In the first half of 2026, Wall Street's attitude towards stock tokenization shifted from observation to full-scale adoption:

The SEC approved Nasdaq's tokenized trading and settlement pilot program, the NYSE partnered with Securitize to build a regulated digital securities platform, and BlackRock CEO Larry Fink defined tokenization as "the next evolution of the market" in his annual letter to investors. Meanwhile, the total market capitalization of on-chain tokenized stocks grew more than 50 times in a year, surpassing $1 billion, with Ondo Global Markets becoming the first tokenized stock platform to achieve a TVL exceeding $1 billion.

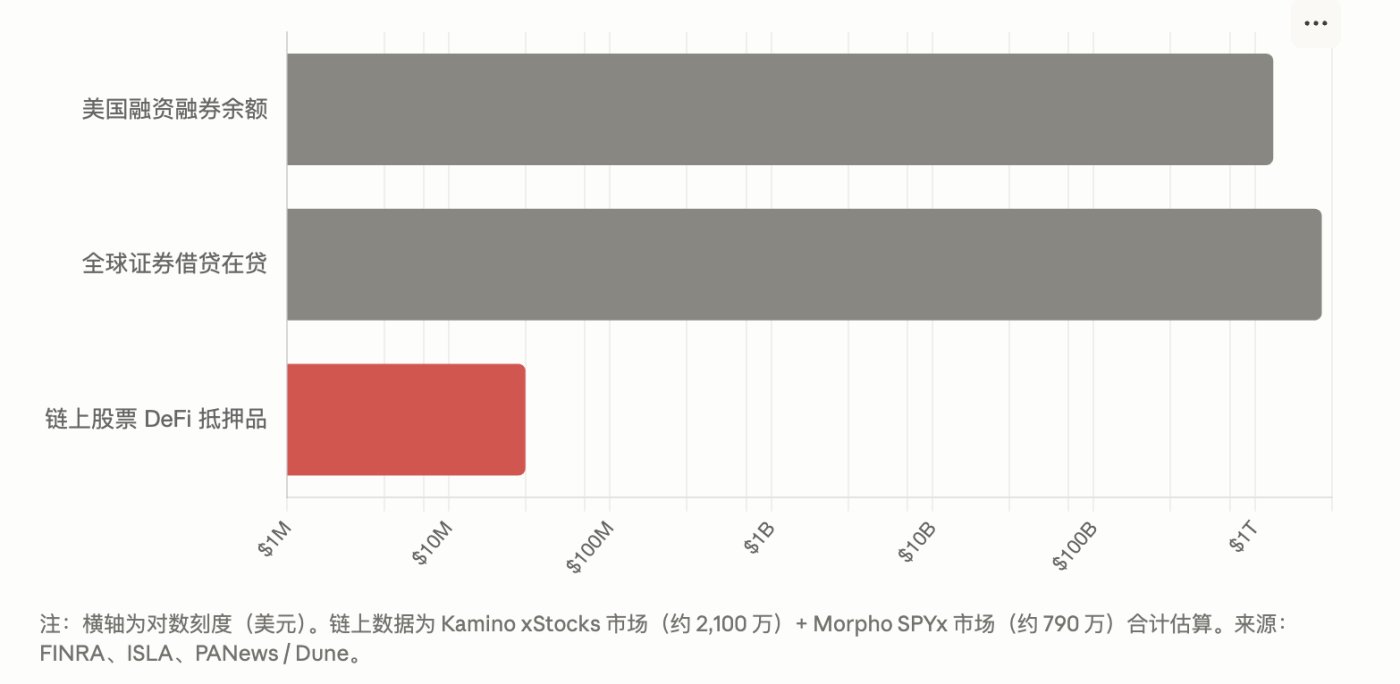

However, we believe that putting assets on-chain is only the first act . On-chain data shows that the current use of tokenized stocks remains highly "traditional"—more than half of the trading volume is concentrated during regular trading hours in the US stock market, with weekend trading accounting for less than 1%. This indicates that simply putting stocks on-chain has not created new demand that differentiates it from traditional brokerages. The real second growth curve lies in the composability of tokenized stocks with DeFi: collateralized lending, on-chain market making, derivatives, and structured yield products. This process is already in its early stages (stock collateralized lending markets on Kamino and Morpho are already online), and the more than $1.3 trillion in US stock margin trading balance and the trillions of dollars in the global securities lending market in traditional finance provide a clear and visible demand anchor for on-chain stock DeFi.

This report argues for three core judgments:

Judgment 1 : The "holding and trading" phase of tokenized stocks is about to reach its peak marginal utility. Tokenized stocks without DeFi composability are essentially just "brokerage firms with a different ledger".

Second prediction : Referring to the historical paths of "stablecoins → DeFi Summer" and "ETH → LSD ecosystem," within 12-24 months after a large number of assets are put on-chain, the financial derivatives layer surrounding those assets will experience explosive growth. Tokenized stocks are at the beginning of this window.

Judgment 3 : The order of beneficiaries is: Issuance layer → Compliant DeFi infrastructure → Lending and derivatives protocols → Hosting public chain. The regulatory ruling on whether "on-chain securities can enter permissionless DeFi" is the biggest variable in the timeline.

I. Introduction: Why is Wall Street collectively moving towards tokenization?

1.1 Landmark Event: In March 2026, the war begins in earnest.

If we had to choose a landmark moment for Wall Street's foray into tokenization, it would be March 2026. During that month, almost every day saw major events:

On March 4, a banking entity associated with Kraken was granted access to the Federal Reserve’s core account system, meaning that for the first time, a crypto-native institution may have direct access to key payment infrastructure such as Fedwire—an “intruder” has obtained a ticket to the deepest part of traditional finance.

On March 18, the SEC officially approved Nasdaq Rule Amendment SR-NASDAQ-2025-072, opening a regulatory pathway for tokenized stocks to enter the mainstream U.S. market after a six-month review. Under the approved framework, tokenized securities and traditional securities will trade on the same order book on Nasdaq, sharing the same CUSIP code and real-time price. Holders will enjoy identical shareholder rights, including dividends and voting rights. The first batch of eligible securities will be limited to Russell 1000 index constituents and ETFs tracking major benchmarks such as the S&P 500 and Nasdaq 100. U.S. investors may see the first tokenized securities traded as early as the end of the third quarter of 2026.

