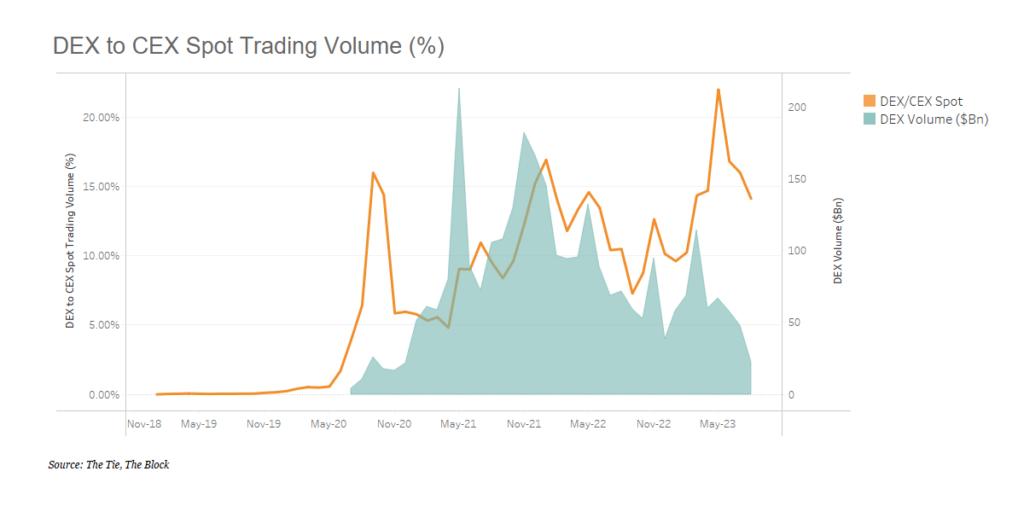

FTX was one of the most reputable cryptocurrency centralized exchanges (CEX) in the world at the time. After FTX became popular, the exchange's market share slowly shifted to decentralized exchanges (DEX). This shift comes in a context where the regulatory environment remains unclear and unpredictable.

Original title: " Decentralized Exchanges: Current Limitations of AMM Models & Exploring the Future of DEX Mechanics "

Written by: Chí Phan, The Tie

Compiled by: Lynn, MarsBit

While decentralized exchanges are poised to benefit from this murky and skeptical environment, they face their own challenges in building sustainable business models. Although the AMM decentralized exchange is one of the most innovative ideas that launched the DeFi movement, it seems unsustainable for liquidity providers to operate without speculative funding subsidies in the form of reward tokens and incentive programs. And it's challenging. Billions of dollars have poured into DeFi protocols and DEXs over the past few years, but these bootstrapping efforts have proven to be either ineffective or short-lived.

Transaction fees alone will not be enough to entice many liquidity providers to keep funds in the pool once the liquidity incentive program ends. The loss of liquidity, coupled with the low capital efficiency of AMM DEX, resulted in high slippage. This in turn makes on-chain transaction costs relatively higher than those on centralized exchanges.

