If Hong Kong in the past was a paradise for crypto adventurers, then Hong Kong in the future will belong to industry players who pay attention to rules and regulations.

Written by: Gu Jiening

Thanks to the loose regulatory environment and favorable tax policies, as well as the huge geographical advantage of being backed by the mainland, Hong Kong, a global financial center that requires money and rich people, was once favored by the encryption industry. Today, under the escort of the Hong Kong government's comprehensive plan, pragmatic spirit, flexible body and determination to land, Hong Kong "Return of the King" is committed to becoming a global encrypted financial center.

If you want to wear a crown, you must bear its weight. Hong Kong may be a huge opportunity for Web3.0 practitioners, but not for everyone. Only on the basis of meeting regulatory requirements, can centralized virtual asset exchanges share the huge opportunities in this market.

1. Voluntary licensing system

For virtual asset trading platforms, the SFC introduced a regulatory framework for virtual asset trading platforms in 2019, and made detailed regulations in the "Position Paper - Supervision of Virtual Asset Trading Platforms" (hereinafter referred to as the "Position Paper").

The Position Statement stipulates that the CSRC has no right to license or supervise platforms that only trade non-securities virtual assets or tokens. Because such virtual assets do not belong to "securities" or "futures contracts" under the Securities and Futures Ordinance, and the business operated by these platforms does not constitute "regulated business" under the Ordinance. Therefore, under the "Voluntary Licensing System", if it is a virtual asset trading platform engaged in non-security tokens, it does not need to be licensed.

In fact, the "Position Statement" is in line with SFC's 2017 "Circular on Publishing the Regulatory Sandbox of the Securities Regulatory Commission" to adopt a regulatory sandbox position for innovation in the "financial technology" field, and it is also its specific implementation in the field of encrypted finance. move. In 2018, the SFC further formulated the "Statement on the Regulatory Framework for Virtual Asset Portfolio Management Companies, Fund Distributors and Trading Platform Operators" (hereinafter referred to as the "Regulatory Framework").

