Written by: BEN LILLY

Compilation: Deep Tide TechFlow

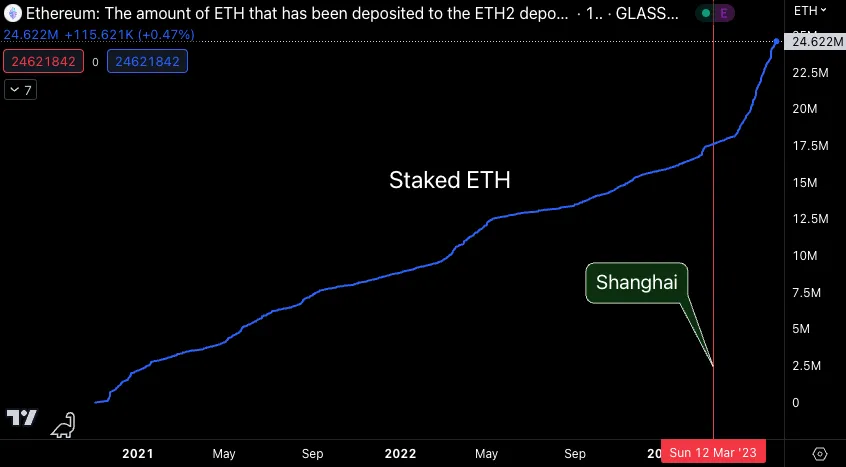

Three months ago, a historic shift began.

This is similar to an undercurrent under the ocean's surface. These undercurrents act like conveyor belts, bringing warm water from the equator to the poles and bringing cold water from the poles back near the equator. For anyone who fishes or lives around the equator, fish species are abundant here.

In the field of cryptocurrency, the Shanghai upgrade has become a new undercurrent in the market. Users are able to unstake their ETH . This was a major risk downgrade, and as a result, the amount of ETH staked exploded quickly and has risen by about 38% since then.

Researcher BEN LILLY and the entire Jarvis team will be sharing this Alpha with you, especially as it looks set to become an increasingly important factor in the ever-changing landscape of cryptocurrency prices.

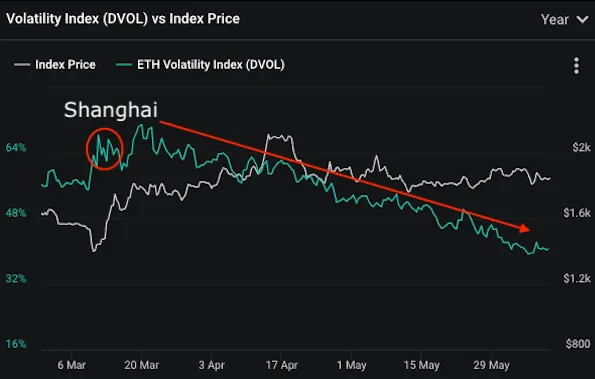

The real reason behind the drop in ETH volatility

In reality, volatility hasn't really changed much, it's just gotten smoother. Below is ETH volatility as measured by the Deribit Volatility Index.

This volatility compression is a market phenomenon that we have been observing. As for why, let's explain with some quotes from Paradigm's Joe Kruy.

First, Joe explains that there is one distinct entity at play in the options market:

A large systematic options trader converted 90,000 March $1800 Bullish options into June $1800 Bullish options, injecting about 125,000 net volatility into the market, easing ETH natural upside buying shortage of homes.

He went on to add:

Paradigm's money flows show that due to this sell side, traders are holding a sizeable position at the June expiry price of $1800, allowing traders to extend their vega and gamma as they sell off, which will cause prices to " pips down/volatility down" as they adjust their long-term volatility exposure relative to this expiration.

I'll still explain that when someone sells a Bullish, they offer a contract to the market. The buyers are likely to be investors who are Bullish on the asset.

Buyers have also Bullish bullish on volatility. All else being equal, the higher the volatility, the higher the premium or value of the contract – for the buyer. Conversely, sellers' profits increase as volatility decreases.