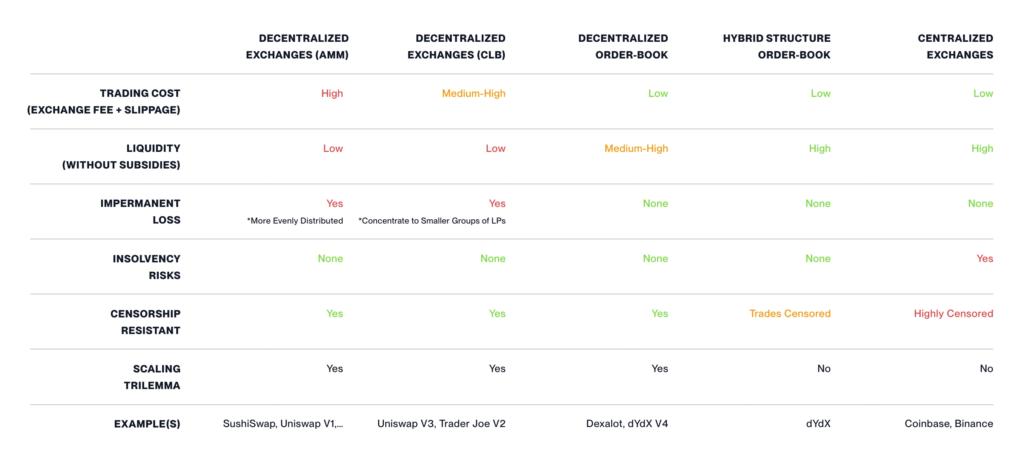

To help DEX compete with CEX, DeFi is working hard to innovate to reduce slippage fees and improve capital efficiency to provide deeper liquidity. These approaches range from further improving the AMM model to introducing order book matching in DeFi.

An example of the latter approach is dYdX, which has integrated order book matching into its hybrid infrastructure. This integration enables its users to trade crypto assets with reasonable trading fees and high levels of liquidity without having to trust unprotected exchanges around the world. Uniswap V3, on the other hand, continues to dominate DeFi with over 60% market share by focusing on improving the AMM model. dYdX and Uniswap both have over $4 billion in weekly trading volume, each paving the way to narrow the gap between DEX and CEX.

Whether it’s an AMM, a decentralized liquidity ledger, or a hybrid structure like dYdX, each approach has its pros and cons. Which model will eventually dominate the cryptocurrency space? This article will explore these pros and cons in detail, while looking toward the future and investigating innovative mechanisms in the DEX space.

Centralized Exchanges – “Trust Me” Option That Requires Proper Protection from Local Governments

Centralized exchanges serve as custodian financial institutions, and users can deposit fiat currency or cryptocurrency assets into their trading accounts to buy (or sell) cryptocurrency assets. All trading activity is settled off-chain and is only transferred back on-chain when a user wishes to withdraw cryptocurrency to their public blockchain address. However, unlike traditional stockbroker (or exchange) trading accounts, these accounts are not insured by the Federal Deposit Insurance Corporation (FDIC) if the exchange goes bankrupt. Considering that many countries around the world still lack a clear regulatory framework for crypto-assets, crypto-asset investors are not as protected by the authorities as investing in other asset classes. Therefore, they can only trust existing centralized exchanges without getting insurance or protection from local governments.

Before and during FTX’s collapse, there were insufficient regulators in place to protect crypto asset investors from the alleged fraud that occurred within FTX’s internal operations, despite the custodian having billions of dollars in custody. Nonetheless, investors who have faith in cryptocurrencies are still looking for other trust-based options for trading crypto assets – decentralized exchanges.

Decentralized exchange

One of the most fundamental differences between centralized exchanges (CEX) and decentralized exchanges (DEX) is the assumption of trust. Given the uncertain cryptocurrency regulations that prevail around the world, ownership of crypto assets is not protected by many institutions. Therefore, it seems safer for market participants to keep cryptocurrencies themselves and conduct trading activities on-chain. Decentralized exchanges enable users to interact with smart contracts and exchange crypto assets on-chain without permission, with all transactions settled in real-time on a public ledger.

However, while this solution can help Web 3.0 enthusiasts reduce the solvency risk of exchanges and seems to be an ideal solution, when choosing between decentralized and centralized exchanges, Transaction costs become an important consideration.

Centralized exchanges typically charge fees ranging from 0.1% (like Binance) to 0.6% (like Coinbase) per trade. In comparison, decentralized exchanges charge fees ranging from 0.04% (such as Curve) to 0.3% (such as Uniswap, SushiSwap, PancakeSwap); dYdX offers a permanent trading fee of 0.02%, in addition to per-trade Network gas fees, which range from a fraction to $10 on the Ethereum network (equivalent to 0.001% to 0.5% of every $2,000 transaction).