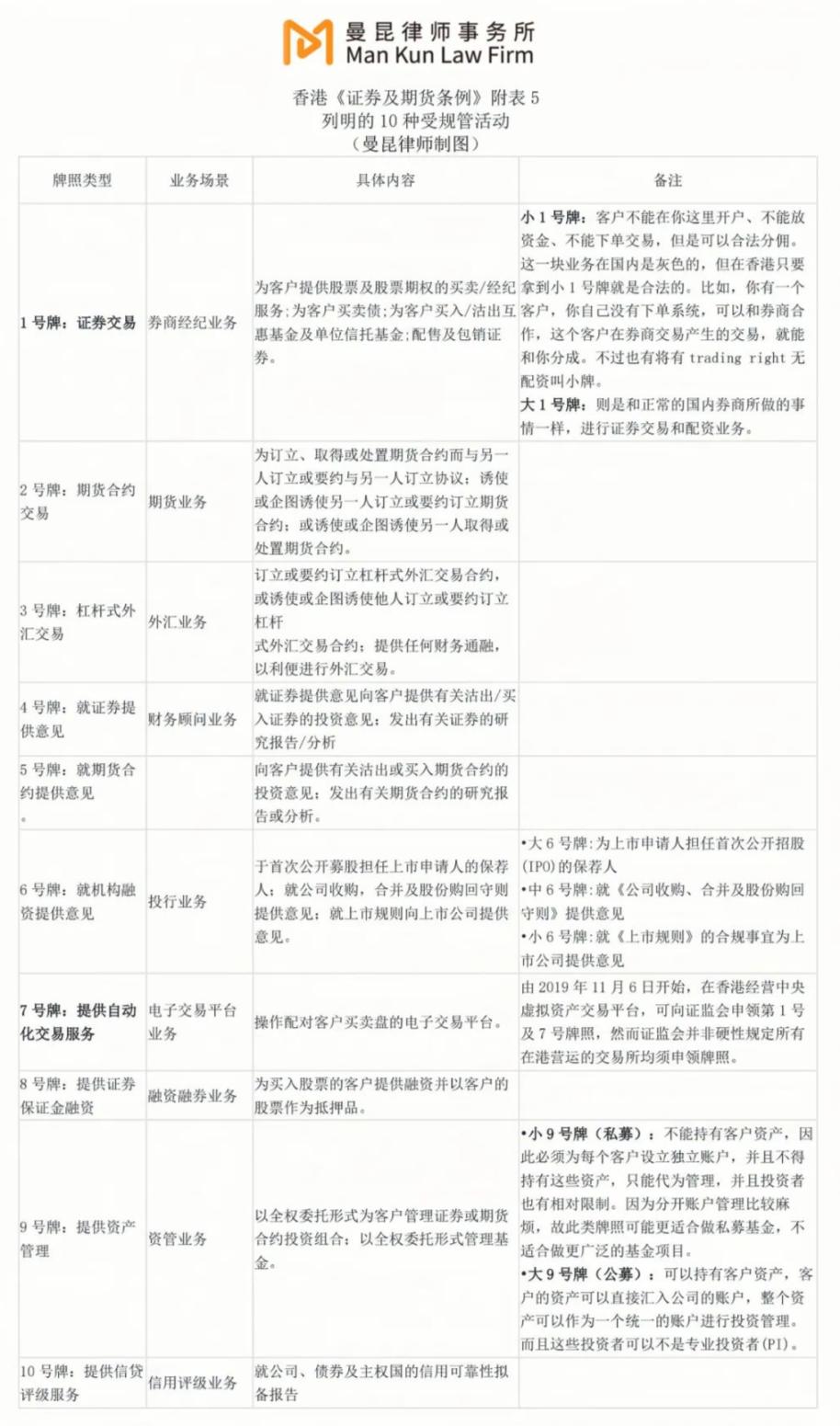

According to the Position Paper, if a central platform that provides virtual asset trading services intends to provide trading services for at least one security token, it may apply to the China Securities Regulatory Commission for Type 1 (securities trading) and Type 7 (providing automated trading services). Services) license for regulated activities. The regulatory framework includes strict standards in custody of assets, cyber security, anti-money laundering, market surveillance, accounting and auditing, product due diligence and risk management.

The SFC also specifically stated that only virtual asset trading platforms (that is, centralized virtual asset exchanges) that provide virtual asset trading, settlement and delivery services and have control over investor assets are regulated. SFC will not accept license applications from platforms that only provide trading services on direct peer-to-peer markets, and whose investors generally retain control of their own assets (whether fiat currency or virtual assets) (i.e. decentralized virtual assets Exchanges are not regulated by the SFC) . In addition, if the platform conducts virtual asset transactions (including sending buying and selling instructions) for customers, but the platform itself does not provide automated trading services, the SFC will not accept their license applications.

So far, only two exchanges have obtained the above two licenses. At the end of 2020, OSL Digital Securities Limied, a subsidiary of BC Technology Group, obtained the No. 1 and No. 7 licenses. It is the first compliant and licensed virtual asset exchange in Hong Kong. In April 2022, Hash Blockchain Limited, a subsidiary of HashKey Group, became the second virtual asset exchange to obtain the No. 1 and No. 7 licenses. Although the number of asset management companies that have obtained the No. 9 license is slightly larger, there are only 6 institutions including Huobi Asset Management, Lion Global Asset Management, MaiCapital, and Fore Elite Capital.

However, licensed entities under the "Voluntary Licensing System" can only provide services to professional investors. For most virtual asset exchanges that focus on the "retail" market, the No. 1 and No. 7 licenses are not practical due to their lack of practicality. Not very attractive. And this highlights the "preciousness" of the VASP license that will be issued in June this year.

2. VASP Licensing System

On December 7, 2022, the "Anti-Money Laundering and Counter-Terrorist Financing (Amendment) Bill 2022" (hereinafter referred to as the "Anti-Money Laundering Ordinance") was passed by the Hong Kong Legislative Council for implementation and will be implemented on June 1, 2023 Licensing system for virtual asset service providers (hereinafter referred to as "VASP licensing system").