Now, to measure your exposure to volatility, the options market uses a term called vega. Joe tells us that someone sold 90,000 June Bullish. This makes the person Bearish on volatility, or "Vega." In fact, they just sell contracts when volatility starts to rise. That's just what's happening at the end of 2022.

But that's just the beginning...

There's also a lot of that activity in the first and second quarters of 2023. To quote Joe:

Sellers dumped around 40,000 vega in February and March via Bullish options (25,000-35,000 contracts) after massive excess withdrawals in June/September contracts. After the Shanghai upgrade, volumes have increased significantly, including 63,000 June/September $2200 Bullish, and some other September option sales, totaling a net vega of negative 200,000.

Back-end volatility pressures continued, hit further by 28,500 Sep/Dec $2,300 Bullish(minus 45,000 vega) and 10,000 Jun $1,800/March $2,300 Bullish(minus 45,000 vega) The 6-9 million volatility that lacks natural demand.

This is massive activity happening in the Ethereum options market. And this type of activity comes up over and over again. When volatility starts to rise, this entity starts selling Bullish options in bulk.

This again dampens volatility. In fact, the original seller would need to hedge himself if the price decided to rise above any strike price being sold (eg - $1800 for the June contract).

When this situation reverses, the entity begins to liquidate these positions. According to Paradigm, the entity bought back 100,000 June contracts over the weekend. Prices responded accordingly.

