Original author: ChandlerZ, Foresight News

On the evening of May 28, the SPACEEX-USDH perpetual contract on Hyperliquid experienced a sharp flash crash, with the price falling from a low of $2,277 to a low of $1,254 within 30 minutes, a drop of nearly 45%, before rebounding to around $2,169.

This crash resulted in the liquidation of 405 users and 1,393 positions, with a total liquidation amount of $1.51 million.

Data shows that the total trading volume of this contract in the past 24 hours was only about $4.87 million, with open interest of less than $2.9 million, indicating extremely low market depth. A single large sell order almost immediately broke through liquidity, triggering a stampede-like sell-off. The liquidated investors were mainly retail investors, with a median margin of only about $31 and generally using leverage of about 3 times.

Ventures, the perpetual contract platform within the Hyperliquid ecosystem, responded via Twitter, stating that the team was aware of the flash crash on the SPACEX market. The incident was caused by an off-chain data provider, a component of the oracle price mechanism, returning incorrect data. This led to significant fluctuations in oracle and token prices in the market, triggering forced liquidation of some user positions.

The team has taken measures to prevent similar incidents from happening again. Furthermore, the team is assessing the impact of this incident on affected users to develop an appropriate compensation plan. Affected users will receive compensation within the next 48 hours.

A fragile pricing chain

SPACEX - USDH is a crypto perpetual contract launched by Hyperliquid that uses the term "SpaceX valuation" to allow users to bet on changes in the market valuation of SpaceX before its IPO, but it does not represent actual shares and does not grant any shareholder rights.

On Ventures, 1 SPACEX represents a valuation of $1 billion for SpaceX. If the SPACEX price is $420.69, it means that the market values SpaceX at $420.69 billion.

The core challenge of these types of contracts lies in how to price a company that doesn't trade publicly.

Ventuals' approach splits pricing into two parts, with one-third of the weight coming from Notice, an off-chain private market data provider. Its pricing model integrates funding rounds, 409A valuations, mutual fund tokens, secondary market transactions and quotes, and comparable listed companies.

Two-thirds of the weighting comes from the index-weighted moving average of the contract's own mark price over the past 2 hours. Notice data is polled at least once per minute, and the oracle price is updated every 3 seconds.

This design ideally balances external information and on-chain price discovery, but it has a fatal single point of failure. If the data returned by the Notice itself is incorrect, one-third of the external anchors become a force pulling the price in the wrong direction.

The other two-thirds of the on-chain average price can hedge against this error when there is sufficient liquidity, but on SPACEX contracts with a daily trading volume of only $4.87 million, the on-chain price itself is very fragile. The combination of two fragile components results in a flash crash in price.

Low liquidity under zero arbitrage and fragmentation

The SpaceX crash exposed problems beyond just Ventures. The entire pre-IPO synthetic product category faces the same dilemma in pricing mechanisms: the lack of a unified spot market and cross-platform arbitrage channels.

In traditional finance, the price difference of the same stock on the NYSE and Nasdaq is almost non-existent because high-frequency market makers manipulate prices in milliseconds. However, in the pre-IPO synthetic product market, such arbitrage is structurally impossible because each platform's contracts are issued according to its own rules, making cross-platform hedging impossible.

SPACEX on Hyperliquid and SPCX on Binance track the same company, but there is no mechanism between them to guarantee price consistency. As a result, each platform forms its own closed pricing pool, and liquidity is dispersed across multiple unconnected venues, each pool being much shallower than the whole.

Ventuals' daily trading volume on SPACEX is $4.87 million. If the liquidity of existing platforms were concentrated in one place, the depth would be completely different, but fragmentation exposes each platform to the risk of low liquidity.

The essence of pre-IPO synthetic products is that a group of people bet on a number without a publicly available price benchmark. The price discovery on each platform only reflects the consensus of that small group of traders on that platform, and there is no rigid connection between it and the company's true valuation.