The following table is a simple comparison of the old and new licensing systems in Hong Kong summarized by the author:

3. Dual License

According to different regulatory authorizations, SFC will supervise the security token transactions conducted by virtual asset trading platforms in accordance with the current system under the Securities and Futures Ordinance; The provider system supervises the non-security token transactions conducted by the virtual asset trading platform.

Given that the terms and characteristics of virtual assets may evolve over time, the classification of a virtual asset may change from a non-security token to a security token (and vice versa). According to the above regulatory logic, in order to avoid violating the requirements of any licensing system and ensure the continuous operation of the business, the virtual asset trading platform should simultaneously comply with the existing system under the Securities and Futures Ordinance and the provision of virtual asset services under the Anti-Money Laundering Ordinance. or system application approval (that is, apply for VASP license and No. 1 and No. 7 licenses at the same time), so as to obtain double licensing and approval.

To simplify the application procedure for dual licenses, applicants who want to apply for a license under both the current regime under the Securities and Futures Ordinance and the virtual asset service provider regime under the Anti-Money Laundering Ordinance need only submit a comprehensive online Application form, and indicate that the two licenses should be applied for at the same time.

The SFC expects that only one notification for a dual-licensed platform operator will be sufficient to comply with the licensing or notification requirements of the existing regime under the SFO and the virtual asset service provider regime under the AMLO .

4. Compliance requirements of exchanges

According to the "Guidelines for Operators of Virtual Asset Trading Platforms" and "Terms and Conditions for Operators of Virtual Asset Trading Platforms" issued by SFC, centralized virtual asset exchanges need to meet the following compliance requirements when operating.

1. Securely keep customer assets

The Platform Operator should hold client monies and client virtual assets on trust through a wholly-owned subsidiary (i.e. an "associated entity"). Platform operators should ensure that no more than 2% of customers' virtual assets are stored in online wallets.

In addition, since access to virtual assets can only be done through the use of private keys, the custody of virtual assets basically requires the safe management of the relevant private keys. Platform Operators should establish and implement written internal policies and governance procedures for private key management to ensure that all encryption seeds and keys are securely generated, stored and backed up.

In addition, platform operators should not deposit, transfer, lend, pledge, re-pledge, or otherwise buy or sell customer virtual assets, or create any encumbrances on customer virtual assets. It must also be insured, and its coverage should cover the risks involved in the custody of customers' virtual assets.

2. Know Your Customer (KYC)

The Platform Operator shall take all reasonable steps to establish the true and full identity, financial status, investment experience and investment objectives of each of its clients.

In addition, platform operators must ensure that customers have sufficient knowledge of virtual assets (including an understanding of the risks involved) before providing any services to customers.

3. Anti-money laundering/terrorist financing

Platform Operators should establish and implement adequate and appropriate AML/CFT policies, procedures and controls. Platform operators can use virtual asset tracking tools to trace the records of specific virtual assets on the blockchain.

4. Conflict of interest

Platform operators should not engage in proprietary trading or self-operated bookmaker activities, and should have policies to manage internal employees' transactions in virtual assets to eliminate, avoid, manage or disclose actual or potential conflicts of interest.

5. Include virtual assets for trading

The platform operator should set up a function responsible for establishing, implementing and enforcing the criteria for the inclusion of virtual assets, the criteria for suspending, suspending and canceling the trading of virtual assets, together with the options exercisable by customers.

In addition, platform operators should conduct reasonable due diligence on any virtual assets before including them for trading and ensure that they continue to comply with all criteria.

6. Prevention of market manipulation and illegal activities

Platform operators should establish and implement written policies and monitoring measures to identify, prevent and report any market manipulation or illegal trading activities on their platforms. Such monitoring measures should include restricting or suspending trading if manipulative or irregular activities are detected. Platform Operators should employ an effective market surveillance system provided by a reputable independent provider to identify, monitor, detect and prevent such manipulative or illicit trading activities and provide the SFC with access to this system.

7. Accounting and auditing

A Platform Operator is required to select auditors with due skill, care and diligence, taking into account their experience, track record and competence in auditing virtual asset-related businesses and Platform Operators.

In addition, platform operators should submit an auditor's report each financial year, which should contain a statement as to whether there has been any breach of applicable regulatory requirements.