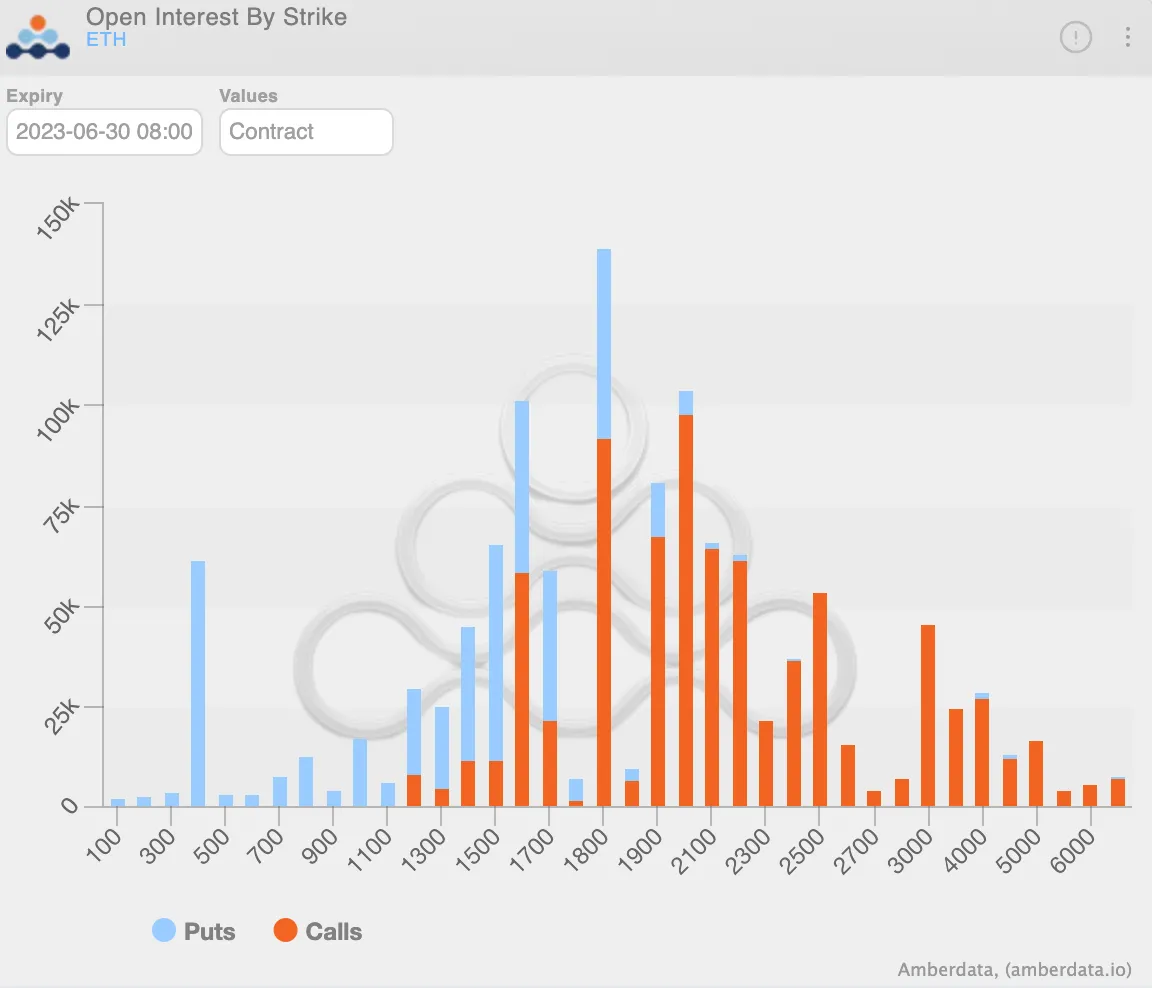

Even though this is a large amount, the impact on volatility is still fairly small as there is still a lot of open interest. You can see this in the bar chart below, which shows the June 30 contract by strike price. Note that in the highest bar below, the $1,800 strike price still opens a large number of Bullish.

This behavior unfolding in the ETH options market is quite remarkable. As Joe said,

The second quarter looks like the crypto options market is going through a major microstructural change.

This begs the question: why is this happening all of a sudden?

The latest market status

Just like changes in ocean currents can affect the functioning of an ecosystem, the Shanghai upgrade appears to have affected activity involving Ethereum. It is believed that this escalation caused the entity's actions.

Going back to Paradigm's words:

This surge in ETH volatility supply can be attributed to two factors: Ethereum’s transition to a proof-of-consensus model and the implementation of the Shanghai upgrade . By introducing withdrawals, the Shanghai fork led to a significant increase in staking activity aimed at reaping rewards with validators.

At the end of that quote, the main point is that the parties involved may be trying to extract additional yield from staked ETH through this option strategy. Now, the staked ETH can be withdrawn and they are using their tokens as collateral.

The positions they are shifting are enormous. It's hard to say what might happen if this type of event goes awry. but:

Staking these transactions requires substantial margin requirements, prompting us to question whether this strategy is indeed the most efficient way to extract additional yield from ETH . We also speculate that there was a unique arrangement between the underwriters and Deribit to prevent automatic liquidation during the strong rally in Q1, especially if the spot price rose/volatility rose.

Remember, when you stake your ETH , you cannot unlock it immediately. So there may be a unique arrangement, as Joe suggests.

So, as to who might be the entity behind this new dynamic in the market:

While this is still purely speculative, given that these transactions do not occur on Paradigm, it is highly likely that this large seller was a large validator . This may explain their impact on the ETH volatility supply and demand imbalance, which has had a significant impact on compressing both ETH implied and realized volatility...

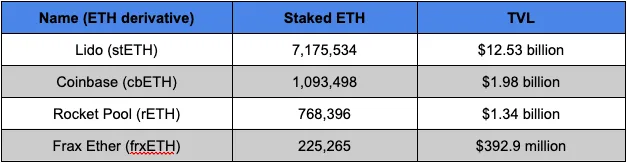

To satisfy my curiosity, I want to see if this entity exists on-chain. Depending on the number of contracts in progress, we can narrow down LSD or Liquidity Derivatives to something like 250,000 ETH .

This gives us a starting point, as it reduces dozens of LSDs of sufficient size to a small set of stETH, cbETH, rETH, and frxETH.

The placement of these tokens in aggregators, options platforms, vault strategy platforms, and exchange pools has not caught my attention. Here, I'd expect to see a Ribbon Finance options vault with $100 million in deposits, but what I'm seeing is clearly far from that.

This means that this entity may have some operations that do not involve the on-chain protocol.

Regardless, this is at least something to be aware of, as this entity becomes more and more important. The bigger they get, the more impact they have on price action.

We should also consider that their upside exposure is likely not just spot ETH. Entities are likely to generate additional revenue from other operations as the price increase creates a positive feedback loop that increases as overall activity increases.

I'll leave the fun of guessing to you guys.