Original author: TechFlow TechFlow

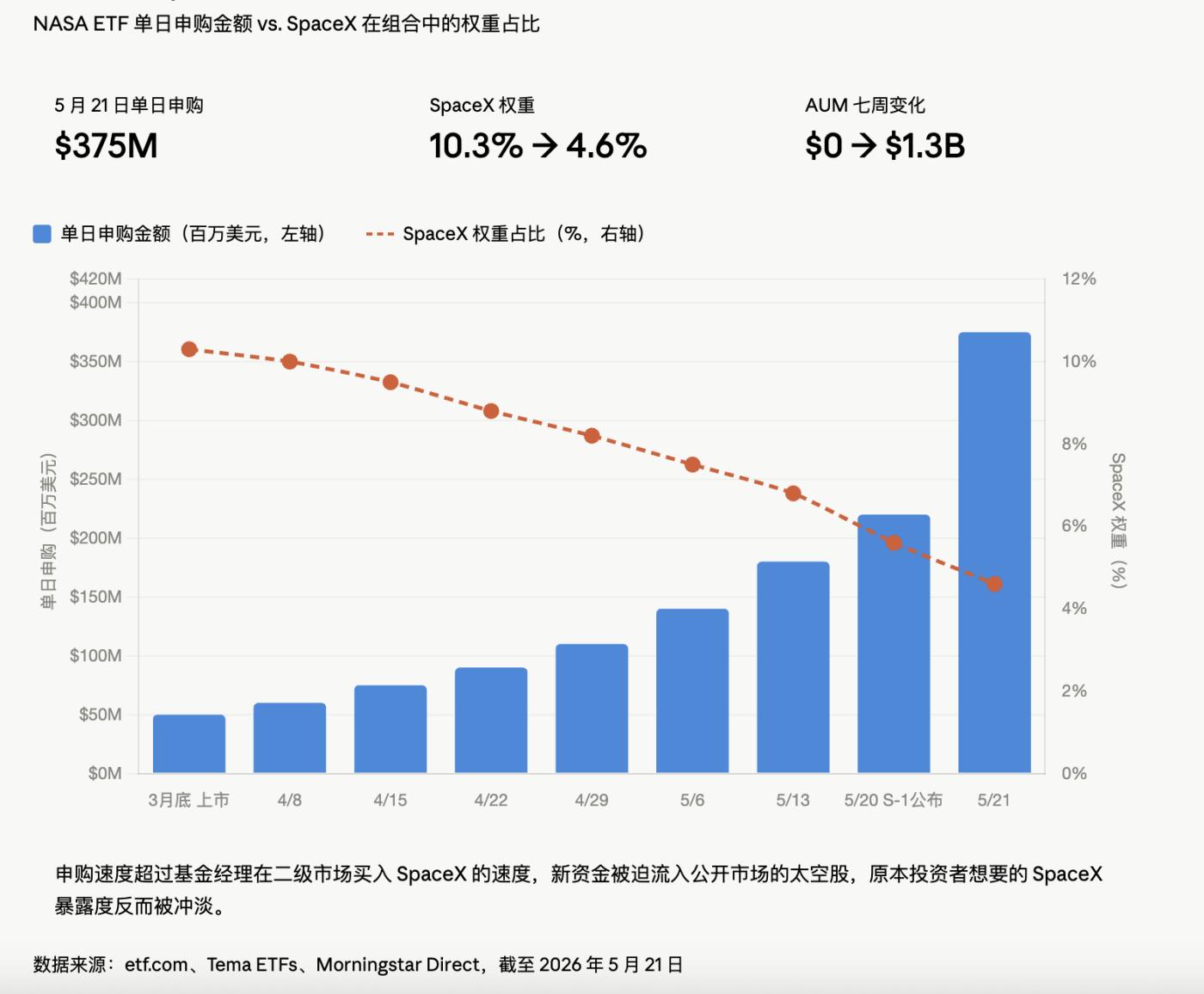

On May 20, SpaceX's S-1 prospectus was published on the SEC website. The next day, a fund with the ticker symbol "NASA" attracted $375 million in a single day, tripling its assets under management (AUM) within a week. This fund had only been established seven weeks prior.

Seven weeks later, it had become the world's largest space-themed ETF, leaving the long-established UFO ETF, which had been running for seven years, far behind. The money it raised in seven weeks was more than the total amount raised by UFO ETF over seven years.

Everyone rushing into NASA wants to buy SpaceX. But the number of SpaceX vehicles they actually acquire is decreasing.

Where did the money go?

The NASA ETF is touted as "the only pure space ETF in the market that holds SpaceX shares." As of May 21, NASA indirectly held 232,000 SpaceX common stock equivalents through a special purpose vehicle (SPV), with a book value of $147.4 million and an implied valuation of approximately $1.51 trillion.

The numbers look impressive. But there's a detail that ordinary investors would completely overlook. According to ETF.com, a week ago, NASA's holdings in SpaceX were 10.3%. A week later, they had been diluted to 4.6%.