If you only consider exchange fees, some decentralized exchanges (DEX) have even lower fees than major CEXs. However, the total transaction costs (including exchange fees and slippage fees) of decentralized exchanges tend to exceed that of centralized exchanges due to slippage fees incurred by decentralized exchanges due to lower liquidity.

Liquidity and Slippage

Liquidity refers to the ability to buy and sell a trading asset without causing large fluctuations in its price and minimizing slippage. Slippage is the difference between the expected price of an order and the price at which it is executed, and is often considered a hidden fee in trading. High levels of liquidity help reduce slippage, making transaction costs more attractive to users.

In illiquid AMM pools, slippage can amount to 1% of the trade value (even 10% on illiquid pairs), making trading on a DEX significantly less attractive than trading on a CEX. Therefore, users must choose to accept the solvency risk of the exchange or trade on a free exchange where trading costs, including exchange fees and slippage charges, are higher.

On exchanges that utilize an order-matching mechanism, market makers make money by maintaining funds on the exchange, matching higher bids with lower ask prices, thereby profiting from the price difference. The presence of market makers on exchanges significantly improves liquidity by increasing trading volumes. To incentivize market makers to invest capital, exchanges often negotiate with them discounts on trading fees. These arrangements benefit both parties: exchanges receive more orders, and market makers increase their operating margins on deployed capital.

AMM pools, on the other hand, require liquidity providers as the primary source of liquidity (not just liquidity enhancers). DeFi reward programs require large amounts of capital to incentivize liquidity providers in the form of reward tokens to keep funds in liquidity pools. However, as interest rates rise and available funds decrease, incentive programs are reduced across chains, resulting in a massive drain on decentralized liquidity. This has led enthusiasts to question the sustainability of DeFi’s current standard growth model.

Impermanent Loss—The Trap of DeFi Liquidity Supply

Automated Market Maker (AMM) pools are the innovation that started the entire DeFi movement. Simply put, the AMM smart contract functions like an over-the-counter (OTC) bot, enabling users to exchange their desired tokens with paired tokens within the pool. The birth of Automated Market Makers (AMMs) is a breakthrough that enables cryptocurrency users to exchange and trade on-chain without relying on centralized third parties around the world.