In the same month, ICE/NYSE signed a memorandum of understanding with Securitize to build a complete market infrastructure covering securities registration, transfer agency, and tokenization issuance for tokenized securities. Previously, in January, ICE/NYSE had announced the development of a tokenized securities platform supporting 24/7 trading, instant settlement, and stablecoin funding channels. ICE's own capital operations are even more aggressive: in October 2025, it invested $1 billion in the prediction market Polymarket, followed by an additional $600 million in March 2026.

Also in March, BlackRock CEO Larry Fink stated explicitly in his annual letter to investors that the era of asset tokenization has only just begun. Franklin Templeton, which manages $1.7 trillion in assets, announced a partnership with Ondo that same month to launch a tokenized version of its ETFs.

The logic behind this series of actions is consistent: this is not a competition about "new products," but a war for control of the next generation of financial infrastructure. Nasdaq's release of the Equity Token Design framework attempts to set industry standards, just as SWIFT defined the information format for cross-border payments and the FIX protocol shaped the communication language of electronic transactions—whoever's framework becomes the industry's default option controls the gateway to the next generation of infrastructure.

1.2 Regulatory Turning Point: Securities are securities, but the channels have been opened.

From a regulatory perspective, the period from the end of 2025 to 2026 is a critical turning point. In December 2025, Depository Trust Companies (DTCs) received SEC approval to launch a tokenization pilot program, paving the way for the on-chain transformation of the US securities clearing system. On January 28, 2026, the SEC's Division of Corporate Finance, Division of Investment Management, and Division of Trading and Markets jointly issued a statement on tokenized securities, systematically defining the classification framework for tokenized securities for the first time. The core position is that the format of securities issuance or the method of recording holders (on-chain or off-chain) does not affect the applicability of federal securities laws— a security is a security .

This seemingly conservative stance actually clears away regulatory uncertainties for compliant players: as long as securities law requirements are met, tokenization itself does not constitute an additional obstacle. The statement also distinguishes between different tokenization models—from "native tokenization" where the issuer issues tokens directly on-chain, to "custodial tokenization" where a custodian holds the underlying securities and issues certificates on-chain, and then to tracking tools issued by third parties through SPVs—different models correspond to different rights structures and regulatory requirements, forming the basic framework for understanding the current market stratification.

But the regulatory boundary game is far from over. In May 2026, the SEC shelved its proposed "innovation exemption" framework at the last minute—a framework that would have allowed third-party-issued stock-tracking tokens to trade 24/7 on decentralized platforms. Intensive lobbying from industry organizations behind traditional exchanges like Nasdaq, Cboe, and CME led the SEC to postpone its release. This event reveals the core tension that will be discussed in detail in Chapter Six of this report: Wall Street welcomes "tokenization under its control" but is wary of "permissionless on-chain securities markets" —the latter being one of the prerequisites for the DeFi boom.

1.3 Core Arguments of this Report

Our core argument can be summarized in one sentence: Tokenized stocks are not the end game; they are merely the "asset deployment" phase of on-chain stock DeFi. The real value capture occurs in the second phase—once tens or even hundreds of billions of dollars of stock assets are deposited on-chain, lending, market making, derivatives, and structured products surrounding these assets will replicate the derivatives layer in traditional finance, which is several times larger than the spot market.

The logical chain is as follows: The current stage (asset on-chaining) addresses the question of "whether stocks can exist on the blockchain"; however, 24/7 trading and global accessibility alone are insufficient to persuade users to abandon mature brokerage systems—on-chain data has already proven this (see Chapter 2 for details). The only truly differentiating advantage of tokenized stocks compared to traditional shareholding is composability —the same asset can simultaneously serve as collateral, market-making funds, and derivatives margin, embedding itself into any financial protocol without intermediary approval. This is a capability that traditional securities account systems cannot physically provide, and it is the fundamental reason for the inevitable explosion of on-chain stock DeFi.

II. Current Status of the Stock Tokenization Market: Achievements and Bottlenecks of the First Phase

2.1 Market Size and Structure: From Proof of Concept to Real Market

The tokenized stock market has completed its transition from a "narrative" to a "real market" over the past year. In January 2026, the total market capitalization of tokenized stocks surpassed $1 billion for the first time, growing more than 50 times in the past year. At that time, xStocks (issued by Backed Finance and distributed through the Kraken system) held a 58.3% share with a market capitalization of over $600 million, followed closely by Ondo Global Markets.

By May 2026, the landscape had changed. Ondo Global Markets (launched in September 2025) surpassed $1 billion in TVL in less than eight months, becoming the first tokenized stock platform to reach this scale , holding over 70% market share by issuer count (RWA.xyz); its cumulative trading volume (across Solana, Ethereum, and BNB Chain) exceeded $18 billion, offering over 260 tokenized US stocks and ETFs. TVL has doubled since January 2026—from $500 million to $1 billion in just about four to five months.

The main players can be divided into three categories based on their "origin path":