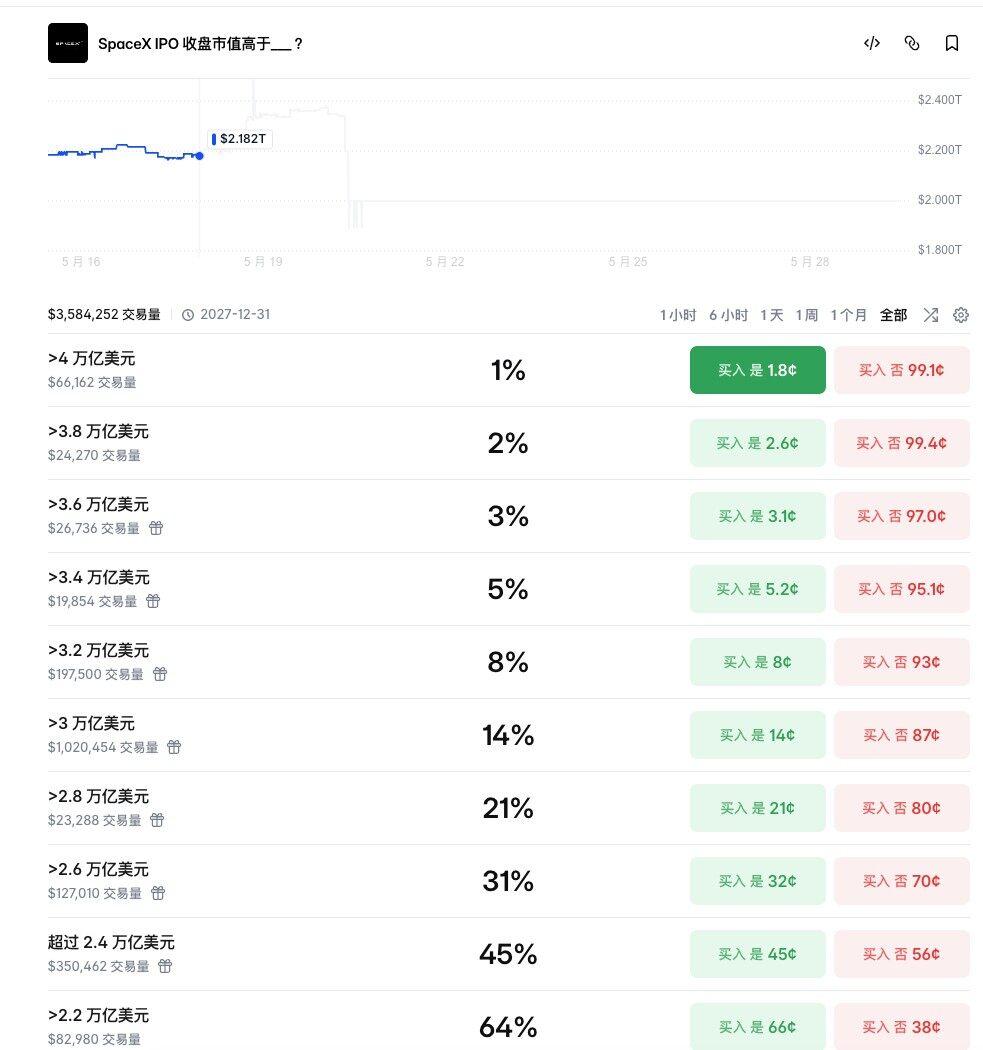

Data sources similar to the Notice are private market information, which is updated infrequently, has narrow coverage, and is opaque. No one really knows how much SpaceX is worth. The valuation of SpaceX's IPO on Polymarket is also scattered, with a 45% probability of exceeding $2.4 trillion and a 31% probability of exceeding $2.6 trillion.

The answer is about to be revealed.

SpaceX filed a confidential S-1 document with the SEC on April 1, aiming to price its shares on Nasdaq on June 11 and begin trading on June 12, with a valuation range of $1.75 trillion to $2 trillion.

The Ventuals documentation outlines the contract's settlement mechanism. On the first day of trading after the IPO, funding rates are zeroed out, the oracle price is locked at the mark price, and a valuation calculated based on the real-time stock price is introduced as an external price constraint. After the market closes, the mark price is overwritten with the valuation based on the closing price, and all open positions are forcibly settled at this price.

This means that on the day of the IPO, all holders of SPACEEX contracts will be settled according to the real share price. If there is a significant gap between the on-chain price and the Nasdaq pricing, the settlement will result in a large-scale one-way liquidation.

Analysts estimate the current gap to be around 60%, and the convergence is unlikely to be smooth because there's no way to hedge on-chain positions with actual SpaceX stock before the IPO; the arbitrage mechanism is structurally broken. Convergence is likely to occur dramatically in the final 72 hours.

The recent price crash stemmed from an oracle data error, while the convergence on the June IPO day was due to a calibration of the true price. The extent of the impact will depend on the total size of open interest across multiple platforms at that time. The closer SpaceX gets to its IPO, the more speculative capital will flood in, leading to a simultaneous expansion of fragmented liquidity and distorted pricing.

The user group with a median margin of $31 will not disappear; they will return with even more $31.