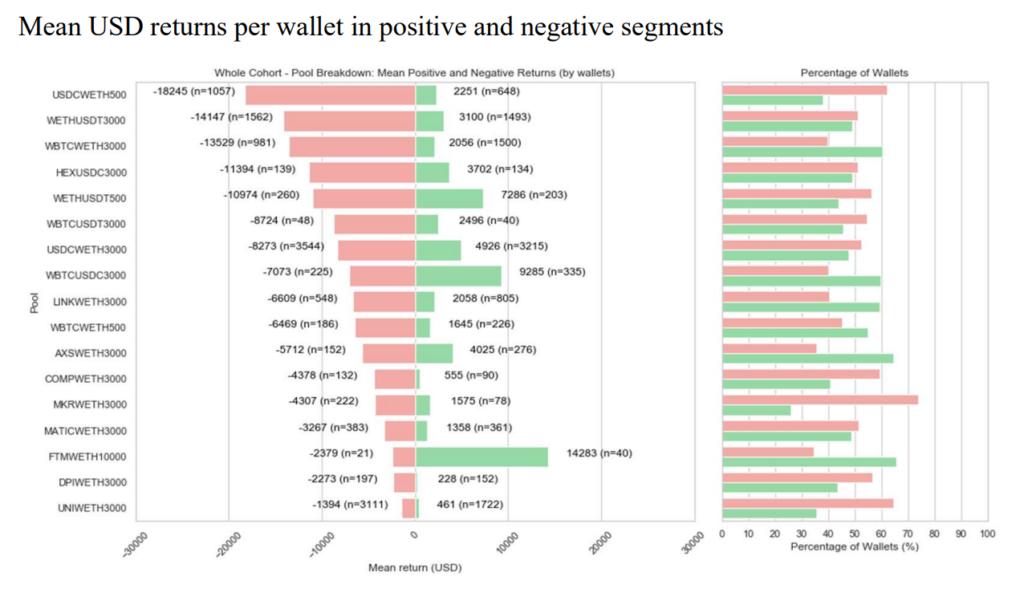

Liquidity providers are the primary source of liquidity, depositing pairs (or groups) of cryptoassets into these pools, expecting to earn trading fees and reward tokens in return. However, a study on Impermanent Loss in Uniswap V3 showed that half of the liquidity providers on Uniswap V3 (the largest DEX with over $4 billion in weekly trading volume) generated negative returns, and the majority of the winning half Poor performance adjusted for inflation, all due to Impermanent Loss.

Most liquidity providers (LPs) and DeFi enthusiasts have realized that Impermanent Loss(IL) is the real trap of high-yield DeFi farming. Impermanent Loss represent the risk of underperformance compared to simply holding the token and doing nothing.

For example, consider a group of investors providing liquidity for 10 ETH and 17,000 USDC to the ETH-USDC pool. A cryptocurrency enthusiast named Vitalik came to the pool and exchanged 1700 USDC for 1 ETH. Now, with 9 ETH and 18,700 USDC in the pool, the price of ETH has increased from $1,700 to $1,800. The total net worth of these liquidity providers becomes $34,900 (9 ETH @ $1800 + 18,700 USDC) instead of $35,000 (10 ETH @ $1,800 + 17,000 USDC). The difference of $100 is an Impermanent Loss.

Due to the huge hurdles posed by Impermanent Loss, DeFi protocols have had to issue reward tokens on top of shared exchange fees to incentivize liquidity providers to keep their funds in the pool. These reward tokens are liquid and their prices continue to trend upward during the bull market, making the AMM (Automated Market Maker) pool seem like a big “free lunch”. However, as trading volumes begin to decline and "cheap money" subsidies dry up, liquidity providers face increasing challenges in staying profitable, coupled with rising cybersecurity risks. Therefore, many liquidity providers chose to withdraw funds and withdraw from the capital pool.