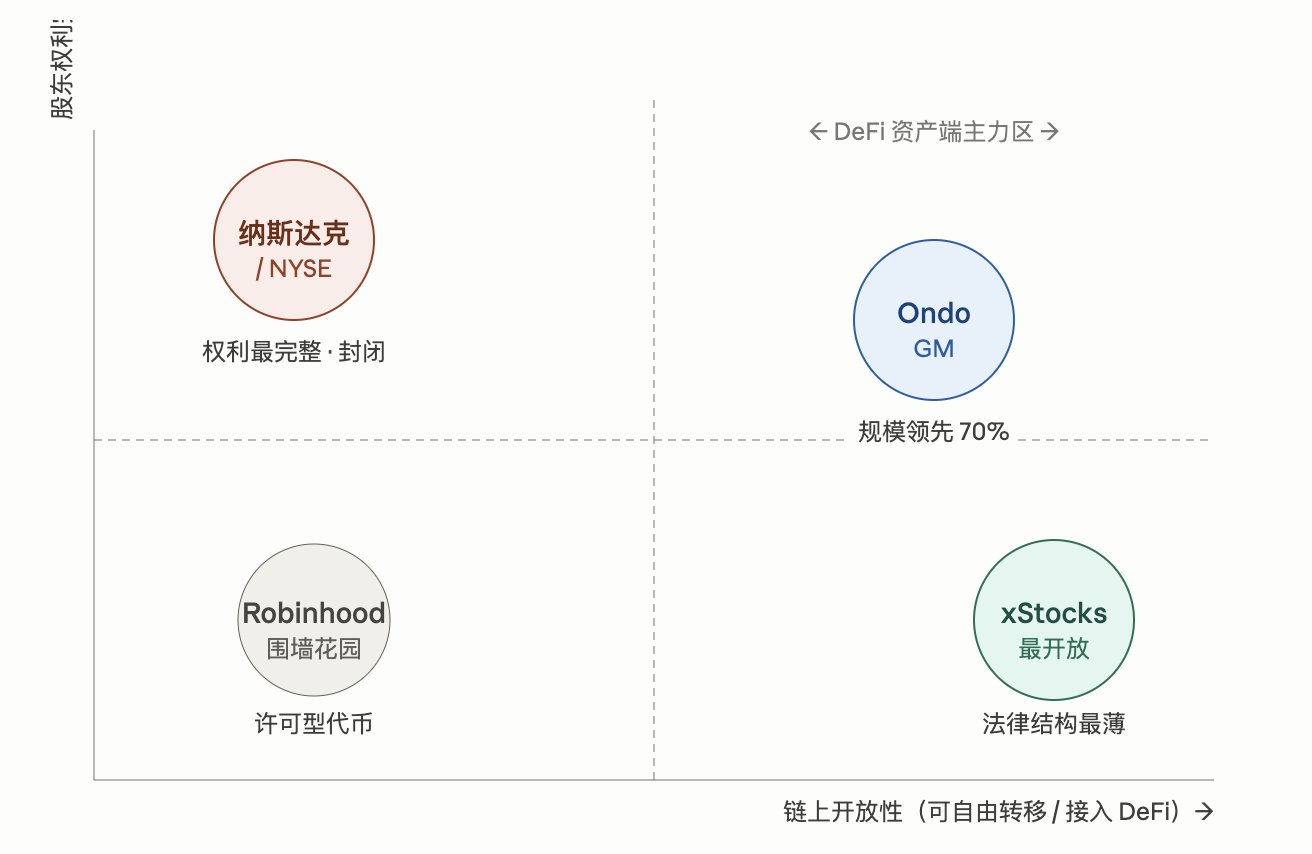

- The first category: Crypto-native issuers. Ondo Global Markets is a representative example. The team originated from Goldman Sachs' digital asset division and follows a "minting/redemption + multi-chain distribution" approach. It has already integrated with platforms such as Binance, Bitget, MetaMask, and Blockchain.com. In February 2026, Binance listed ten Ondo tokenized assets, including AAPlon, TSLAon, NVDAon, and QQQon, on Binance Alpha and Binance Wallet, directly reaching hundreds of millions of users. Ondo is also pursuing EU/EEA regulatory approval and SEC registration, and has established institutional settlement partnerships with JP Morgan, Mastercard, and Ripple. xStocks, issued by Backed Finance (Swiss background, EU compliant ISIN number), is distributed through a licensed entity of Kraken's subsidiary and deployed on multiple public chains such as Solana and Ethereum. By design, it is a freely transferable standard token—a technological prerequisite for its DeFi integration.

- The second category: Internet brokerages. Robinhood launched tokenized stocks in Europe, but it uses a permissioned token design: transfer restrictions are embedded in the contract, and each transaction requires verification through a whitelist registry. This is a typical "walled garden"—users gain 24/7 trading, but their assets cannot leave the Robinhood system, completely isolated from open DeFi protocols.

- The third category: Traditional exchanges. Nasdaq and NYSE represent the route "starting from within the traditional market infrastructure": instead of creating new assets, they bring the clearing and settlement of existing securities onto the blockchain, preserving full shareholder rights, and relying on DTCC's enterprise-grade blockchain. This route offers the most thorough compliance and the most complete shareholder rights, but it is also the furthest removed from the public blockchain DeFi ecosystem.

2.2 Real-world on-chain data reveals an on-chain market that is not yet "on-chain".

Bitget Wallet Research Institute's in-depth analysis of Ondo Global Markets based on Dune data (as of May 2026, covering Ethereum and BNB Chain, 180,000+ wallets, 2.8 million transactions, and $5.5 billion in transaction volume) reveals the most interesting truth about this market: even with the Web3 shell, this market still operates like traditional Wall Street, "clocking in and out" most of the time.

Despite the on-chain infrastructure providing 24/7 liquidity, approximately 52% of trading volume remains concentrated during regular US stock market trading hours; the much-anticipated "weekend stock trading" only accounts for 0.55% of total trading volume. Market activity is trending upward—reaching a historical peak of $1.38 billion in monthly trading volume in March 2026—but the "time zone distribution" of trading behavior reveals a crucial fact: the way users currently use tokenized stocks is virtually indistinguishable from using traditional brokerages.

2.3 Bottlenecks in the First Stage

Based on a comprehensive analysis of market structure and on-chain data, the first phase (pure asset on-chaining) faces three major bottlenecks:

Bottleneck 1: Limited Differentiated Demand. 24/7 trading sounds appealing, but pricing power remains largely concentrated during Nasdaq and NYSE opening hours—after-hours on-chain prices lack a spot market anchor, liquidity and slippage deteriorate significantly, and rational users naturally revert to "Wall Street time." For users who can already open US stock accounts, the core selling point of tokenized stocks is currently only "crypto assets and stocks in the same wallet."

Bottleneck Two: Liquidity Fragmentation. The same Apple stock exists in multiple, non-circulating tokens, such as the Ondo version (AAPLon), xStocks version (AAPLx), and Robinhood version, scattered across multiple blockchains including Solana, Ethereum, and BNB Chain. Each version is backed by a different issuance structure, custody arrangement, and redemption commitment, resulting in fragmented liquidity.

Bottleneck Three: The "Discount" of the Legal Structure. Taking xStocks as an example, its essence is a debt structure (a certificate tracking the underlying assets) rather than an equity token—the issuing entity is an SPV that does not require custody qualifications, and holders do not directly enjoy shareholder rights such as voting rights. Users receive "economic exposure" rather than "stocks themselves." This is ignored in a bull market, but in extreme situations, the ability to repay is a real tail risk.

2.4 Key Insight: Tokenized Stocks Without Composability ≈ Brokerage Firms with Changed Ledgers

Putting all these bottlenecks together, the conclusion is clear: if the sole function of tokenized stocks is "buy, hold, sell," then it is essentially no different from a 24/7 offshore brokerage, and lags far behind in investor protection and liquidity depth. This market will either remain confined to the limited scenario of "a convenient channel for crypto users to buy US stocks," or it will move towards the only direction that can create incremental value— making on-chain stocks programmable financial raw materials .

