Author: Matthew Lee

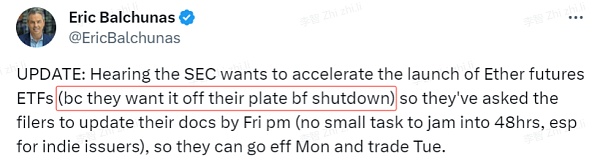

On September 27, SEC Chairman Gary Gensler participated in a hearing of the U.S. House of Representatives Financial Services Committee. The hearing examined the SEC's regulatory developments, rulemaking and activities during the period since October 5, 2021, including the SEC's proposal to modify the definition of "exchange" and expand the SEC's authority over digital asset trading platforms. Although Gary Gensler still maintains a strict attitude towards virtual assets, the SEC is no longer a monolith, and internal personnel are already exhausted . Senior ETF analysts at Bloomberg also said employees wanted to be freed from their type of work before the government shutdown .

Although U.S. regulation has been suppressing the development of the industry, the saving grace is that it is developing a due process legal system that ensures the correct path to correction when things may develop out of control (please refer to the U.S. case caused by the bankruptcy of FTX investors and Asian investors).

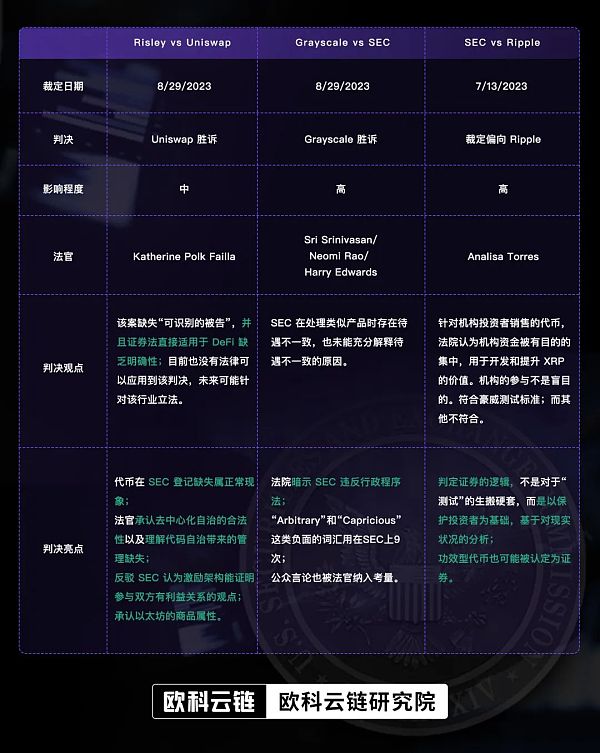

In the past three months, the court has ruled on three industry-related cases, namely Risley vs Uniswap, SEC vs Ripple, and SEC vs Grayscale. The results of the rulings are all favorable to the industry. Combined with the judicial department’s frequent series of judgments against the SEC, one can’t help but wonder whether the SEC’s “long arm” behavior against virtual assets will be restricted.

There are details worth discussing in the judgment that highlight the positive factors in the U.S. regulatory environment. Below, we will observe the judicial system’s attitude towards virtual assets and SEC supervision from the details of the recent judicial department’s penalties on virtual assets, and explore the regulatory trends of virtual assets.

TL;DR

Risley vs Uniswap Verdict Points

The court's judgment on Uniswap and Risley attracted the least public attention, but it also contained the most details. It contained some very clear and directional views that can illustrate the court's attitude towards the industry.

Allegation

Risley's accusations against Uniswap Labs and its venture capital companies Paradigm, Andreessen Horowitz, USV, etc. mainly include the following points:

i). The Uniswap platform sells unregistered securities;

ii). Uniswap is an unregistered broker-dealer;

iii). Uniswap Labs makes money through false propaganda.

court response

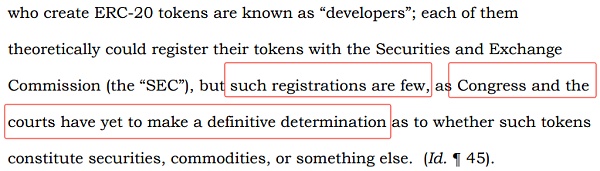

Uniswap’s decentralized architecture makes it impossible to identify fraudulent token issuers , resulting in the absence of an “identifiable defendant” in the case. There is a lack of clarity on the direct application of securities laws to DeFi , and there is no federal law that would allow courts to pursue Uniswap Labs and its venture capital firms. Therefore, the mere fact that Uniswap Labs has the authority to collect transaction fees and other aspects is not enough to determine that Uniswap Labs or the venture capital firm should be held responsible.

Highlights of the verdict

This paragraph is a very important paragraph. The judge believed that the law was not unreasonable. Combining the actual situation and the law, he believed that the lack of registration of tokens with the SEC was a normal phenomenon . Therefore, many SEC accusations such as "violating securities laws by failing to register with the SEC or publish a prospectus or annual report" are untenable.