Liquidity plan – failure to build long-term moat for AMM pool

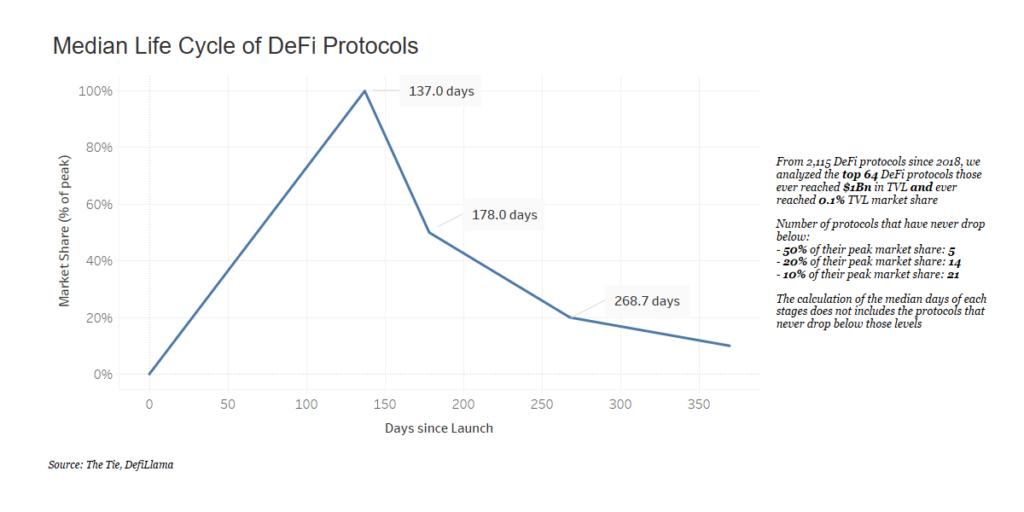

Many protocols use raised funds for incentive programs, often involving the distribution of reward tokens, with the primary purpose of attracting liquidity providers and users. Nonetheless, these incentive programs generally result in short-lived DeFi protocols. We conducted data analysis on a sample size of more than 2,115 protocols since 2018. We further narrowed the analysis to focus on the most successful protocols, 64 in total, that were able to achieve at least 0.1% of the Total Value Locked (TVL) market share at some point during their existence and have a TVL of over $1 billion .

Even among these 64 top DeFi protocols, their life cycles are relatively short as measured by retained liquidity (TVL). As liquidity and community participation gain momentum, it typically takes three to four months for them to reach peak TVL market share (in %). However, over the next month or two, their market share declines rapidly, often reaching only 10% of their peak liquidity market share within a year.

Trading fees alone will not be enough to entice many liquidity providers to keep funds in the pool once the liquidity reward program ends. As a result, a large portion of funds are withdrawn from the pool, causing slippage to increase and users to churn. This downward spiral in trading activity quickly turned these exchanges into ghost towns.

Further innovate the AMM model or introduce order books into DeFi

In response to the challenges of liquidity provision and competitiveness in the cryptocurrency exchange market, two popular innovative approaches have emerged, bringing inspiration to DeFi enthusiasts: the continuous innovation of the AMM model and the introduction of replica order book matching infrastructure .

The first method: innovative AMM model

Over the three-year life cycle of DeFi, multiple variants have been derived from the original AMM model, the constant product market maker (CPMM), such as the constant sum MM (CSMM) or the hybrid constant function MM (curve). However, none of them successfully solved the problem of Impermanent Loss(IL) and mainly focused on reducing slippage.

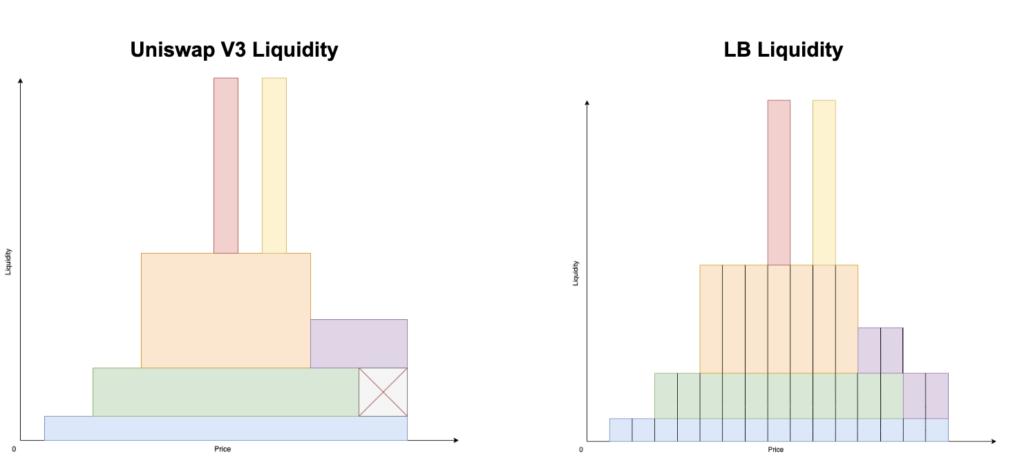

Uniswap V3, the AMM DEX with the largest trading volume, introduces the concept of centralized liquidity book (CLB). This feature allows liquidity providers (LPs) to concentrate their funds within a specific price range, thereby deepening the liquidity book and better utilizing the liquidity in the AMM pool. Recently, Trader Joe’s introduced price ranges based on the centralized liquidity ledger (CLB) to provide liquidity providers (LPs) with greater flexibility.

