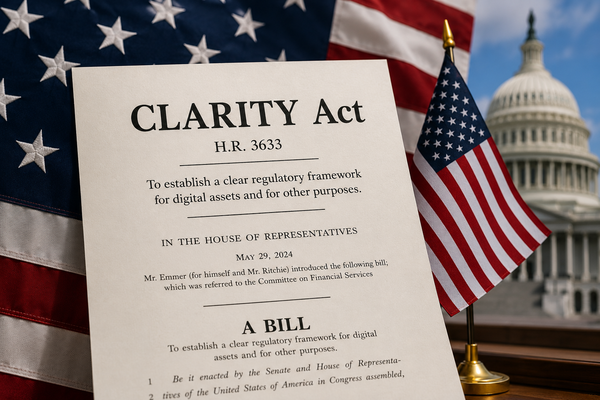

The 'CLARITY Act,' a bill to restructure the U.S. digital asset market that has been stalled for months, will be put to a vote by the Senate Banking Committee on the 14th. The industry views this vote as a watershed moment that will determine the direction of the U.S. cryptocurrency regulatory framework.

This bill primarily focuses on clarifying the criteria for classifying cryptocurrencies as securities or commodities, and establishing a supervisory framework for stablecoins and digital asset service providers. It effectively amounts to the U.S. version of the 'Digital Asset Framework Act.'

Discussions on the bill have been delayed due to disagreements over the stablecoin reward system. In particular, the key issue was whether to allow a structure that pays interest simply for holding the coins. It has recently been reported that the U.S. Congress has reached a compromise that restricts interest based on simple deposits while permitting rewards based on payment and transaction activities.

The market anticipates that the passage of this bill will bring significant changes to the competitive landscape of the global stablecoin market. This is because if the U.S. clarifies the legal definition and supervisory authority of digital assets, it is highly likely that institutional investors and the traditional financial sector will accelerate their entry into the market.

In fact, moves to secure a leading position in the tokenization market are rapidly spreading within the U.S. financial sector. The DTCC is pushing to expand its infrastructure for settling tokenized securities, and the New York Stock Exchange (NYSE) has initiated the process of amending regulations to allow the trading of tokenized stocks. JPMorgan and BlackRock are also actively working to expand the markets for tokenized government bonds and on-chain assets.

There is also analysis in the industry that the CLARITY bill could serve as a catalyst to go beyond simple cryptocurrency regulation and incorporate the entire stablecoin, RWA (Real Asset Tokenization), and STO (Security Token Offering) markets into the institutional financial system.

In particular, if the United States preempts digital asset regulatory standards, there is a high possibility that the global market will be reorganized into a U.S.-centric system. Although Europe has established the MiCA framework, it is considered relatively more conservative than the U.S. in terms of industrial growth potential, and Asian countries are also closely watching the final legislative direction of the United States.

However, variables still remain before the bill can pass. Even if it clears the Senate Banking Committee, it must go through coordination procedures in the Senate plenary session and the House. Some Democratic lawmakers are still maintaining a cautious stance, citing issues such as anti-money laundering measures and political conflicts of interest.

The White House is reportedly aiming to complete the final legislation before U.S. Independence Day on July 4. If processed according to schedule, the U.S. digital asset market is expected to increasingly likely enter a phase of full-scale institutionalization starting in the second half of this year.