Due to the characteristics of decentralized autonomy, the judge understood the lack of management of "Scam Tokens", but as the law becomes more and more perfect, decentralized organizations should also use on-chain tools such as OKLink 's on-chain tag system to remind users risks of certain tokens to avoid legal disputes. Institutions should also consider using on-chain tools to avoid risky interactions when conducting large transactions on decentralized autonomous platforms.

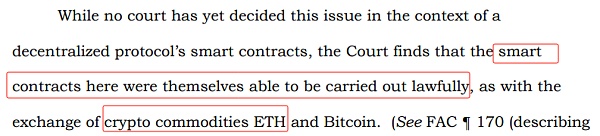

The judge revealed two pieces of information: i). Acknowledging the legality of smart contracts in the operation process ; ii). Acknowledging the attributes of Ethereum commodities (SEC claimed that ETH is a security rather than a commodity when suing Coinbase).

Due to the lack of laws, decentralized trading platforms have not been punished, but there will be more stringent supervision of decentralized organizations , especially trading platforms. Take Hong Kong and Singapore as examples. Both have enacted strict laws requiring trading platforms to strictly review the trading tokens on the platform. For compliance, many platforms have also purchased the data labeling services of many on-chain data service providers to target counter-attacks. The field of money laundering . In the future, decentralized trading platforms will not have too many privileges.

However, the judge’s current conclusion is also clearly different from the SEC Chairman’s previous view that “most DeFi trading platforms are actually no different from traditional exchanges.”

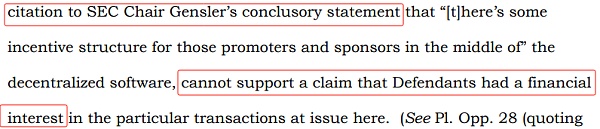

The court also scoffed at the plaintiff’s argument citing the SEC , holding that the existence of an incentive structure did not prove that the defendant had an interest relationship with the project parties . This perspective can bring some relief to many projects with incentives.

summary

There are two very important pieces of information in the judgment, i). The judge has a very deep understanding of the operating logic and characteristics of decentralized projects; ii). The judge is relatively tolerant of the code operation of decentralized projects and recognizes the legality of smart contract operations. sex.

However, the most important thing is that the decentralized operating model and the lack of legal framework prevent the court from making objective decisions. Several senators have now proposed a new legal framework for virtual assets, KYC, and even decentralized protocols, aiming to clarify the regulatory framework and responsible persons. In the future, decentralized operations will also need to find ways to comply with regulations, and more data service providers like OKLink will be needed to help identify potential "Rug-Pull" or "Pump and Dump" situations.

Grayscale vs SEC Verdict Key Points

Allegation

Grayscale accused the SEC of arbitrarily and repeatedly rejecting the listing of Grayscale's Bitcoin ETP, but approved the listing of a substantially similar Bitcoin futures ETP.

court response

The SEC neither disputed Grayscale’s evidence that Bitcoin spot and futures markets have a 99.9% correlation, nor suggested that market inefficiencies or other factors undermined the correlation. The judge found that the SEC had inconsistent treatment when dealing with similar products.

Therefore, the judge granted Grayscale's request and vacated the SEC's order.

Highlights of the verdict

Courts rarely state in judgments that an agency violated the law (the Administrative Procedure Act), and courts use very harsh words to suggest that "defendants'" decisions were rash and capricious, or even an "abuse of discretion."

In the judgment, very negative words such as "Arbitrary" and "Capricious" appeared nine times.

Public opinion was also taken into consideration by the judge. It can be said that in this judgment, the SEC was disliked by almost everyone.

summary

In this overwhelming 3:0 ruling, the judge questioned how Grayscale's ETP was fundamentally different from other approved ETPs, allowing the SEC to "treat it differently." The SEC was unsuccessful in answering that question.

In response to Grayscale’s judgment, Paradigm’s policy director also brought some additional information: the two judges appointed by Presidents Obama and Carter were very disgusted with the SEC’s arguments, so as Democrats (the Democratic Party is more opposed to crypto assets) they also joined Opinions of Conservative Party Rao. Therefore, the probability of the SEC requesting a joint trial will be very small, because it is likely to anger the court. If the reason for disapproval is raised again, it should be about the company's internal operations, not the hidden dangers of the ETP itself.

SEC vs Ripple Verdict Key Points

Allegation

i). Ripple’s sale of tokens to institutions is suspected of constituting the sale of securities;

ii). Ripple’s sale of tokens to the public on its digital trading platform is suspected of constituting the sale of securities;

iii). Giving away tokens to outsourcing companies is suspected of constituting the sale of securities;

iv). No similar prospectus or updated annual report has been submitted to the SEC.

Since this article extensively uses the Howey Test to verify whether it is a security, let’s start with a simple popular science - the Howey Test: 1. Whether there is capital investment; 2. Whether it is invested in a common enterprise; 3. Whether it generates profits Have expectations; 4. Whether to obtain additional returns by virtue of the sponsor.