For example, assume the current ETH price is $1,700. Liquidity providers now have the option to pool their funds within a specific price range, say between $1,650 and $1,750. This is why it is called centralized liquidity.

While these changes can increase order book depth and reduce slippage when prices are less volatile, they do not reduce liquidity providers' overall Impermanent Loss. In the standard AMM model (CPMM), IL is distributed equally, while in the centralized liquidity book (CLB), IL is now concentrated among those liquidity providers that cannot reallocate their capital fast enough when the price exceeds their allocation range On the body.

Let's say you have 1 ETH and 1,700 USDC, and you decide to provide liquidity in the price range of $1,650 to $1,750.

When the price reaches $1,800, your coin position is quickly emptied (your ETH is now cheaper than the market price) and all your ETH is converted to USDC. You now hold 3,400 USDC instead of 3,500 USD (1 ETH @ 1,800 USD and 1,700 USDC).

When the price goes to $1,600, all the USDC in your chosen pool will soon be wiped out (as people can buy cheaper ETH and swap it into your pool) and you will be holding 2 ETH and 0 USDC, which would be worth $3,200 instead of $3,300.

In short, if the asset price falls below $1,650 or rises above $1,750, liquidity providers that do not automatically rebalance will suffer huge intangible losses.

The only situation where LPs can profit from providing liquidity to centralized pools is when prices are stable and trading volume is high, such that swap fees exceed the Impermanent Loss(IL). Another study conducted by the ETH Zurich team on the risks and returns of Uniswap V3 LPs showed that impermanent Impermanent Loss are zero only when the price remains unchanged compared to the initial price at which liquidity was injected. Otherwise, IL will always be negative whether the price is rising or falling.

One potential way to address this challenge is to consider revising the swap fee structure. For example, Trader Joe’s introduced a volatility accumulation mechanism, known as “surge pricing.” This mechanism aims to reduce the cost attractiveness of trading on DEX by levying variable fees on users to incentivize liquidity providers to respond to market fluctuations.

While increasing swap fees can increase profitability for liquidity providers, it comes at the cost of reducing competitiveness and potentially directing users to other decentralized exchanges (DEX) and centralized exchanges.

Second method: Introduce order matching mechanism into DeFi

dYdX founder Antonio Juliano believes that this mechanism is superior to AMM alternatives in achieving high liquidity. The dYdX team chose a hybrid infrastructure that combines on-chain settlement with an off-chain low-latency matching engine equipped with an order book. Market makers operating on the dYdX platform mainly emphasize algorithmic methods and utilize APIs. dYdX has proven its principles by becoming the second largest decentralized exchange on the market, behind Uniswap. This year, it facilitated average weekly trading volume of more than $7 billion.

Dexalot is another protocol with a similar goal of replicating the trading experience on a centralized exchange on Avalanche, but with a slightly different approach. Rather than employing an off-chain matching engine like dYdX, the Dexalot team leverages subnet infrastructure and the LayerZero messaging protocol to achieve low latency and minimal transaction fees. Still, the blockchain scaling trilemma remains the main problem with this approach. Higher trading volumes and more orders translate into higher data and transaction processing demands on the network. Market making operations also require high-frequency trading activities, such as updating quotes and transmitting cancellation indicators between multiple exchanges.

In 2013, the U.S. Securities and Exchange Commission (SEC) reported that 96.8% of orders were canceled before being executed, with 90% of orders canceled within one second.

Therefore, excessive transaction costs may discourage market makers, which may lead to reduced liquidity as the structure further expands toward decentralization. In contrast, decentralization advocates and cryptocurrency enthusiasts believe that the use of centralized structures in DeFi is a security bottleneck, and they doubt the willingness of regulators to promote the development of such innovations.