In addition, we now impose a licensing condition requiring platform operators to provide the SFC with monthly reports on their business activities within two weeks of the end of each calendar month and when the SFC so requests.

8. Risk management

Platform Operators should establish a robust risk management framework to enable them to identify, measure, monitor and manage all risks arising from their business and operations.

Platform operators should also require customers to deposit funds into their accounts in advance, and must not provide customers with any financial accommodation to purchase virtual assets.

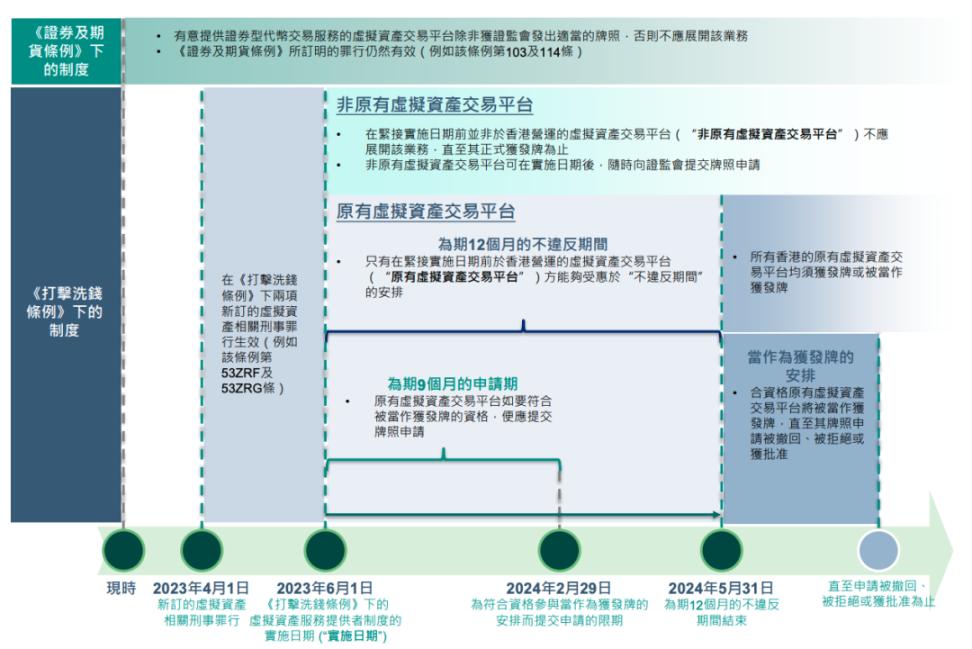

V. Arrangements for the transitional period

For the "original virtual asset trading platform", the "Anti-Money Laundering Regulations" stipulates that before June 1, 2024, it will be a transition period.

If the operator applies to the SFC within nine months after 1 June 2023 and confirms that it will comply with the regulatory requirements set by the SFC, the operator may be deemed to have been licensed until the SFC approves its a decision on a license application, during which time services will be able to continue until (i) the end of the first 12 months, (ii) the application is withdrawn, (iii) the SFC rejects the application, and (iv) the SFC grants the license, to Whichever is earlier shall prevail.

If its application for a virtual asset service provider license is rejected by the China Securities Regulatory Commission, it must terminate its virtual asset service business within 3 months of receiving the rejection notice or before June 1, 2024, whichever is later. During this period, the operator may only take actions purely aimed at shutting down its services. Operators may apply to the CSRC for an extension of the closure period for such a period as the CSRC deems appropriate, taking into account the business and activities of the operator.

For "non-original virtual asset trading platforms" that plan to provide virtual asset services in Hong Kong after June 1, 2023, they should apply to the Securities Regulatory Commission and obtain a virtual asset service provider license before starting their business.

6. "Regulatory arbitrage" is fading away

Under the Anti-Money Laundering Regulations, relevant sanctions will be imposed for violations and non-compliance, including providing virtual asset services without a license and failing to comply with AML/CTF requirements. In addition, any active marketing of services to the Hong Kong public will be regarded as providing virtual asset services, regardless of where the service is provided or whether the service provider is in Hong Kong.