*SEC considers most tokens to meet the second and third criteria.

court response

i). Ripple’s sale of tokens to institutions through contracts constitutes the sale of securities . The court found that institutional funds were purposefully concentrated to develop and enhance the value of XRP. Institutional participation is not blind. Comply with Howey Test standards;

ii). Ripple’s sale of XRP to the public through a “programmed interface” (exchange) does not constitute a sale of securities . The public does not know the source of the token and has no expectation of profit from the issuer's efforts (but from other factors, such as market trends), and does not have the characteristics of generating an expectation of "profit". Failure to meet the third and fourth criteria;

iii). Distribution through other channels does not constitute the sale of bonds . Because there is no “tangible or definable thing” paid to Ripple, the payment of XRP cannot be considered a sale of securities. The first criterion is not met.

Highlights of the verdict

Ripple proposed an “essential ingredient” test—a “narrow version” of the Howey Test—and was undoubtedly struck down by the courts. The judge also showed that the logic of determining securities is definitely not a mechanical application of "tests", but is based on protecting investors and based on an analysis of the current situation . In contrast, the test proposed by Ripple pays more attention to form.

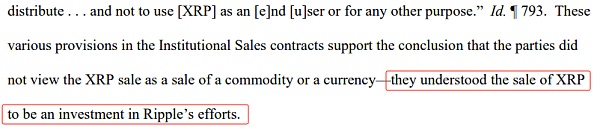

The court held that institutional users clearly understood the terms of the investment contract, and their purchase of XRP did not regard it as a currency or commodity, but as an investment product. Therefore, the sales to the institution were securities sales.

On the contrary, ordinary users do not understand the various SEC documents and Ripple's marketing promotions, and they are related to investment returns, so they do not meet the "expectation of returns" of the Howey Test.

Ripple argued that XRP is not a security, but more like ordinary assets such as gold and silver, so it does not have the "commercial nature" of a security. The court did not recognize the relational logic of XRP. Because the court held that even commodities can be sold in the form of investment contracts .

Many projects also claim that the project team's tokens are not securities, but utility tokens. However, from the perspective of the court, although they have functions, they do not prevent them from being recognized as securities .

summary

Unlike the one-sided "support" of Grayscale and Uniswap, although the judge took a more positive attitude towards the virtual market, the court still made some rulings that were favorable to the SEC. For example, the Howey Test should not be formalistic, and this ruling to a certain extent Comply with how the SEC defines securities. It is difficult for projects that claim their tokens are “utility” tokens to stand up in court.

What puzzles me about this judgment is that tokens sold to institutional investors are deemed securities because institutional investors are aware of the investment regulations and the source of the sales, while retail investors are "unclear." But the "original intent" of the securities was deemed to be investor protection, and retail investors did not get that. And according to this logic: If tokens are sold through an exchange, then securities laws do not apply. Can retail investors who purchase tokens on the trading platform not be protected?

Regulatory signals revealed by the judgment

There are some "unreasonable" aspects in several judgments, which demonstrate the bias of the judicial department towards the industry, and also highlight the characteristics of mutual checks and balances within the United States. In the past few years, the SEC has taken radical measures in an attempt to expand its "jurisdiction" regarding whether virtual currencies are securities. However, before the legislative branch has taken formal action, the judicial branch has begun to vigorously crack down on the executive branch's arrogance.

As an example specifically used by the SEC to issue a warning to the industry, Ripple has not succeeded in establishing authority, but has instead given the industry a great gift. As a country represented by case law, the judgment of "Ripple vs SEC" will give a clearer direction to the industry that lacks definitions and legislation in the future , especially pointing out that "programmed" sales of tokens do not belong to "securities" as defined by the SEC.

Although the Uniswap ruling has nothing to do with the SEC, it reveals the court's attitude: decentralized projects are different from ordinary companies, and tokens cannot be confused with company securities . The judge in the case, Katherine Failla, serves as the judge for the SEC and Coinbase cases. The market is also very optimistic that Coinbase will dismiss the SEC's lawsuit.

If the cases of Ripple and Uniswap are the judicial department's overture to the industry, then Grayscale's penalty is a blow to the SEC . With the overwhelming verdict of 3:0, both the Radical Party and the Conservative Party revealed their disappointment with the SEC .

The hearing held yesterday also sent a signal to the industry that the SEC's strong supervision will be restricted, and the legislative branch will follow closely to clarify the regulatory framework . Although supervision will not be completely relaxed, future law enforcement will be more "law-based." I believe that members of Congress will not give up this opportunity to promote their own ideas in the virtual currency industry and seize political capital. There will be a lot of ETF applications in October, and these applications have already put strong political pressure on the SEC. Combined with the recent "rising in the east and falling in the west" brought about the lull in the Permissionless conference, it is hammering the SEC. If it continues to take unreasonable measures Measures will be abandoned by popular sentiment and political resources.