It's worth noting that the market has already begun to vote with its feet. On-chain data shows that while early DeFi integrations of tokenized stocks (see Chapters 4 and 5) are still small in scale—the Kamino xStocks collateral market has approximately $21 million in assets, and the Morpho SPYx market has approximately $7.9 million—the infrastructure is already live, and on-chain lending activity using stocks as collateral is truly taking place. The first domino has fallen.

III. Historical Mirror: Why We Believe the DeFi Boom Is Inevitable

The assertion that "the DeFi boom will follow tokenized stocks" is not a mere deduction. Over the past eight years, every type of underlying asset in the crypto industry has undergone almost identical evolutionary paths after being massively tokenized. We will use two historical analogies and a comparison with traditional finance to demonstrate this pattern.

3.1 Analogy 1: Stablecoins → DeFi Summer

Between 2017 and 2019, stablecoins (USDT and USDC) completed the "on-chaining of the US dollar." In the initial stages, stablecoins had a similarly limited purpose: fund transfers between exchanges and safe-haven asset allocation—essentially, "US dollars with a different ledger." The market at the time also questioned: what else could on-chain US dollars do besides cryptocurrency trading and settlement?

The answer was revealed in 2020. As the on-chain dollar reserves accumulated to a sufficient scale, lending markets like Compound and Aave, along with AMMs like Uniswap and Curve, transformed them into interest-bearing assets and market-making funds. The DeFi Summer boosted total locked value in DeFi from approximately $1 billion to tens of billions of dollars within months. The key wasn't that stablecoins themselves changed, but rather that the composable protocol layer surrounding stablecoins matured . Today, the vast majority of on-chain value capture for stablecoins occurs at the derivative layer (lending spreads, market-making revenue, yield aggregation), rather than the transfer itself.

Tokenized stocks are currently in a position similar to stablecoins in 2019: assets are on-chain, stock is rapidly accumulating (US$1 billion TVL, a 50-fold increase year-over-year), and the protocol layer is beginning to tentatively integrate.

3.2 Analogy 2: ETH → LSD and the Restaking Ecosystem

The second analogy is the Liquidity Staking Derivatives (LSD) wave of 2021-2023. After ETH transitioned to PoS, staked ETH was essentially a "locked-up" asset; protocols like Lido tokenized it (stETH), allowing the staked asset to regain liquidity and be embedded in lending and market making. As a result, stETH became one of the largest collateral categories on Aave, further spawning a restaking ecosystem represented by EigenLayer. A single underlying asset (ETH) was repeatedly "refinancialized" by derivative layers, each layer creating independent protocol value and fee revenue.

The implication of this analogy is that stagnant assets are the best raw material for DeFi . Tokenized stocks are precisely a typical stagnant asset—the default behavior of holders is to hold them for the long term (blue-chip stocks, index ETFs). This part of the "static" asset naturally craves activation: collateralized borrowing without selling, lending to earn fees, and using cover put options to enhance yield. Traditional finance has built a huge industry for these needs (see 3.3), and there is no reason for the on-chain world to be an exception.

3.3 Comparison with Traditional Finance: Derivative Demand is Real and Huge

On-chain stock DeFi doesn't need to "create" demand; it only needs to absorb demand that has been validated in traditional finance for over a century. Three sets of figures are enough to illustrate the size of this market:

Margin trading. According to FINRA data, US investor margin debt first surpassed $1 trillion in June 2025 and reached a historical peak of approximately $1.3 trillion in early 2026, representing a year-on-year growth of over 50%. This means that in the US market alone, "borrowing money against collateral" represents a trillion-dollar existing business – and this is precisely the most mature product form of on-chain collateralized lending protocols (Aave, Morpho, Kamino).

Securities lending. According to the International Securities Lending Association (ISLA), the global securities lending market (including stocks and fixed income) had an outstanding loan balance of approximately €2.4 trillion at the end of 2020, with a pool of assets available for lending exceeding $13 trillion. Earning fees through securities lending is essentially a mirror image of the "deposit assets to earn interest" business in DeFi.

Equity derivatives. The notional size of global equity derivatives (options, futures, total return swaps) is several times that of the spot market, and the options market has continued to set trading records in recent years, driven by retail investors. On-chain perpetual contract protocols (such as Hyperliquid) have proven the product-market fit of on-chain derivatives on crypto assets. Expanding the underlying asset from BTC/ETH to tokenized stocks is merely an engineering problem, not a demand problem.

Conclusion: In traditional finance, revenue from the "derivative layer" surrounding stocks (financing interest, borrowing fees, derivatives market-making and clearing fees) far exceeds revenue from "spot brokerage"—this is precisely why brokerages can operate with zero commission. The ultimate outcome for tokenized stocks will inevitably be the same: free spot trading and value capture through the derivative layer .

3.4 Deductive Framework: Four-Stage Model

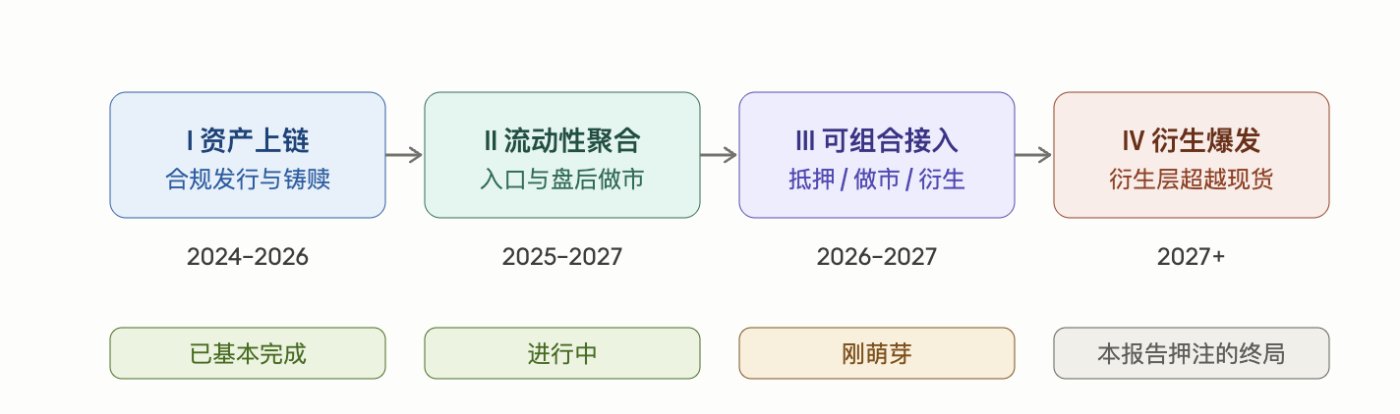

Based on the above analogies, we propose a four-stage deductive framework for the tokenized stock market:

- Phase I: Asset Tokenization (2024-2026) : Solving compliant issuance, custody, and redemption channels. Landmark events: Total market capitalization exceeding $1 billion, Nasdaq approval, and full participation from Wall Street. — Currently largely complete.