After June 1, 2023, it will be a crime to operate and provide virtual asset services without a VASP license. On conviction upon indictment, a fine of HK$5 million and 7 years' imprisonment, and in the case of a continuing offence, an additional fine of HK$100,000 for each day during which the offense continues. A fine of HK$5 million and 2 years' imprisonment on summary conviction and, in the case of a continuing offence, an additional fine of HK$10,000 for each day during which the offense continues.

If the statutory AML/CTF regulations are not complied with, the licensed service provider and its responsible personnel are guilty of a crime. Once convicted, each person may be fined HK$1 million and imprisoned for 2 years. In addition to criminal liability, they are subject to disciplinary action by the SFC, including suspension or revocation of licenses, reprimands, orders to take remedial action and fines.

In addition, various "misconduct" in the operation of virtual asset exchanges may also face disciplinary fines from the SFC.

Compared with other jurisdictions, especially other regions in East Asia, Hong Kong's previous regulatory environment for virtual asset transactions can be said to be very loose. That's why there are countless companies, large and small, who have placed their headquarters or operation centers in Hong Kong. However, with the introduction of the "Encryption New Deal", Hong Kong has drifted away from "regulatory arbitrage".

7. Hong Kong: The Return of the King

Thanks to the relaxed regulatory environment and favorable tax policies, as well as the huge geographical advantage of being backed by the mainland, Hong Kong, a global financial center that requires money and rich people, was once favored by the encryption industry, especially in asset management and trading. The largest "fat meat" in the industry. In addition to the major Chinese exchanges rooted in Hong Kong, the well-known Bitfinex and Crypto.com are headquartered in Hong Kong. Alameda Research and FTX, which were once in the limelight, also started from Hong Kong, not to mention that BitMEX once rented an apartment in the Yangtze River Center. The whole floor becomes the neighbor of SFC. As the center of gravity of the encryption industry "falls in the east and rises in the west", Hong Kong was once silent, and the limelight was overshadowed by Singapore next to it and Silicon Valley on the other side of the ocean.

Today, Hong Kong "returns the king" and is committed to becoming a global encrypted financial center. Regarding Hong Kong's "Encryption New Deal", starting from the second half of 2022 when the Hong Kong government announced on various occasions, there have been various doubts and even mocking voices. But this does not prevent the "big tide surging in Hong Kong". In April this year, the Hong Kong Web3 Carnival not only reunited the strength of the Chinese in the industry, but also attracted the attention of the world, witnessing another historical turning point in the encryption industry.

In the context of the fall of FTX and the ensuing tightening of regulation on the encryption industry in the West, as well as the competition for talents and funds by "Xingang", many people think that the "New Encryption Deal" of the Hong Kong government may be just a flash in the pan. But looking back at the previous review, from the financial technology regulatory sandbox in 2017 and the regulatory framework in 2018, to the "Position Statement" in 2019, and to the current VASP licensing system, we can not only see that the Hong Kong government has a strong attitude towards the encryption industry. Its supervision has very good policy continuity, and it can also be seen from its comprehensive plan, pragmatic spirit, flexible body and determination to implement.

Hong Kong is one of the top four financial centers in the world, and it is also an asset management center in Asia. The loose foreign exchange environment and perfect legal system have brought countless hot money here. For centralized virtual asset exchanges, Hong Kong is a rare treasure. However, if you want to wear the crown, you must bear its weight. Only on the basis of meeting regulatory requirements can exchanges participate in the distribution of this huge cake.

If Hong Kong in the past was a paradise for crypto adventurers, then Hong Kong in the future will belong to industry players who pay attention to rules and regulations.

References:

https://www.elegislation.gov.hk/hk/cap571!zh-Hant-HK

https://www.sfc.hk/TC/Regulatory-functions/Intermediaries/Licensing/Do-you-need-a-licence-or-registration

https://apps.sfc.hk/edistrationWeb/api/consultation/openFile?lang=TC&refNo=23CP1

https://apps.sfc.hk/publicreg/Terms-and-Conditions-for-VATP_10Dec20.pdf

https://www.hkex.com.hk/-/media/HKEX-Market/News/Research-Reports/HKEx-Research-Papers/2023/CCEO_CryptoETF_202304_c.pdf