Whether it’s an AMM, a decentralized liquidity ledger, or a hybrid structure like dYdX, each approach has its pros and cons, as well as its supporters and skeptics. Only time will reveal which approach will be more popular in the coming years, especially if the cryptocurrency market picks up again.

Summarize

No matter which DEX model wins, the most important competitor for any DEX will still be centralized exchanges. While the growing popularity of DEXs over the past three years may lead some to believe that decentralized exchanges will eventually dominate exchange market share, this prediction is based on a strong assumption: the global cryptocurrency regulatory framework remains unclear. Clear and unpredictable.

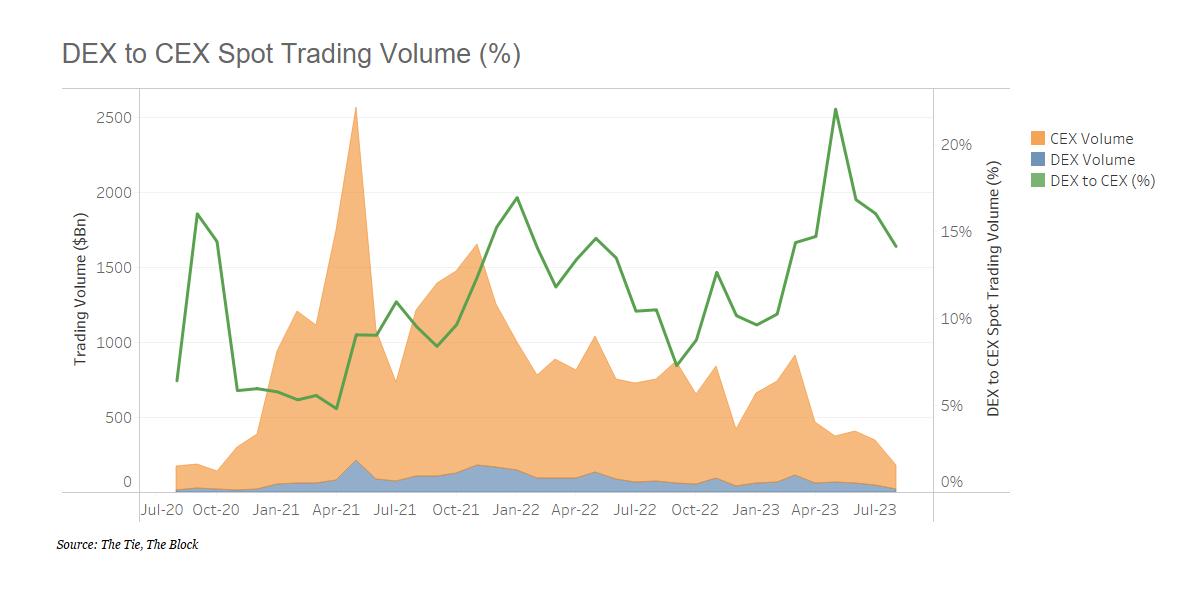

Even after FTX’s shocking collapse, which resulted in billions of dollars in losses, total trading volume on centralized exchanges is still five times that of decentralized exchanges. Although trust in centralized exchanges has declined, most users still choose to trust these platforms rather than learn how to use a cryptocurrency wallet or endure the high transaction costs of decentralized exchanges.

Assuming that cryptocurrencies continue to gain widespread adoption around the world, regulators will increasingly recognize the need to strengthen the protection of cryptocurrency investors. Since regulatory uncertainty is still a major disadvantage of centralized exchanges, centralized exchanges should seize the opportunity, accelerate the development process, and improve product quality to avoid the risk of centralized exchanges becoming more clarified in the next few years as regulations are further clarified. It is possible to regain bargaining power.

While centralized exchanges may lack censorship-resistant features than free exchanges, they offer valuable onboarding/offline services and the general benefits of greater market competition. In the future, DEX and DeFi services will need to continue to innovate to provide better services, ultimately driving the growing popularity of DeFi.