- Phase II Liquidity Aggregation (Liquidity, 2025-2027) : Solving the "fragmentation" problem. CEX entry point (Binance Alpha), DEX deep market making, cross-issuer liquidity bridging, and a mature after-hours pricing mechanism. —In progress.

- Phase III Composability (2026-2027) : Tokenized stocks are accepted as collateral by mainstream lending protocols, enter AMM pools, and are integrated into derivatives protocols. Key indicator: Stock-based collateral in a single lending protocol surpasses $100 million and then $1 billion. — Just emerging (currently totaling tens of millions of US dollars).

- Phase IV: DeFi Explosion (starting in 2027) : A complete ecosystem will form around on-chain equity lending, options vaults, structured products, and index protocols, with the TVL of the derivative layer exceeding the TVL of the spot layer. — This report bets on the final outcome.

Historical experience shows that the transition time from Phase I to Phase IV is 12-24 months (stablecoins 2019→2020, LSD 2021→2022). Taking 2026 as the base year for the completion of Phase I, we expect 2027 to be the "first year of access" for on-chain equity DeFi, with 2028 marking a period of large-scale explosive growth.

IV. Breakdown of Core Scenarios of On-Chain Stock DeFi

This chapter breaks down the six core scenarios of on-chain stock DeFi one by one, and assesses the demand intensity, technological maturity and current progress of each scenario.

4.1 Collateralized Lending: On-chain "Stock Pledge Financing"

This is the scenario with the highest certainty and the clearest demand anchor. The corresponding counterpart in traditional finance is margin trading and stock-backed loans, with US margin debt alone reaching $1.3 trillion. The core demand of users is "to obtain liquidity without selling stocks": long-term holders pledge AAPLON to borrow stablecoins for consumption, reinvestment, or tax planning.

Current developments validate the authenticity of the demand: Kamino, the largest lending protocol on Solana, has launched a collateral market for seven xStocks (SPYx, TSLAx, QQQx, NVDAx, GOOGLx, MSTRx, and AAPLx), with a size of approximately $21 million; the SPYx market on Morpho has approximately $7.9 million; and Aave is exploring RWA collateralized lending through its permissioned institutional marketplace Horizon (size of $161 million, 256 addresses, average holding of $1.5 million), achieving a stablecoin utilization rate of 77%.

The current small scale is not due to insufficient demand, but rather supply-side constraints: the stock of equity tokens available for collateral is only in the $1 billion range, and mainstream protocols are extremely conservative in their risk control parameters (LLTV, liquidation threshold) for new collateral. This scenario will be the first to scale up as Phase II liquidity aggregation progresses. We expect collateralized lending to account for over 60% of early-stage TVL in on-chain equity DeFi , replicating stETH's growth path on Aave.

Key design challenge: Clearing mechanisms during stock market closures. When underlying stocks close on Friday, on-chain collateral prices are frozen, or pricing relies on scarce after-hours liquidity, weekend events (earnings reports, geopolitical events) can cause gap liquidations at Monday's opening. Solutions include lower LTV, after-hours oracle discount mechanisms, and off-exchange clearing arrangements with market makers—this is where the value of professional risk management service providers (such as the Morpho vault manager model) lies.

4.2 AMM and On-Chain Market Making: The Real Solution for 24/7 Liquidity

Chapter Two points out that 24/7 trading is currently a false demand—the fundamental reason being the lack of liquidity after hours. AMMs offer a structural solution: passive liquidity pools don't require market makers to be "on duty," providing basic depth after hours and over the weekend. xStocks has integrated with the Solana DEX ecosystem, including Raydium and Jupiter; Ondo GM has accumulated $18 billion in trading volume across CEX, DEX, and minting/redemption channels, and provides liquidity outside of the 24/5 hours of Nasdaq and NYSE trading.

However, stock AMMs have a unique problem: adverse selection under known information . Stocks accumulate information during market closure (earnings report releases), and the price jumps instantly at the opening. Arbitrageurs can instantly drain the liquidity of the "expired price" in the AMM pool, causing limited partners (LPs) to suffer a deterministic loss (an extreme form of the LVR problem). Therefore, the design of stock AMMs will differ from that of crypto asset AMMs: oracle-anchored pools (similar to Curve V2) and "trading period-aware" pools that automatically pause or widen spreads at market close will become the mainstream design. This is a noteworthy direction for protocol innovation.

4.3 Derivatives: On-chain Stock Perpetual Contracts and Options

Crypto perpetual contracts are the most proven profitable sector in DeFi. Expanding the underlying assets to include stocks means gaining exposure without holding the underlying assets—bypassing the full complexities of issuance, custody, and redemption, relying solely on oracle price feeds. In fact, crypto platforms have already launched contract trading for popular US stocks such as AMD, and perpetual contracts for gold, silver, and oil have also appeared, demonstrating the initial validation of retail investors' demand for "24/7 trading exposure to traditional assets."

Synthetic exposure (perpetual contracts) and physically backed (spot tokens) will coexist and complement each other in the long term: perpetual contracts provide leverage and short tools, while spot tokens provide collateral and real holdings; the arbitrage of funding rates between the two, in turn, creates institutional demand for spot tokens (similar to the Ethena model: holding spot tokens + short perpetual tokens to earn funding fees). We suggest a specific direction: delta-neutral yield products that use tokenized stocks as collateral and charge funding fees may become a blockbuster category connecting these two routes.

At the options level, on-chain options protocols have yet to achieve scale in crypto assets, but stock options are the derivatives with the highest retail investor participation in traditional markets. The on-chain covered call vault (holding AAPLON and rolling out call options to enhance returns) has a simple product structure and intuitive returns, making it suitable as an entry point into the options market.