Because the money from subscriptions came in so quickly, fund managers simply couldn't keep up with the demand for SpaceX shares on the secondary market. A large amount of new money was forced to buy space-related stocks on the open market, which in turn diluted the SpaceX holdings that investors originally intended to acquire.

Retail investors rushed in wanting to buy SpaceX, but ended up buying Rocket Lab, AST SpaceMobile, and a bunch of other stocks.

Even more subtle is the valuation mechanism. The SPV's holdings are only updated when Tema itself makes a transaction. In other words, regardless of how SpaceX's secondary market price fluctuates, NASA's portion remains unchanged on paper.

This setup goes unnoticed in a bull market. However, if the stock price falls below the IPO price after listing, the SPV portion will react in a strangely delayed way. Not to mention, this SPV will be locked up for six months after SpaceX's official IPO. If the opening price crashes, retail investors can escape, but the SPV cannot.

The ETF charges a 0.87% management fee annually, but the apparent 65% of the actual gains come from stocks like Rocket Lab and Intuitive Machines, which have already seen explosive growth. SpaceX, on the other hand, hasn't contributed much.

NASA is essentially a thematic fund using SpaceX as bait, holding a bunch of small-cap space stocks. The taste of the bait is important, but what's served on the plate is something else entirely.

Valuation inversion

What many people don't know is that some of the major stocks in this sector have already experienced a round of price increases.

Rocket Labs has risen 357% in the past 12 months; Planet Labs has risen 979%; and LUNR has risen 212%. ARKX has risen 62% in the past year, and ROKT has risen 75%. SpaceX has merely lit a tinderbox that was already smoldering.

Looking at these figures in detail, questions arise. Planet Labs' stock price surged 979% in a year, but the company's main business is selling satellite imagery data. Does its fundamentals justify a stock price nearly ten times its initial value?

There were 102 orbital launches globally in 2019 and 342 in 2025, double the peak of the space race in 1967. Grand View Research predicts that the global space industry will be worth $466 billion in 2024 and grow to $769 billion by 2030.

But the question is, how can the industry's growth from 466 billion to 769 billion correspond to a 10-fold increase in the secondary market?

This is a classic scenario of valuation inversion. The fundamentals are growing linearly, while the stock price is growing exponentially, with the difference being made up by a "narrative premium." And the source of this narrative premium is only one: SpaceX's upcoming IPO.

What exactly did the people who actually bought into the deal?

Let's return to SpaceX as a company.

In 2024, the company's revenue reached $18.67 billion, compared to only $10.3 billion in 2023. However, it suffered a loss of $4.59 billion in 2024, compared to a profit of $791 million in 2023, turning from profit to loss.

CNN reported that the AI division lost nearly $5 billion last year because it was burning through cash building data centers.

SpaceX disclosed in its prospectus that xAI has been merged into SpaceX, and X (formerly Twitter) is also included. This so-called "space IPO" is essentially a bundle of all of Musk's assets. The prospectus also reveals that Musk controls 85% of the voting rights, and unless he votes to fire himself, no one can touch him.

SpaceX's $1.75 trillion valuation corresponds to a four-in-one narrative of "space + AI + satellite internet + social media". The bigger the narrative, the more inflated the price.

But the secondary market doesn't care about any of that. What the secondary market cares about is that everyone is rushing to get on board, so I have to get on too.

After going around in circles, the biggest winners are not the retail shareholders of SpaceX, because they haven't gotten on board yet; nor are they the ETF investors who rushed into NASA, because their SpaceX holdings are being diluted.

The most profitable are ETF issuers. NASA's expense ratio is 0.87%, the third highest among similar funds. $1.3 billion in assets under management (AUM) translates to $11 million in management fees annually.

Issuing an ETF is essentially the same as issuing cryptocurrency; you need a story, a timing, and a seemingly plausible benchmark. SpaceX provided all three.

Written before the IPO

On June 12, SpaceX is expected to list on Nasdaq under the ticker symbol SPCX. The underwriting syndicate is led by some of the world's largest investment banks, with a fundraising target of $40 billion to $80 billion, far exceeding the record set by Saudi Aramco in 2020.

This will be the largest IPO in human history.

If the price falls below the initial offering price on the first day of trading, all ETF investors who bought in following the SpaceX story will find that their SPV positions are still at "old prices" from several months ago. They will be unable to cut their losses or exit immediately.

If the price surges at the open, those who missed out on the ETF will rush in, further pushing up the ETF premium and diluting SpaceX's actual weighting within the ETF, creating a comical inverse flywheel where the more people buy, the less SpaceX each individual actually receives.

Following SpaceX, a host of industry giants are queuing up for IPOs. Each IPO of a leading company in a "concept sector" will spawn a new batch of ETFs. And each new batch of ETFs will repeat the same dilution game.

The industry isn't lacking in new stories, but it lacks people who will ask, "Did I really buy what I thought I bought?" The answer will come after June 12th. But by then, those who rushed into NASA today won't care about the answer; they'll either be counting their money or fighting for their rights.