Global bond yields rose sharply across the board on Friday as oil prices surged. The 30-year UK government bond reached 5.82%, its highest level since 1998.

The sell-off has impacted US Treasury bonds, as well as UK and Japanese government bonds. Traders are now questioning what signals these bonds are sending about China, oil supply, and government budget deficits.

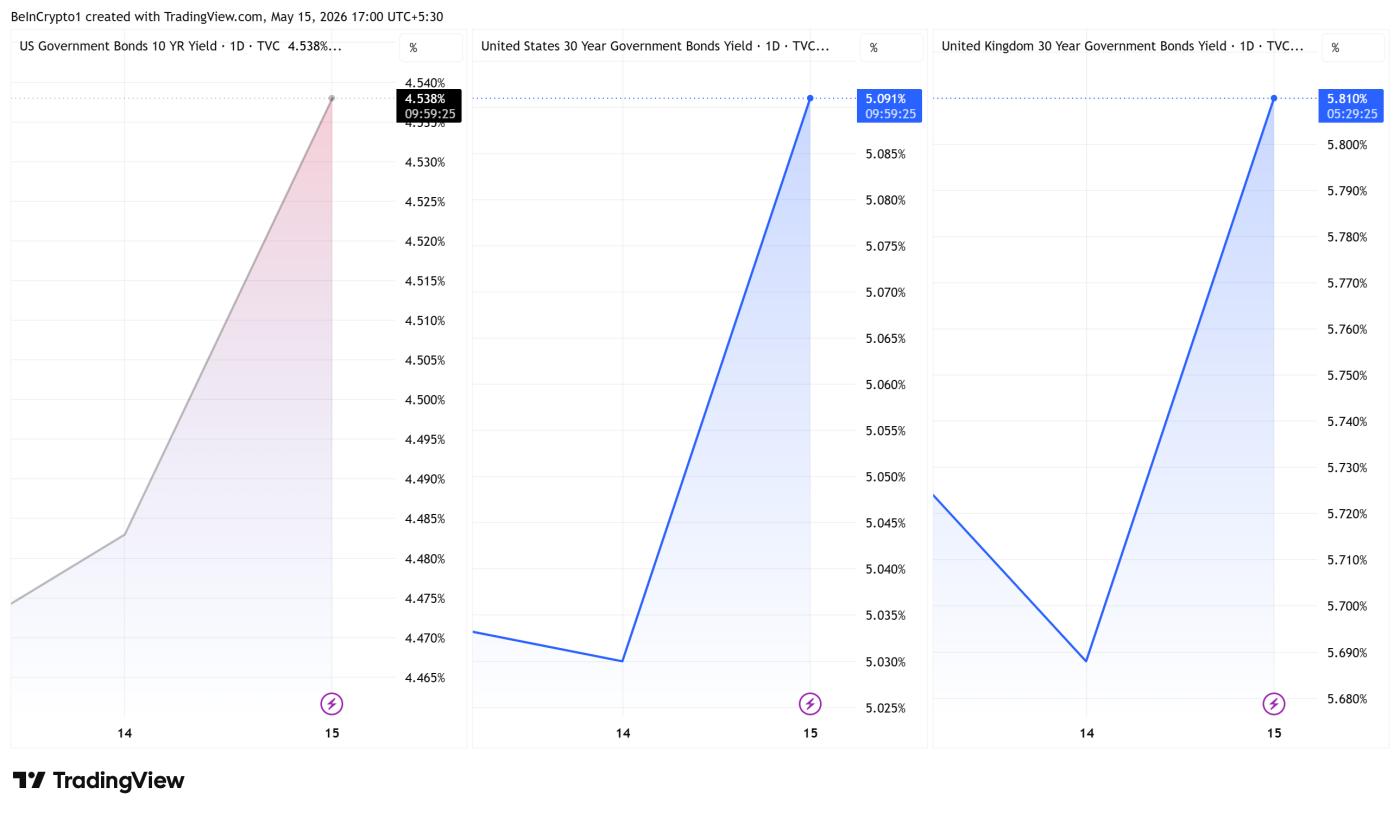

A wave of simultaneous yield increases across major economies.

Allianz's chief economic advisor, Mohamed El-Erian, said the main reason for this increase was the surge in oil prices . In addition, Japanese producer price data was also hotter than expected.

Japanese 30-year Treasury yields traded at 4% for the first time since 1999. British 10-year Treasury yields hovered around 5.14%, and German yields of the same maturity rose 7.5 basis points to 3.12%.

US Treasury bond yields also rose. The 10-year US Treasury yield remained at around 4.54%, the 20-year yield at 5.10%, and the 30-year yield at 5.09%.

Yields on 10-year and 30-year US Treasury bonds, and performance of 30-year UK government bonds. Source: TradingView

Yields on 10-year and 30-year US Treasury bonds, and performance of 30-year UK government bonds. Source: TradingView"All maturities increased at the same time," the Bull Theory trader emphasized .

The stock market was largely unaffected. The S&P 500 index continued to hold near its record high of 7,501 thanks to optimism about AI . The S&P's yield is now significantly lower than the 10-year yield, a situation not seen since 2003.

“Bond yields don’t care about AI. They only care about the annual budget deficit of $2 trillion, oil prices hitting $100, inflation remaining high, and the government constantly borrowing money every day to finance wars,” Bull Theory added.

What do yields say about China and the economy?

On the Chinese side, the general sentiment is one of skepticism. Mad Money host Jim Cramer suggests that the stock market is placing its faith in President Xi Jinping's ability to withstand the disruption to oil supply associated with President Donald Trump.

He also noted that no clear trade commitments had emerged. Bond traders, however, seemed less optimistic.

Economically, bonds are reflecting inflation that has lasted longer than expected . Added to this are growing budget deficits and the difficulty for central banks to quickly cut interest rates.

UK government bonds are signaling fiscal strain, while long-term Japanese bonds suggest the end of a prolonged period of yield restraint as the Bank of Japan begins to normalize policy.

Bond yields are currently reflecting expectations of limited diplomatic impact from China, inflation fueled by rising oil prices, and increasing Capital costs. Meanwhile, the stock market remains confident in profit growth driven by AI .

These two viewpoints are unlikely to remain valid indefinitely. The upcoming developments in oil prices, the message from the Bank of Japan, and any post-Trump-Xi moves will be key factors in determining which side must concede first.