4.4 Enhanced Returns and Structured Products

Tokenized stocks combined with DeFi yield instruments can be used to create structured products that traditional brokerages typically require high net worth thresholds to offer: automatic dividend reinvestment (an on-chain native version of DRIP), snowball structures, and dual-currency wealth management (mutual subscription of stocks/stablecoins). In terms of issuance structure, these products are naturally suited to the vault model—users deposit a single asset, the strategy contract executes automatically, and Morpho/Kamino's vault infrastructure can be directly reused.

4.5 Indices and Portfolio Assets: The Original Form of On-Chain ETFs

On-chain index protocols can do what traditional ETFs cannot: real-time transparent composition and net asset value, unlimited subdivision of minimum units, no Authorized Participant (AP) system for creation and redemption, and cross-asset class mixing (a "one-click all-day portfolio" of 50% US stock seven giants + 30% BTC/ETH + 20% tokenized government bonds). Franklin Templeton's partnership with Ondo to issue a tokenized ETF signals the entry of traditional asset management; while crypto-native index protocols may move from "on-chain mirrors of traditional ETFs" to "on-chain native indices"—this is the value capture point of asset management fees (management fees + creation and redemption fees) on the blockchain.

4.6 Cross-industry collaboration: The final piece of the puzzle for on-chain full asset allocation

Tokenized government bonds (BlackRock BUIDL, with a scale of approximately $1.83 billion, has been used as collateral for the Ethena USDtb stablecoin) have solved the problem of "risk-free interest rates" on-chain, stablecoins have solved the problem of "cash," and tokenized stocks have filled the gap in "equity assets"—thus, for the first time on-chain, all the raw materials for building a complete multi-asset portfolio are available. For investors worldwide who cannot easily access the US brokerage system, completing the full allocation and rebalancing of "cash—government bonds—stocks—crypto assets" within a single wallet is an experience that the traditional financial system cannot provide. The potential of this scenario lies not in a single protocol, but in the emergence of on-chain private banking/robo-advisory models.

The scenario priorities are summarized and sorted by "demand certainty × infrastructure readiness": Mortgage lending > Perpetual contracts > AMM market making > Yield vaults > Index protocols > Total asset allocation. The first three will define the competitive landscape in 2026-2027, while the latter three represent the depth beyond 2028.

V. Infrastructure and Key Player Map

5.1 Issuance Layer: The Source Determining Asset Quality

5.2 Transaction/Distribution Layer

Distribution determines scale. Binance's introduction of Ondo tokenized shares to Alpha and Wallet in February 2026 was the largest single distribution event to date—reaching hundreds of millions of users far exceeding any native DeFi entry point. Kraken has built a vertical integration of "crypto exchage+ banking infrastructure" through xStocks and access to Federal Reserve accounts. On the traditional side, Nasdaq and NYSE's on-chain platforms are expected to gradually roll out from the end of Q3 2026, bringing tokenized securities to traditional brokerage clients—but as mentioned above, this traffic will most likely remain within closed systems.

5.3 DeFi Protocol Layer: Who's Positioning Themselves?

The protocols that have already implemented tokenized stocks constitute the "first tier": Kamino (Solana's largest lending protocol, with $587 million in RWA collateral, including $21 million in the xStocks market), Morpho (a permissionless market architecture naturally suited for isolating risk pricing of long-tail collateral, with $7.9 million in the SPYx market, $8 billion in TVL, and integrated by institutions such as Coinbase), and Aave Horizon (a permissioned RWA market with $161 million).

It's worth noting an early experimental result from Aave Horizon: when the crypto arbitrage fund token USCC offered approximately 15% APY, it accounted for 93% of all RWA collateral, while government bond products launched at the same time received almost no interest. This illustrates that on-chain funds naturally chase "yield differentials + leverage" rather than "security narratives" —good news for tokenized stocks: stock volatility and the demand for leveraged long are precisely the engines driving the utilization of lending protocols.

On the derivatives side, on-chain perpetual platforms such as Hyperliquid possess the strongest ability to "expand product categories"; on the oracle side, Chainlink has provided price feeds and proof-of-reserves (PoR) for xStocks, and RedStone and others are also actively positioning themselves— oracles are an undervalued part of stock DeFi , and the data services for after-hours pricing, suspension processing, and corporate actions (stock splits/dividend ex-rights) are far more complex than price feeds for crypto assets, making pricing ability a moat.

5.4 The Public Blockchain Debate

Current Landscape: Solana is the de facto home turf for stock DeFi (xStocks main battlefield + Kamino/Raydium/Jupiter ecosystem + Ondo deployment), with low fees and high throughput suitable for high-frequency trading scenarios; Ethereum hosts institutional and large-scale transactions (Ondo's Ethereum deployment, Aave Horizon, and BUIDL main positions); BNB Chain is rapidly scaling up through Binance distribution (Ondo's market capitalization on the BNB Chain has exceeded $50 million). We believe the dual-center structure of "Solana for trading and retail DeFi, Ethereum for institutional and settlement" will continue. The real variable is whether Nasdaq/DTCC enterprise chains will open up interoperability with public chains in the future.

5.5 Liquidation and Corporate Behavior Infrastructure

The on-chain automated processing of corporate actions such as dividends, stock splits, mergers, and delistings is currently the weakest link—issuers handle these manually in a centralized manner (adjusting token balances or airdrop compensation). Standardization of this link (which the Nasdaq Equity Token Design framework attempts to cover) is a prerequisite for large-scale institutional investment in equity DeFi and also a potential direction for startups/investments.

VI. Key Obstacles and Risks

6.1 Regulation: The Biggest Variable in Timing

The core question remains: Will the SEC allow "security tokens" to enter permissionless DeFi protocols? The shelving of the "innovation exemption" framework in May 2026 is a clear warning signal—traditional exchanges will use all their lobbying power to prevent the circulation of on-chain securities that bypass their systems. Three scenarios:

- Scenario A (Optimistic, 30% probability) : The revised innovation exemption framework is implemented in the second half of 2026-2027, granting third-party tracking tokens compliant status for 24/7 decentralized trading. Stock DeFi explodes within the US regulatory framework.

- Scenario B (Baseline, 50% probability) : The US maintains a strict stance that "securities are securities," and permissionless DeFi access remains restricted in the US; however, offshore markets (xStocks/Ondo models under the EU MiCA framework, targeting non-US users) continue to grow, and stock DeFi develops in a form that is "primarily offshore, supplemented by KYC-compliant DeFi." This means that permissioned DeFi like Aave Horizon and segregated markets like Morpho will be the main channels for institutional funds.

