the commodity definition reads. Until the SEC acts, the framework remains a draft.

What should readers remember?

The 85/15 framework is best seen as a rule structure for multi-asset crypto trust products. It may give issuers more flexibility, but only within clear limits.

| Principle | What it means in practice |

| Eligible assets must dominate | At least 85% of NAV must meet existing standards |

| Non-qualifying exposure stays capped | The 15% sleeve has a hard limit |

| Derivatives receive strict treatment | Counted by aggregate gross notional value |

| NFTs and collectibles do not qualify here | Excluded from the proposed commodity definition |

| No specific ETF is approved | This is a listing standard, not an approval |

Most importantly, the proposal does not approve any specific Bitcoin, Ethereum, Solana, or XRP ETF. It changes the listing path for certain Commodity-Based Trust Shares, and as of May 01, 2026, that change is still under SEC review.

Frequently asked questions

What is the 85/15 crypto ETF framework?

The 85/15 framework is a proposed rule for certain Commodity-Based Trust Shares listed on NYSE Arca. It would require at least 85% of a product’s NAV to consist of eligible assets, while up to 15% could include holdings that do not independently meet generic list standards. The proposal is under SEC review and has not been approved as of May 1, 2026.

Is the 85/15 framework already approved?

No. The 85/15 framework is a proposed exchange rule change that the SEC has published for public comment. Comments on the NYSE Arca filing are due by May 21, 2026, and the SEC can approve, reject, or start formal proceedings within its review window. Until then, the framework remains a proposal, not a final SEC rule.

Why are Bitcoin, Ethereum, Solana, and XRP named in the filing?

They appear in the filing’s example portfolios because each one currently meets at least one of the proposed eligibility routes for the 85% side. Their inclusion shows how a multi-asset trust could combine major crypto assets while clearing the threshold. The filing does not describe them as approved tokens, and it does not endorse any specific product built around them.

Can smaller tokens appear in a crypto ETF under the proposal?

Smaller tokens that do not independently meet the eligibility routes may appear inside the 15% sleeve. They would still need to fit within the cap, and the product would have to meet the rest of the rule set, including derivative treatment. The proposal does not turn the 15% side into an open path for any non-qualifying asset.

Can NFTs qualify under the 85/15 framework?

NFTs and other collectibles would not qualify under this generic route, based on the proposed commodity definition change. They sit outside both the 85% side and the 15% sleeve for this specific listing path. An exchange could still file a separate rule change for products that include such assets, which would go through its own SEC review.

Are crypto ETFs and crypto ETPs the same?

They are not always the same. Crypto ETF is a common search term, while the rule text refers to Commodity-Based Trust Shares, which are exchange-traded products that typically register under the Securities Act of 1933. That structure differs from many traditional ETFs registered under the Investment Company Act of 1940, and the investor protections can vary as a result.

Does the framework mean more XRP or Solana ETF launches are guaranteed?

No. The proposal may help certain multi-asset products that include XRP or Solana, but it does not guarantee approval, launch, liquidity, or any price impact for either token. Each new product would still need to meet the full rule set and any further SEC review specific to that filing.