- Scenario C (pessimistic, 20% probability) : A major risk event (issuer default/liquidation spiral) triggers global regulatory tightening, restricting on-chain stocks to exchanges, and delaying the DeFi boom until after 2029.

It is worth emphasizing that even under the baseline scenario, the arguments in this report still hold true—non-US investors (the existing target customer base of Ondo and xStocks) constitute the entirety of the current market, and KYC-compliant DeFi ("compliant composability") is an undervalued middle ground.

6.2 Structural Risk: What exactly are you holding?

xStocks' debt certificate structure means that holders are creditors, not shareholders, of the issuing SPV; Ondo's minting and redemption model relies on custodians and the management of cash in transit. Redemption capacity under extreme market conditions, the fee trap of SPVs (management fees erode tracking accuracy), and custodian credit are common tail risks for all physically backed tokens. When these tokens further become collateral in DeFi, the issuer's credit risk is amplified through lending protocols —a single redemption crisis could trigger a chain of liquidations across protocols. From a risk control perspective, setting a cap on the exposure of DeFi protocols to collateral from a single issuer is a necessary discipline.

6.3 Technological Risks: The Unique Liquidation Challenges of Stocks

Three new problems that crypto DeFi doesn't have:

- Market close gap liquidation – Information accumulated over the weekend is released instantly at the opening of trading on Monday, potentially causing the collateral ratio to plummet below the liquidation line, leading to bad debts;

- Oracle manipulation window – with scarce on-chain liquidity after hours, the cost of manipulating spot prices to trigger liquidation has decreased significantly;

- Mismatch in corporate behavior – If the oracle and token balance adjustments are not synchronized on the stock split/ex-rights date, it will cause systemic erroneous liquidation.

These issues determine that the risk control parameters for stock collateral will be significantly more conservative than those for mainstream crypto assets in the foreseeable future (lower LLTV, higher liquidation penalties), and also determine that risk control innovation based on "trading time perception" is a real protocol-level opportunity.

6.4 Liquidity Cold Start

The DeFi flywheel requires initial liquidity: without depth, there is no reliable liquidation; without reliable liquidation, there is no lending market; and without lending demand, there are no LP rewards. The force that breaks this cycle most likely comes from issuer subsidies (Ondo has the strongest incentive to expand its own DeFi use cases) and the on-chain extension of CEX market makers. Observing whether Ondo launches an "OGM Asset DeFi Incentive Program" is a concrete leading indicator.

VII. Market Space Calculation and Timeline Projection

7.1 TAM Measurement

We use the "traditional benchmarking × on-chain penetration rate" framework for three-layer calculations:

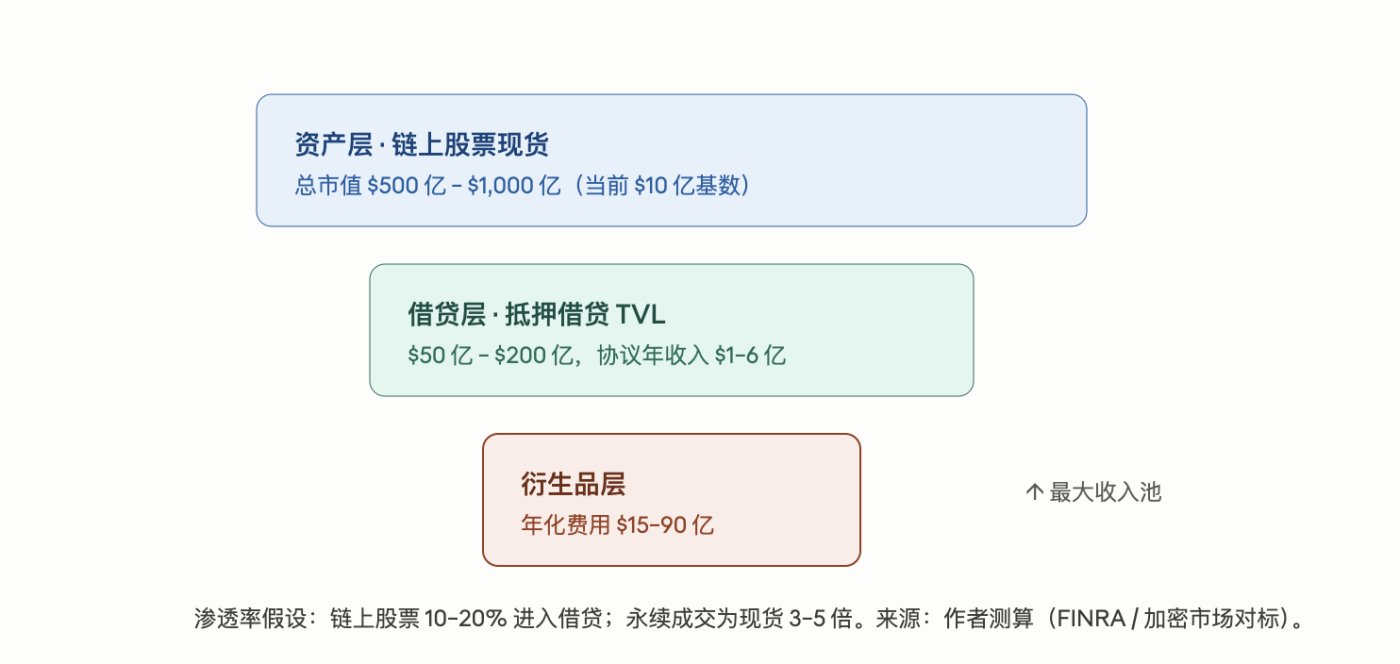

- Asset Layer (Total Market Capitalization of Tokenized Stocks) : The global stock market capitalization is approximately US$120 trillion. Assuming that 0.5%–1% of tokenized stocks complete open tokenization by 2030 (referring to the penetration trajectory of stablecoins in M2), this corresponds to US$600 billion–1.2 trillion. Under a neutral assumption, it will reach US$50 billion–100 billion by 2028 (from the current base of US$1 billion, continuing but slowing the growth rate by 50 times/year → 8–10 times/year).

- Lending Layer : The US margin debt/stock market capitalization ratio is approximately 2%-4% (US$1.3 trillion/approximately US$50 trillion US stock market capitalization). On-chain users have a higher risk appetite. Referring to stETH's 20%+ collateralization penetration in lending protocols, assuming 10%-20% of on-chain stocks enter the lending protocol, this corresponds to a lending TVL of US$5 billion-20 billion in 2028. Based on a net interest margin of 2%-3%, the protocol layer's annual revenue would be US$100 million-600 million.

- Derivatives Layer : The trading volume of perpetual contracts in the crypto market is approximately 3-5 times that of spot trading. If the average daily trading volume of on-chain stock spot reaches $500 million to $1 billion (neutral assumptions for 2028; the current monthly peak on the Ondo single platform is $1.38 billion), the average daily trading volume of the perpetual layer will be $2 billion to $5 billion. At a fee rate of 0.02% to 0.05%, the annualized fee revenue will be $1.5 billion to $9 billion —this is the largest revenue pool in the entire ecosystem.

7.2 Three-Phase Timeline

- 2026: The Year of the Asset On-Chain Race. Nasdaq's tokenized settlement went live at the end of Q3; Ondo/xStocks' total market capitalization approached $3-5 billion; distribution channels such as Binance continued to expand; the game of innovation exemption frameworks was set in motion.

- 2027: The Year of DeFi Integration. Mainstream lending protocols saw equity collateral surpass $1 billion; the first large-scale on-chain perpetual equity platform emerged; the "time-aware" design of equity AMMs matured; and the first batch of covered call/delta neutral vault products began to take off.

- 2028+: On-chain capital markets take shape. Derivative layer TVL surpasses spot TVL; tokenized ETFs from traditional asset management directly compete with native on-chain index protocols; clearing/corporate behavior infrastructure is standardized; the first "native on-chain IPO" may occur.

7.3 Summary of Scenario Analysis

Optimistic Scenario (Innovation Exemption Implemented + No Major Risk Events): Total TVL of Equity DeFi to $30 billion+ by 2028;

Baseline scenario: $10 billion to $15 billion;

Pessimistic scenario (tighter regulation/payout crisis): <$3 billion and stagnant growth.

Even with probability weighting, this remains an asymmetric opportunity with extremely high expected value—because the current market pricing of the entire sector (issuance + protocol) hardly takes into account any value of the derivative layer.

VIII. Investment Logic and Target Mapping

8.1 Beneficiary Tier Ranking

The first beneficiary layer: the issuers. Asset size is the foundation of all derivative businesses, and the issuer layer has already shown a winner-takes-all phenomenon (Ondo holds 70% of the market share). Issuers also hold the dominant power in "DeFiizing their own assets"—Ondo is both an asset issuer and a channel and market maker for stock DeFi, and its business model can be expanded in three dimensions: custody fees + minting and redemption fees + ecosystem extraction.

The second beneficiary layer: compliance and infrastructure. Securitize (whose backdoor listing has been approved by the SEC and is about to be listed on the NYSE, and is tied to the NYSE/BlackRock ecosystem) represents the "water seller" logic; oracles (Chainlink and Challenger) benefit from the complexity premium of stock data services; clearing and corporate behavior services are a blank area where there is no clear leader yet.

The third beneficiary layer: DeFi protocols. Priority given to established players: Kamino (Solana's early stock collateralization), Morpho (isolated market architecture + institutional integration), and Aave (Horizon's permissioned gateway). On the derivatives side, focus on the expansion of stock categories by leading perpetual platforms. This layer offers the greatest flexibility, but the competitive landscape is still undetermined.

The fourth beneficiary layer: public chains. Solana (the main platform for retail stock DeFi) and BNB Chain (distributed by Binance) benefit more than Ethereum, but the value capture of the public chain layer is diluted by multiple ecosystems, resulting in the lowest elasticity.

8.2 Targets to Watch (Illustrative, not investment advice)

Secondary Market: ONDO (the leading issuance layer; note that its price has partially reflected the issuance narrative but not yet the DeFi narrative), MORPHO/AAVE/KMNO (protocol layer), LINK (data layer), SOL/BNB (public chain layer); Stock Market: Securitize (listed after listing), vertically integrated exchanges such as Coinbase/Kraken (if listed), ICE/Nasdaq (traditional side options).

Primary Market: Stock AMM design, time-period-aware risk control, automated corporate behavior, and on-chain structured product issuance—these four areas currently have almost no established players.

8.3 Key Observation Indicators

On the asset side: the total market capitalization of tokenized stocks exceeded US$5 billion; the market capitalization of a single asset (such as AAPlon) exceeded US$500 million.

In the DeFi space: equity collateral on a single lending protocol surpasses $100 million (the most important leading indicator, currently around $30 million) ; Aave's main market (excluding Horizon) launches its first equity collateral; leading perpetual platforms launch equity assets and their holdings enter the top ten.

Regulatory side: The innovation exemption framework has been restarted; the first US-licensed platform has been approved to offer freely transferable stock tokens to US users. Liquidity side: After-hours/weekend trading volume increased from 0.55% to over 5% (indicating genuine on-chain demand).

IX. Conclusion

Wall Street's foray into stock tokenization is often interpreted as a victory narrative of "traditional finance embracing blockchain." This report takes the opposite perspective: the tokenization efforts of Nasdaq and NYSE are defensive —using their own ledger upgrades in exchange for control over next-generation infrastructure standards, keeping tokenized securities within their walls. The offensive force, however, lies outside those walls: open-access tokenized stocks are accumulating at a rate of 50x per year and have already begun to infiltrate lending protocols.

History doesn't simply repeat itself, but the story of stablecoins and LSD provides a clear enough rhyme: when an asset class completes its on-chain deployment and accumulates to a critical scale, the explosion of the derivative financial layer surrounding it is only a matter of time—because the capital efficiency gains brought about by composability are something no walled garden can provide. Today, the total size of on-chain stock DeFi is only tens of millions of dollars, while opposite it stands a $1.3 trillion margin trading market and a multi-trillion dollar securities lending and derivatives market. This gap is the opportunity itself.

Our timeline is as follows: asset deployment completed in 2026, DeFi access ramp-up in 2027, and the derivatives layer surpassing the spot layer in 2028. The biggest risk is regulatory blockade of permissionless DeFi, but even in a restricted scenario, offshore markets and KYC-compliant DeFi are sufficient to support the weak form of our argument. For investors, the core contradiction at this juncture is that the market is still pricing this sector based on the "scale of tokenized stock issuance," rather than pricing it based on the "on-chain stock financial system."